Crispr Therapeutics shares tumble after significant earnings miss

Introduction & Market Context

TriMas Corporation (NASDAQ:TRS) shares surged 10.77% to $23.25 on Tuesday after the diversified manufacturer presented its first quarter 2025 results, showcasing strong growth across key metrics. The company, which operates in packaging, aerospace, and specialty products segments, reported significant improvements in sales, margins, and profitability, marking a substantial turnaround from the previous quarter when its stock had fallen despite beating expectations.

The positive market reaction reflects investor confidence in TriMas’s strategic positioning and its ability to navigate global market challenges, particularly in managing tariff impacts while capitalizing on strong aerospace demand.

Quarterly Performance Highlights

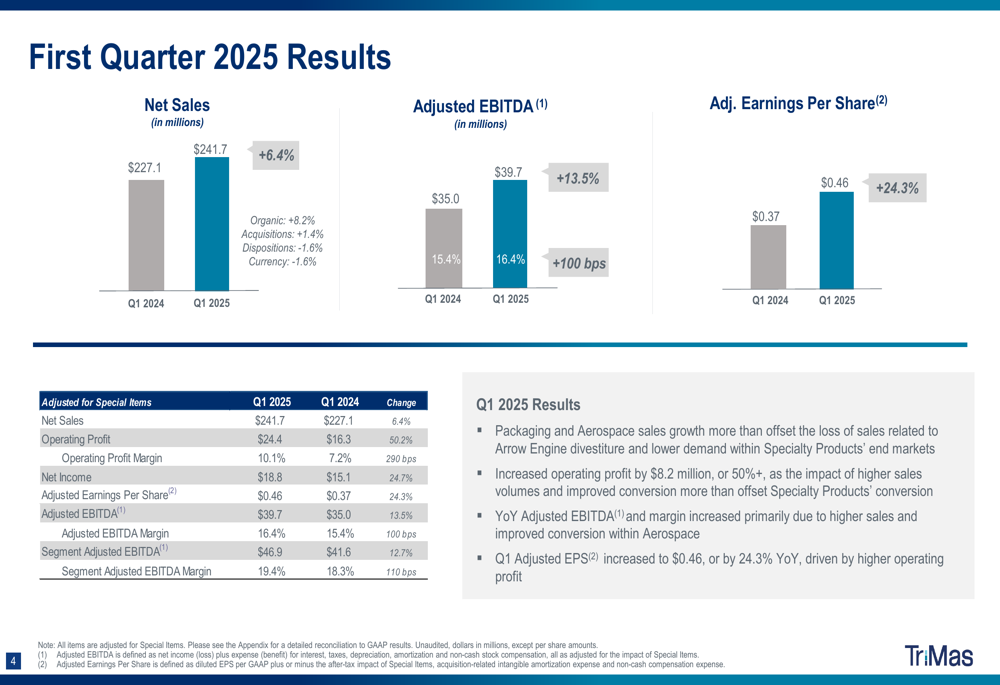

TriMas reported consolidated sales of $241.7 million for Q1 2025, representing a 6.4% increase compared to the same period last year. More impressively, the company’s operating profit surged 50.2% to $24.4 million, while adjusted EBITDA grew 13.5% to $39.7 million with a margin of 16.4% - a 100 basis point improvement year-over-year.

As shown in the following chart comparing Q1 2024 and Q1 2025 performance:

Adjusted earnings per share increased 24.3% to $0.46, significantly outpacing sales growth and indicating improved operational efficiency. Net income more than doubled from $5.1 million in Q1 2024 to $12.4 million in Q1 2025, with diluted EPS reaching $0.30 compared to $0.12 in the prior year period.

The company attributed these strong results to higher sales volumes and improved conversion rates, particularly in the Aerospace segment, which offset challenges in the Specialty Products segment.

