TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

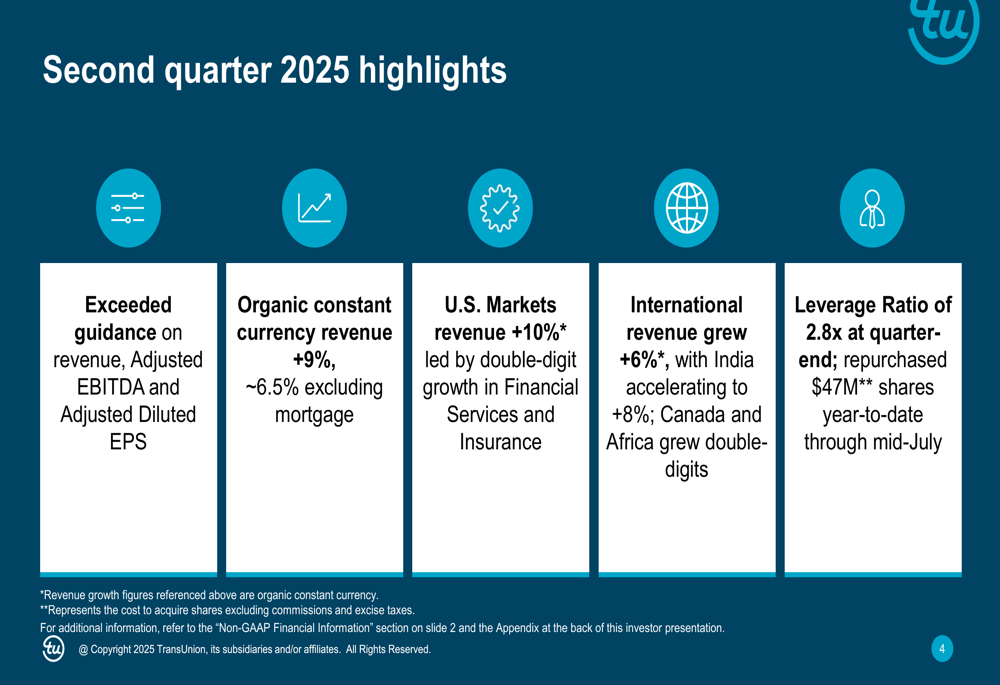

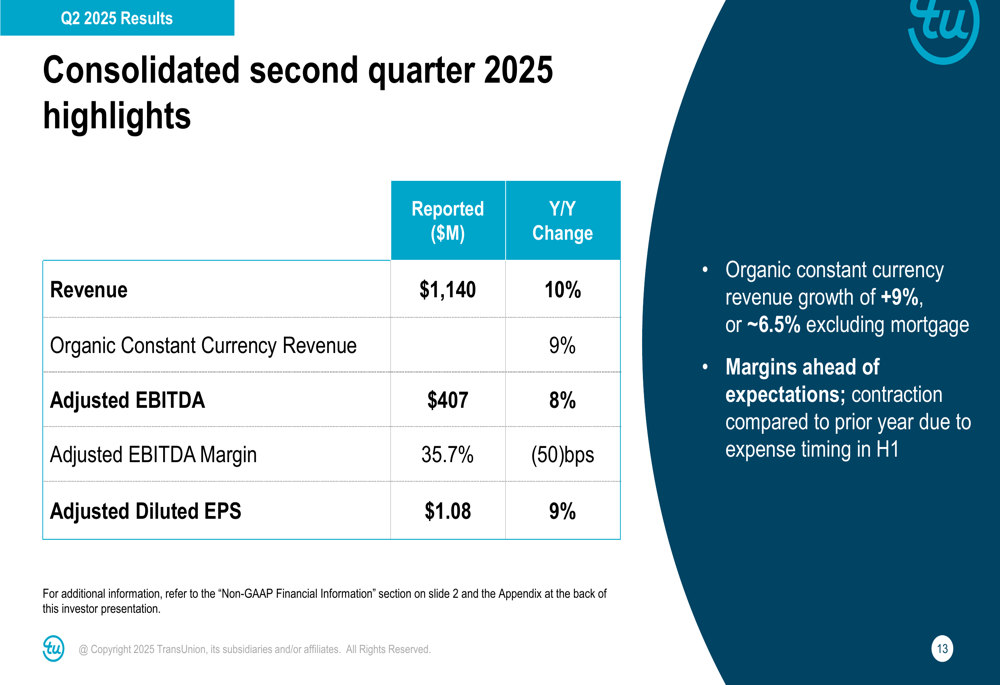

TransUnion (NYSE:TRU) reported strong second-quarter 2025 results on July 24, marking the seventh consecutive quarter of exceeding financial guidance. The credit reporting and information services company saw its stock rise 4.58% in pre-market trading to $98.90, building on the positive momentum established in Q1 when the company also beat expectations.

