EU and US could reach trade deal this weekend - Reuters

Executive Summary

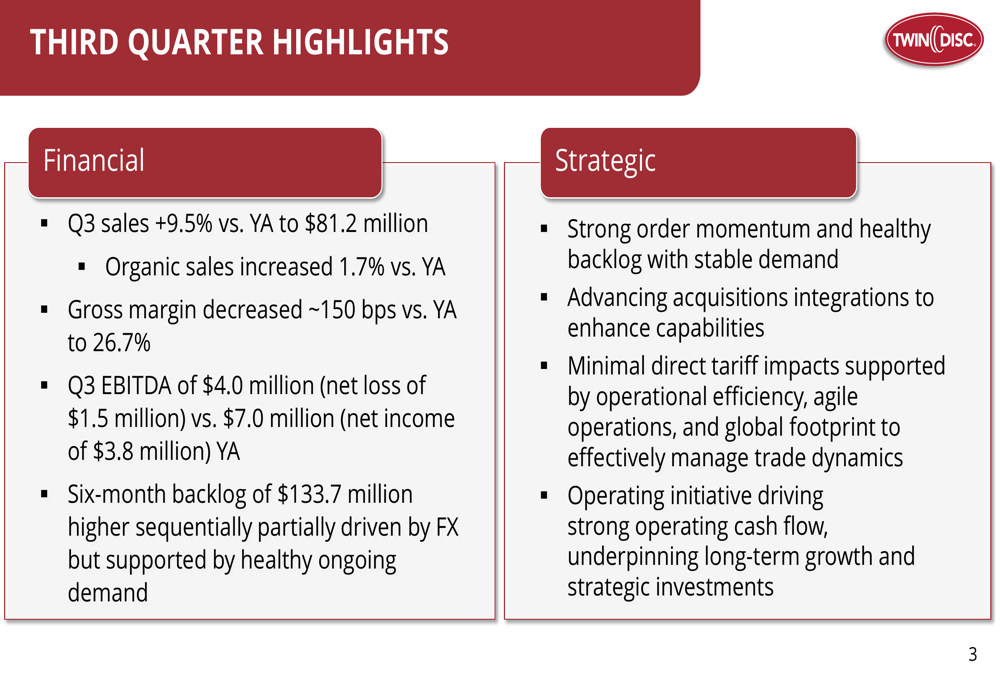

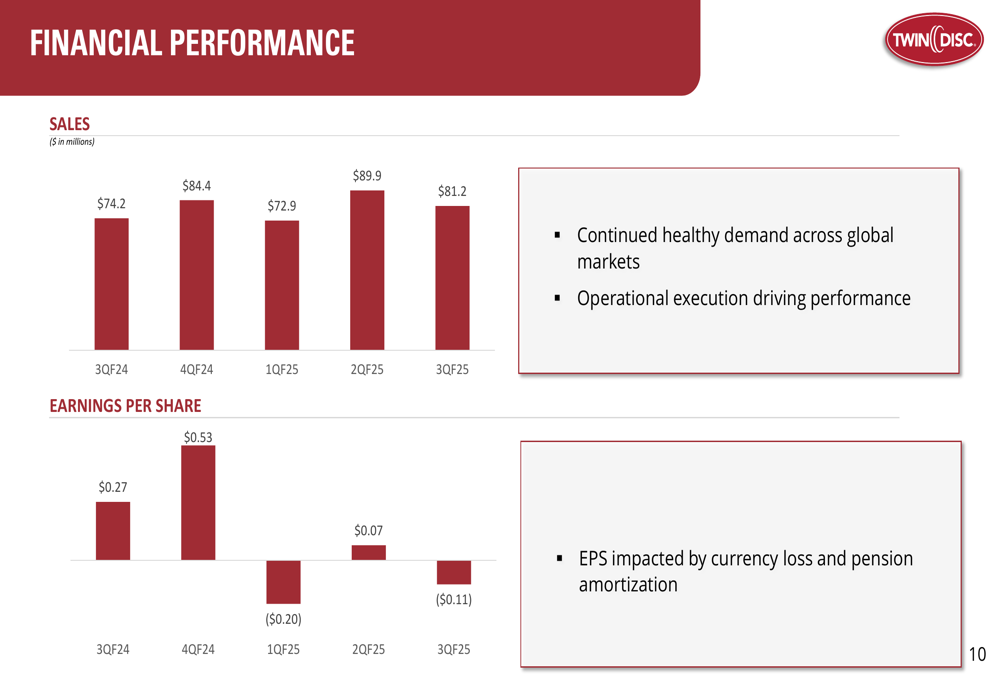

Twin Disc , Inc. (NASDAQ:TWIN) reported a 9.5% year-over-year increase in sales to $81.2 million for its third quarter of fiscal year 2025, according to the company’s investor presentation released on May 7, 2025. Despite the revenue growth, the power transmission technology provider posted a net loss of $1.5 million, or $(0.11) per share, compared to net income of $3.8 million, or $0.27 per share, in the same quarter last year.

