Bitcoin price today: rises to $116.5k on Trump 401k order, altcoins rally

Introduction & Market Context

Ultragenyx Pharmaceutical (TADAWUL:2070) Inc. (NASDAQ:RARE) presented its corporate overview on August 5, 2025, highlighting its position as a "next generation rare disease company" focused on developing transformative treatments for conditions with high unmet needs. The presentation comes at a critical time for the company, as its stock has experienced volatility following its Q1 2025 earnings report, which showed strong revenue growth but continued losses. Currently trading at $28.46, the stock remains well below its 52-week high of $60.37, reflecting investor concerns about the path to profitability despite robust revenue growth.

Executive Summary

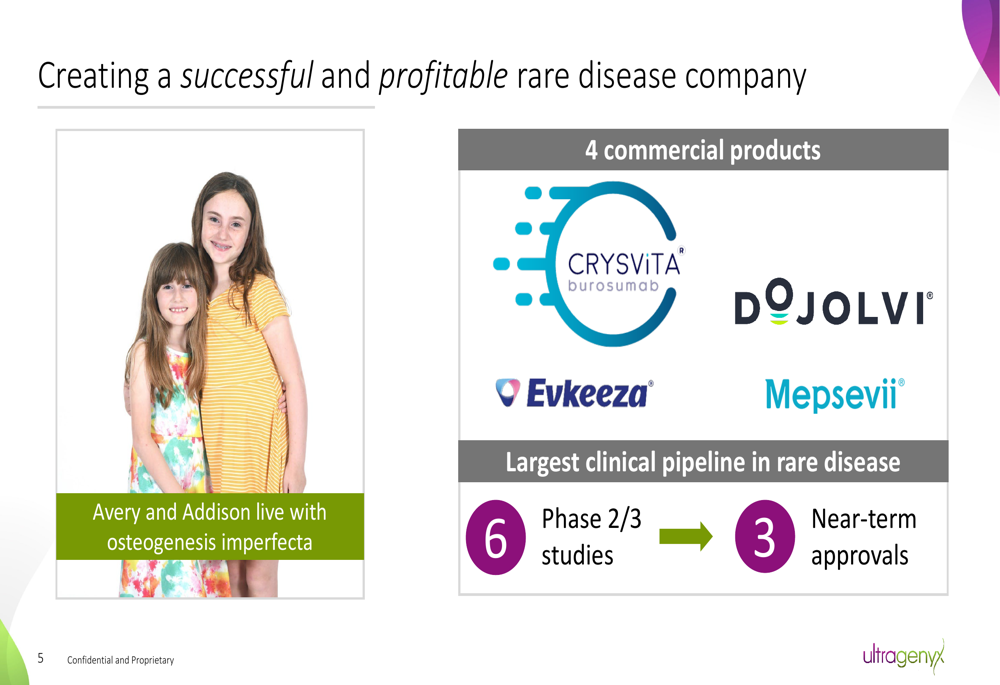

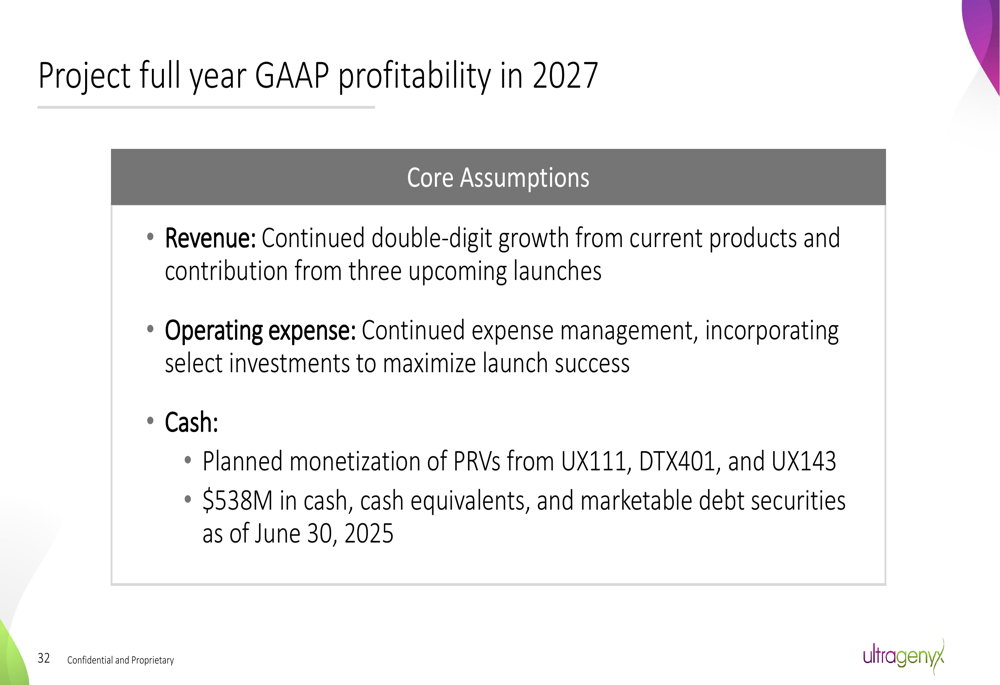

Ultragenyx has built a diversified rare disease portfolio with four commercial products and what it describes as "the largest clinical pipeline in rare diseases" with six Phase 2/3 studies underway and three