German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Ultra Clean Holdings Inc (NASDAQ:UCTT) presented its Q2 2025 investor presentation on July 28, 2025, highlighting the company’s financial performance and strategic positioning in the semiconductor manufacturing ecosystem. The presentation comes as the semiconductor industry continues to navigate a complex landscape of AI-driven demand, geopolitical uncertainties, and varying segment performance.

UCT’s stock closed at $23.96 on the day of the presentation, up 3.21%, with after-hours trading showing an additional 1.71% gain to $24.37. The company, which recently celebrated its 30th anniversary, has positioned itself as a critical supplier in the semiconductor manufacturing supply chain, providing both products and services across the chip production lifecycle.

Quarterly Performance Highlights

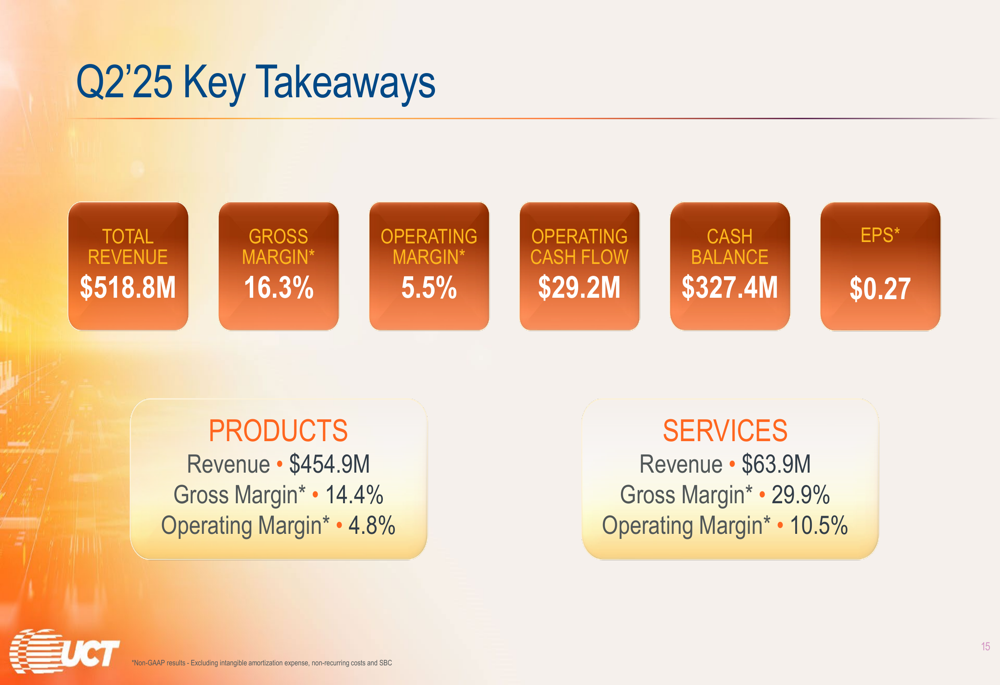

Ultra Clean reported Q2 2025 revenue of $518.8 million, essentially flat compared to the $518.6 million reported in Q1 2025. The company posted a non-GAAP EPS of $0.27, slightly down from $0.28 in the previous quarter, reflecting ongoing challenges in the semiconductor equipment market.

The company’s financial results show a clear distinction between its two business segments. The Products division generated $454.9 million in revenue with a 14.4% gross margin and 4.8% operating margin, while the Services division contributed $63.9 million with substantially higher profitability metrics – 29.9% gross margin and 10.5% operating margin.

As shown in the following quarterly financial summary:

UCT’s operating cash flow remained positive at $29.2 million, and the company ended the quarter with a strengthened cash position of $327.4 million, up from $317.6 million in Q1 2025. This improved liquidity provides the company with flexibility to pursue its strategic initiatives while navigating market uncertainties.