The company’s shares responded positively to the results, rising 4.99% to $7.16 in after-hours trading, suggesting investors may be focusing on the company’s continued backlog growth and strategic positioning rather than the short-term profitability challenges.

As shown in the following quarterly performance highlights, Twin Disc achieved sales growth while facing margin pressure:

Segment Performance Analysis

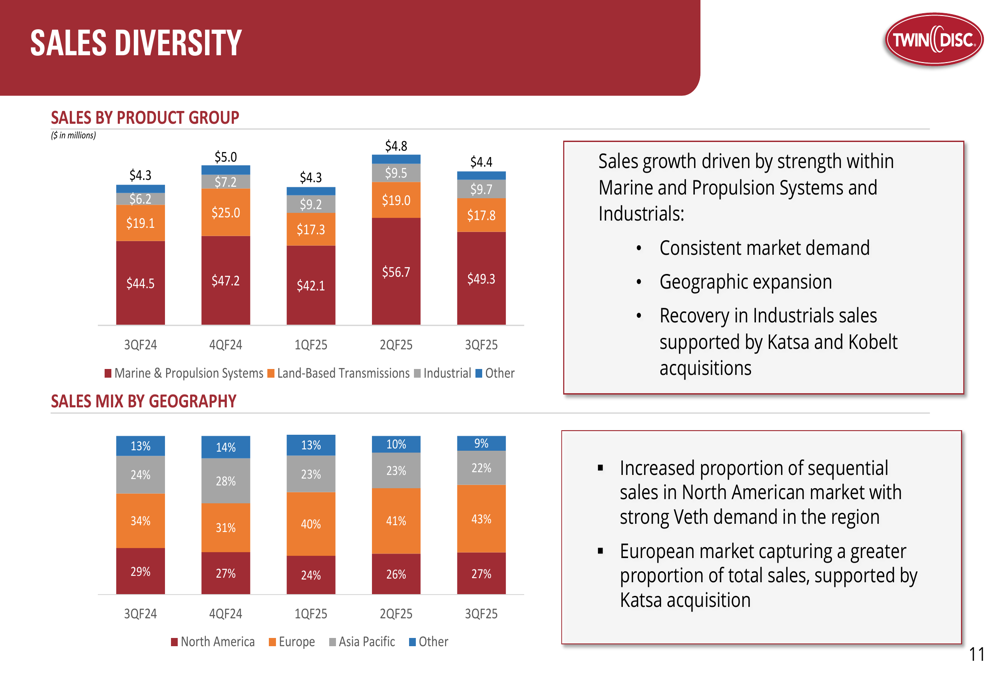

Twin Disc’s performance varied significantly across its three main business segments. The Marine & Propulsion Systems segment, which represents the largest portion of the company’s revenue, increased sales by 10.7% year-over-year, driven by strong commercial markets globally and robust demand for Veth propulsion systems.

"Commercial markets show notable strength globally," the company noted in its presentation, adding that "strong Veth orders and healthy backlog [are] supported by robust demand across markets." The company also highlighted that its Rolla & Veth partnership continues to perform well in the luxury yacht market.

In contrast, the Land-Based Transmissions segment saw sales decrease by 6.9% year-over-year. While the company reported strong shipments and backlog growth for its ARFF (Aircraft Rescue and Fire Fighting) transmissions, the Oil & Gas segment faced challenges with muted North American new build activity due to capital discipline. Additionally, in China, "lower but stable volumes persist, though tariff uncertainties are impacting new build pace."

The Industrial segment delivered the strongest growth, with sales increasing by 56.2% year-over-year, primarily due to the contributions from the recent acquisitions of Katsa Oy and Kobelt.

