5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

TTM Technologies Inc (NASDAQ:TTMI) presented its second quarter 2025 earnings results on July 30, showcasing strong financial performance that exceeded guidance across key metrics. Despite the robust results, the company’s stock fell 3.66% in premarket trading, reflecting investor caution about future growth prospects.

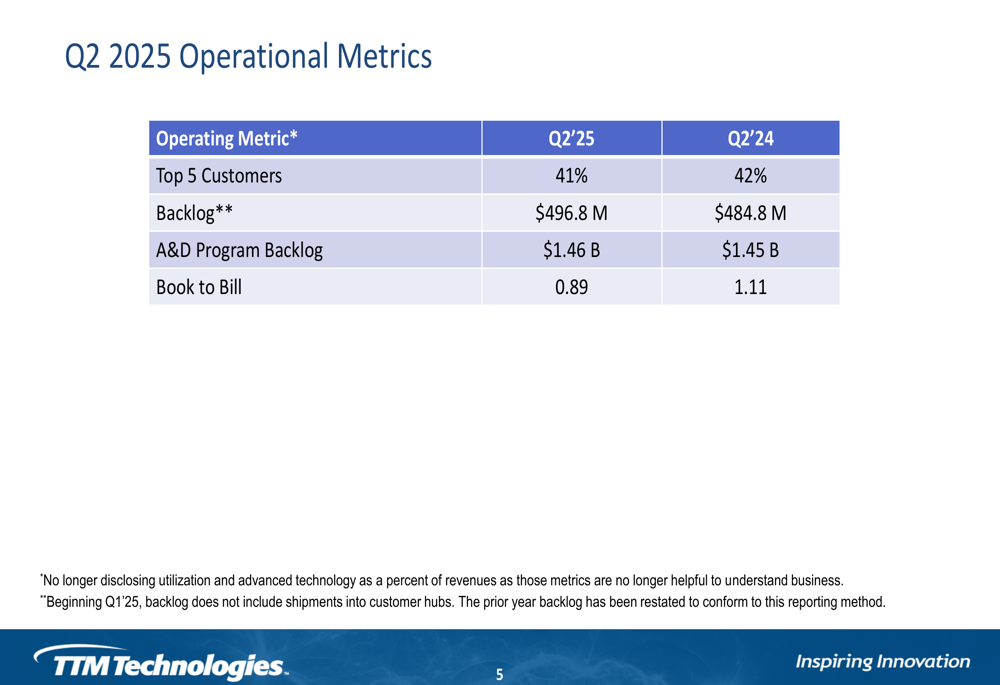

The printed circuit board manufacturer reported significant year-over-year improvements in revenue, margins, and earnings per share, driven primarily by strength in its Aerospace & Defense and Networking segments. However, a declining book-to-bill ratio of 0.89 (compared to 1.11 in Q2 2024) suggests potential moderation in near-term growth momentum.

