Trump/Cook, Nissan weakness, more tariffs and gold - what’s moving markets

Introduction & Market Context

Velocity Financial Inc. (NYSE:VEL) reported strong second-quarter 2025 results on August 7, showcasing significant improvement across key financial metrics compared to both the previous quarter and the same period last year. The company’s stock closed at $16.33, down 1.03% on the day of the earnings release, a notably milder reaction compared to the 10.36% drop following its Q1 results.

The Q2 performance represents a substantial improvement from the first quarter, when Velocity missed EPS forecasts but beat on revenue. The latest results demonstrate the company’s continued progress toward its stated goal of growing its loan portfolio to $10 billion over the next five years.

Quarterly Performance Highlights

Velocity Financial reported impressive earnings growth in the second quarter of 2025, with net income reaching $26.0 million, a 75.9% increase from Q2 2024. Diluted earnings per share rose to $0.69, up from $0.42 in the same period last year. Core net income, which adjusts for equity award and ESPP costs, grew 72.6% year-over-year to $27.5 million, with core diluted EPS of $0.73 compared to $0.45 in Q2 2024.

As shown in the following chart of Velocity’s key Q2 2025 highlights, the company demonstrated strong performance across earnings, production, loan portfolio, and financing metrics:

The company’s portfolio net interest margin (NIM) improved significantly to 3.82% in Q2 2025, representing an increase of 47 basis points from Q1 2025 and 28 basis points from Q2 2024. This marks a substantial improvement from the 3.35% NIM reported in Q1 2025, as mentioned in the company’s previous earnings report.

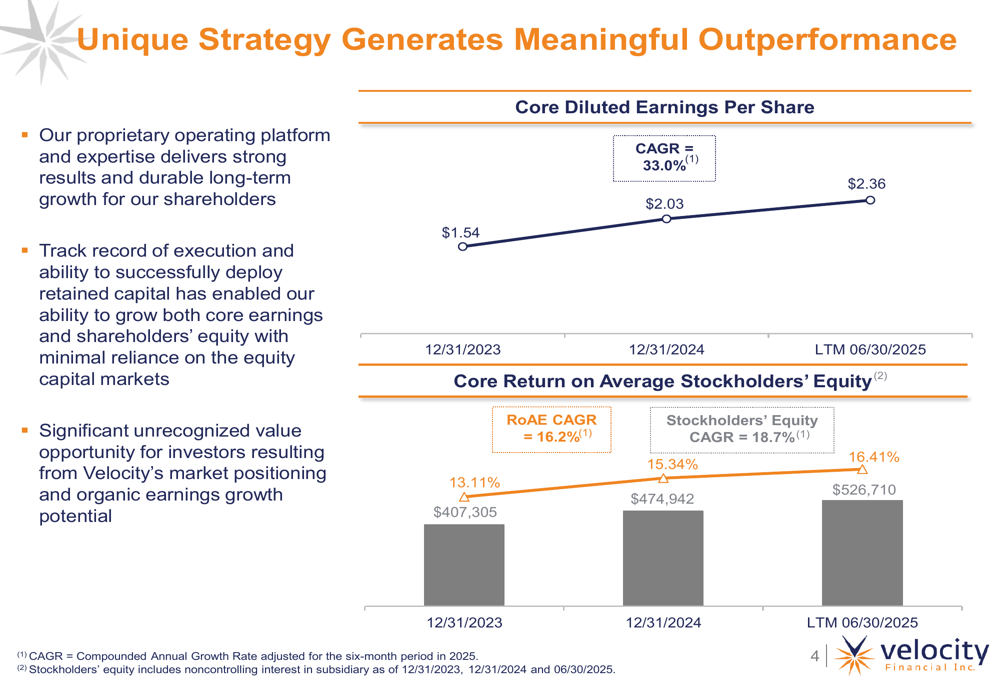

Velocity’s unique business strategy has delivered consistent growth in core earnings and returns on equity. Core diluted earnings per share have grown at a compound annual growth rate of 33.0% from December 31, 2023, to June 30, 2025, while core return on average stockholders’ equity has improved from 13.11% to 16.41% over the same period.

The following chart illustrates this consistent growth trajectory:

Book value metrics also showed solid improvement, with diluted book value per share reaching $15.62 as of June 30, 2025, a 5.1% increase from $14.87 at the end of the previous quarter. Adjusted diluted book value per share, which reflects the estimated fair value of loans carried at amortized cost, stood at $17.60.

