Figma Shares Indicated To Open $105/$110

Introduction & Market Context

Upstart Holdings Inc (NASDAQ:UPST) released its Q1 2025 earnings presentation on May 6, showcasing significant year-over-year growth in loan originations and revenue. Despite these strong results, the company’s shares plummeted 15.12% in after-hours trading to $43.63, suggesting investors may be concerned about declining contribution margins and sequential guidance for Q2.

The AI-powered lending platform reported near-breakeven GAAP results while continuing to expand its product offerings across personal loans, auto loans, and home equity lines of credit. This quarter marks a continuation of the growth trajectory seen in Q3 2024, when the company reported a 43% sequential increase in lending volume.

Quarterly Performance Highlights

Upstart delivered substantial growth in Q1 2025, with loan originations reaching $2.1 billion, representing an 89% year-over-year increase. Total (EPA:TTEF) revenue climbed to $213 million, up 67% compared to the same period last year. The company reported a GAAP net loss of just $2 million, described as "near breakeven," while Adjusted EBITDA reached $43 million, equating to a 20% margin.

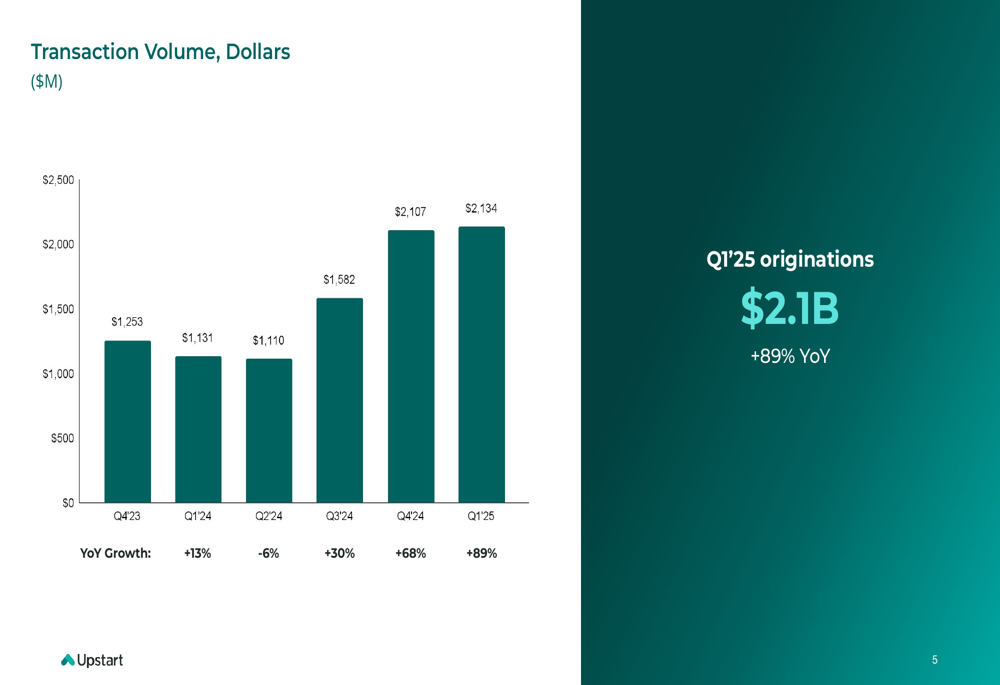

As shown in the following chart of quarterly transaction volume:

The company’s transaction volume has grown consistently over the past several quarters, with Q1 2025 originations of $2.13 billion representing an 89% year-over-year increase from the $1.13 billion reported in Q1 2024.