Against a backdrop of stable credit volumes and healthy consumer finances, TransUnion delivered solid growth across most business segments while highlighting its strategic focus on Trusted Call Solutions (TCS) as a key growth driver for the future.

Quarterly Performance Highlights

TransUnion reported Q2 2025 revenue of $1.140 billion, representing a 10% increase year-over-year. Organic constant currency revenue grew by 9%, or approximately 6.5% when excluding mortgage-related revenue.

The company’s adjusted EBITDA reached $407 million, up 8% compared to the same period last year, with an adjusted EBITDA margin of 35.7%, which was 50 basis points lower than the previous year but ahead of expectations. Adjusted diluted earnings per share came in at $1.08, representing a 9% year-over-year increase.

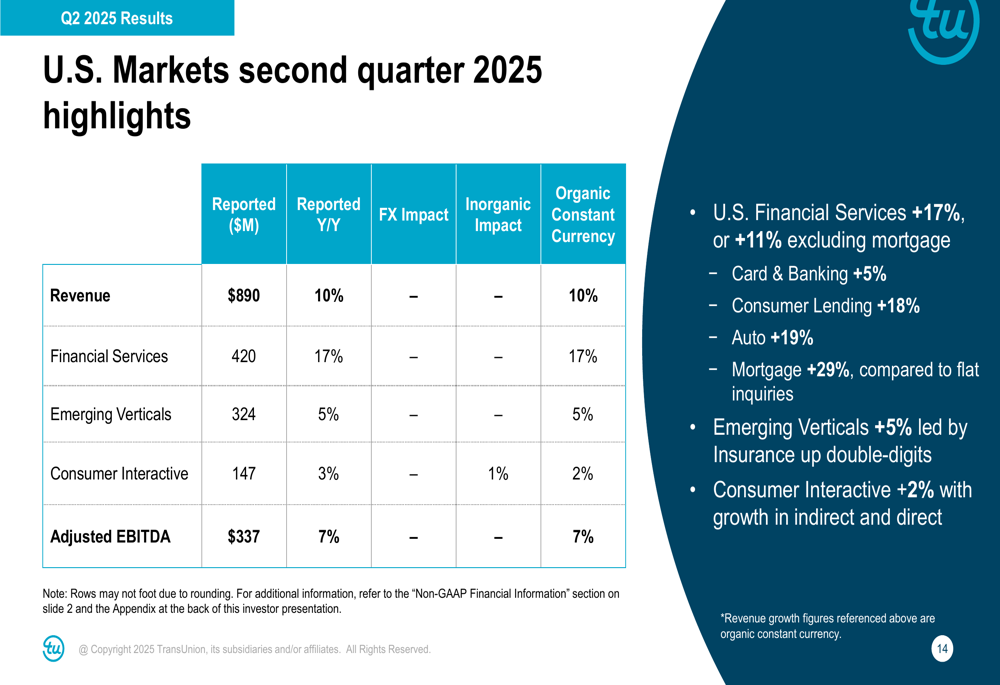

U.S. Markets, which accounts for the largest portion of TransUnion’s business, saw revenue increase by 10% to $890 million. Within this segment, Financial Services revenue grew by an impressive 17%, driven by strong performance in Consumer Lending (+18%), Auto (+19%), and Card & Banking (+5%). When excluding mortgage-related revenue, Financial Services still posted a robust 11% growth.

