German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Unisys Corporation (NYSE:UIS) reported its second quarter 2025 financial results on July 30, showing modest year-over-year revenue growth but stronger sequential improvement, while raising its profitability guidance for the full year. The company’s stock closed at $4.15, down 2.17% on the day of the presentation.

The results mark a significant improvement from the first quarter, when Unisys reported an 11.4% year-over-year revenue decline. The company has also made strategic moves to address its pension liabilities and improve its capital structure through a major debt transaction.

Quarterly Performance Highlights

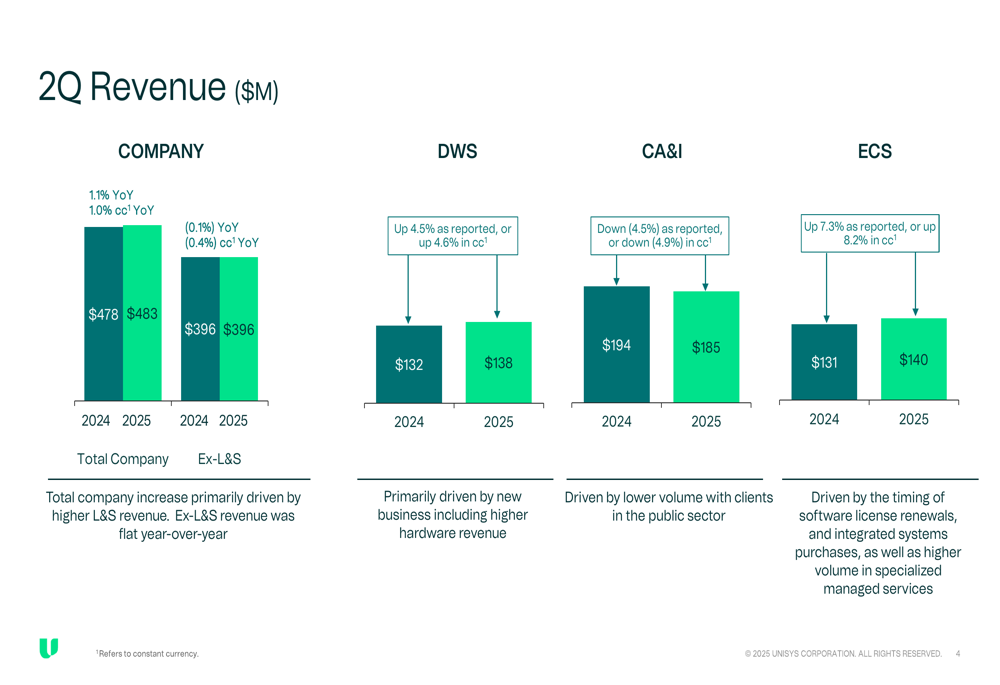

Unisys reported second quarter revenue of $483 million, representing a 1.1% increase as reported and 1.0% growth in constant currency compared to the same period last year. The company achieved more substantial sequential growth of 8.5% in constant currency from the first quarter.

As shown in the following revenue breakdown by segment:

The performance across business segments was mixed. Digital Workplace Solutions (DWS) revenue grew 4.5% year-over-year to $138 million, while Enterprise Computing Solutions (ECS) increased 7.3% to $140 million. However, Cloud, Applications & Infrastructure (CA&I) revenue declined 4.5% to $185 million.