Segment Analysis

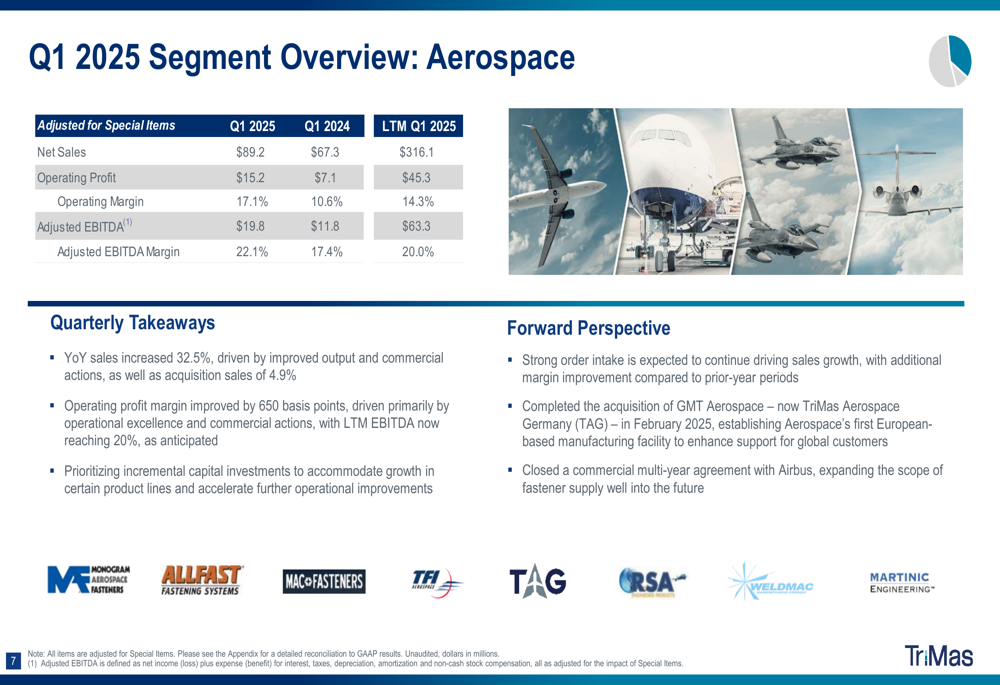

Aerospace: Record Performance

The Aerospace segment delivered exceptional results, achieving record quarterly sales of $89.2 million, a 32.5% increase year-over-year. Operating profit in this segment reached $15.2 million with a 17.1% margin, while adjusted EBITDA hit $19.8 million with an impressive 22.1% margin.

The segment’s performance details and outlook are illustrated below:

Key drivers included improved output, effective commercial actions, and contribution from acquisitions (4.9% of growth). The operating profit margin improved by 650 basis points, demonstrating significant operational leverage. The company highlighted strong order intake and backlog, which positions the segment well for continued growth. The recent acquisition of GMT Aerospace and a new multi-year agreement with Airbus further strengthen this segment’s outlook.

Packaging (NYSE:PKG): Steady Growth Amid Tariff Challenges

The Packaging segment, which represents the largest portion of TriMas’s business, delivered organic sales growth of 3.3% (adjusted for currency) to reach $127.6 million. Operating profit was $17.8 million with a 14.0% margin, while adjusted EBITDA reached $26.2 million with a 20.5% margin.

The segment saw strong demand in beauty & personal care, home care, and industrial end markets, partially offset by lower demand in food & beverage. Margin was slightly down due to freight charges, but the company reported commercial gains with consumer packaged goods and life sciences customers.

TriMas is actively managing tariff dynamics in this segment, including moving to a new manufacturing facility in Vietnam, which appears to be a strategic response to potential tariff impacts from China-based production.

Specialty Products: Ongoing Challenges

The Specialty Products segment continued to face headwinds, with sales of $24.9 million and minimal operating profit of $0.1 million (0.4% margin). Adjusted EBITDA was $0.9 million with a 3.7% margin.

The segment’s performance was negatively impacted by the Arrow Engine divestiture and reduced demand for Norris Cylinder products. However, management noted improving order intake and is focused on managing through the current tariff environment while collaborating with suppliers and customers to improve results.

Balance Sheet & Cash Flow

TriMas maintained a solid financial position with total debt of $434.2 million and cash of $32.7 million, resulting in net debt of $401.5 million and a net leverage ratio of 2.7x. The company generated quarterly free cash flow of $0.6 million, an improvement from the previous year.

The company emphasized its strong balance sheet, backed by low-interest, long-term debt with no maturities until 2029. The increase in net debt was primarily attributed to the GMT Aerospace acquisition, while the year-over-year improvement in free cash flow resulted from enhanced performance and disciplined working capital management.

