Nvidia, AMD to pay 15% of China chip sales revenue to US govt- FT

Introduction & Market Context

United Fire Group (NASDAQ:UFCS) presented its second quarter 2025 financial results on August 6, 2025, revealing accelerated premium growth and the company’s best underwriting performance in over a decade. The results demonstrate significant improvement from the first quarter, when the company reported an EPS of $0.67 and a combined ratio of 99.4%. UFCS shares closed at $26.66 on August 5, having risen 0.53% ahead of the earnings presentation.

Quarterly Performance Highlights

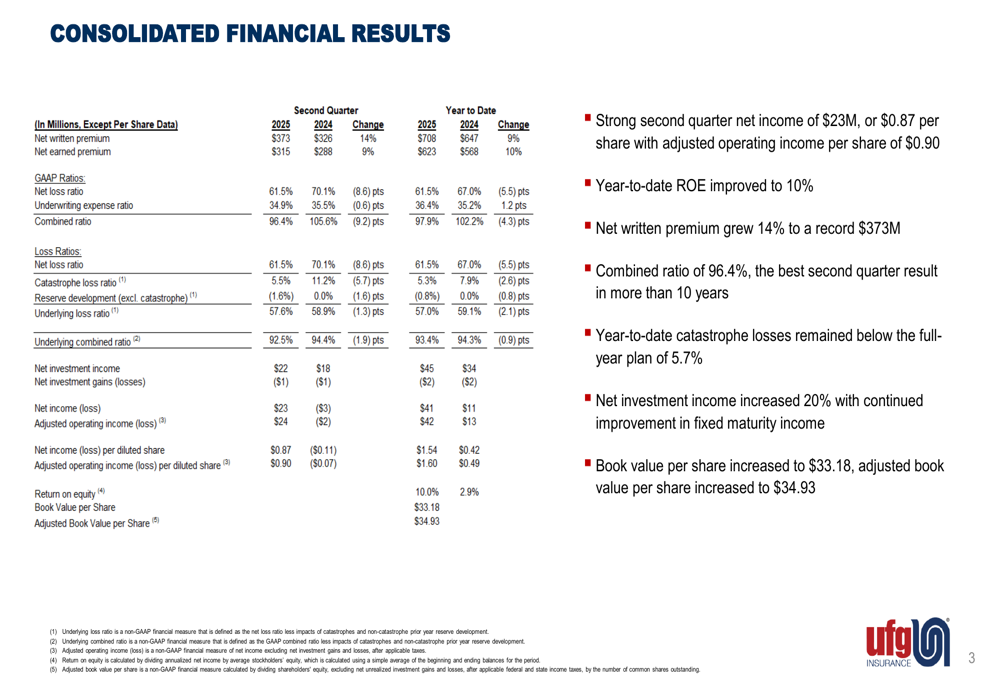

UFG reported strong second quarter results with net income of $23 million, or $0.87 per diluted share, while adjusted operating income reached $24 million, or $0.90 per diluted share. This represents a substantial improvement from the first quarter’s EPS of $0.67. The company achieved a combined ratio of 96.4%, marking its best second-quarter underwriting result in more than ten years.

As shown in the following consolidated financial results:

Net written premium grew 14% year-over-year to a record $373 million, significantly accelerating from the 4% growth reported in Q1. Net earned premium increased 9% to $315 million. The company’s year-to-date return on equity improved to 10%, while book value per share rose to $33.18, up from $32.13 at the end of Q1 2025.