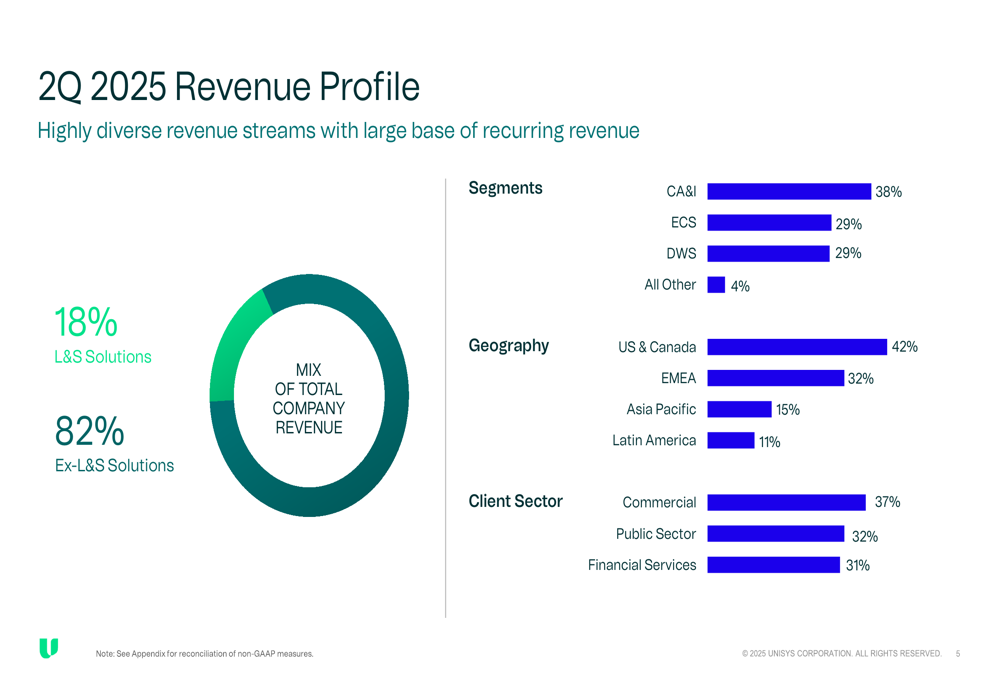

Unisys maintains a diverse revenue profile across segments, geographies, and client sectors:

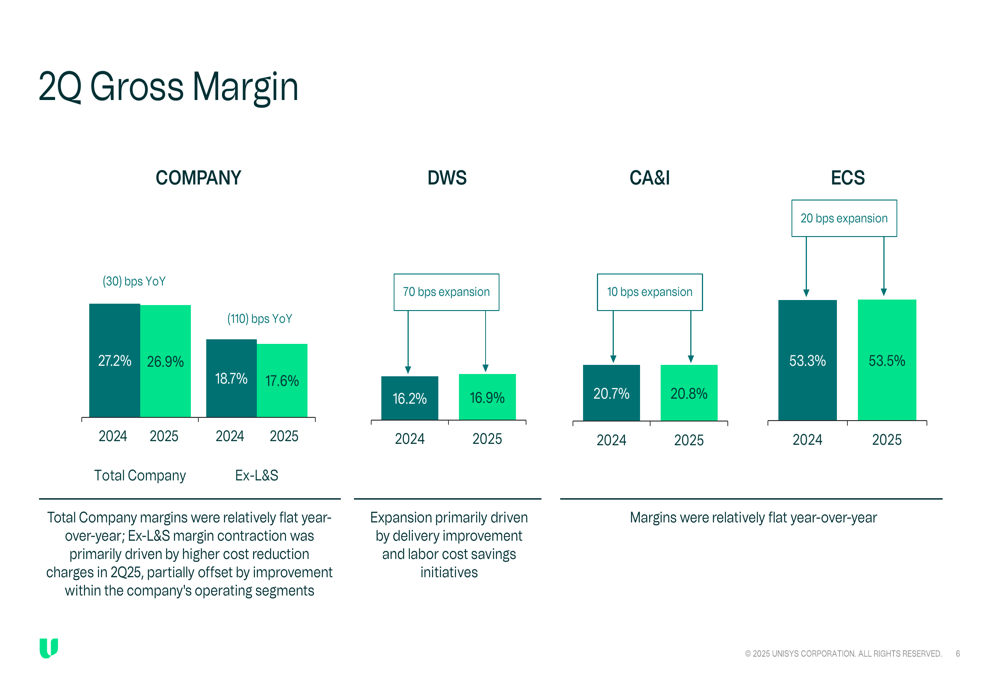

Profitability metrics showed improvement, with GAAP operating profit of $29 million (6.1% margin) and non-GAAP operating profit of $37 million (7.6% margin), exceeding company expectations. However, gross margin declined slightly to 26.9%, down 30 basis points year-over-year.

The following chart illustrates gross margin performance by segment:

Despite the overall margin decline, individual segments showed improvement, with DWS gross margin expanding 70 basis points to 16.9%, CA&I increasing 10 basis points to 20.8%, and ECS up 20 basis points to 53.5%.