near-term approvals anticipated. The company is targeting full-year GAAP profitability by 2027, driven by continued double-digit revenue growth from existing products and contributions from upcoming product launches.

As shown in the following presentation slide, Ultragenyx has established itself with four commercial products while maintaining a robust clinical pipeline:

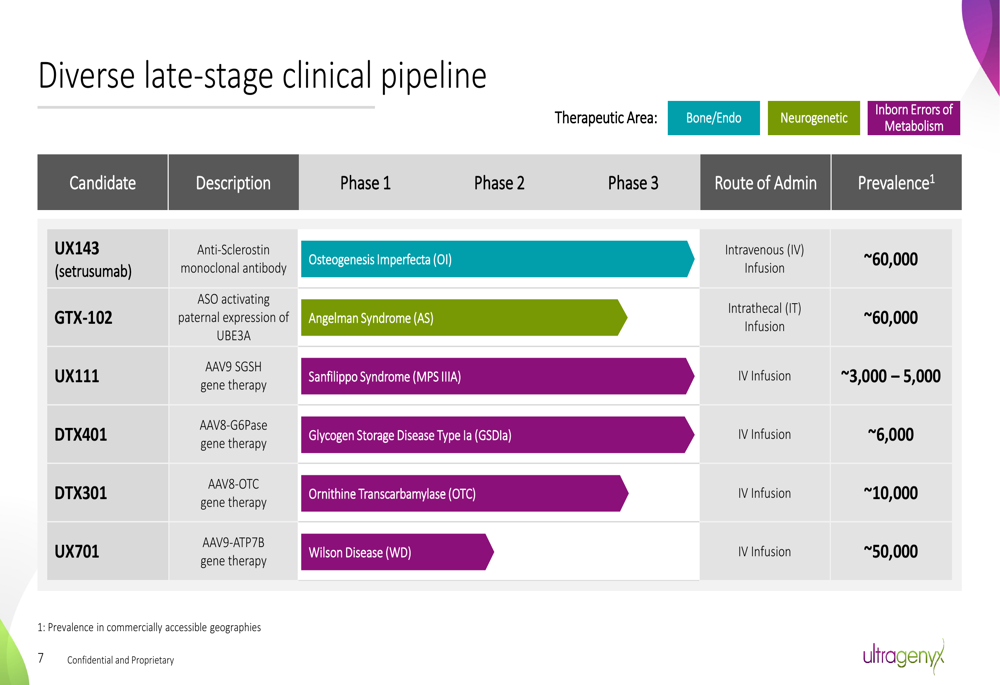

The company’s late-stage clinical pipeline spans three therapeutic areas: Bone-Endocrine, Neurogenetic, and Inborn Errors of Metabolism. This diversified approach provides multiple opportunities for growth while mitigating risk through portfolio diversification.

Strategic Initiatives

Ultragenyx’s corporate strategy centers on a differentiated approach to rare diseases across research, development, and commercialization. The company focuses on high-potential programs addressing severe diseases with unmet needs, accelerates development through adaptive trial designs, and employs a patient-centric commercial model with lean teams.