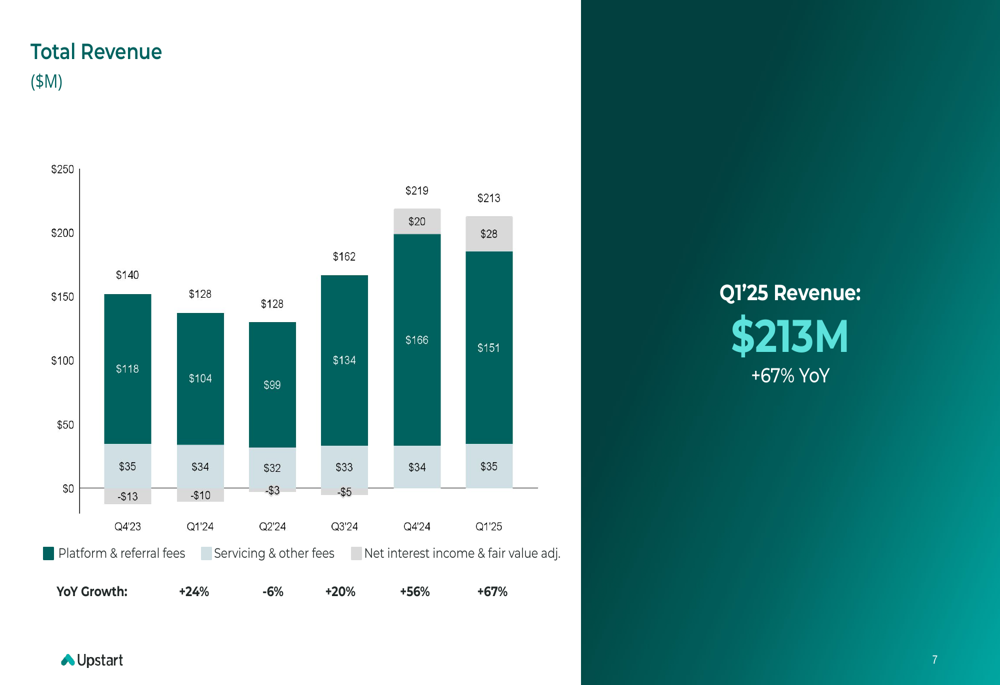

Revenue growth has similarly been strong, with a detailed breakdown of revenue components showing positive trends across platform fees, servicing fees, and net interest income:

Notably, Upstart has turned the corner on net interest income, which was negative in earlier quarters but contributed $28 million in Q1 2025, helping drive the overall revenue growth to $213 million.

Product and Segment Performance

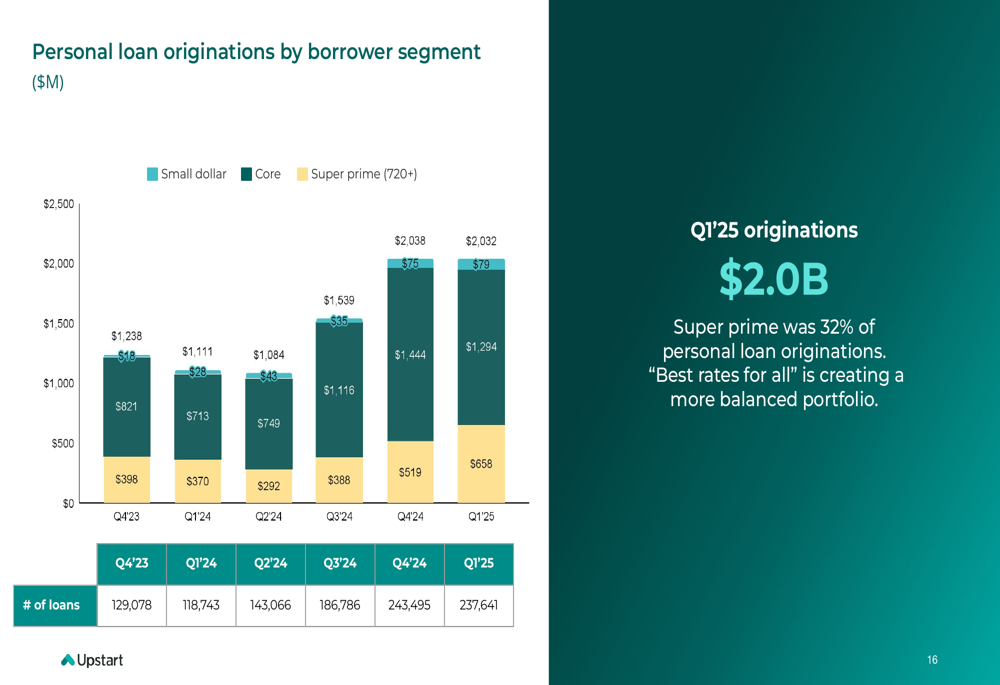

Upstart’s strategy of diversifying across borrower segments and loan products showed significant progress in Q1 2025. The company’s personal loan business remains the core revenue driver, with originations of $2.03 billion in Q1 2025, representing 83% year-over-year growth.

The borrower segment mix has evolved substantially, as illustrated in this breakdown:

Super prime borrowers (those with credit scores of 720+) accounted for 32% of personal loan originations in Q1 2025, growing to $179 million from just $28 million a year earlier. This shift reflects Upstart’s "Best rates for all" strategy, which aims to create a more balanced portfolio across credit tiers.