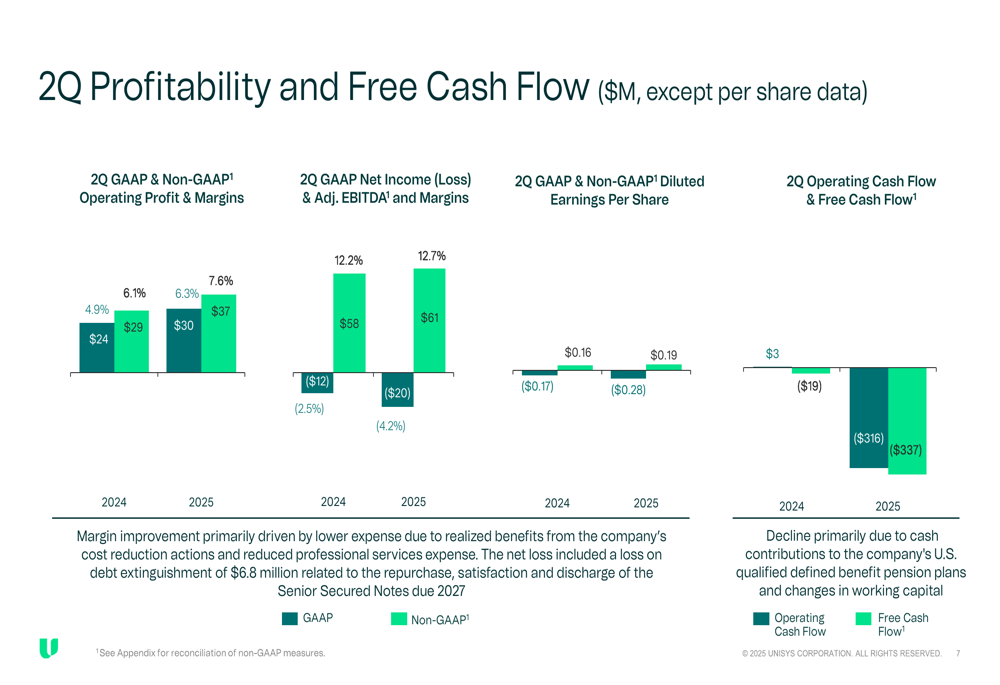

The company reported a GAAP net loss of $20 million (-4.2% margin) but achieved non-GAAP diluted earnings per share of $0.19, compared to $0.16 in the same period last year. Adjusted EBITDA reached $61 million (12.7% margin), up from $58 million (12.2% margin) in Q2 2024.

The following chart details profitability and free cash flow metrics:

Strategic Initiatives

A significant focus of Unisys’ presentation was its recent debt transaction and pension strategy. The company closed a $700 million senior secured notes offering on June 27, 2025, with a 10.625% coupon and 5.5-year maturity. The proceeds were used to refinance existing $485 million notes, contribute $250 million to U.S. Qualified Defined Benefit (QDB) Pension Plans, and for general corporate purposes.

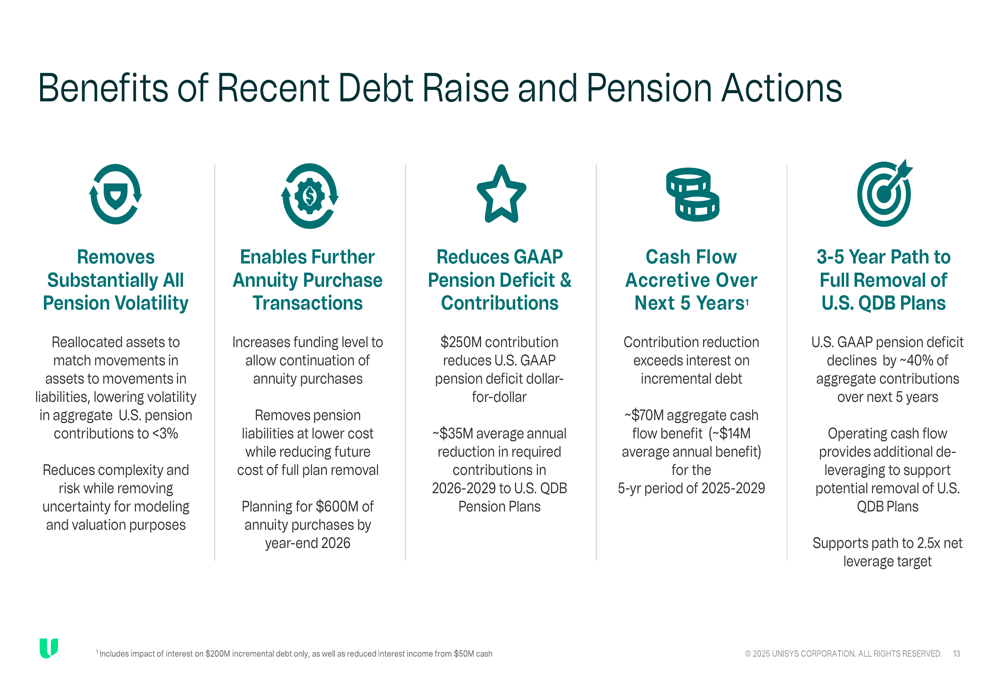

The company outlined several benefits from these actions:

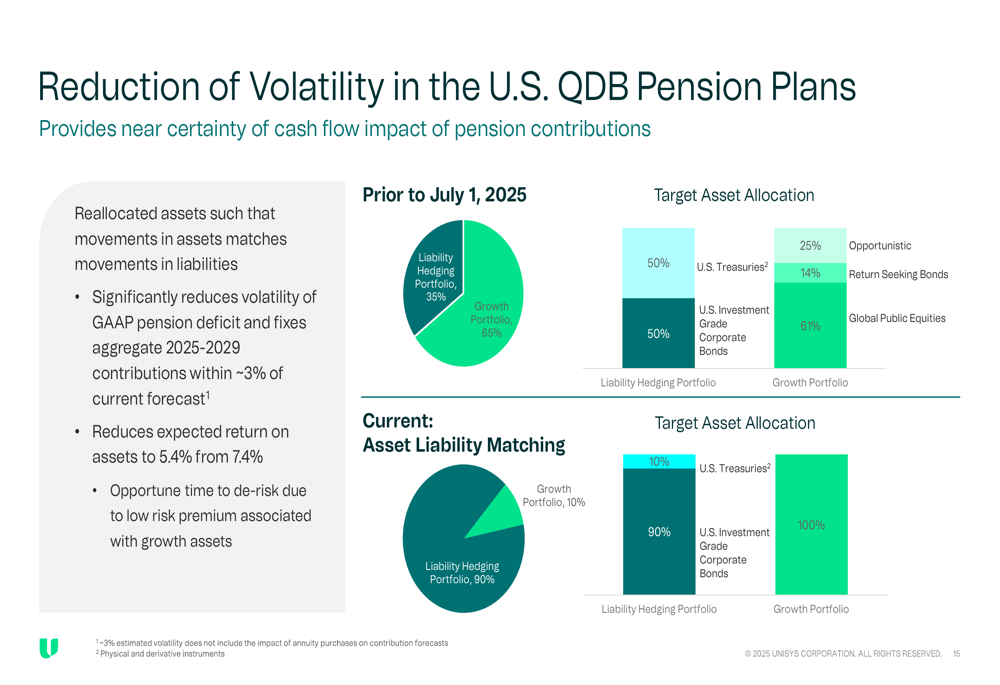

Unisys has also taken steps to reduce volatility in its pension plans by reallocating assets to better match movements in liabilities:

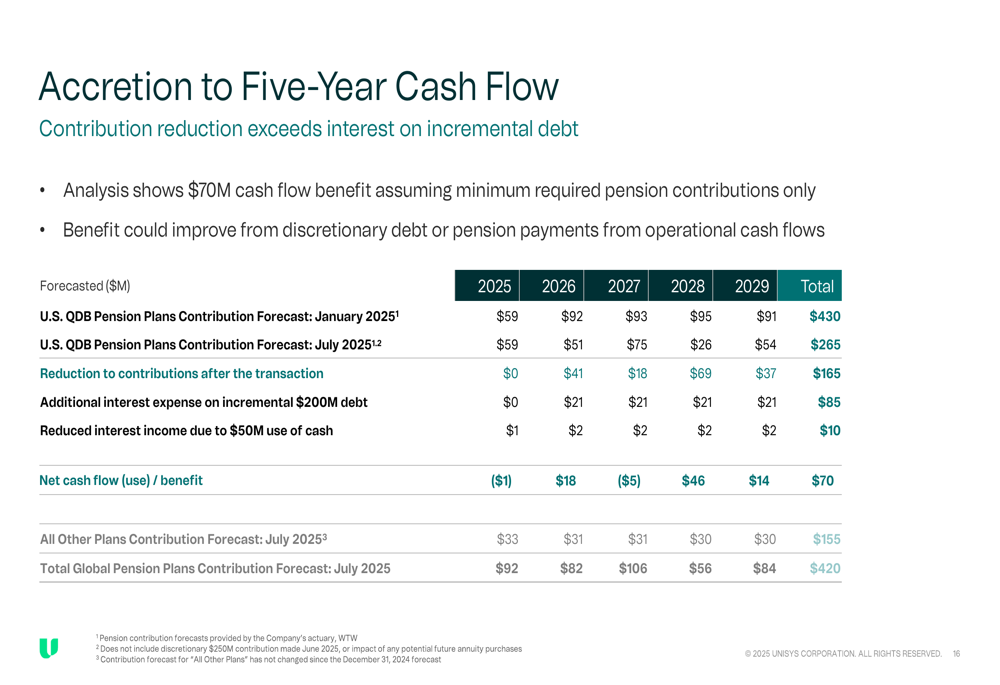

The company expects these strategic moves to be accretive to five-year cash flow, with contribution reductions exceeding the interest on incremental debt:

Forward-Looking Statements

Unisys updated its financial guidance for full-year 2025, revising its constant currency revenue growth expectation to between -1.0% and +1.0%, down from the previous guidance of 0.5% to 2.5%. However, the company raised its non-GAAP operating profit margin guidance to 8.0% to 9.0%, up from the previous 6.5% to 8.5%.

The company also increased its pre-pension free cash flow outlook by $10 million to approximately $110 million:

Unisys continues to focus on its strategic capital structure objectives, which include reducing the size of pension plans, maintaining strong cash balances, improving net leverage ratio, and eventually instituting a capital return program.

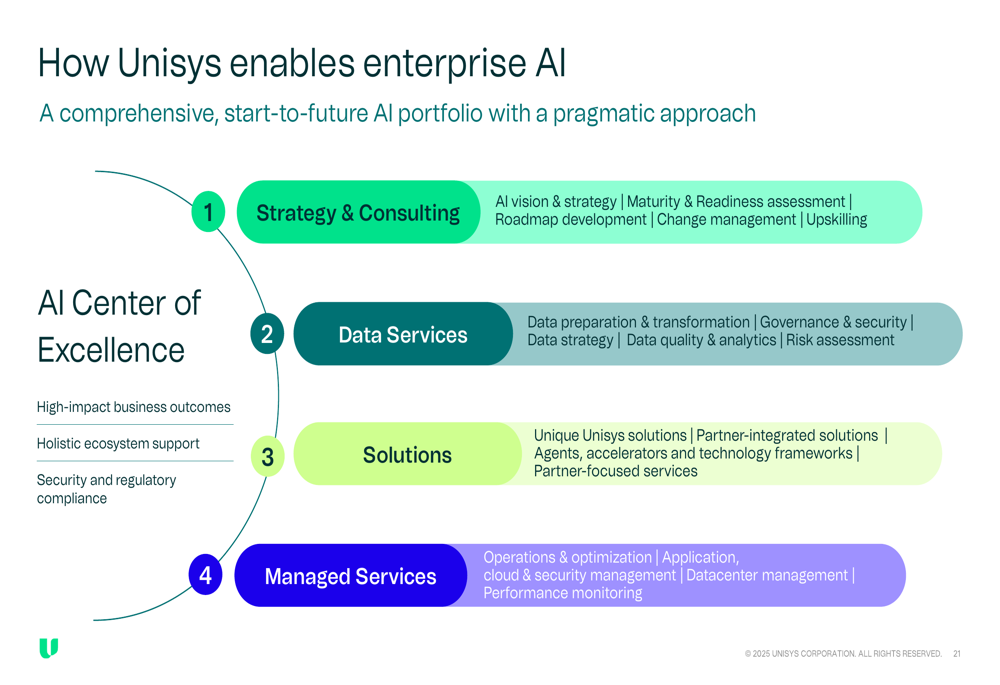

The company is also positioning itself in the enterprise AI market with a comprehensive approach:

Conclusion

Unisys’ second quarter 2025 results demonstrate modest year-over-year growth but significant sequential improvement from the first quarter. While the company has revised its revenue growth guidance downward, it has raised its profitability outlook, suggesting confidence in operational efficiency and margin expansion.

The strategic debt transaction and pension plan actions represent significant steps toward reducing volatility and improving the company’s long-term financial position. With a book-to-bill ratio of 1.0x and backlog of $2.9 billion (up 5% year-over-year), Unisys appears positioned for stability despite mixed segment performance.

The company’s focus on enterprise AI solutions and its diverse revenue streams across segments, geographies, and client sectors provide multiple avenues for potential growth, even as it navigates a challenging macroeconomic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.