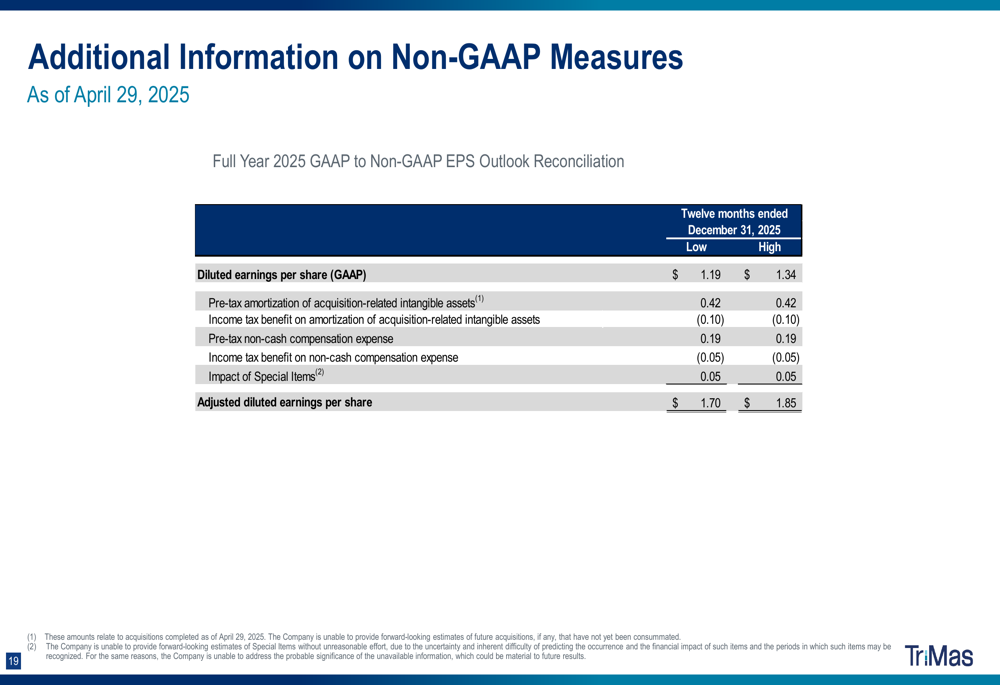

As illustrated in the detailed reconciliation of the company’s non-GAAP financial measures:

Forward-Looking Statements

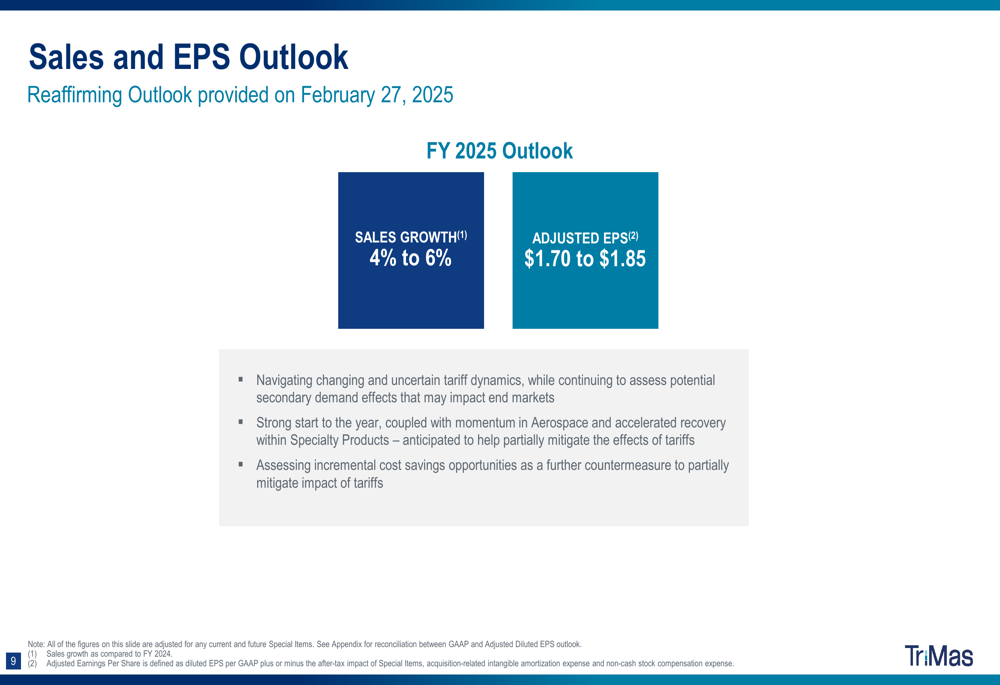

TriMas reaffirmed its full-year 2025 outlook, projecting sales growth between 4% and 6%, with adjusted EPS expected to range from $1.70 to $1.85. This guidance is consistent with the outlook provided in the previous quarter.

The company’s forward perspective includes:

Management highlighted several key factors supporting this outlook, including navigating changing tariff dynamics, the strong start to the year in the Aerospace segment, an accelerated recovery within Specialty Products, and ongoing assessment of incremental cost-saving opportunities.

The company appears well-positioned to continue its growth trajectory, particularly through its Aerospace segment, while actively addressing challenges in its other business units. The market’s strongly positive reaction to this quarter’s results suggests investor confidence in TriMas’s strategic direction and execution capabilities, representing a significant turnaround from the previous quarter’s stock performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.