Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

Universal Insurance Holdings (NYSE:UVE) presented its second-quarter 2025 financial results on July 24, revealing a mixed performance that sent shares down 7.43% in after-hours trading. The company reported adjusted earnings per share of $1.23, beating analyst expectations of $1.12, but posted revenue of $400.14 million, significantly below the forecasted $595.62 million.

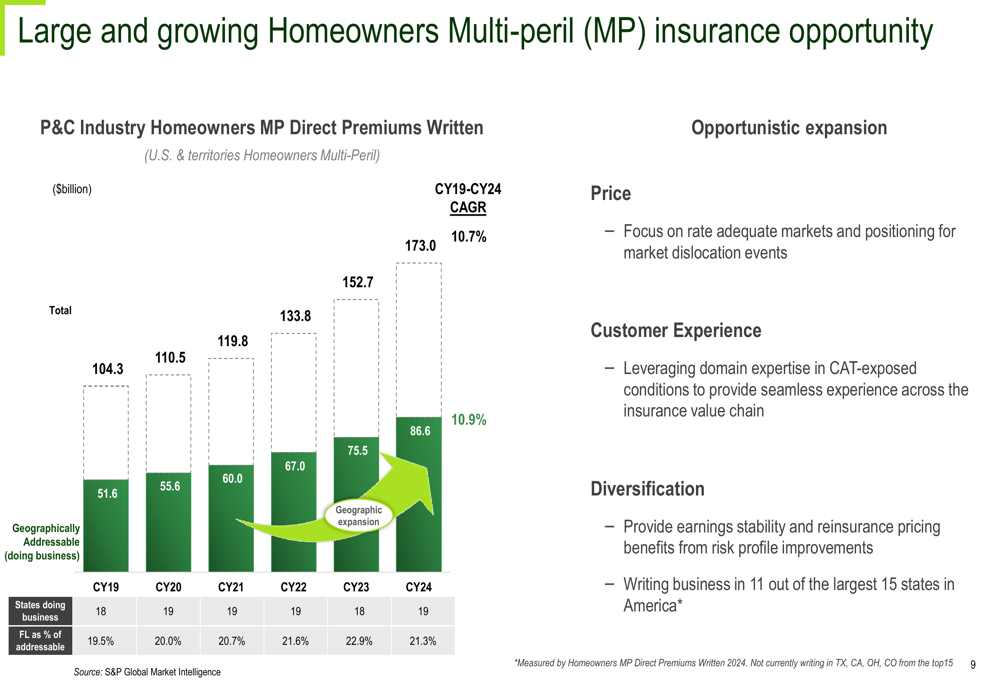

The homeowners insurance market continues to present both opportunities and challenges, with industry-wide premiums growing at a 10.7% CAGR from 2019 to 2024, reaching $173 billion. Universal Insurance has maintained its position as a significant player in this expanding market, particularly in Florida where it holds an 8.0% market share.

As shown in the following chart of the homeowners multi-peril insurance opportunity:

Quarterly Performance Highlights

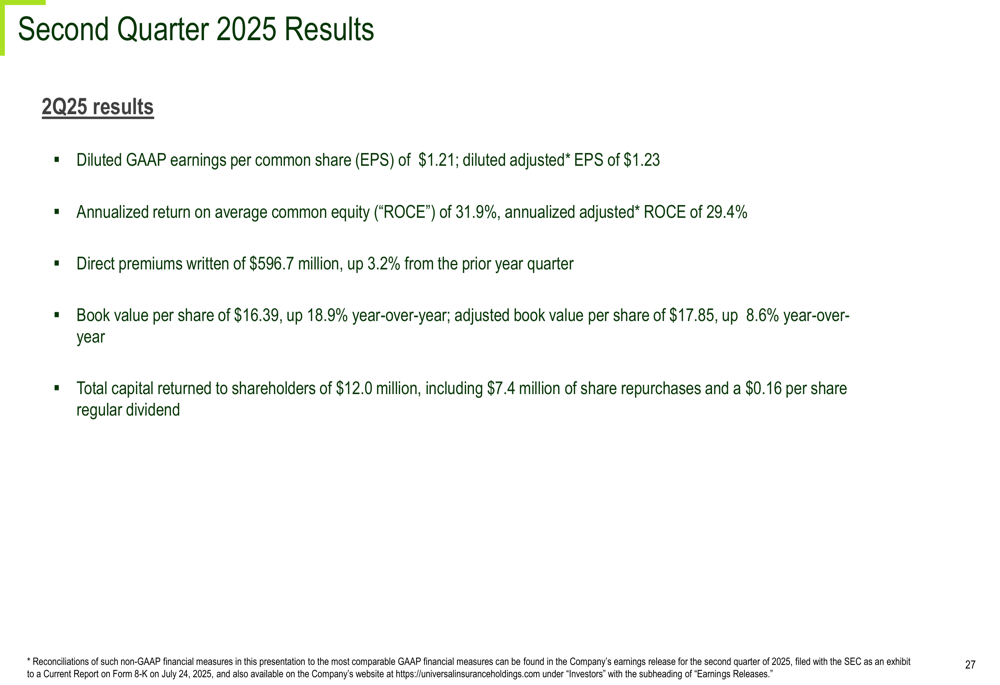

Universal Insurance reported direct premiums written of $596.7 million in Q2 2025, representing a 3.2% increase from the prior year quarter. The company achieved diluted adjusted earnings per share of $1.23, driving an annualized return on average common equity (ROCE) of 31.9% (29.4% on an adjusted basis).

Book value per share reached $16.39, up 18.9% year-over-year, while adjusted book value per share grew to $17.85, an 8.6% increase. During the quarter, the company returned $12.0 million to shareholders through $7.4 million in share repurchases and a $0.16 per share regular dividend.

The key quarterly results are summarized in the following slide:

Despite these positive metrics, the significant revenue shortfall raises concerns about operational execution. The company’s net combined ratio increased to 97.8%, up 1.9 percentage points, with the net loss ratio rising to 72.3%, up 1.7 points. These increases suggest growing cost pressures that could impact future profitability.

Strategic Initiatives

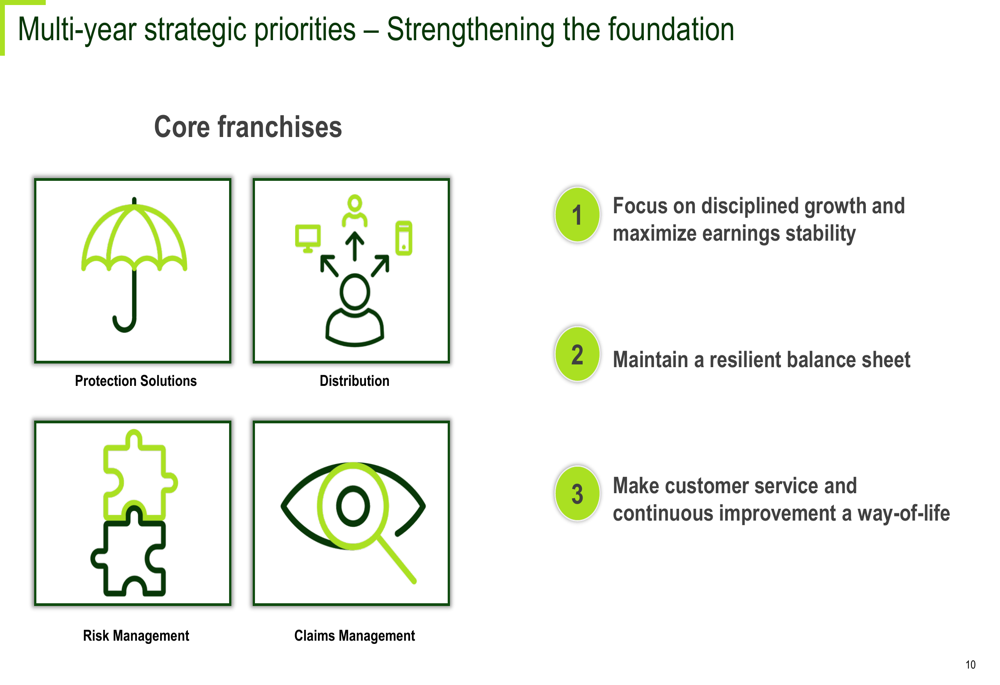

Universal Insurance continues to focus on three key strategic priorities: disciplined growth with earnings stability, maintaining a resilient balance sheet, and enhancing customer service. The company operates across four core franchises: Protection Solutions, Distribution, Risk Management, and Claims Management.