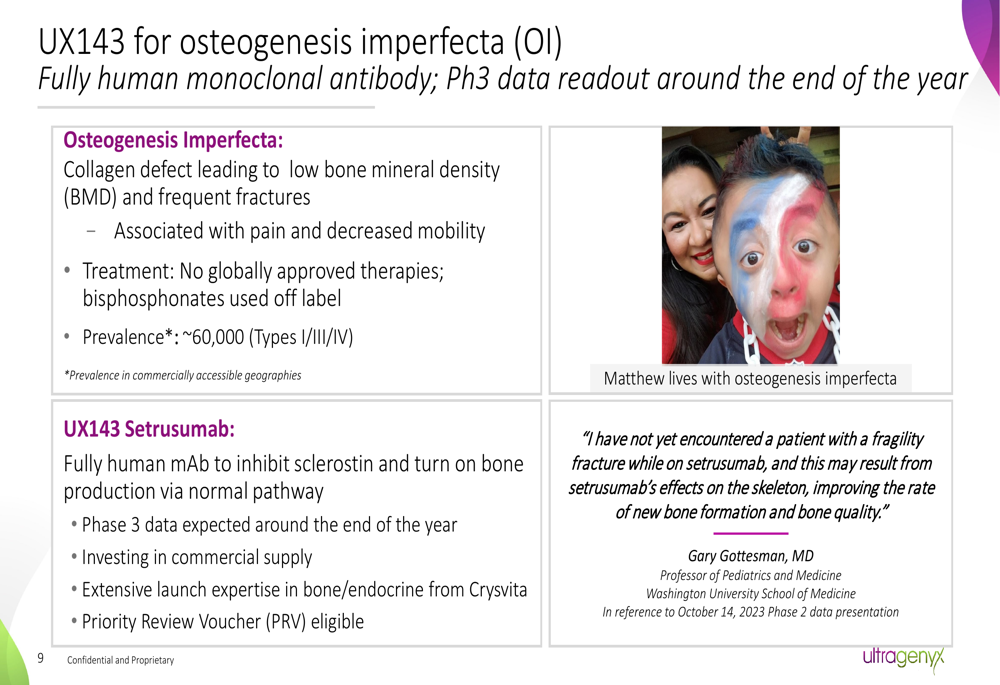

UX143 for Osteogenesis Imperfecta

One of Ultragenyx’s most promising late-stage candidates is UX143 (setrusumab), an anti-sclerostin monoclonal antibody for Osteogenesis Imperfecta (OI), a serious condition affecting approximately 60,000 patients globally. The Phase 3 data readout is expected around the end of 2025.

The following slide provides an overview of the disease and treatment approach:

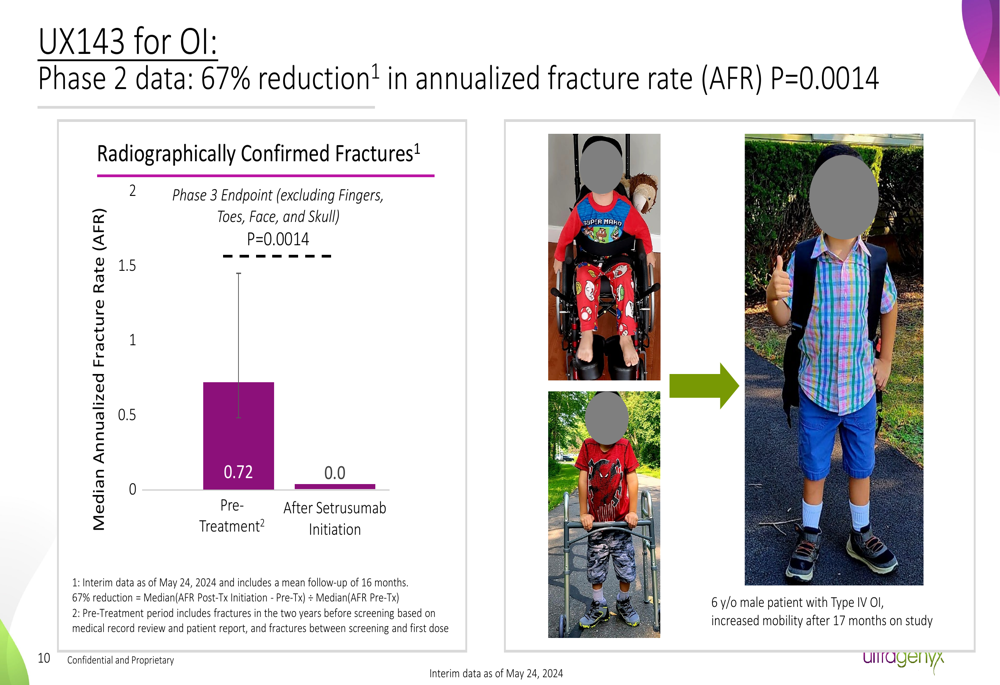

Phase 2 data has demonstrated impressive efficacy, with a 67% reduction in annualized fracture rate (p=0.0014). This significant improvement in fracture reduction represents a potentially transformative treatment option for patients with OI, who currently have no FDA-approved therapies.