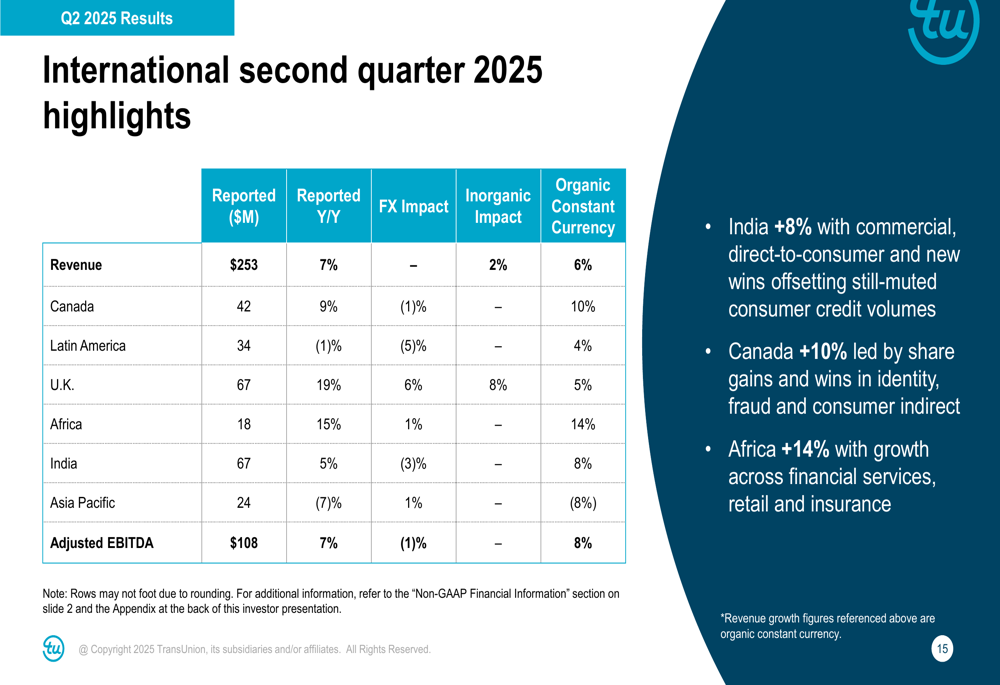

The International segment delivered 7% revenue growth, reaching $253 million, with organic constant currency growth of 6%. Particularly strong performance was seen in Canada (+10%), Africa (+14%), and India (+8% on a commercial basis). The U.K. showed 19% reported growth, translating to 5% organic constant currency growth.

Strategic Initiatives

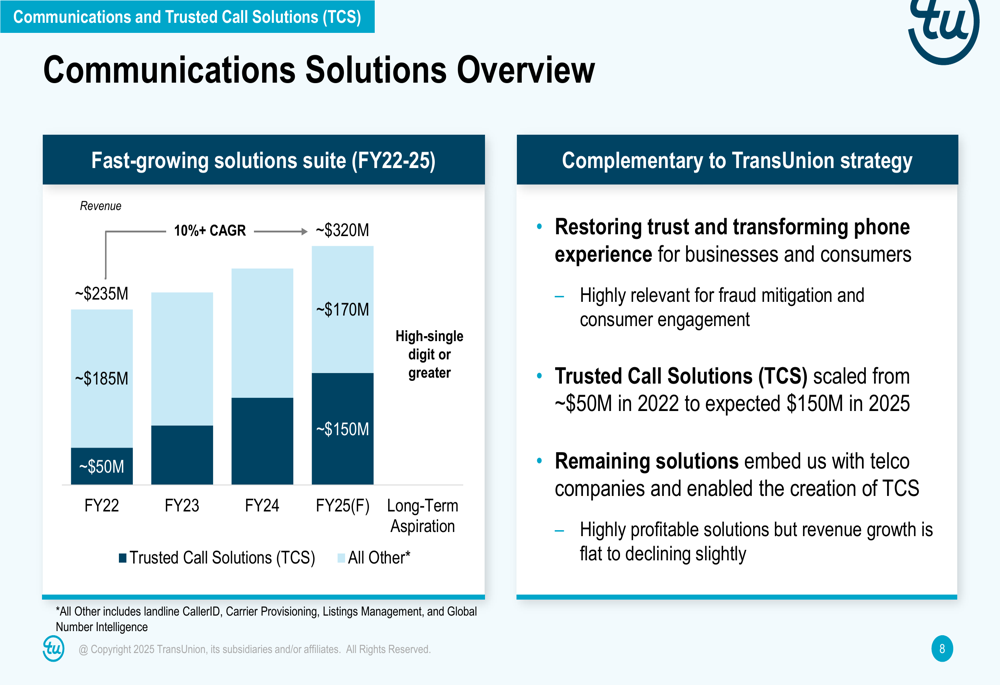

A significant portion of TransUnion’s presentation focused on its Trusted Call Solutions (TCS), which the company highlighted as a fast-growing solutions suite with a projected 10%+ CAGR from FY22-25. TCS is expected to grow from approximately $50 million in FY22 to $320 million, addressing what TransUnion identifies as a $1 billion+ addressable market.