Strategic Initiatives and Growth Strategy

A cornerstone of UCT’s long-term strategy has been its disciplined acquisition approach, which has enabled the company to expand its addressable market, diversify offerings, and improve margins. The presentation highlighted several strategic acquisitions over the past decade that have contributed significantly to revenue growth and margin expansion.

The company’s acquisition strategy is illustrated in this timeline:

These acquisitions have helped UCT increase its total addressable market, which the company now estimates at $28-31 billion for its products division and $1.6-1.8 billion for services within a total wafer fabrication equipment (WFE) market of $100-105 billion in 2025.

The company’s market opportunity is visualized in the following slide:

UCT has also established a global footprint with strategic locations across North America, Europe, and Asia, positioning itself close to major customers and semiconductor manufacturing hubs. This global presence has become increasingly important as semiconductor companies diversify their supply chains in response to geopolitical concerns.

Industry Positioning and Customer Diversification

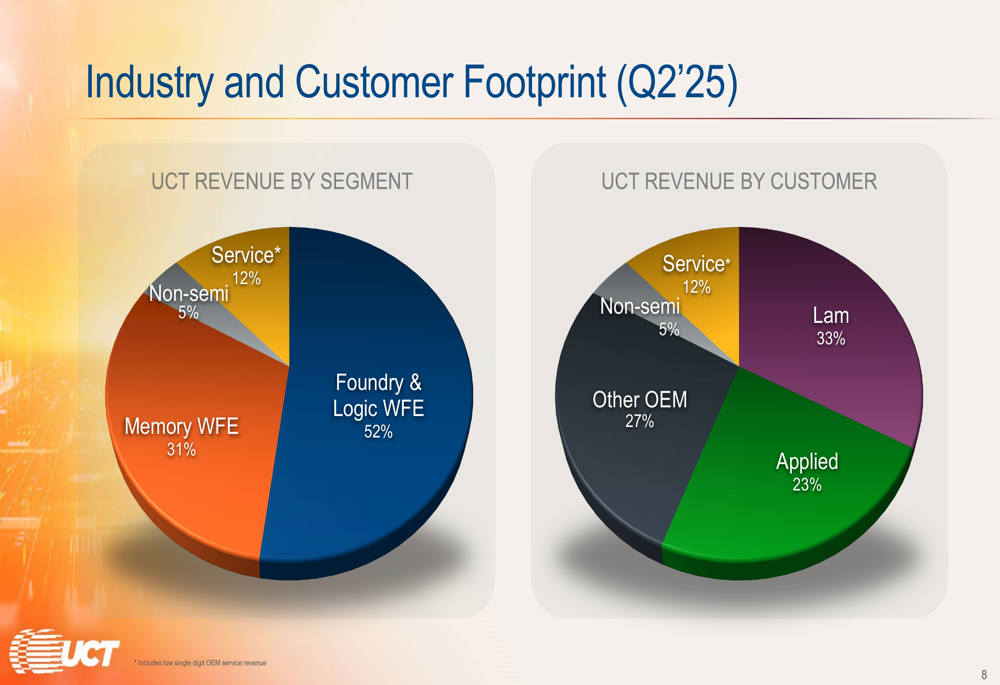

Ultra Clean has established a diverse customer base within the semiconductor industry, with significant revenue contributions from major OEMs including Lam Research (NASDAQ:LRCX) (33%) and Applied Materials (NASDAQ:AMAT) (23%). The company’s revenue is primarily derived from foundry and logic wafer fabrication equipment (52%) and memory WFE (31%), with services and non-semiconductor applications accounting for the remainder.

The following chart illustrates UCT’s revenue breakdown by segment and customer:

UCT’s involvement spans the entire chip manufacturing lifecycle, from fab construction support to equipment buildout and production services. The company plays a critical role in various process steps of semiconductor manufacturing, including lithography, etching, deposition, and cleaning – processes that require hundreds of tools per fab and thousands of steps per device.