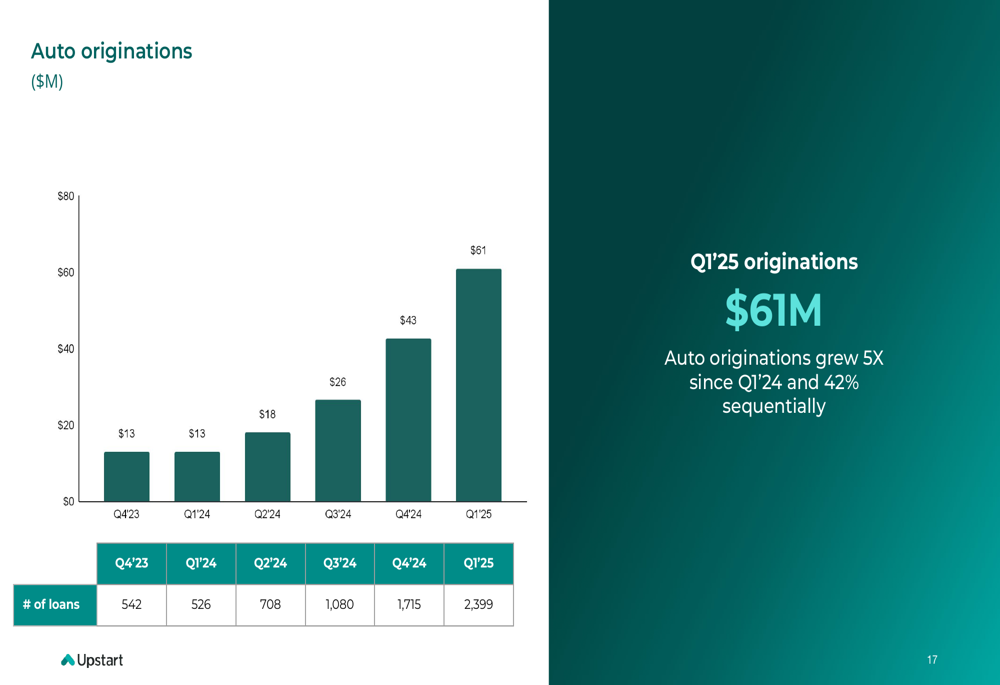

The company’s newer product lines showed impressive growth as well. Auto loan originations reached $61 million in Q1 2025:

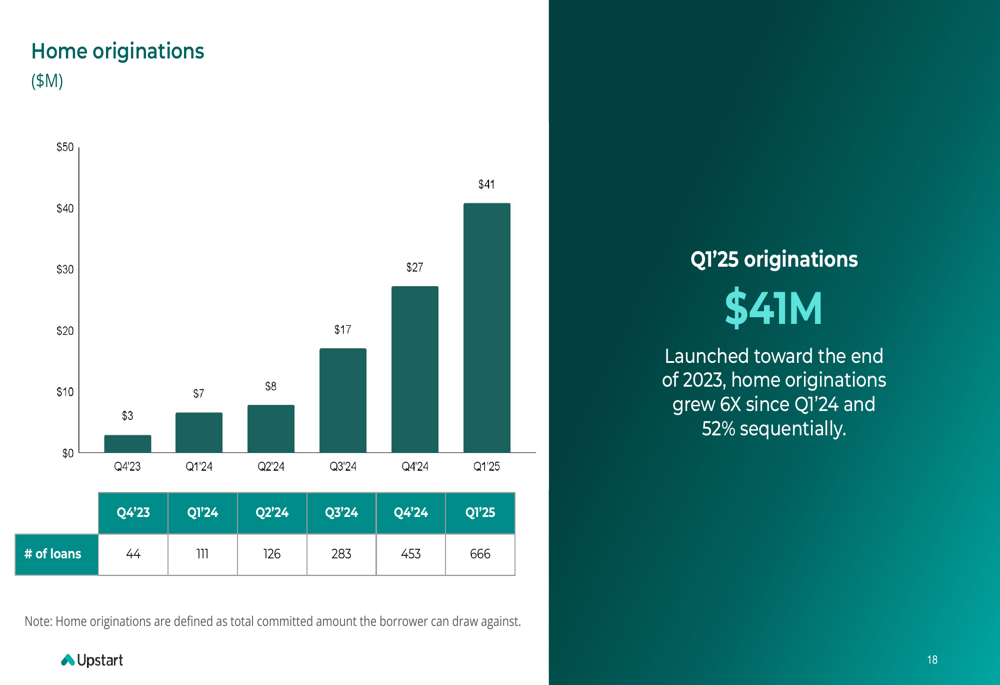

This represents a five-fold increase since Q1 2024 and 42% sequential growth from Q4 2024. Similarly, home loan originations grew to $41 million:

Home originations, which were launched toward the end of 2023, have grown six-fold since Q1 2024 and 52% sequentially from the previous quarter.