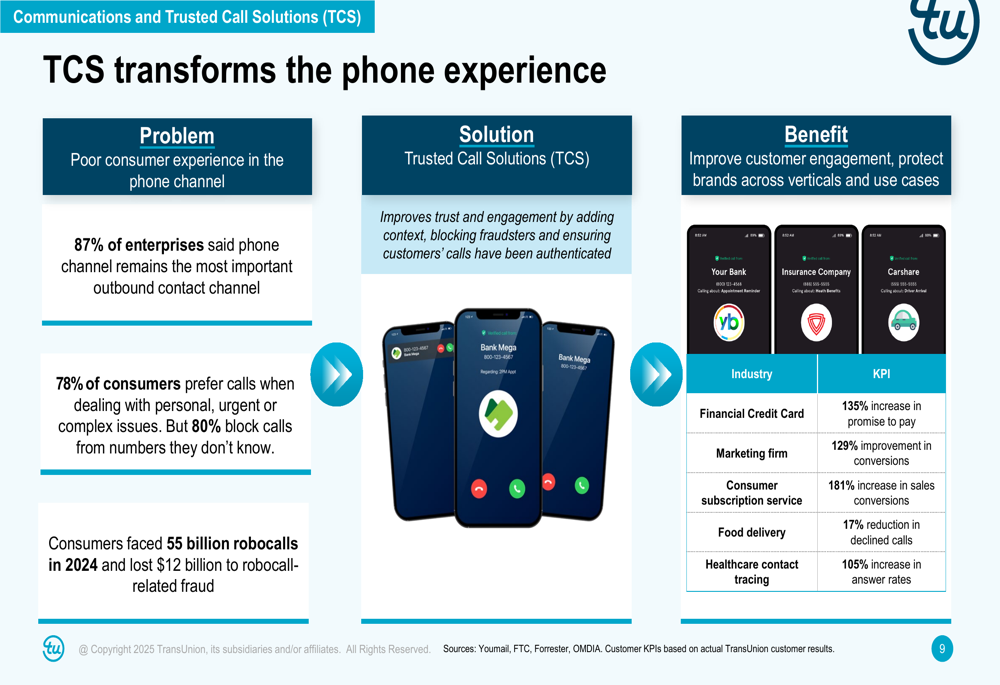

The company explained how TCS transforms the phone experience by addressing the problem of poor consumer engagement in the phone channel. While 87% of enterprises view phone as the most important outbound contact channel and 78% of consumers prefer calls for personal issues, 80% of consumers block calls from unknown numbers. TCS aims to improve trust and engagement through phone verification, with impressive results including a 135% increase in promised payments for financial credit cards and a 181% increase in sales conversions for consumer subscription services.

TransUnion’s 2025 strategic priorities also include completing technology modernizations, enhancing its global operating model, and accelerating innovation across solution suites. The company reported progress in strengthening credit functionality on its OneTru platform, migrating key customers, and expanding use cases for OneTru Assist.