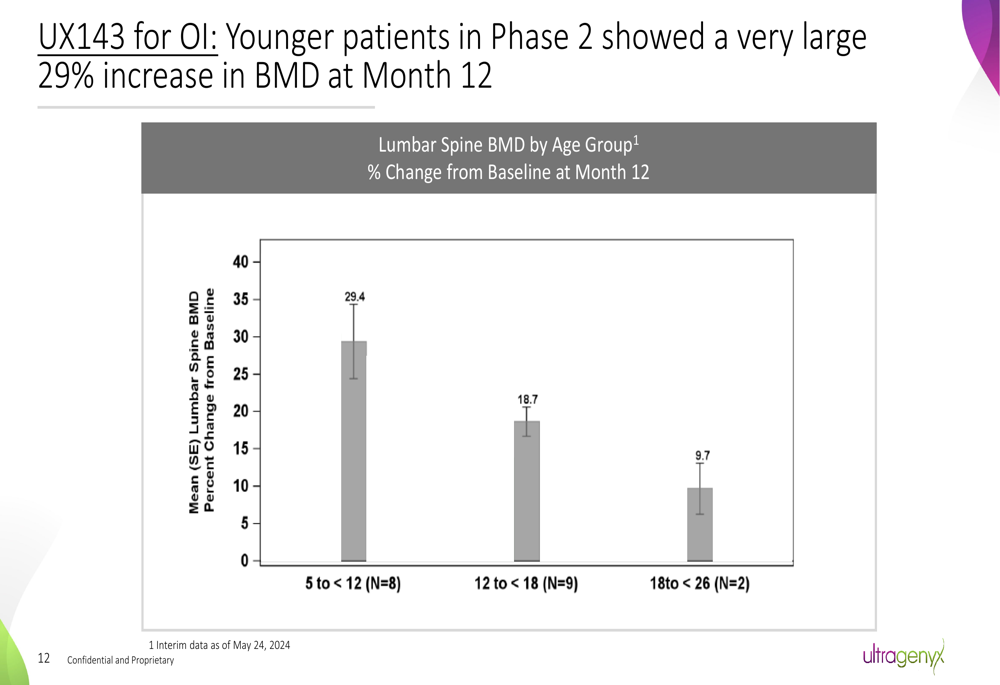

The treatment has shown particularly strong effects in younger patients, with those aged 5 to 12 years demonstrating a 29.4% increase in lumbar spine bone mineral density (BMD) at 12 months, compared to 18.7% in patients aged 12 to 18 years.