Loan Production and Portfolio Growth

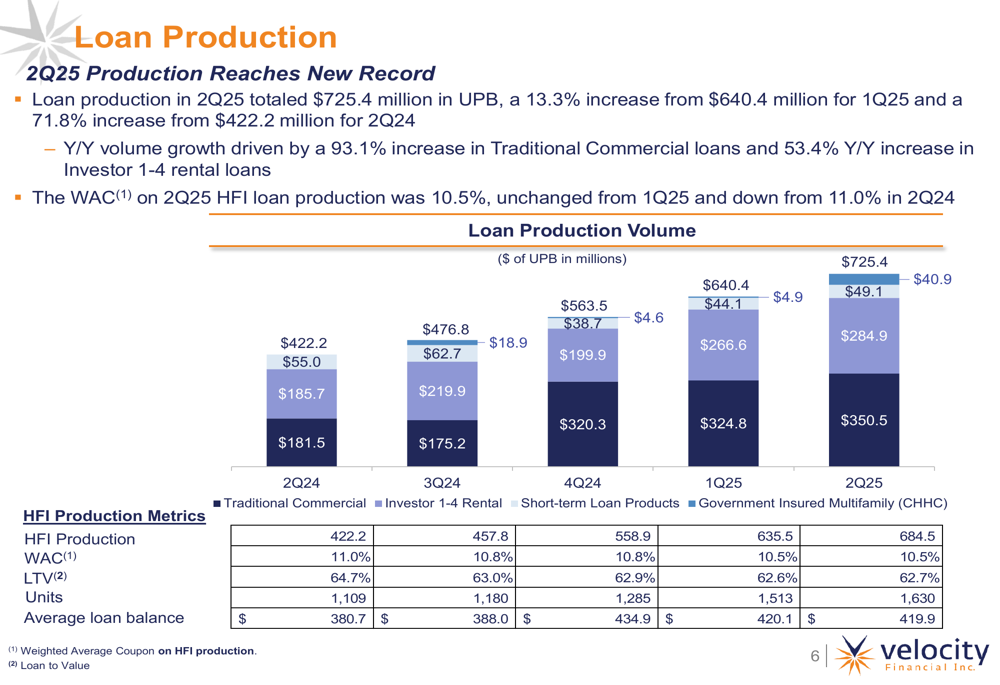

Velocity Financial achieved record loan production in Q2 2025, originating $725.4 million in unpaid principal balance (UPB), representing a 13.3% increase from Q1 2025 and a remarkable 71.8% increase from Q2 2024. This growth was primarily driven by a 93.1% year-over-year increase in Traditional Commercial loans and a 53.4% increase in Investor 1-4 rental loans.

The weighted average coupon (WAC) on Q2 2025 held-for-investment loan production remained stable at 10.5%, unchanged from Q1 2025 and down from 11.0% in Q2 2024, suggesting the company has maintained pricing discipline despite the competitive environment.

The following chart details Velocity’s loan production volume by product type over the past five quarters:

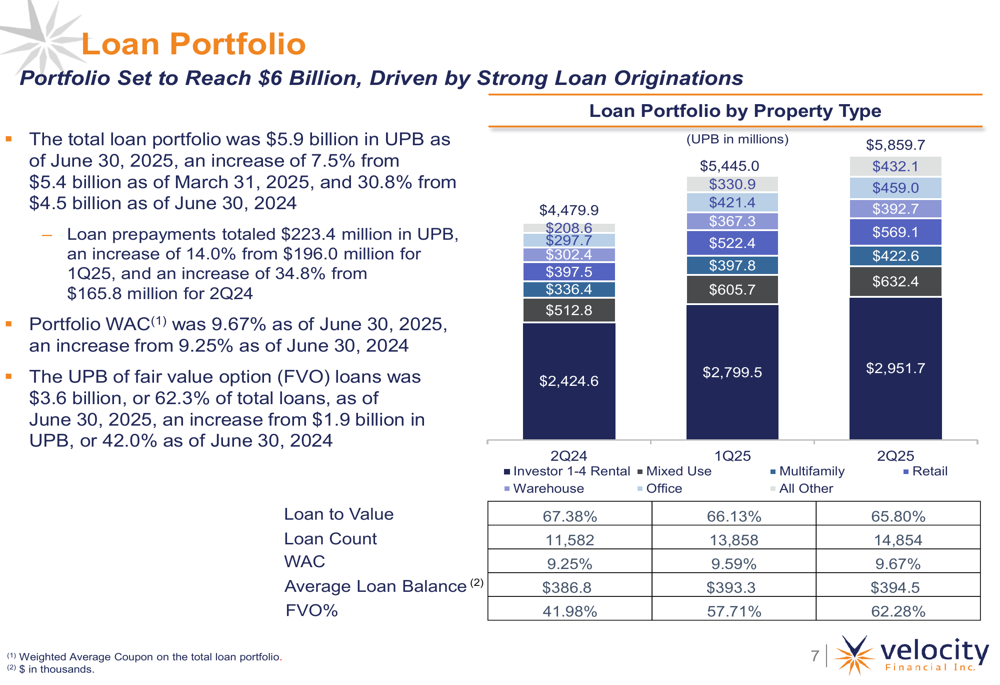

The total loan portfolio reached $5.9 billion in UPB as of June 30, 2025, up 7.5% from March 31, 2025, and 30.8% from June 30, 2024. This represents continued progress from the $5.5 billion reported at the end of Q1 2025, confirming the company’s growth trajectory.

The portfolio remains well-diversified across property types, with Investor 1-4 Rental properties representing the largest segment at 50.4% of the total portfolio. The portfolio’s weighted average coupon was 9.67% as of June 30, 2025, up from 9.25% a year earlier.