Financial Health and Capital Allocation

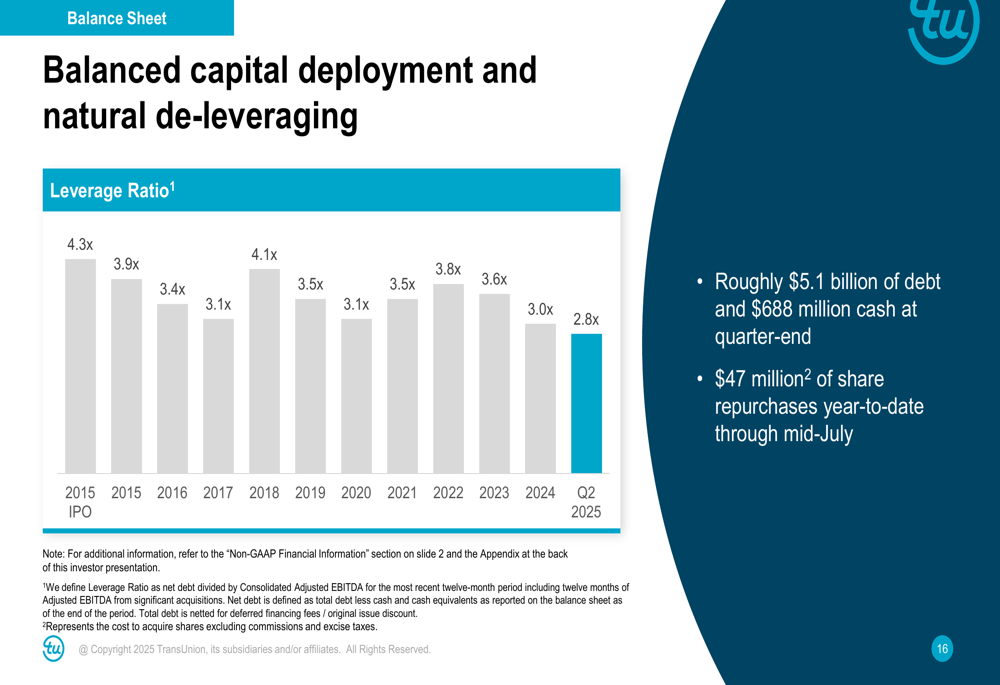

TransUnion continues to strengthen its financial position, with its leverage ratio decreasing to 2.8x at the end of Q2 2025, down significantly from 4.3x at the time of its IPO. The company reported approximately $5.1 billion of debt and $688 million of cash at quarter-end, along with approximately $47 million of share repurchases year-to-date through mid-July.

Forward-Looking Statements

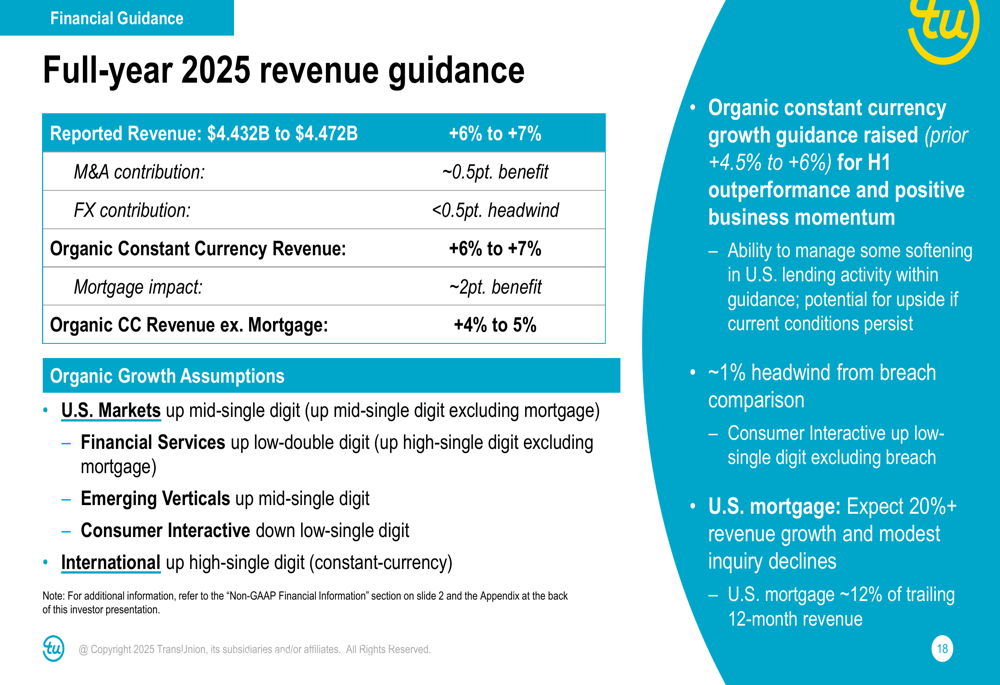

Based on its strong first-half performance, TransUnion raised its full-year 2025 guidance. The company now expects reported revenue between $4.432 billion and $4.472 billion, representing 6% to 7% growth, with organic constant currency growth also projected at 6% to 7%. Excluding mortgage-related revenue, organic constant currency growth is expected to be 4% to 5%.