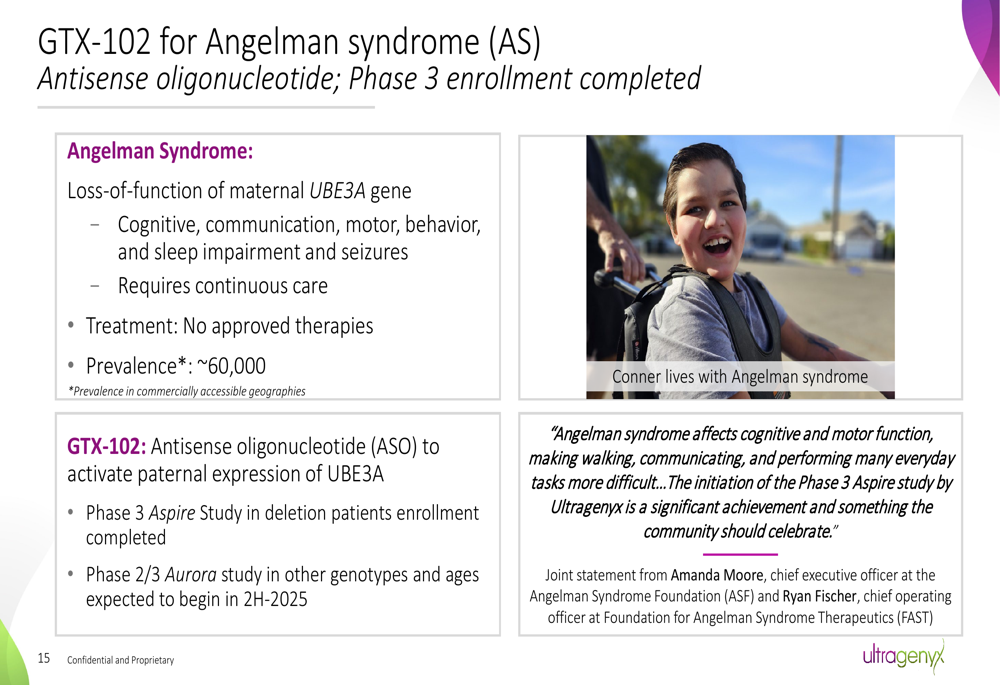

GTX-102 for Angelman Syndrome

Another key program in Ultragenyx’s pipeline is GTX-102, an antisense oligonucleotide designed to activate paternal expression of UBE3A for the treatment of Angelman Syndrome (AS). The Phase 3 Aspire study enrollment was completed in July 2025, representing a significant milestone for this program.

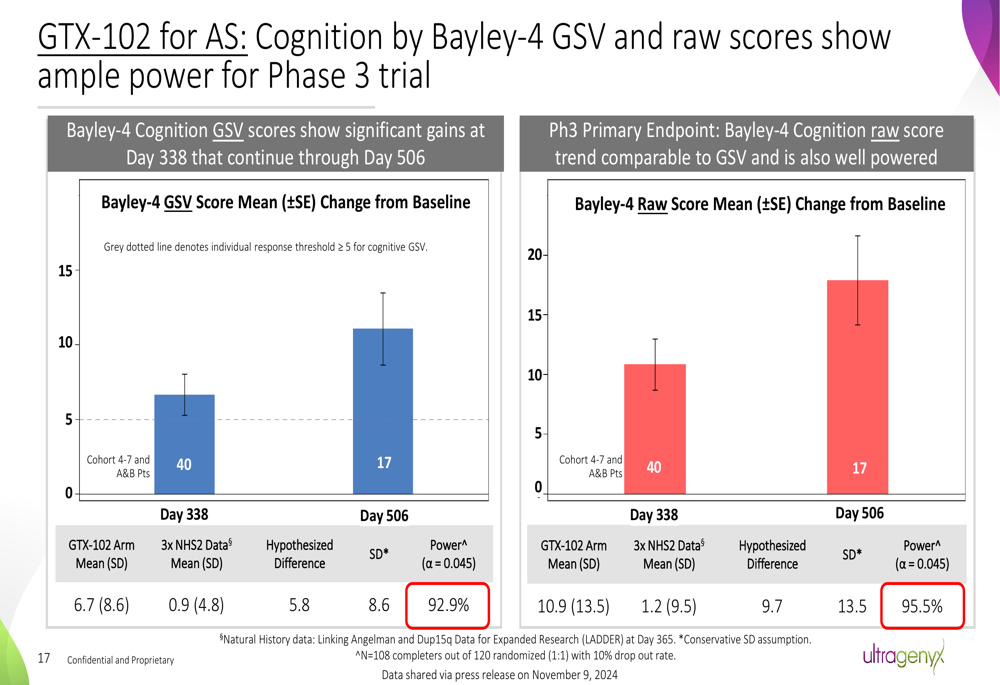

The Phase 1/2 data has shown consistent developmental gains across multiple symptom domains with sustained improvements for up to 3 years on therapy. The company has designed the Phase 3 study with ample statistical power based on the strong Phase 1/2 results.

