ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Twilio Inc. (NYSE:TWLO) presented its third-quarter 2025 earnings results on October 30, 2025, showcasing accelerating revenue growth and raised guidance for the full year. Despite beating earnings expectations with EPS of $1.25 versus the forecasted $1.08, Twilio's stock experienced a slight decline of 0.62% in aftermarket trading, closing at $110.92.

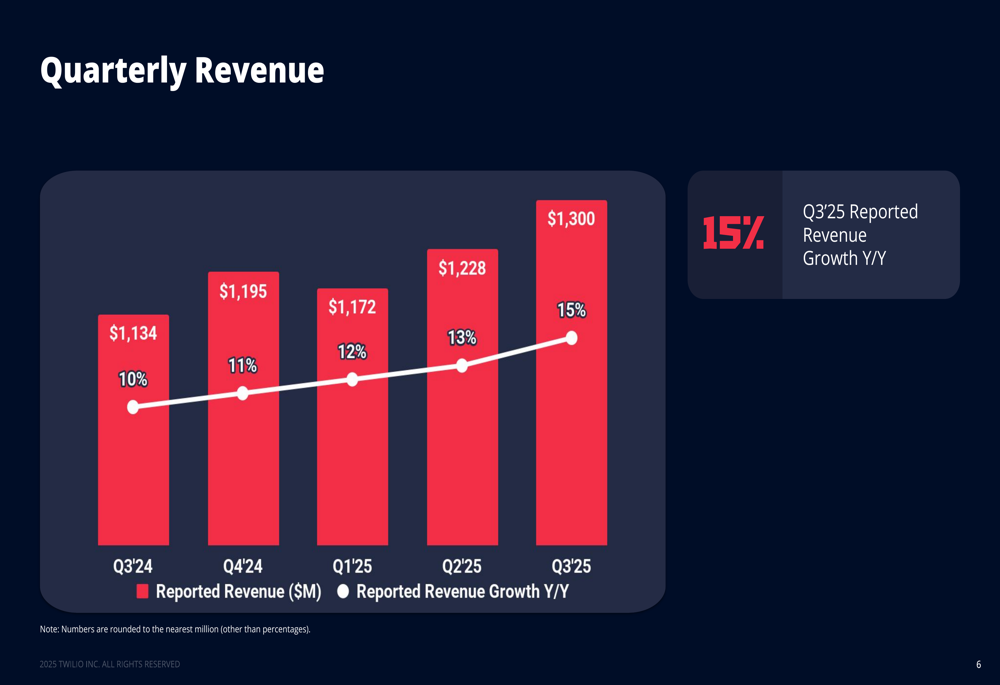

The cloud communications platform provider reported $1.3 billion in revenue, representing a 15% year-over-year increase, exceeding analyst expectations of $1.25 billion. The company continues to expand its customer base, which now exceeds 392,000 active accounts.