Technology and AI Advancements

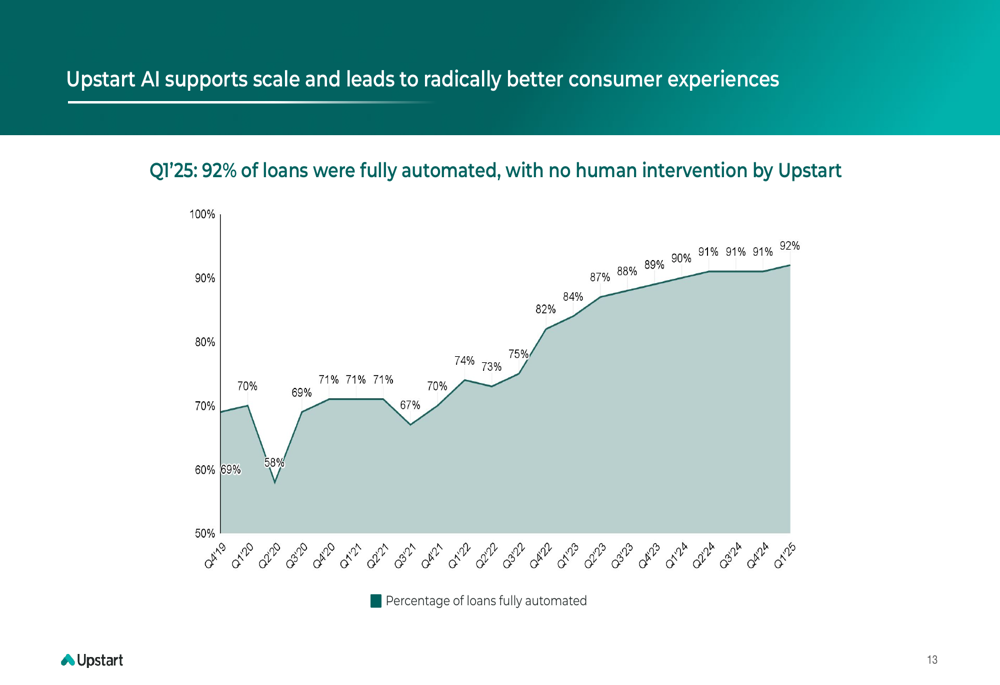

A key competitive advantage for Upstart continues to be its AI-powered automation capabilities. In Q1 2025, 92% of loans were fully automated with no human intervention, continuing a steady upward trend:

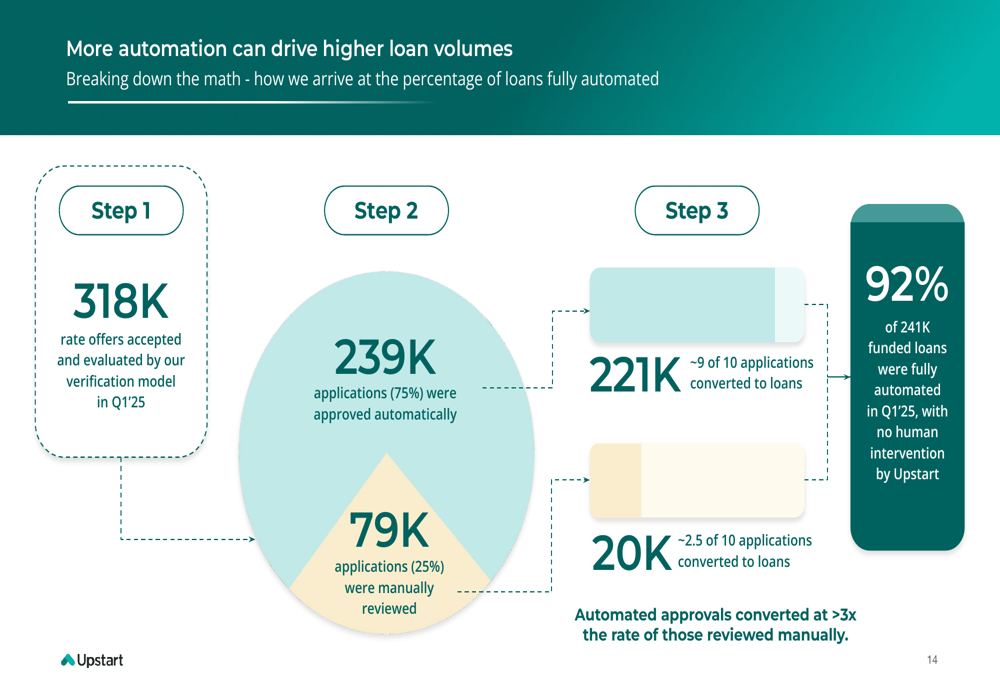

The company highlighted that automated approvals converted at more than three times the rate of manually reviewed applications, demonstrating the efficiency of its AI systems:

Upstart also introduced embedding algorithms into its core personal loan underwriting model during the quarter. This machine learning technique converts complex, unstructured data into useful model inputs, helping uncover subtle patterns that improve model generalization and accuracy.