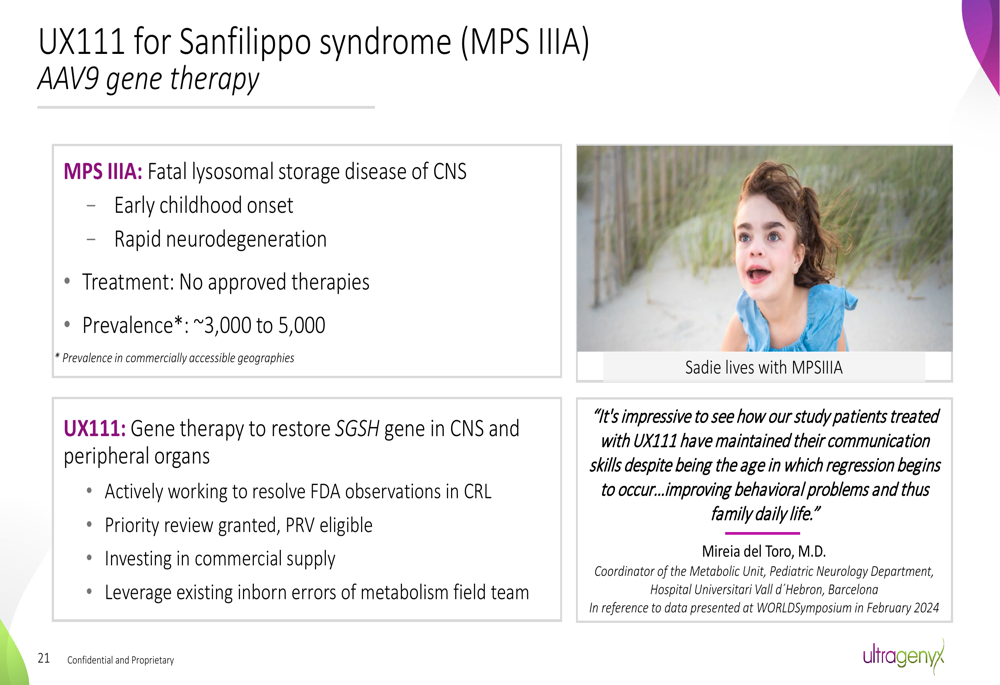

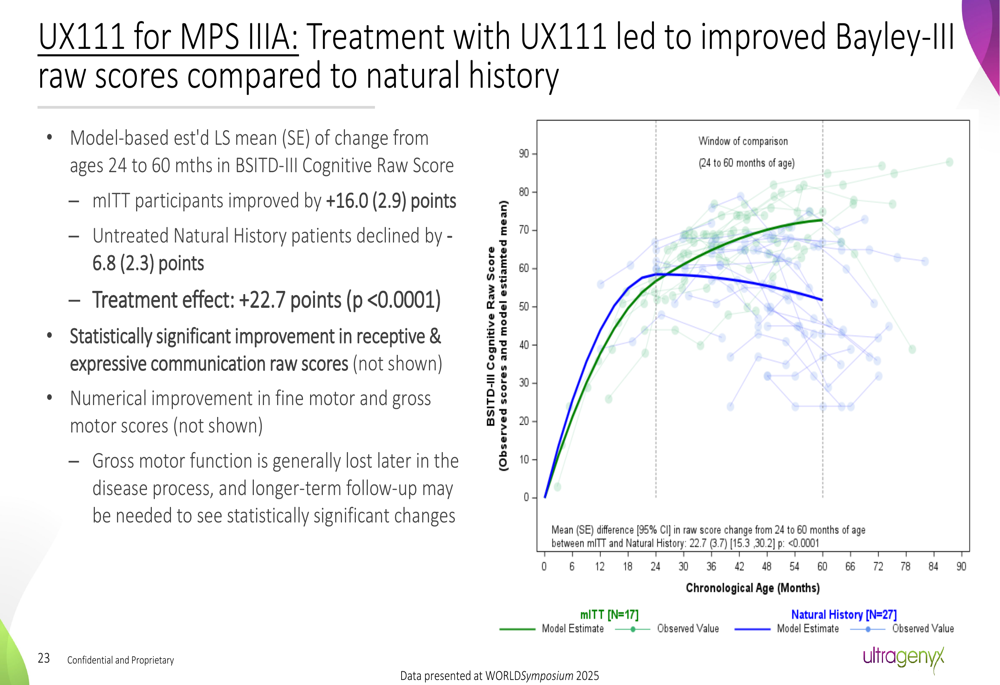

UX111 for Sanfilippo Syndrome

UX111, an AAV9 gene therapy for Sanfilippo Syndrome (MPS IIIA), has demonstrated promising results in clinical trials. The company is actively working to resolve FDA observations in a Complete Response Letter (CRL) and resubmit its Biologics License Application (BLA).