Detailed Financial Analysis

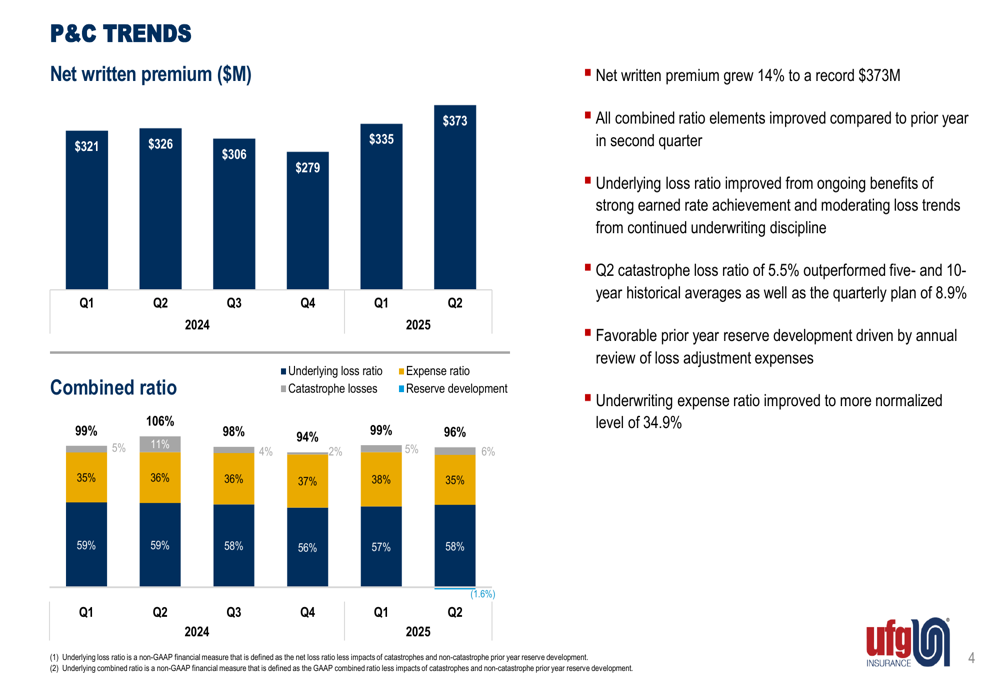

UFG’s P&C business demonstrated strong momentum across multiple metrics. The quarterly trend shows consistent premium growth culminating in the record $373 million in Q2, while the combined ratio improved across all components.

The following chart illustrates these P&C trends:

The underlying loss ratio improved to 58% in 2025 from 59% in 2024, reflecting benefits from strong earned rate achievement and moderating loss trends due to disciplined underwriting. Catastrophe losses were particularly favorable at 5.5% for Q2, outperforming both the company’s quarterly plan of 8.9% and historical five and ten-year averages. The underwriting expense ratio normalized to 34.9%, contributing to the overall improvement in the combined ratio.