The company’s strategic priorities are illustrated in this slide:

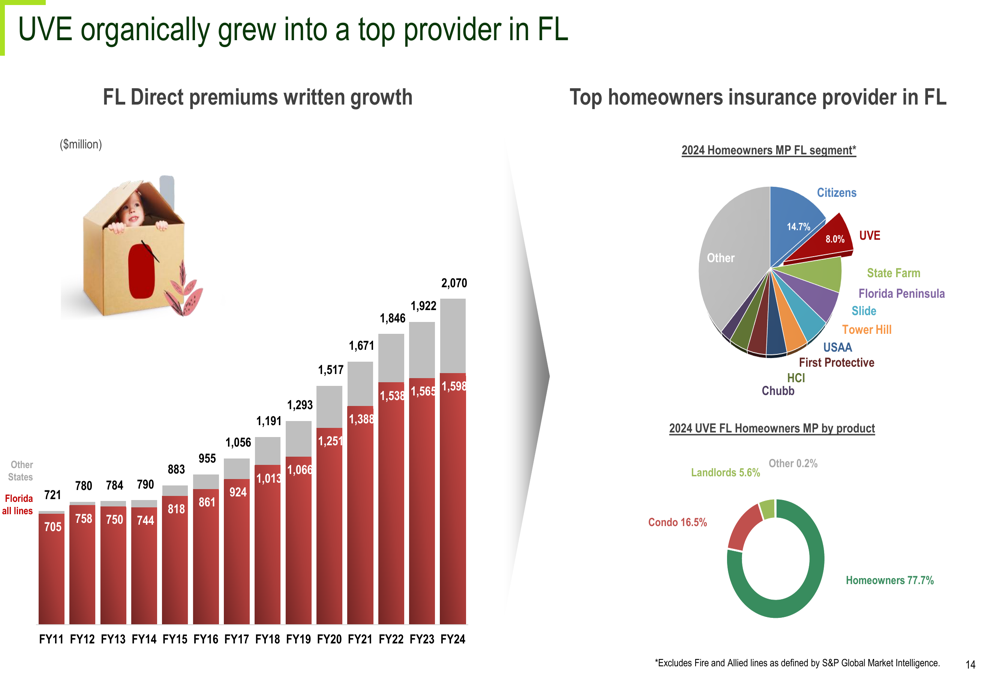

Geographic diversification remains a central component of Universal’s growth strategy. While Florida remains its primary market, the company now operates in 19 states, gradually reducing its concentration risk. This expansion is supported by a multi-product approach that includes homeowners, condo, and landlord insurance policies.

The company’s market position in Florida is detailed in the following chart:

CEO Steve Donaghy emphasized the company’s strategic focus during the earnings call, stating, "We are not driven by the competition. We are driven by twenty-five years of experience in Florida." This statement underscores the company’s confidence in its established markets while pursuing measured expansion.

Financial Analysis

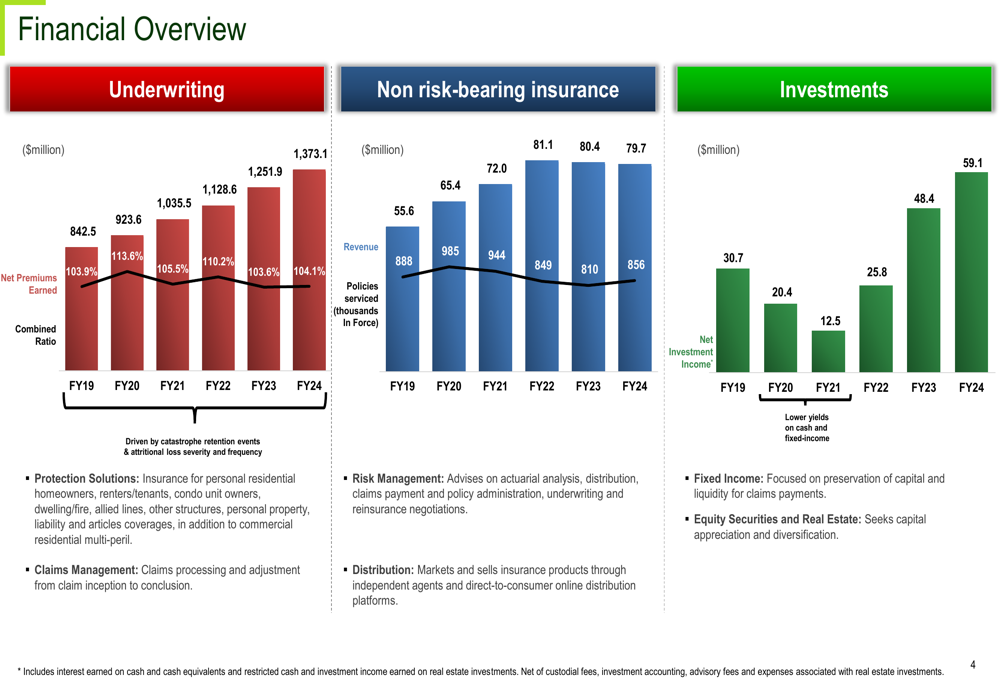

Universal Insurance has demonstrated consistent financial growth over the past several years, with net premiums earned increasing from $842.5 million in FY19 to $1,373.1 million in FY24. However, the combined ratio has remained above 100% during this period, reaching 104.1% in FY24, indicating underwriting losses.