Clinical data has shown significant improvements in cognitive function compared to natural history, with treated patients showing gains while untreated patients typically decline:

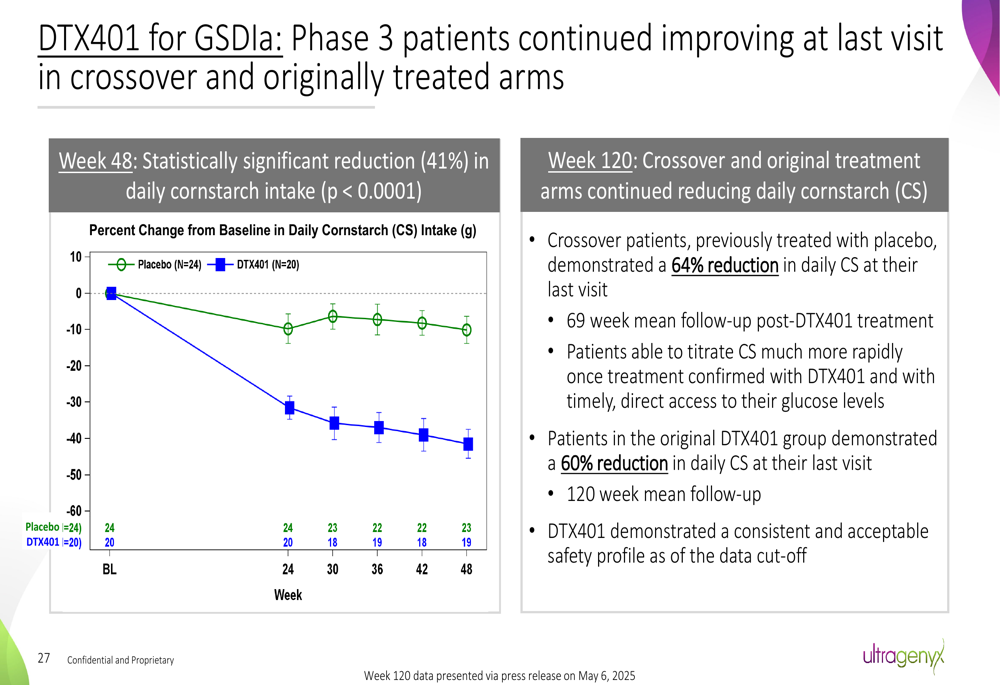

DTX401 for Glycogen Storage Disease Type Ia

DTX401, an AAV8 gene therapy for Glycogen Storage Disease Type Ia (GSDIa), has successfully completed Phase 3 trials with BLA submission expected in Q4 2025. The therapy demonstrated a 41% reduction in daily cornstarch intake at Week 48 (p<0.0001), addressing a critical need for these patients who must consume cornstarch every few hours to maintain glucose levels.

Detailed Financial Analysis

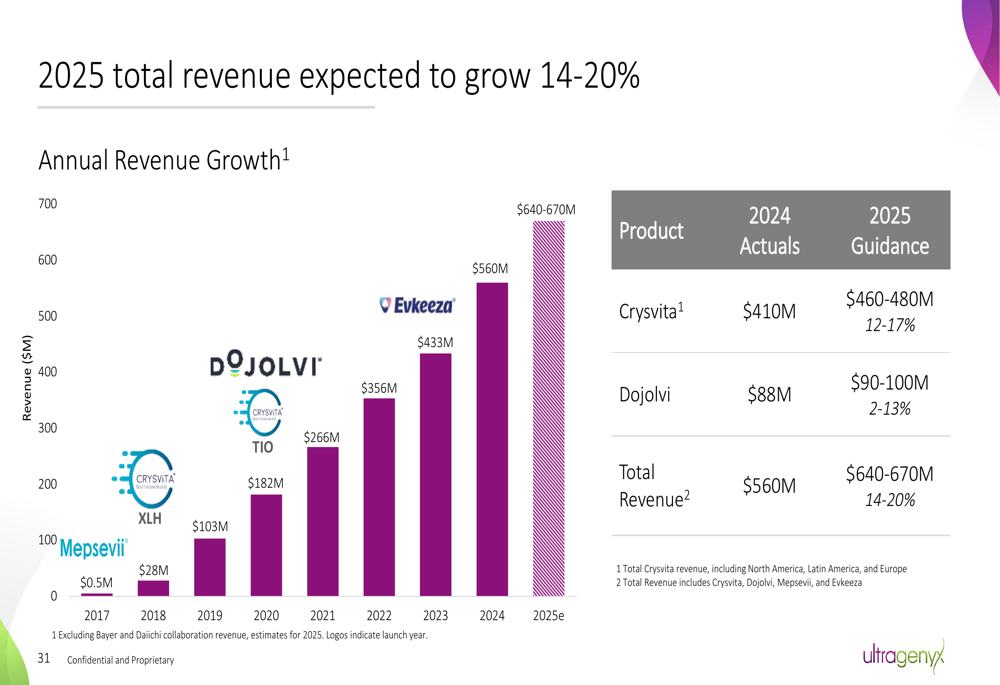

Ultragenyx projects 14-20% revenue growth for 2025, with total revenue expected to reach $640-670 million, up from $560 million in 2024. This growth is primarily driven by its lead product Crysvita, which is projected to generate $460-480 million in 2025, representing 12-17% growth from 2024.