End Market Trends and Outlook

The presentation provided insights into current trends across key semiconductor end markets. In the foundry segment, investments continue to support long-term demand, particularly for advanced packaging and gate-all-around (GAA) technologies to support AI applications, though trailing edge spending has paused to align with segment demand.

Logic spending is occurring across a wider base as inventories stabilize and global supply chains realign. In memory, 3D NAND node transitions are driving spending, with some strength for high-capacity AI solid-state drives, while DRAM profitability is improving on AI demand, with high-bandwidth memory (HBM) continuing to drive fab and packaging spending.

The company’s analysis of end market trends is shown here:

Forward-Looking Statements

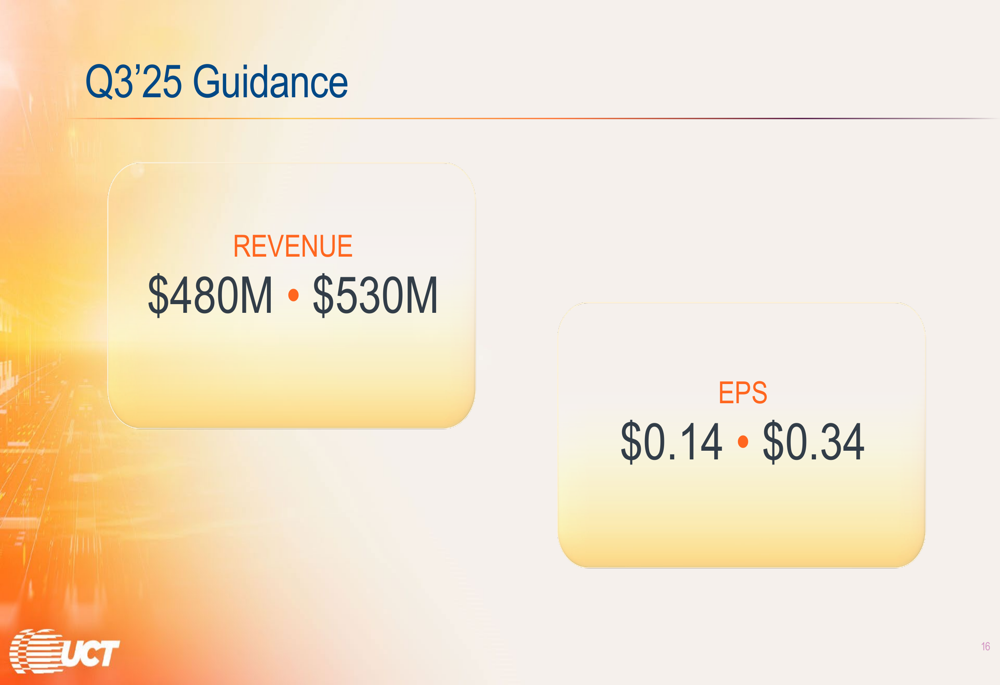

Looking ahead, UCT provided guidance for Q3 2025, projecting revenue between $480 million and $530 million and EPS in the range of $0.14 to $0.34. This guidance suggests potential revenue growth but with a wider EPS range, reflecting ongoing market uncertainties.

The Q3 guidance is presented here:

For the Products division, UCT outlined opportunities to increase share in manufactured components, further penetrate current major customers, expand presence at other major OEMs, grow engagement with smaller customers, and pursue opportunistic consolidation within the fragmented supply chain.

In the Services division, the company aims to reduce cost of ownership through advanced technology, create integrated solutions across UCT’s core competencies, improve efficiencies by leveraging part cleaning knowledge, and introduce proven atomically clean surfaces to new customers.

These strategic initiatives align with the company’s interim CEO Clarence Granger’s recent comments about focusing on cost reduction and scalability while positioning the company for market recovery. As the semiconductor industry continues to evolve with AI-driven demand and shifting geopolitical considerations, UCT’s diversified approach and global footprint provide a foundation for navigating the complex market landscape ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.