Quarterly Performance Highlights

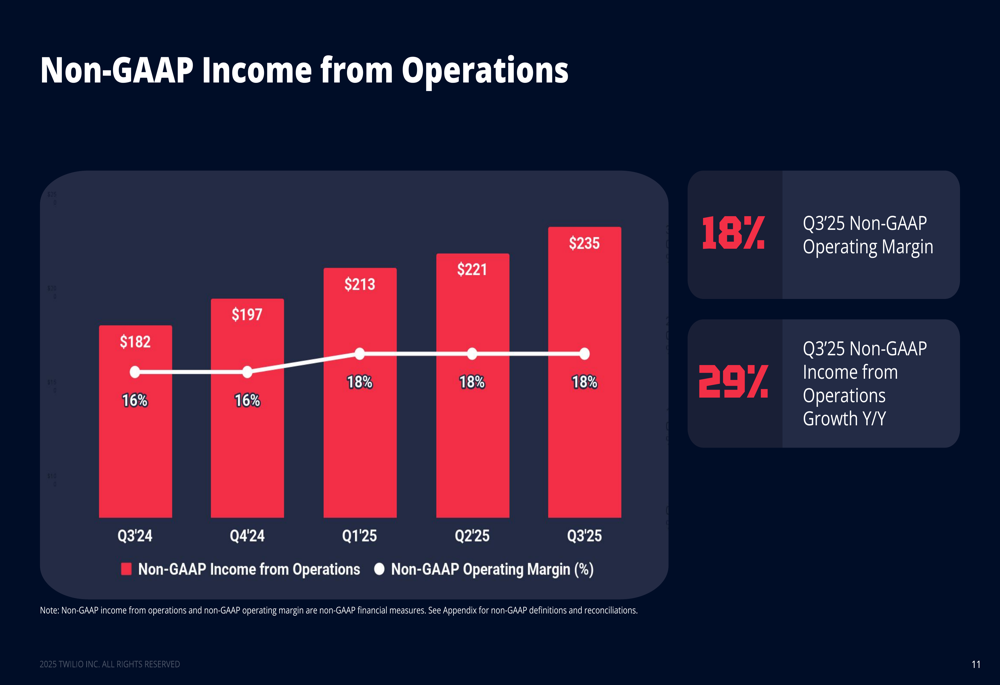

Twilio's Q3 2025 results demonstrated solid performance across key metrics. Revenue reached $1.3 billion, reflecting 15% reported growth and 13% organic growth year-over-year. The company achieved a non-GAAP income from operations of $235 million, representing a 29% increase from the same period last year.

As shown in the following chart of quarterly revenue growth:

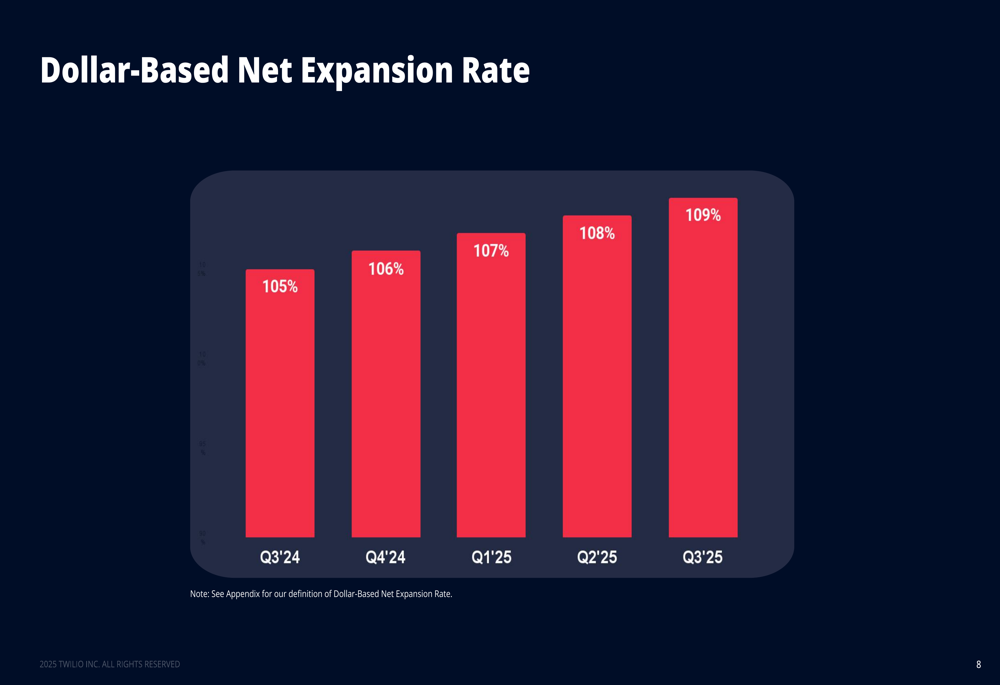

The Dollar-Based Net Expansion Rate, which measures increased spending from existing customers, continued its upward trajectory, reaching 109% in Q3 2025 compared to 105% a year earlier. This metric indicates Twilio's success in expanding relationships with existing customers.