Despite strong revenue growth, Ultragenyx continues to operate at a loss. In Q1 2025, the company reported a net loss of $151 million, or $1.57 per share, slightly missing analyst expectations of -$1.56 per share. High operating expenses of $282 million in Q1 2025 continue to impact profitability, though the company maintains a strong cash position with $538 million as of June 30, 2025.

The company’s path to profitability relies on continued revenue growth from existing products, contribution from upcoming product launches, and disciplined expense management. Ultragenyx also plans to monetize Priority Review Vouchers (PRVs) from UX111, DTX401, and UX143 to strengthen its financial position.

Forward-Looking Statements

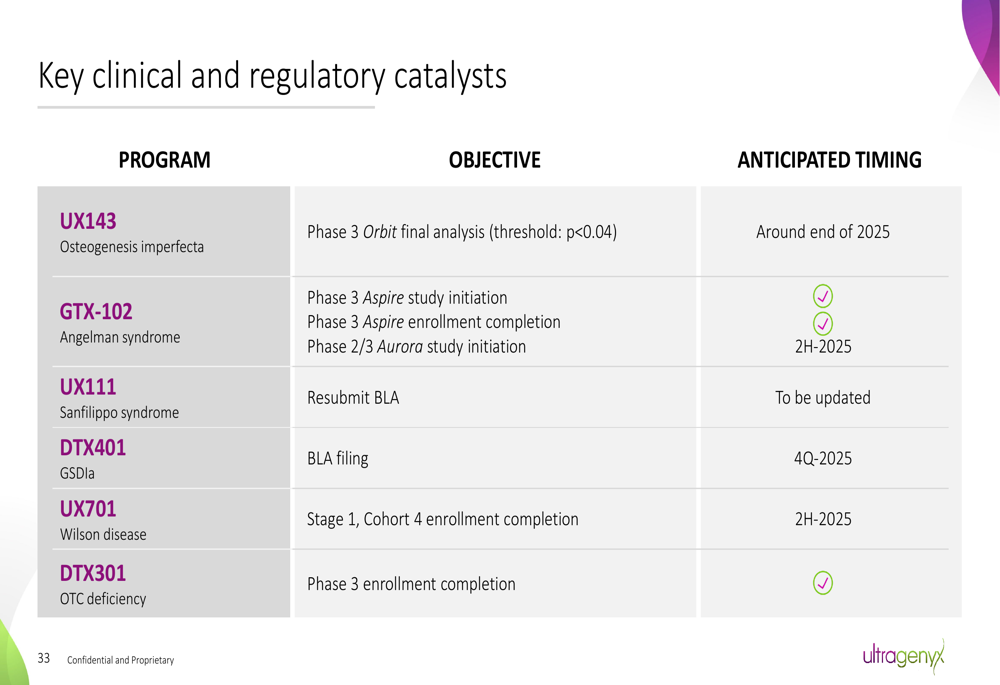

Ultragenyx has outlined several key catalysts expected in the coming months, including the Phase 3 data readout for UX143 in Osteogenesis Imperfecta, BLA filing for DTX401 in GSDIa, and the initiation of the Phase 2/3 Aurora study for GTX-102 in Angelman Syndrome.

The company’s CEO, Emil Kakas, stated during the Q1 2025 earnings call, "We expect 2025 to be the most productive year in our company’s history," highlighting the company’s strategic initiatives and focus on execution. This sentiment is reflected in the presentation’s emphasis on near-term catalysts and the path to profitability.

Ultragenyx faces several challenges, including high operating expenses that continue to impact profitability, potential regulatory hurdles for its pipeline programs, and competitive pressures in the rare disease market. However, the company’s diverse pipeline, strong revenue growth, and clear strategic focus position it well to navigate these challenges and potentially achieve its goal of GAAP profitability by 2027.

In conclusion, Ultragenyx’s August 2025 corporate presentation portrays a company at an inflection point, with multiple late-stage programs approaching potential approval and commercialization, driving its transition from a development-stage company to a profitable rare disease leader. Investors will be closely watching the upcoming clinical and regulatory milestones, particularly the Phase 3 data for UX143, which could significantly impact the company’s valuation and long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.