Nvidia, AMD to pay 15% of China chip sales revenue to US govt- FT

Introduction & Market Context

Uniti Group Inc (NASDAQ:UNIT) presented its first quarter 2025 financial results on May 6, 2025, highlighting year-over-year revenue growth of 3% and continued progress toward its planned merger with Windstream. Despite a slight earnings miss in the previous quarter, the company’s stock has shown resilience, trading at $5.00 as of May 5, 2025, with a market capitalization of approximately $1.4 billion.

The fiber infrastructure provider continues to position itself strategically in the growing market for high-speed connectivity, with particular emphasis on Tier II and III markets where competition is less intense. The company’s presentation focused on its improving financial metrics, strategic growth initiatives, and the transformative potential of its pending Windstream merger.

Quarterly Performance Highlights

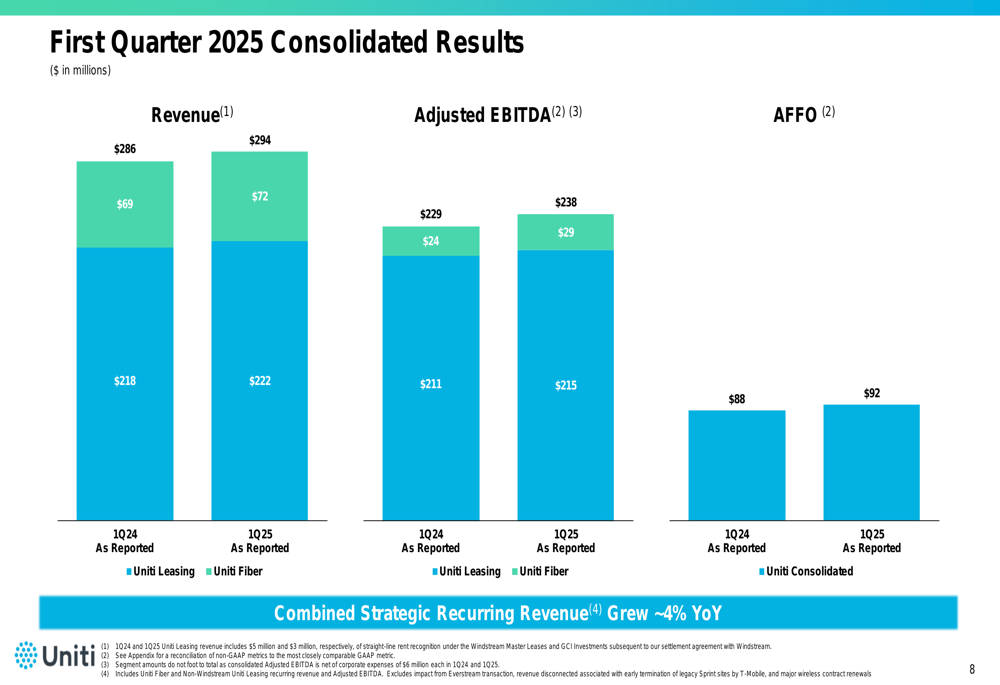

Uniti reported Q1 2025 revenue of $294 million, up from $286 million in the same period last year, representing a 3% increase. Adjusted EBITDA grew to $238 million from $229 million in Q1 2024, a 4% improvement. The company’s AFFO (Adjusted Funds From Operations) reached $92 million, compared to $88 million in the prior-year period.

As shown in the following consolidated results chart, both the Uniti Leasing and Uniti Fiber segments contributed to this growth:

The company highlighted that its combined strategic recurring revenue grew approximately 4% year-over-year, demonstrating the resilience of its core fiber business. This growth was primarily driven by wholesale and enterprise lease-up activities, which continue to be a focus area for the company.