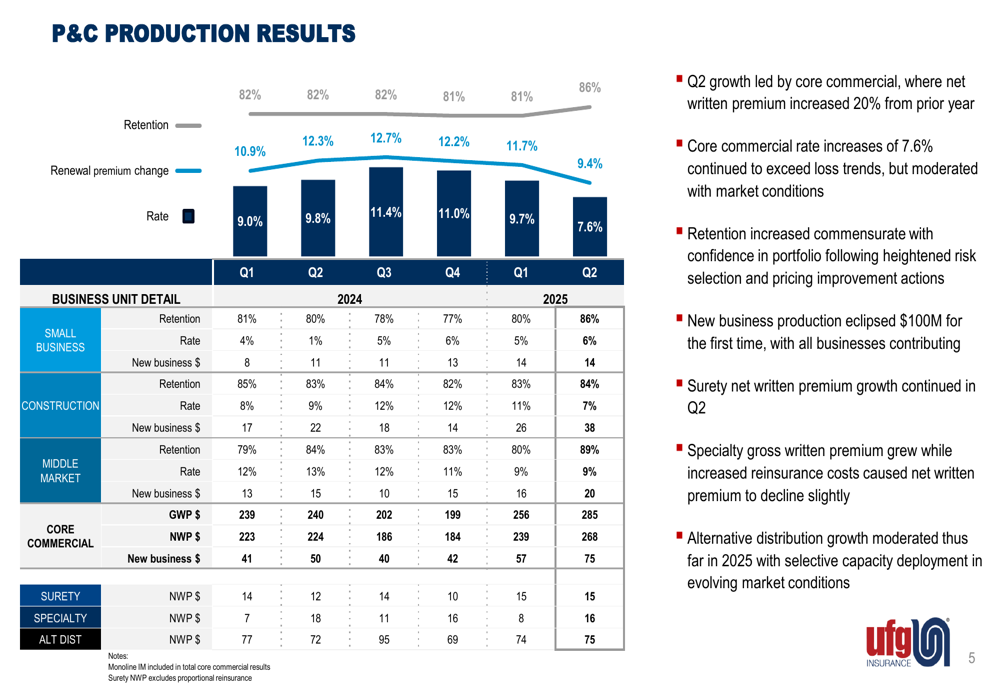

The company’s production results by business segment reveal broad-based growth:

Core commercial lines led the growth, with net written premium increasing 20% year-over-year. Commercial rate increases of 7.6% continued to exceed loss trends, though they moderated with changing market conditions. Retention rates improved as the company gained confidence in its portfolio following risk selection and pricing improvement actions. New business production exceeded $100 million for the first time, with all business units contributing to this milestone.

Investment Portfolio Performance

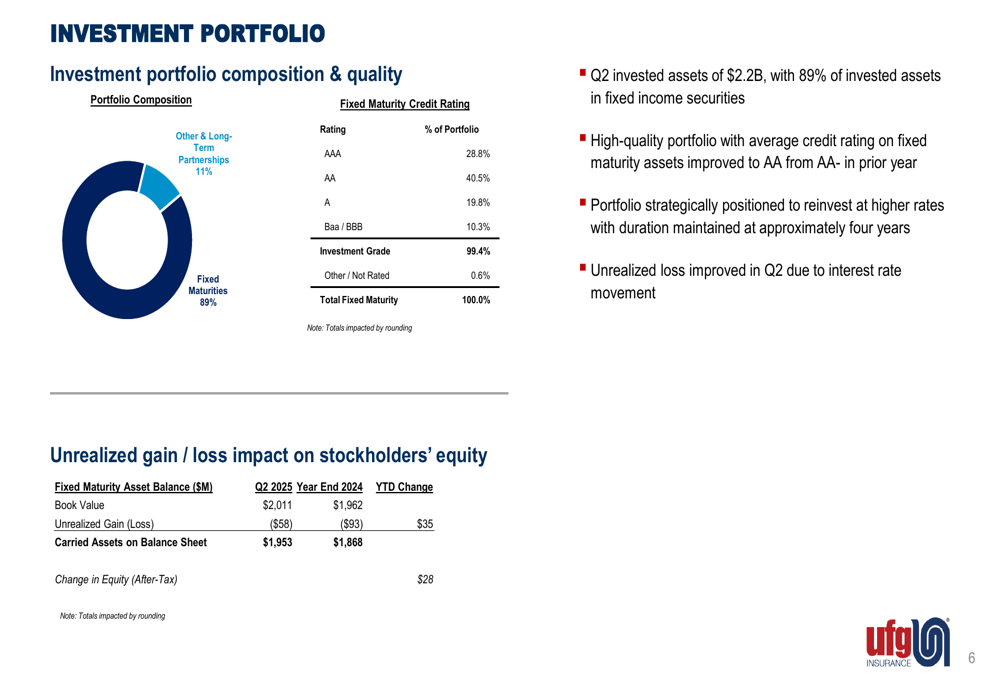

UFG’s investment portfolio remains a significant contributor to overall results. The company maintains a high-quality portfolio with 89% of its $2.2 billion in invested assets allocated to fixed income securities. The average credit rating on fixed maturity assets improved to AA from AA- in the prior year.