Financial Health and Capital Partnerships

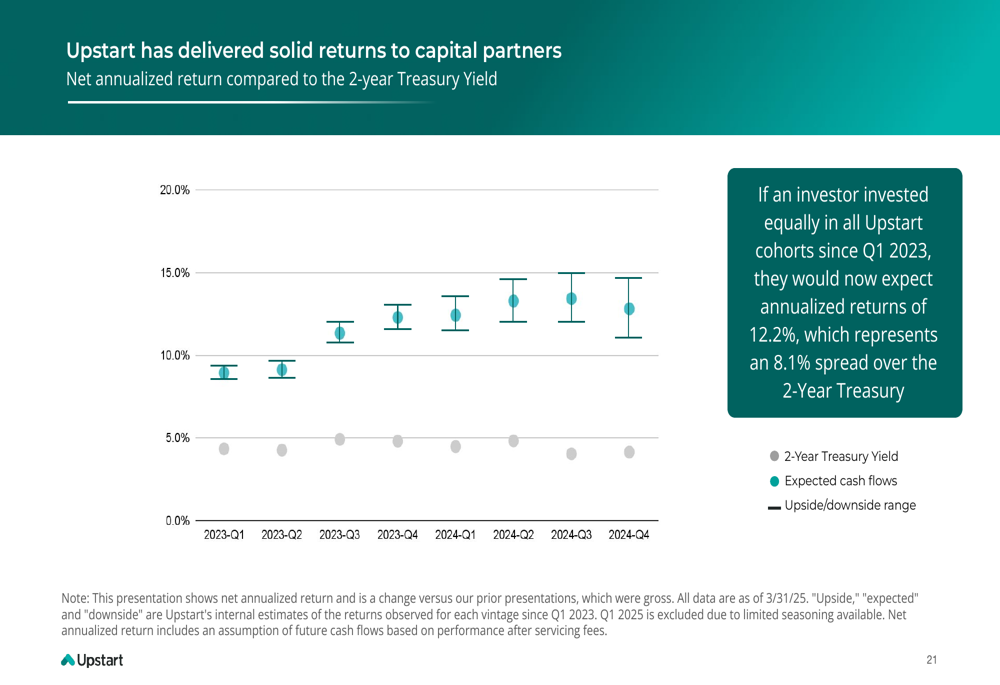

Upstart reported that its capital partners have received solid returns on their investments. If an investor had invested equally in all Upstart cohorts since Q1 2023, they would now expect annualized returns of 12.2%, representing an 8.1% spread over the 2-Year Treasury:

The company’s co-investments in committed capital partnerships increased to $526 million in Q1 2025, with a current assessed value of $564 million. This represents a significant increase from $433 million in the previous quarter.

Outlook and Guidance

For Q2 2025, Upstart provided the following guidance:

The company expects total revenue of $225 million, representing a modest sequential increase from Q1’s $213 million. However, Adjusted EBITDA is projected at $37 million (19% margin), down from the $43 million (20% margin) achieved in Q1. For the full year 2025, Upstart forecasts total revenue of $1.01 billion and expects to achieve positive GAAP net income in the second half of 2025 and for the full year.

Market Response and Analysis

Despite the strong year-over-year growth metrics, Upstart’s stock dropped sharply in after-hours trading following the earnings release. Several factors may have contributed to this negative reaction:

1. Contribution margin decreased to 55% in Q1 2025 from 61% in Q4 2024. The company attributed this to "faster expansion into super-prime and new products than anticipated."

2. The Q2 2025 guidance shows a sequential decline in Adjusted EBITDA from $43 million to $37 million, which may have disappointed investors expecting continued sequential improvement.

3. While the company is approaching GAAP profitability, the $2 million net loss in Q1 2025 may have fallen short of some analysts’ expectations given the strong revenue growth.

The market reaction suggests investors may be concerned about the sustainability of Upstart’s growth trajectory and its path to consistent profitability, despite the company’s significant progress in diversifying its loan portfolio and improving its AI capabilities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.