Strategic Initiatives

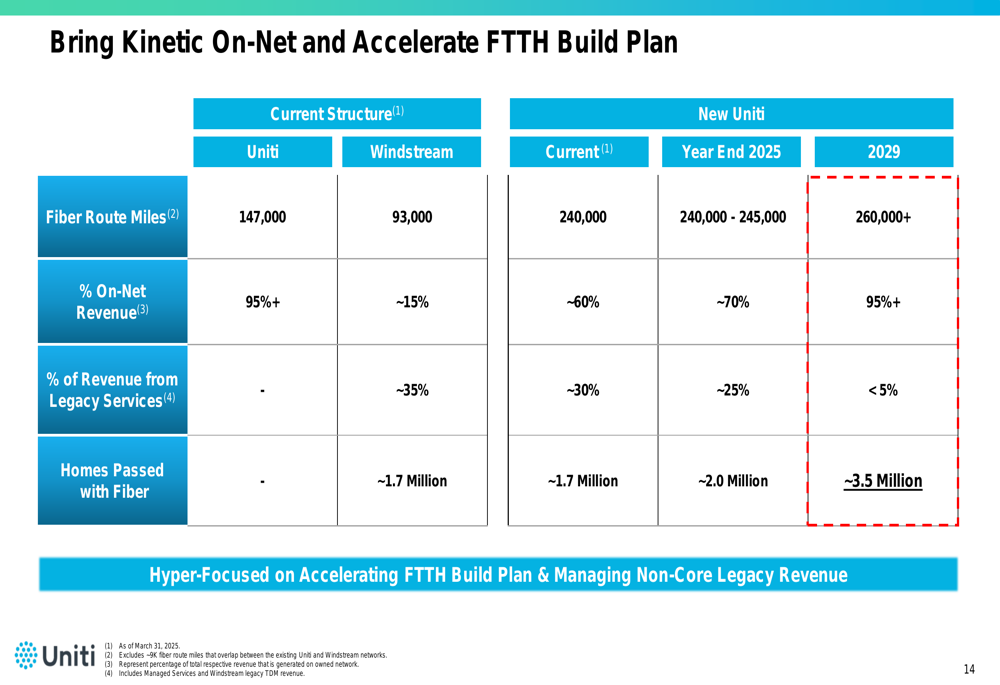

Central to Uniti’s strategy is the pending merger with Windstream, which is expected to close in the third quarter of 2025. This transaction will create what the company describes as a "Premier Insurgent Fiber Provider" with approximately 240,000 fiber route miles and connections to 4.4 million residential households.

The company’s 2025 priorities include continued best-in-class execution, optionality to fund its new business plan, and accelerating its fiber-to-the-home (FTTH) build plan through the Windstream integration. As illustrated in the following slide:

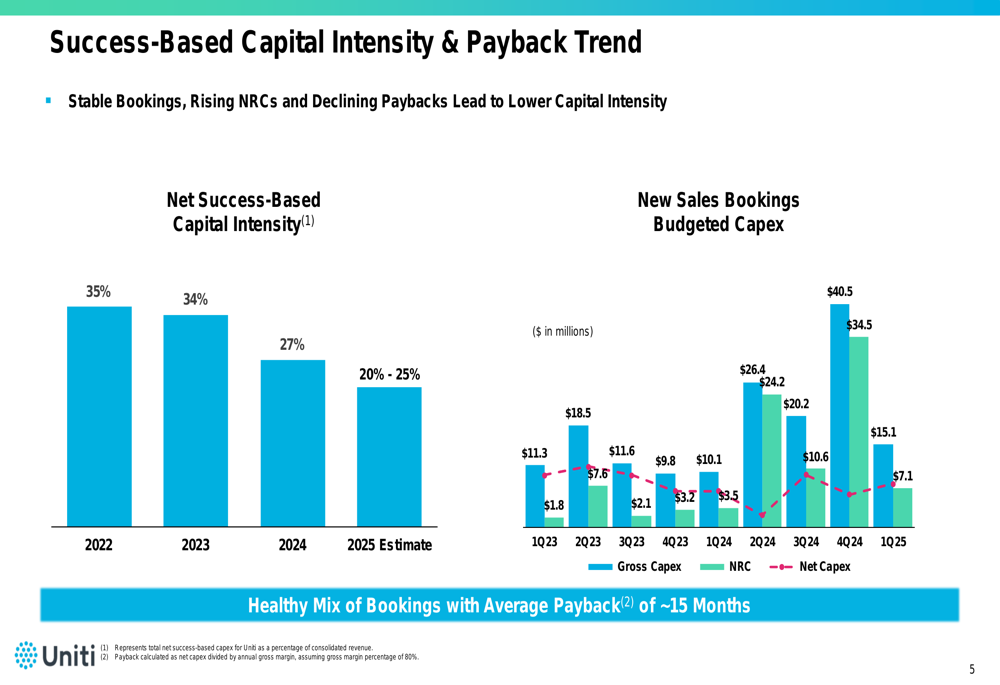

A key aspect of Uniti’s strategy is improving its financial efficiency. The company has made significant progress in reducing its capital intensity, with net success-based capital intensity projected to decline from 35% in 2022 to between 20% and 25% in 2025. This improvement is attributed to stable bookings, rising non-recurring charges (NRCs), and declining payback periods.

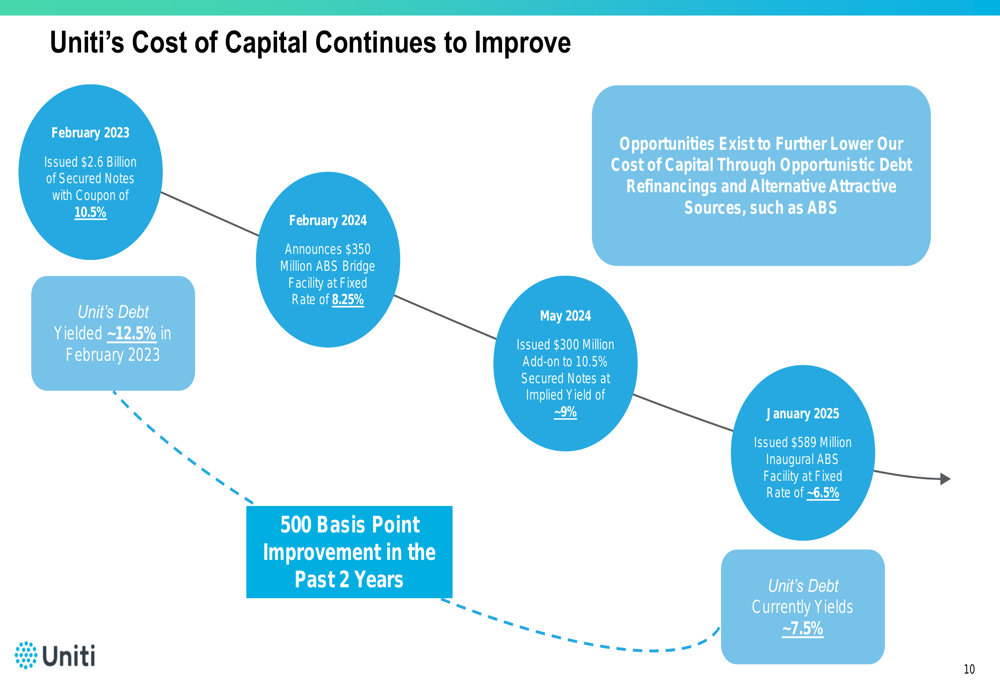

Additionally, Uniti has substantially improved its cost of capital over the past two years, reducing it by approximately 500 basis points from around 12.5% in February 2023 to approximately 7.5% currently. This improvement provides the company with greater financial flexibility and enhances its ability to fund growth initiatives.