The following chart illustrates the company’s sales diversity by product group, highlighting the relative contribution of each segment:

Backlog and Financial Position

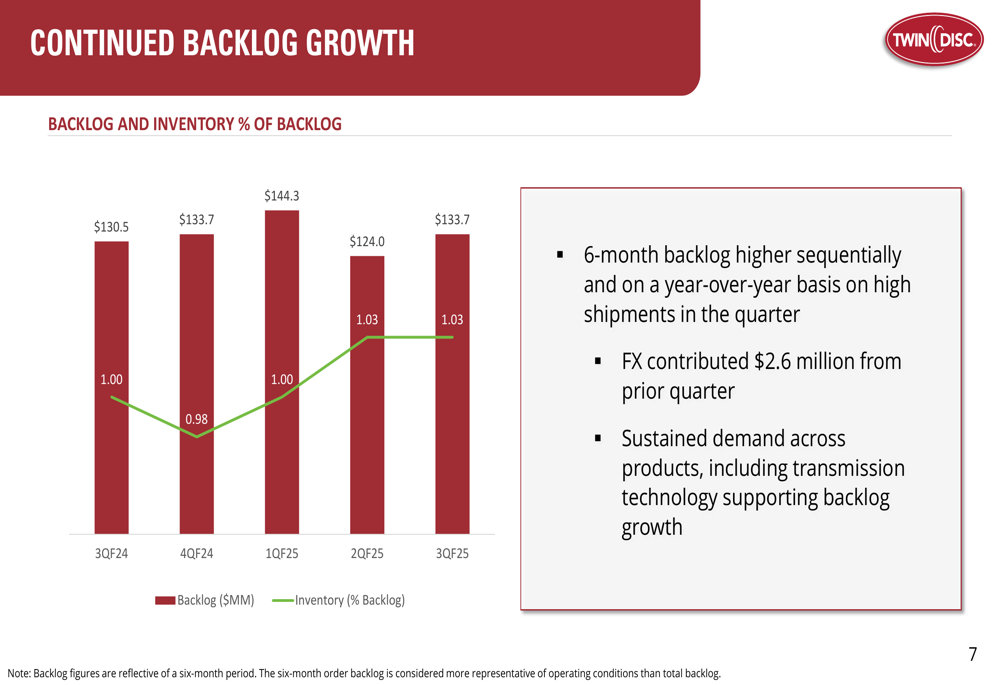

Twin Disc reported a six-month backlog of $133.7 million, higher both sequentially and year-over-year, indicating sustained demand across its product lines. Foreign exchange contributed $2.6 million to the backlog increase from the prior quarter.

The company’s backlog trend over recent quarters demonstrates consistent demand, as shown in the following chart:

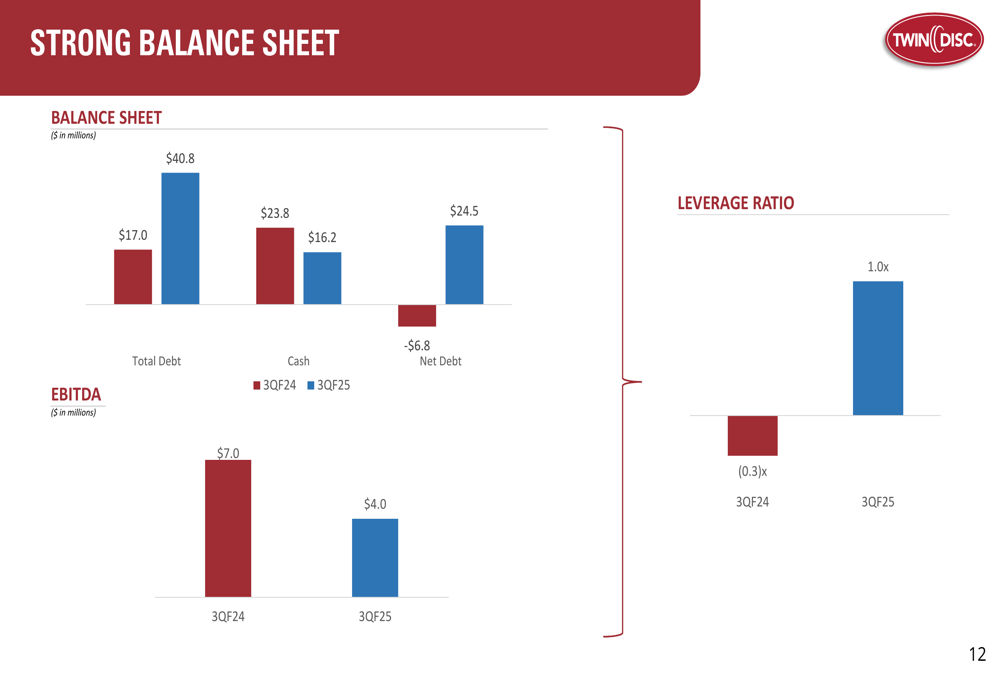

Twin Disc’s balance sheet showed a shift from a net cash position last year to a net debt position this year, primarily due to the funding of recent acquisitions. As of March 28, 2025, the company reported total debt of $40.8 million and cash of $16.2 million, resulting in net debt of $24.5 million, compared to a net cash position of $6.8 million a year earlier. The leverage ratio stood at 1.0x, which remains at a manageable level.