The company’s financial performance across key segments is shown in this comprehensive overview:

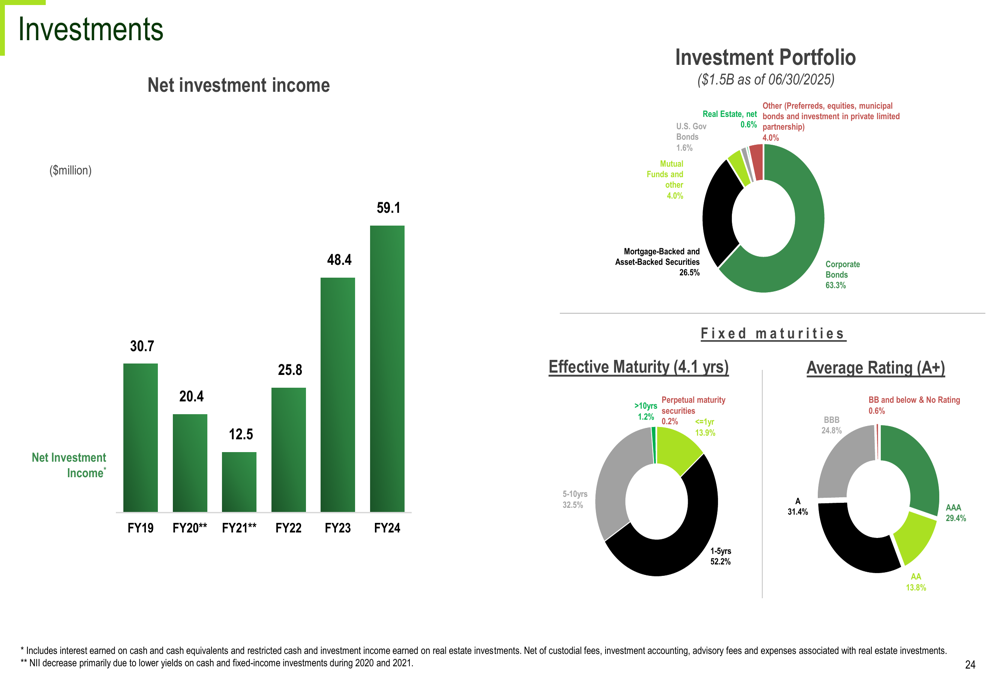

The investment portfolio, valued at $1.5 billion as of June 30, 2025, is primarily allocated to fixed income securities, with 63.3% in corporate bonds and 26.5% in mortgage-backed and asset-backed securities. The portfolio has an effective maturity of 4.1 years and an average rating of A+, providing a stable foundation for the company’s operations.

The investment allocation is detailed in the following chart:

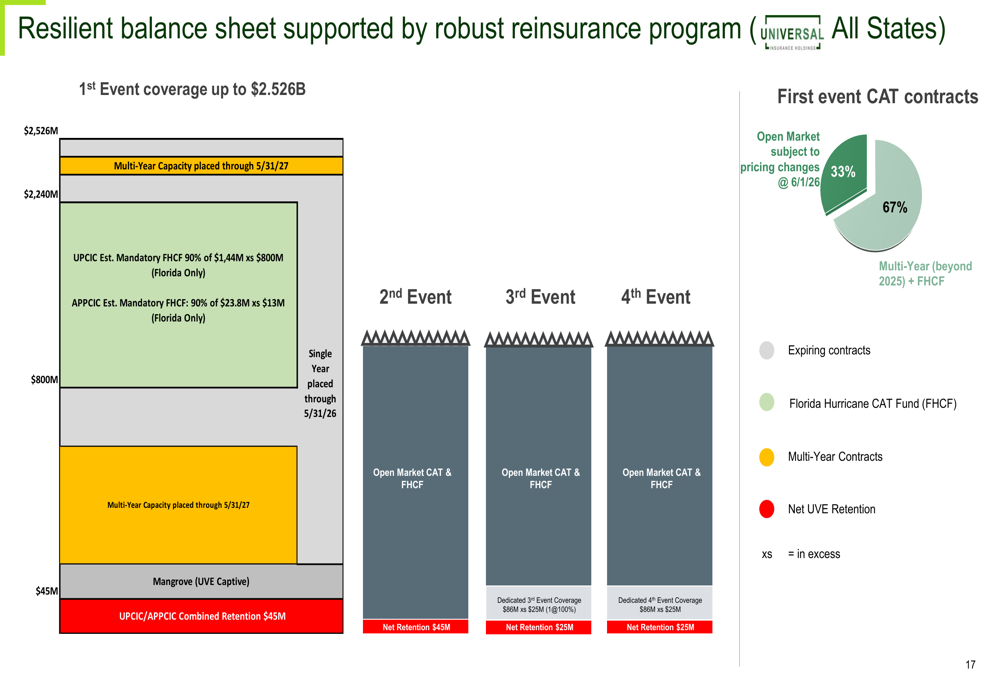

Universal’s balance sheet is further strengthened by its reinsurance program, which provides first event coverage up to $2.526 billion. This program, comprising 67% multi-year contracts and 33% expiring contracts, helps mitigate catastrophe risk, particularly important given the company’s significant Florida exposure.

The reinsurance structure is illustrated in this slide:

Forward-Looking Statements

Despite the revenue challenges in Q2, Universal Insurance remains optimistic about its future performance. The company expects continued growth through its multi-state expansion strategy and product diversification efforts. Analyst consensus maintains a "Buy" recommendation with a price target of $29, suggesting potential upside from current levels.

CFO Frank Wilcox highlighted the company’s financial stability during the earnings call, noting that "the holding company capital is abundant." This statement aims to reassure investors about the company’s ability to weather market volatility and support its growth initiatives.

However, investors should consider several risk factors, including the significant revenue shortfall in Q2, increasing competition in the Florida market, rising combined and loss ratios, and broader economic conditions that could impact future growth. The company’s ability to address these challenges while executing its expansion strategy will be critical to its long-term success.

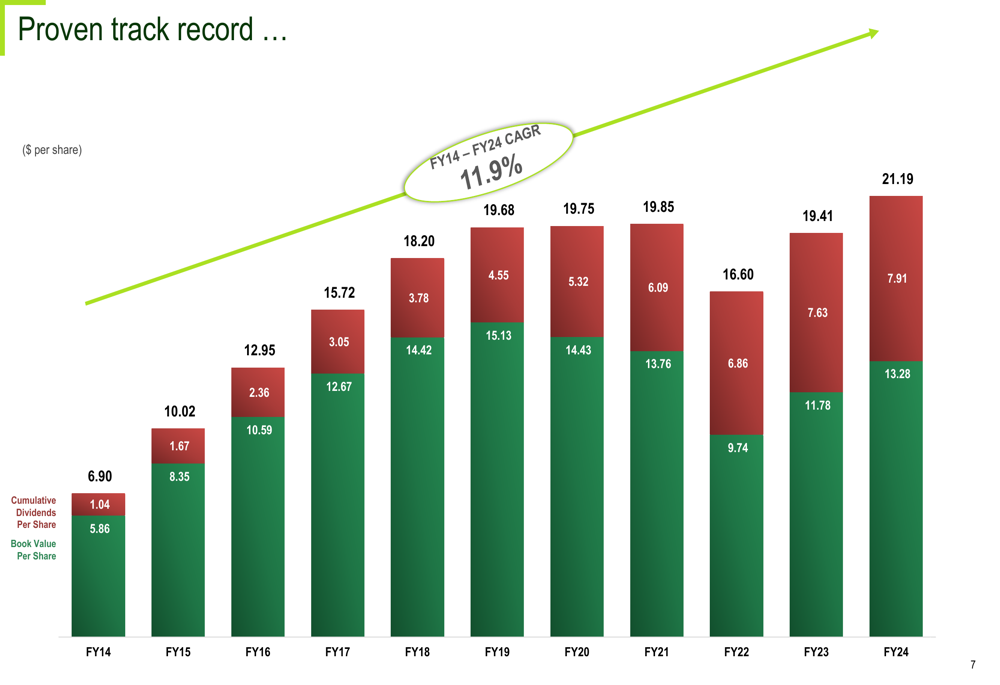

Universal Insurance’s long-term performance shows a proven track record of growth, with an 11.9% CAGR from FY14 to FY24 and consistent increases in book value per share and cumulative dividends:

As Universal Insurance navigates the competitive homeowners insurance landscape, its established market position, geographic diversification strategy, and strong capital position provide a foundation for potential growth, though revenue execution remains a key area to monitor in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.