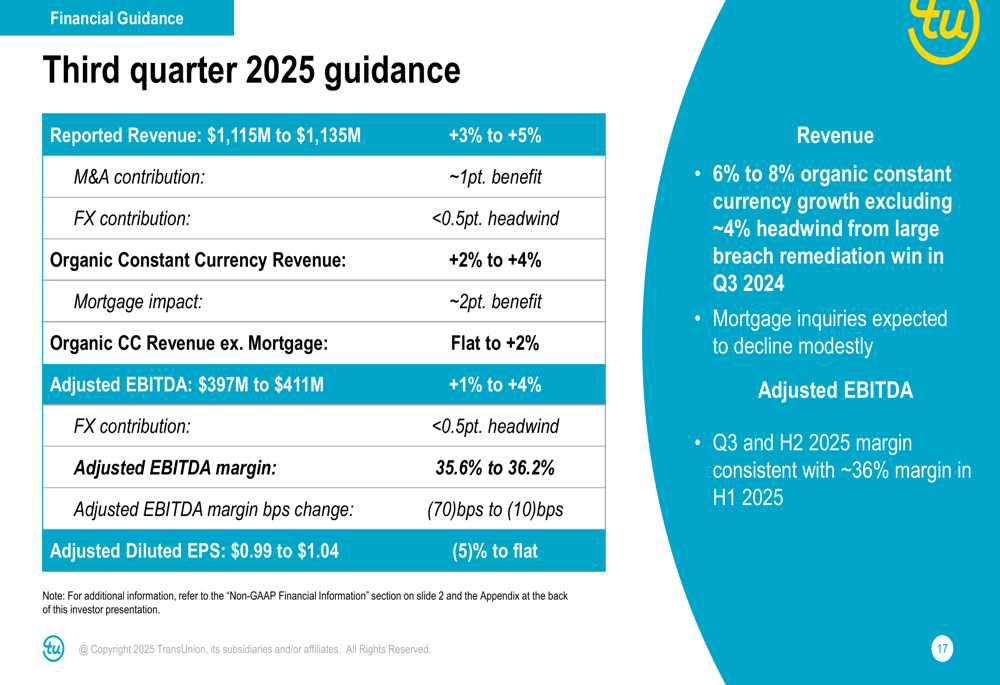

For the third quarter of 2025, TransUnion projects reported revenue between $1.115 billion and $1.135 billion (3% to 5% growth), with organic constant currency revenue growth between 2% and 4%. Adjusted EBITDA is expected to be between $397 million and $411 million (1% to 4% growth), with an adjusted EBITDA margin of approximately 36%. Adjusted diluted EPS is projected to be between $0.99 and $1.04.

The company also raised its adjusted EBITDA guidance for the full year to between $1.580 billion and $1.610 billion, with adjusted diluted EPS now expected to be between $4.03 and $4.14.

Market Perspectives

TransUnion’s presentation included insights on market conditions, noting that U.S. credit volumes are stable and modestly better than anticipated in Q2. The company highlighted that consumer finances remain healthy, supported by low unemployment, modest real wage growth, and manageable inflation. Lenders are described as well-positioned with strong earnings, adequate capital, and good credit performance.

While the company acknowledged improving clarity on U.S. trade and fiscal policies, it also noted ongoing risks around inflation, interest rates, employment, and economic growth. The raised full-year guidance reflects both first-half outperformance and what TransUnion describes as "prudent conservatism given ongoing market uncertainty."

Conclusion

TransUnion’s Q2 2025 results demonstrate continued momentum across most business segments, with particularly strong performance in U.S. Financial Services and key international markets. The company’s strategic focus on Trusted Call Solutions positions it to capture growth in a significant addressable market, while ongoing de-leveraging efforts strengthen its financial foundation.

With raised guidance for the full year and a clear strategic direction, TransUnion appears well-positioned to navigate market uncertainties while delivering continued growth. The positive pre-market stock reaction suggests investors are responding favorably to both the quarterly results and the company’s forward outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.