Quarterly Performance Highlights

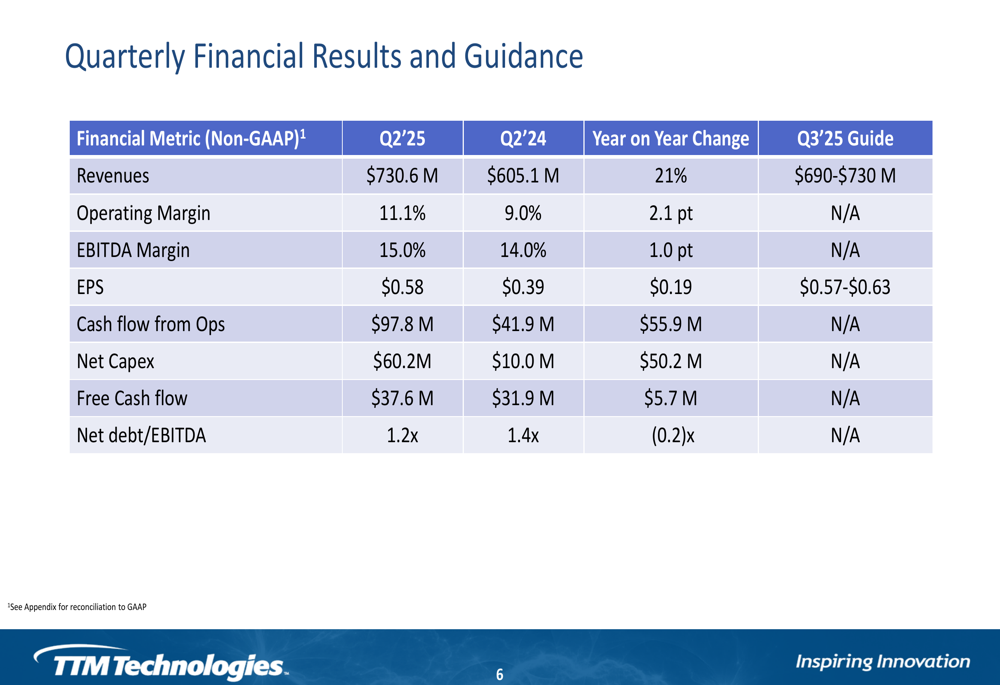

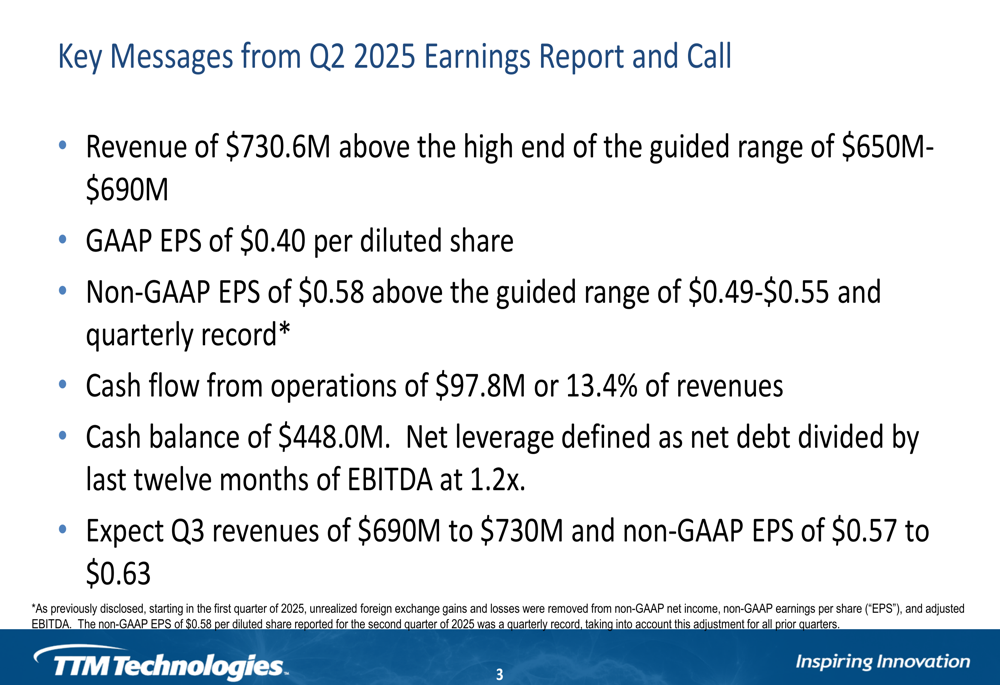

TTM Technologies delivered Q2 2025 revenue of $730.6 million, exceeding its guided range of $650-$690 million and representing a 21% increase from the $605.1 million reported in the same period last year. The company achieved a GAAP EPS of $0.40 per diluted share and a record non-GAAP EPS of $0.58, surpassing the guided range of $0.49-$0.55.

As shown in the following quarterly financial results:

Operating margin improved to 11.1%, up 2.1 percentage points year-over-year, while EBITDA margin increased to 15.0% from 14.0% in Q2 2024. Cash flow from operations reached $97.8 million or 13.4% of revenues, compared to $41.9 million in the prior year period. Free cash flow was $37.6 million, up from $31.9 million, despite a significant increase in capital expenditures to $60.2 million from $10.0 million a year ago.

The company’s key messages from the earnings report highlight these strong results:

End Market Analysis

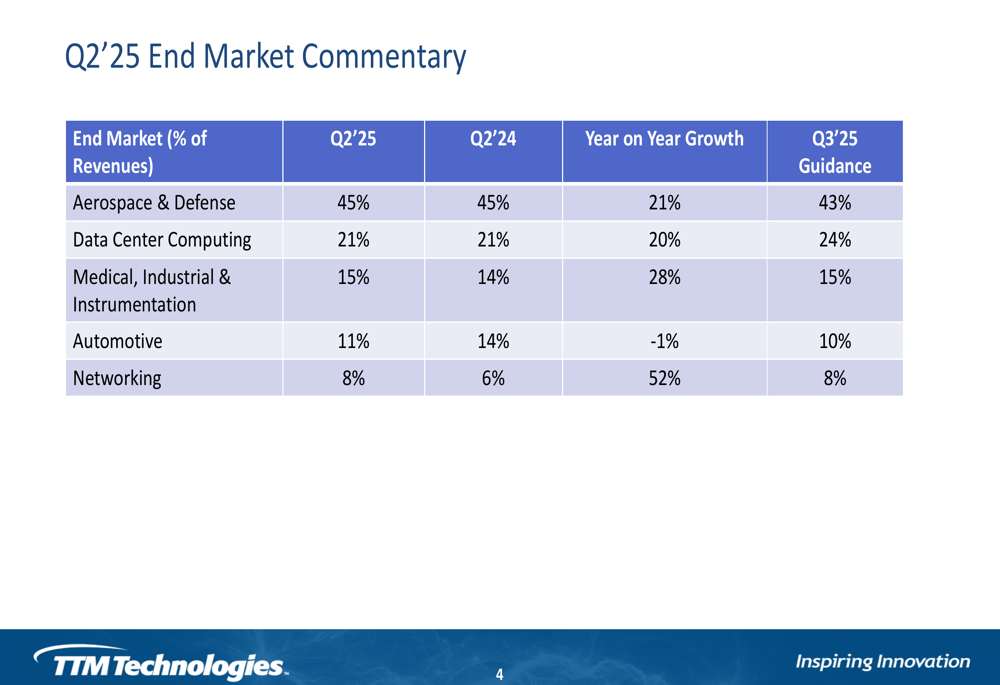

TTM’s performance across its five end markets showed robust growth in four segments, with only the Automotive sector experiencing a slight decline. The company’s revenue diversification strategy appears to be succeeding, with growth in multiple sectors contributing to overall performance.