Forward-Looking Statements

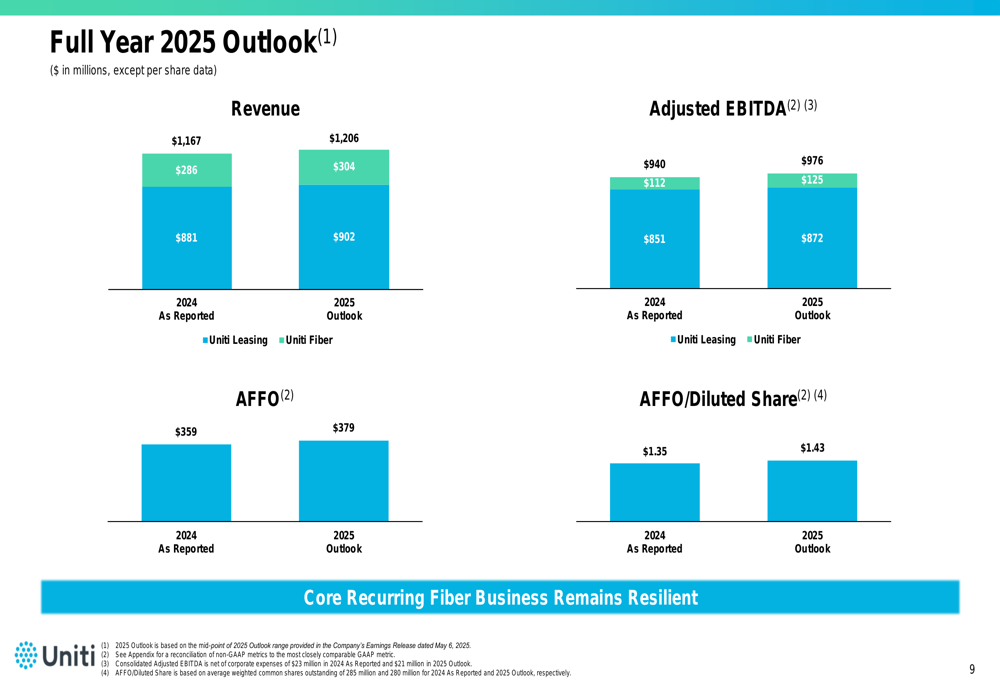

Uniti provided a detailed outlook for 2025, projecting full-year revenue of $1,206 million, adjusted EBITDA of $976 million, and AFFO of $379 million. This translates to an AFFO per diluted share of $1.43, representing a 6% increase from 2024.

The company is targeting strategic recurring revenue growth of 4-6% and strategic recurring adjusted EBITDA growth of 8-10% for 2025. These targets reflect Uniti’s focus on high-margin, recurring revenue streams and operational efficiency.

A significant component of Uniti’s forward strategy is the acceleration of its fiber-to-the-home (FTTH) build plan. Through the Windstream merger, the company expects to pass an incremental 325,000 homes with fiber in 2025, approximately double the prior year’s level, reaching a total of about 2 million homes. By 2029, Uniti aims to have approximately 3.5 million homes passed with fiber.

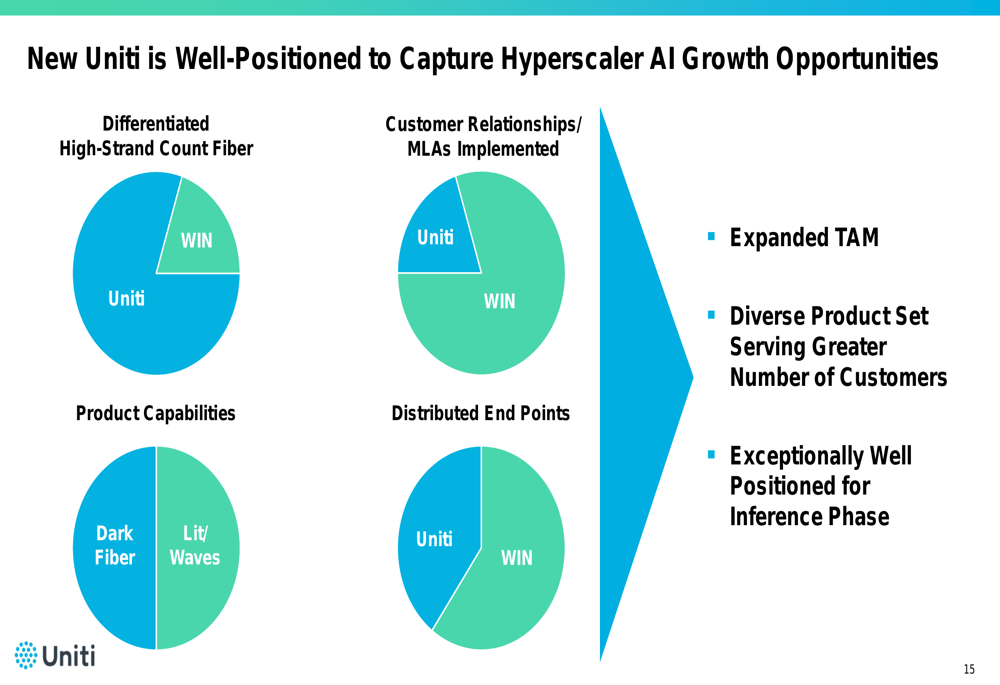

The company also highlighted its positioning to capture growth opportunities in the hyperscaler and AI markets. Uniti believes it is particularly well-positioned for the AI inference phase, which is expected to grow significantly as a percentage of the total AI market by 2030.