The following chart illustrates the composition and growth of Velocity’s loan portfolio:

Credit Quality and Asset Performance

Velocity Financial reported improvements in credit quality during Q2 2025. Nonperforming loans (NPLs) as a percentage of total held-for-investment loans decreased to 10.3% as of June 30, 2025, down from 10.8% in the previous quarter and 10.5% in Q2 2024.

The company’s non-performing asset resolution activities were particularly strong in Q2 2025, with resolutions totaling $104.0 million in UPB and realizing 103.5% of UPB resolved. This represents a gain of 3.5% on resolutions, up from 2.4% in Q1 2025 and 1.3% in Q2 2024. The UPB of loans resolved in Q2 2025 represented 17.7% of nonperforming loan UPB as of March 31, 2025.

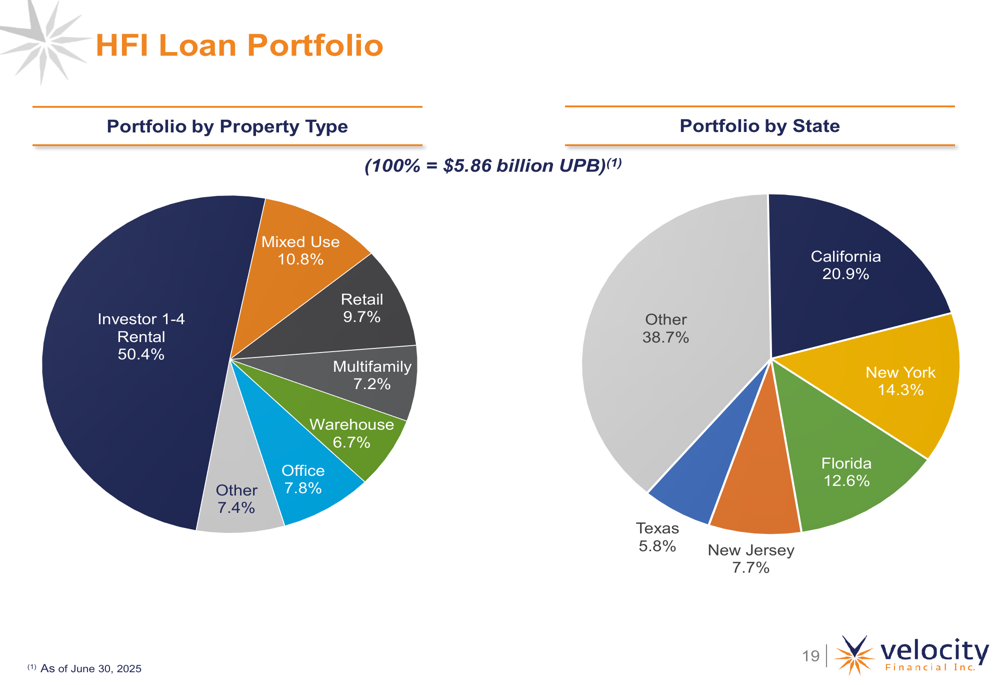

The geographic distribution of Velocity’s loan portfolio shows concentration in key real estate markets, with California (20.9%), New York (14.3%), and Florida (12.6%) representing the largest state exposures. This diversification helps mitigate regional real estate market risks.

The following pie charts illustrate the company’s portfolio diversification by property type and state:

Funding Strategy and Liquidity

Velocity Financial maintained a strong liquidity position while executing an active securitization strategy in Q2 2025. The company completed four securitizations totaling $985.5 million, including the VCC 2025-2 and 2025-3 securitizations totaling $760.0 million with a weighted average rate of 6.6%.

Additionally, Velocity refinanced an existing mixed collateral securitization and collapsed and refinanced two securitizations totaling $68.0 million in debt outstanding, releasing $53.5 million of capital. These activities helped reduce the company’s recourse debt to equity ratio to 1.0x, down from 1.5x as of March 31, 2025.

Liquidity reached $139.2 million as of June 30, 2025, with $79.6 million in unrestricted cash and $59.7 million in available borrowings. The company also maintained $476.9 million in available non-mark-to-market warehouse line capacity, providing significant flexibility for future loan originations.

Forward-Looking Statements

Looking ahead, Velocity Financial provided a positive outlook for its key business drivers. The company expects the investor loan market to continue growing, with broker engagement remaining strong. While acknowledging that the U.S. economic outlook remains mixed, management anticipates that non-performing asset resolution trends will continue.

Velocity is targeting its next long-term loan securitization for September 2025 and expects the securitization market to remain supportive. From an earnings perspective, the company aims to maintain stable net interest margins and achieve strong interest income growth, with a positive production outlook.

The company remains opportunistic regarding product and revenue diversification, which aligns with CEO Chris Ferrar’s previous comments about the company’s growth strategy requiring modest headcount increases and potential office expansions to the Midwest or Texas.

With its strong financial performance, improving credit metrics, and robust liquidity position, Velocity Financial appears well-positioned to continue its growth trajectory and make progress toward its goal of growing its loan portfolio to $10 billion over the next five years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.