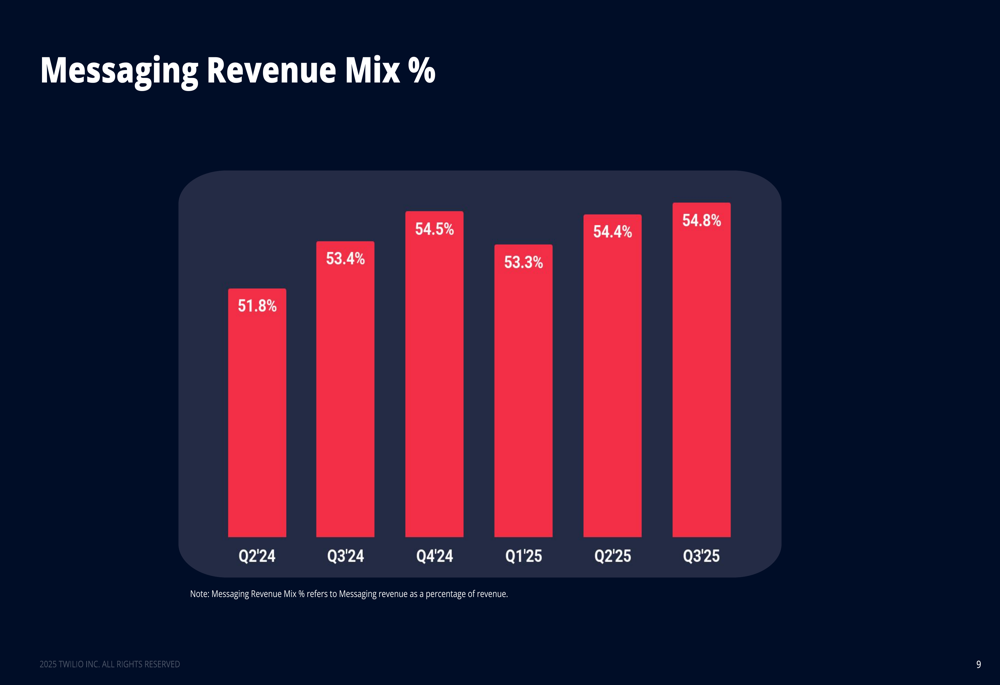

Twilio's messaging services continue to be the primary revenue driver, accounting for 54.8% of total revenue in Q3 2025, up from 53.4% in the same quarter last year.

Detailed Financial Analysis

While Twilio's revenue growth has been impressive, the company has experienced some margin pressure. Non-GAAP gross margin stood at 50.1% in Q3 2025, down from 53% in Q3 2024. This represents a 290 basis point decline year-over-year, though the company's gross profit in absolute terms grew by 9% to $652 million.

The following chart illustrates this trend:

On the operational front, Twilio has shown significant improvement. Non-GAAP operating margin held steady at 18% for the third consecutive quarter, while non-GAAP income from operations grew by 29% year-over-year to $235 million.

The company has made substantial progress in GAAP profitability as well, with GAAP income from operations reaching $41 million (3% margin) in Q3 2025, compared to a loss of $5 million in Q3 2024.

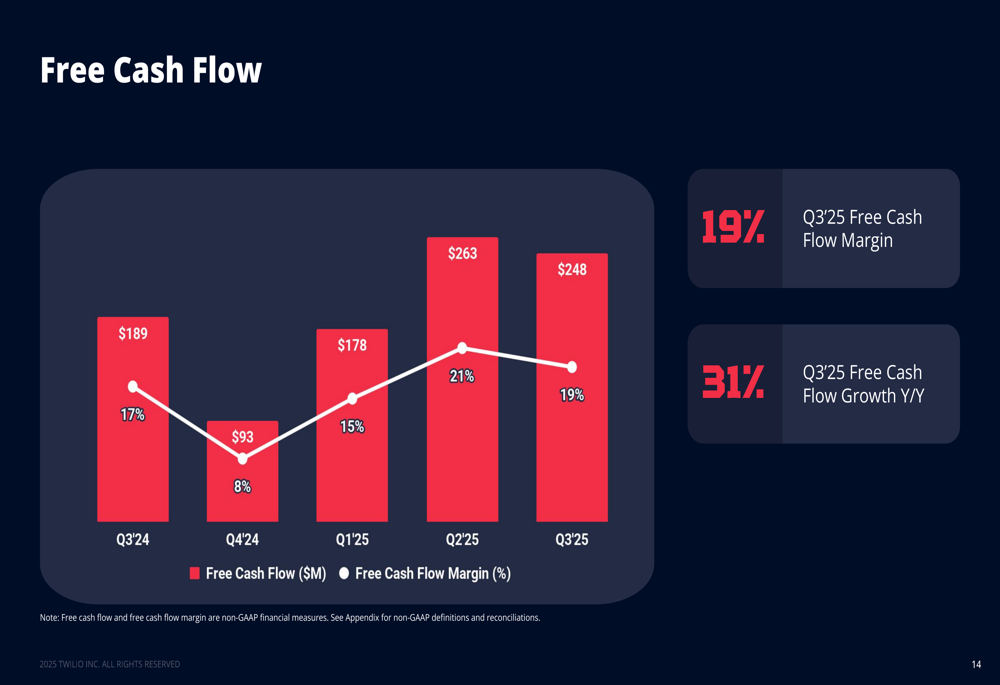

Free cash flow performance has been particularly strong, reaching $248 million in Q3 2025, a 31% increase year-over-year. Free cash flow margin stood at 19%, demonstrating Twilio's improving operational efficiency and cash generation capabilities.