The following table breaks down TTM’s revenue by end market, showing year-over-year growth and Q3 2025 guidance:

Aerospace & Defense remained TTM’s largest segment at 45% of total revenue, growing 21% year-over-year. The company reported an A&D program backlog of $1.46 billion, slightly up from $1.45 billion in Q2 2024, indicating continued demand stability in this sector.

The Networking segment delivered the strongest growth at 52% year-over-year, while Medical, Industrial & Instrumentation grew 28% and Data Center Computing increased 20%. The Automotive segment was the only underperformer, declining 1% compared to the previous year and projected to decrease as a percentage of revenue in Q3 2025.

Financial Position and Outlook

TTM Technologies maintained a solid financial position with a cash balance of $448.0 million and improved its net leverage ratio to 1.2x, down from 1.4x in Q2 2024. The company’s operational metrics showed stability in customer concentration, with its top five customers representing 41% of revenue compared to 42% a year ago.

The operational metrics table provides additional insights into TTM’s performance:

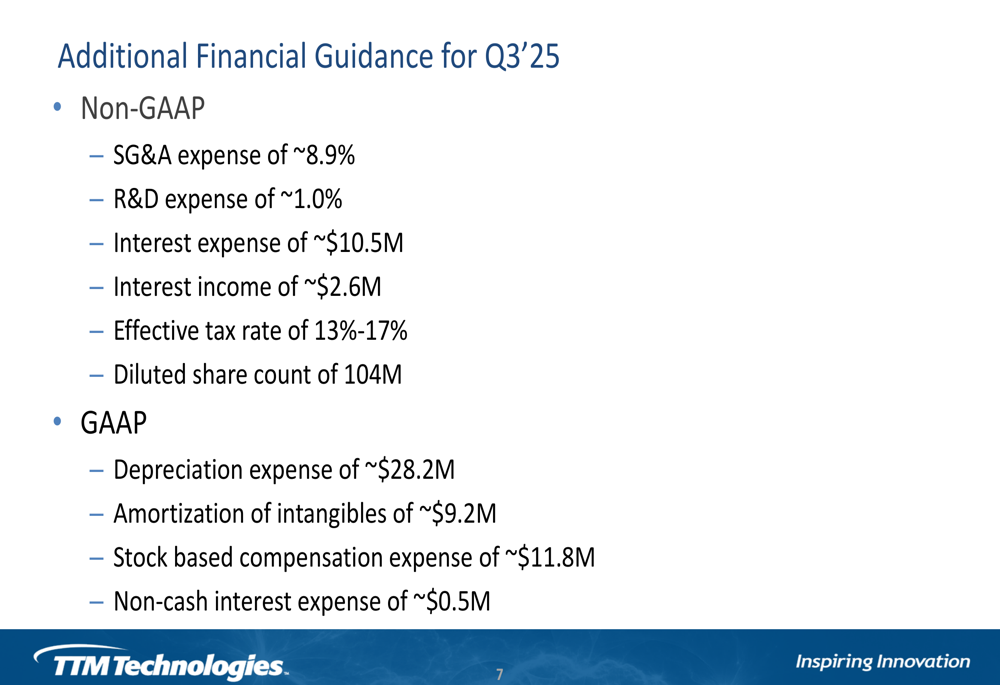

For the third quarter of 2025, TTM expects revenues between $690 million and $730 million and non-GAAP EPS of $0.57 to $0.63. The company provided detailed additional guidance for Q3:

Strategic Initiatives and Challenges

According to the earnings call transcript, TTM is focusing on expanding its manufacturing footprint, with ongoing investments in a new facility in Wisconsin and continued ramp-up of its Penang facility. CEO Tom Edmond highlighted growing interest from companies looking to invest in new facilities in the U.S., particularly for generative AI applications, underscoring the strategic importance of the company’s Eau Claire facility.

Despite the positive quarterly results, TTM faces several challenges. The declining book-to-bill ratio of 0.89 suggests potential softening in order momentum. Additionally, the company is navigating the complexities of supply chain diversification and managing potentially higher manufacturing costs in the U.S. compared to other regions.

The slower-than-expected ramp-up of the Penang facility, mentioned in the earnings call, could impact future growth if delays persist. However, TTM’s strong position in the Aerospace & Defense sector, which contributes nearly half of its revenue, provides a stable foundation as the company addresses these challenges.

While TTM delivered impressive results for Q2 2025, the market’s cautious reaction suggests investors are weighing the company’s strong current performance against indicators of potential future growth moderation. The company’s strategic expansions and diversified end-market exposure position it to navigate changing market conditions, but execution of its facility ramp-ups will be crucial to maintaining growth momentum in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.