The following chart illustrates the company’s debt position:

Margin Pressure and Operational Challenges

Despite the sales growth, Twin Disc experienced margin pressure during the quarter. Gross margin decreased by approximately 150 basis points year-over-year to 26.7%, which the company attributed to "unfavorable product mix with reduced shipments of oil and gas transmissions into China."

The company’s quarterly EPS trend shows the impact of these challenges on profitability:

Twin Disc’s EBITDA for the third quarter was $4.0 million, down from $7.0 million in the same quarter last year. This decline in profitability occurred despite the increase in sales, highlighting the margin challenges the company is facing.

Strategic Initiatives

Twin Disc outlined several strategic initiatives aimed at long-term growth and value creation. The company is positioning itself as a "leading Hybrid/Electric solution provider for niche marine and land-based applications" and plans to continue expanding its Veth product line to reach new markets and geographies.

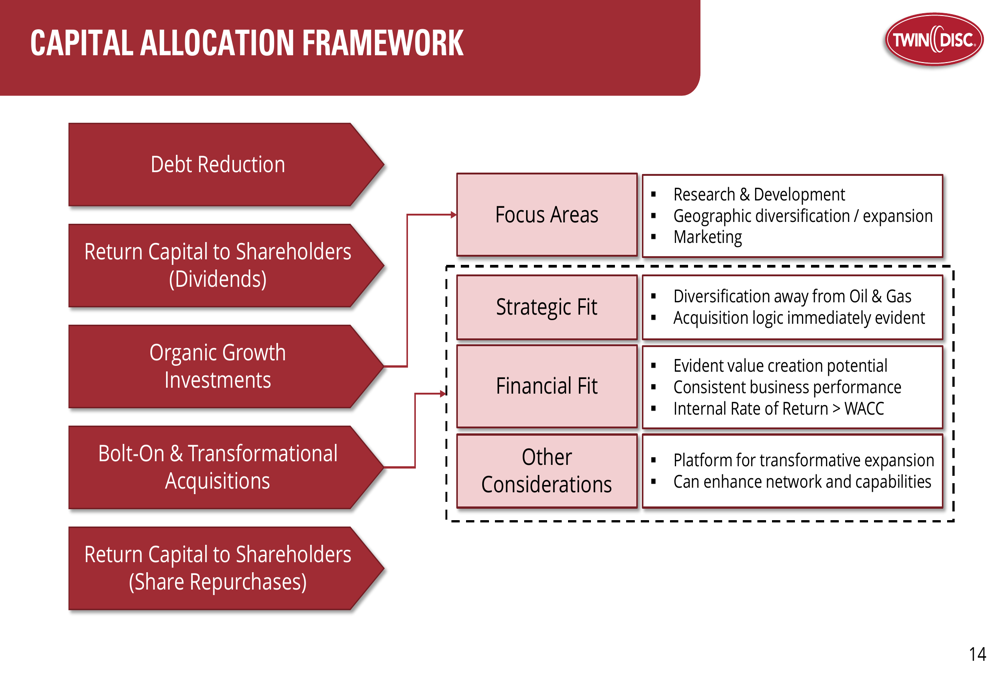

The company’s capital allocation framework prioritizes debt reduction, shareholder returns through dividends, organic growth investments, and strategic acquisitions. M&A priorities focus on Industrial and Marine Technology with an emphasis on hybrid solutions.

As illustrated in the following capital allocation framework, Twin Disc has a structured approach to deploying capital:

Forward-Looking Statements

Looking ahead, Twin Disc emphasized its focus on navigating economic uncertainties, particularly regarding tariffs. The company stated it has "limited direct tariff exposure combined with agile global operations," which it believes positions it well to effectively manage potential challenges.

In its previous earnings call, Twin Disc had outlined ambitious targets of reaching approximately $500 million in revenue by 2030 with gross margins of 30% and a free cash flow conversion rate of at least 60%. While these specific targets were not reiterated in the current presentation, the company continues to emphasize its strategic initiatives aimed at long-term growth.

The company’s key takeaways emphasized its "solid quarter with strong margins and operational execution," despite the reported decline in gross margin and profitability. Twin Disc also highlighted its "strong balance sheet and financial foundation driving long term growth through disciplined capital deployment."

As Twin Disc continues to integrate its recent acquisitions and navigate market uncertainties, investors will be watching closely to see if the company can translate its growing backlog into improved profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.