Twilio has also made progress in reducing stock-based compensation as a percentage of revenue, which decreased to 12% in Q3 2025 from 14% in Q3 2024.

Strategic Initiatives

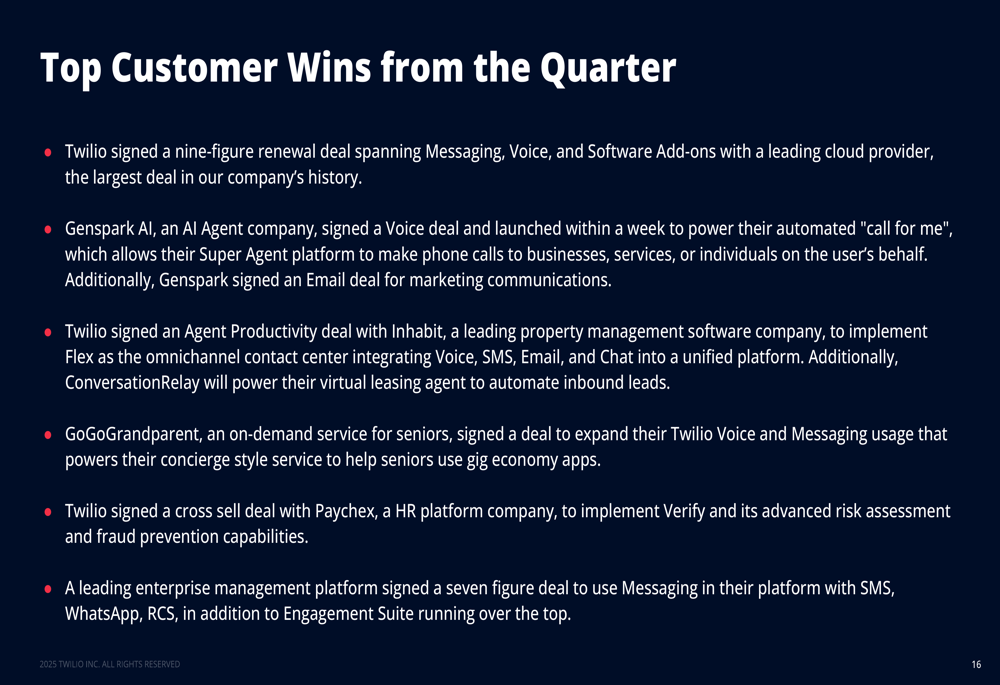

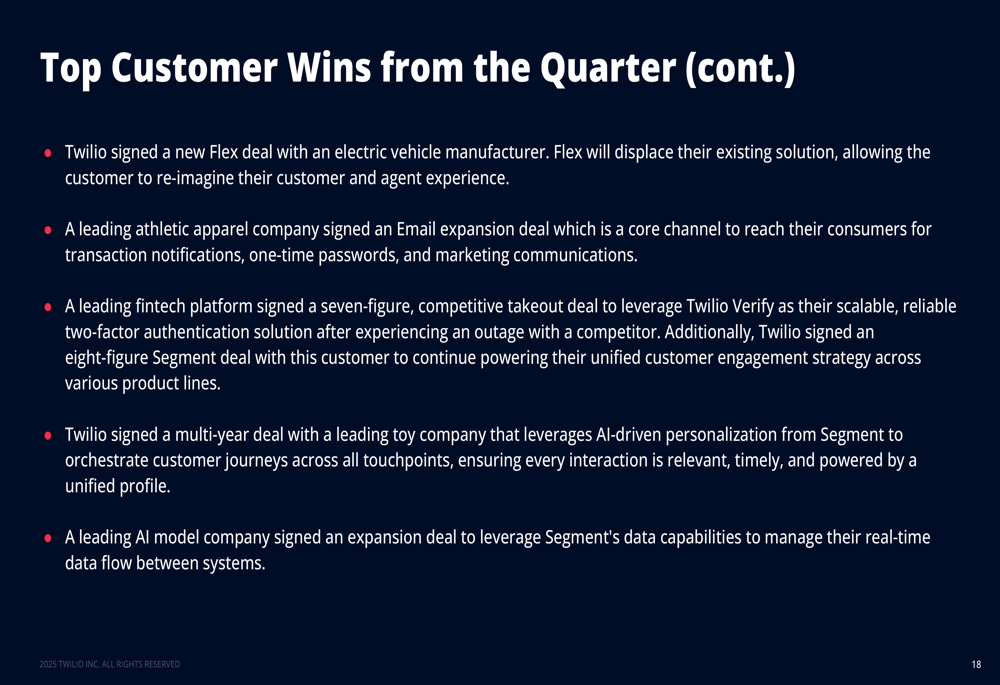

Twilio highlighted numerous customer wins during the quarter across various sectors, demonstrating the company's broad market appeal. Notable deals included:

- A nine-figure renewal with a leading cloud provider spanning Messaging, Voice, and Software Add-ons

- New deals with AI companies in healthcare, mortgage, and model development

- An eight-figure deal with a leading real estate technology platform

- Cross-sell successes with companies like Paychex

- International expansion with a large Argentinian bank

The company's ability to secure deals across diverse industries and geographies underscores its strong competitive position in the communications platform-as-a-service (CPaaS) market.

Twilio's focus on cross-selling multiple products was evident in several deals mentioned during the presentation:

Forward-Looking Statements

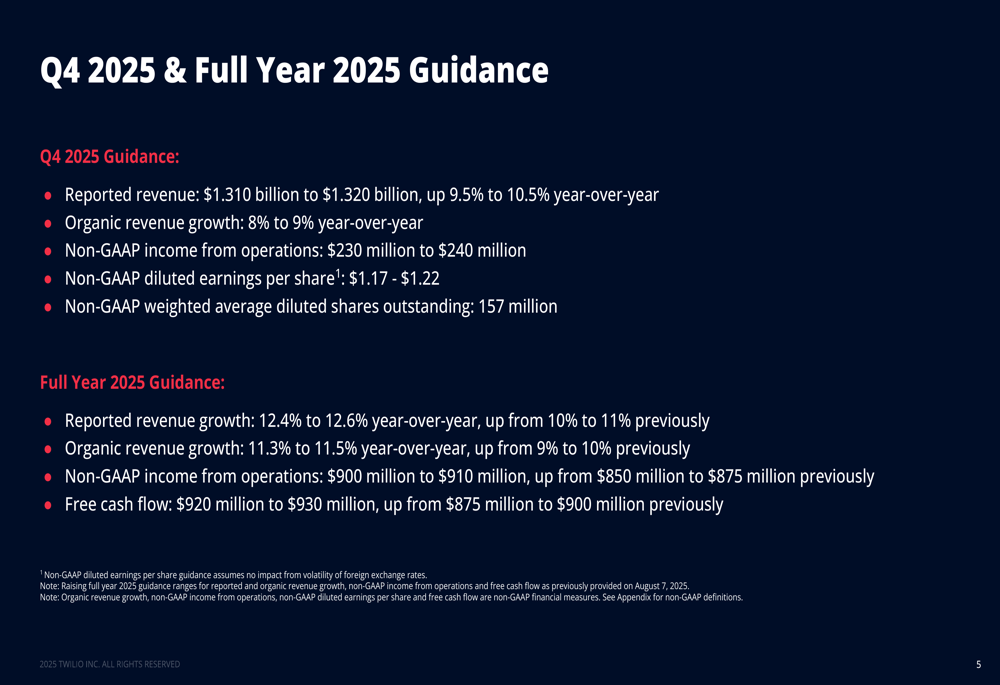

Twilio raised its full-year 2025 guidance, reflecting confidence in continued strong performance. The company now expects:

- Full-year reported revenue growth of 12.4% to 12.6% (up from previous guidance of 10% to 11%)

- Organic revenue growth of 11.3% to 11.5% (up from 9% to 10%)

- Non-GAAP income from operations of $900 million to $910 million (up from $850-$875 million)

- Free cash flow of $920 million to $930 million (up from $875-$900 million)

For the fourth quarter of 2025, Twilio projects:

- Revenue between $1.31 billion and $1.32 billion (9.5% to 10.5% year-over-year growth)

- Organic revenue growth of 8% to 9%

- Non-GAAP income from operations of $230 million to $240 million

- Non-GAAP diluted EPS of $1.17 to $1.22

The detailed guidance is presented in the following slide:

While Q4 revenue growth is projected to slow compared to Q3, the raised full-year guidance suggests management's confidence in the company's overall trajectory. CEO Khozema Shipchandler emphasized Twilio's potential to be "the customer experience layer of the internet," highlighting the company's strategic focus on AI and international expansion.

Despite the strong quarterly performance and raised guidance, investors reacted cautiously, possibly due to the projected growth deceleration in Q4 and ongoing margin pressure. However, with the stock trading well above its 52-week low of $77.51, the market appears to maintain overall confidence in Twilio's long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.