Competitive Industry Position

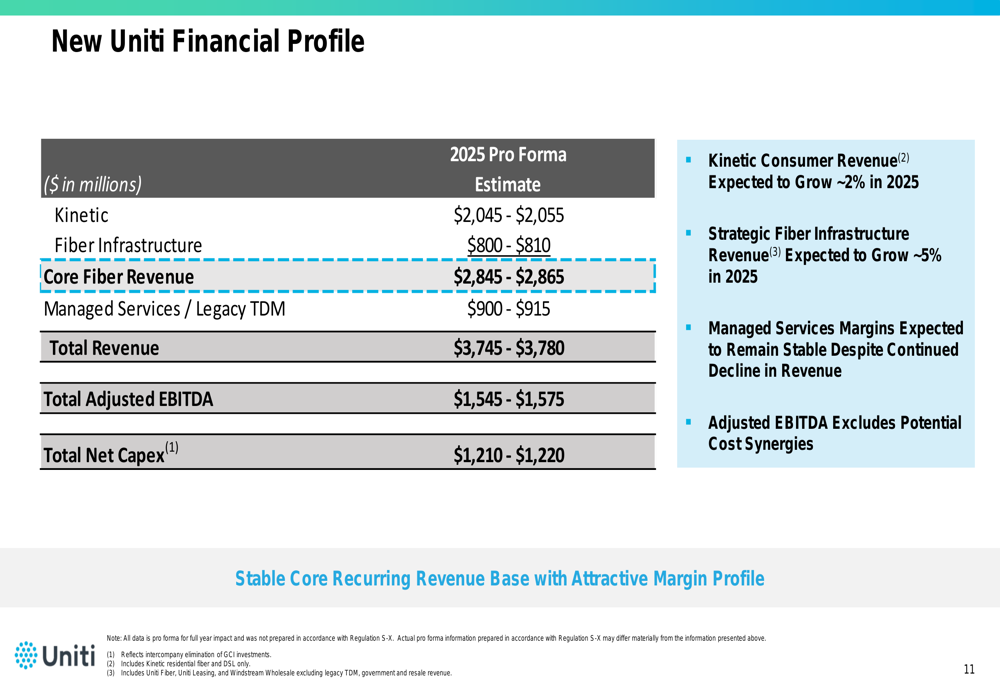

Following the Windstream merger, Uniti will present a new financial profile with multiple revenue streams. The combined entity is expected to generate between $3.745 billion and $3.780 billion in total revenue in 2025, with adjusted EBITDA between $1.545 billion and $1.575 billion.

The company emphasized that its combined Tier II and III market footprint creates a significant competitive advantage. These markets typically have less competition from major telecommunications providers, allowing Uniti to establish stronger market positions.

Uniti’s strategic focus on increasing the percentage of on-net revenue (revenue generated on its owned network) is expected to improve margins over time. The company aims to increase this metric from the current ~60% to ~70% by year-end 2025 and to more than 95% by 2029.

Risks and Challenges

While the presentation focused primarily on growth opportunities and strategic initiatives, there are several challenges that Uniti faces. The successful integration of Windstream following the merger will be critical, as will the execution of the accelerated FTTH build plan.

The company also faces competition in the fiber infrastructure market, particularly as demand for high-speed connectivity continues to grow. Additionally, economic uncertainties and interest rate fluctuations could affect financing costs, despite the company’s improved cost of capital.

Regulatory changes in the telecommunications sector could also impact Uniti’s operations and growth plans. The company will need to navigate these challenges while executing on its strategic initiatives to deliver the projected financial results.

In conclusion, Uniti’s Q1 2025 presentation portrays a company in transition, with steady financial growth and a clear strategic direction centered around the Windstream merger and fiber infrastructure expansion. The coming quarters will be critical as the company works to close the merger and begin realizing the anticipated synergies and growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.