The portfolio composition and quality are illustrated here:

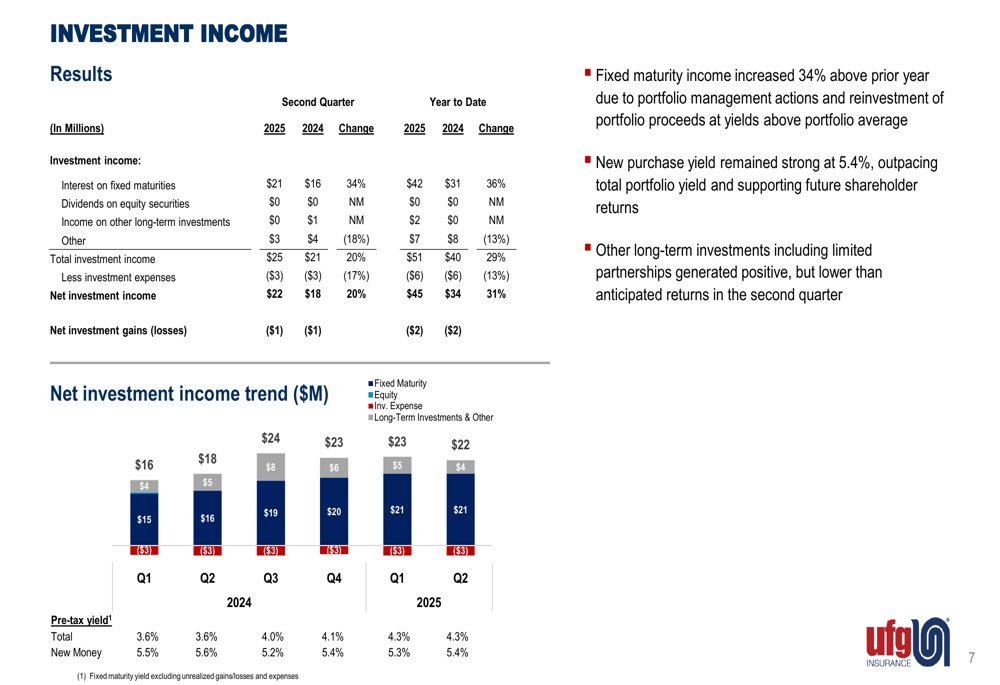

Investment income showed substantial improvement, with fixed maturity income increasing 34% year-over-year due to portfolio management actions and reinvestment at higher yields. The new purchase yield remained strong at 5.4%, outpacing the total portfolio yield and supporting future shareholder returns.

The following chart details the investment income performance:

Total (EPA:TTEF) investment income reached $25 million for Q2 2025, up from $21 million in Q2 2024, while net investment income increased to $22 million from $18 million in the same period last year. The strategic positioning of the portfolio, with duration maintained at approximately four years, allows the company to benefit from higher interest rates while managing risk.

Forward-Looking Statements

Building on the momentum from Q1, when CEO Kevin Leidwinger noted that "2025 is off to a promising start," the Q2 results demonstrate continued execution of the company’s strategy. The catastrophe losses for the year-to-date period remained below the full-year plan of 5.7%, positioning the company well for the second half of 2025.

The improvement in book value per share from $32.13 in Q1 to $33.18 in Q2, and in adjusted book value per share from $34.16 to $34.93, reflects the company’s strengthening financial position. With the unrealized loss position improving in Q2 due to interest rate movements, and the investment portfolio strategically positioned to reinvest at higher rates, UFG appears well-positioned to maintain its positive trajectory.

The company’s focus on disciplined pricing and risk selection, combined with process efficiency improvements, aligns with statements made during the Q1 earnings call about managing potential tariff impacts and maintaining pricing power. As noted in that call, "Our rates are currently exceeding our view of net loss trends," a trend that appears to have continued into Q2 with commercial rate increases of 7.6% still exceeding loss trends.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.