Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

Corporacion Inmobiliaria Vesta (MEX:VESTA), a leading Mexican industrial real estate developer, has released its Q2 2025 supplemental information, showcasing continued operational growth despite a challenging market environment. The company, which specializes in manufacturing and logistics facilities, reported solid revenue growth and significant improvements in key operational metrics while continuing its strategic expansion across Mexico’s industrial corridors.

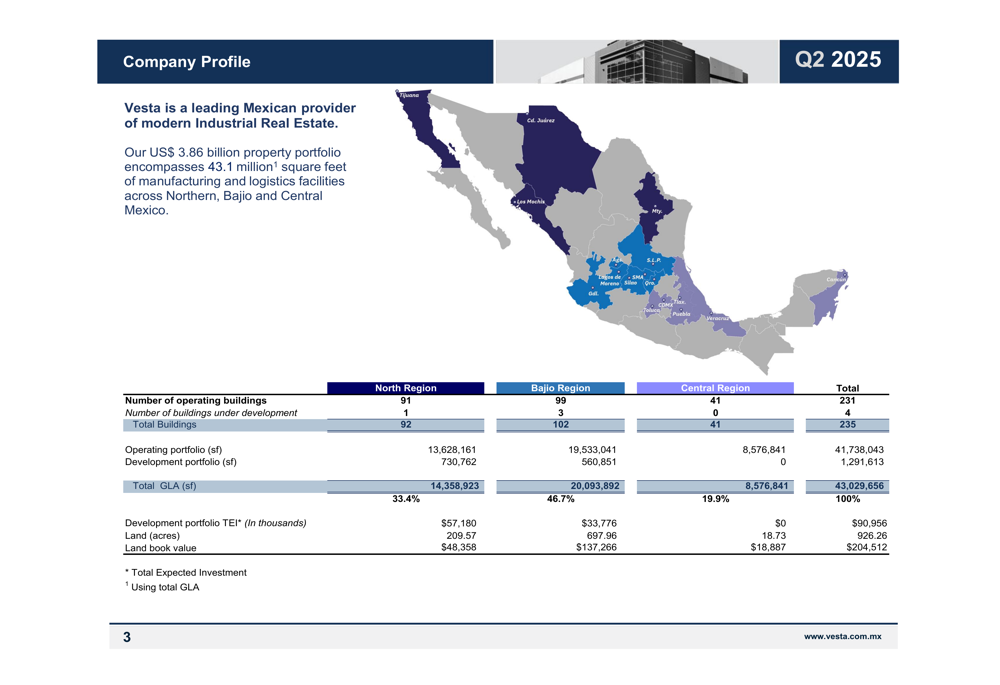

Building on momentum from Q1 2025, when the company reported 10.7% revenue growth, Vesta has maintained its growth trajectory through the second quarter with a focus on high-quality industrial assets in strategic locations. The company’s portfolio now encompasses 43.1 million square feet across 235 properties, positioning it to capitalize on nearshoring trends and e-commerce growth in Mexico.

Quarterly Performance Highlights

Vesta reported total revenues of $67.27 million for Q2 2025, representing a 6.8% increase compared to $63.01 million in Q2 2024. More impressively, the company’s Funds From Operations (FFO) grew by 12.9% year-over-year to $43.12 million, demonstrating strong operational efficiency.

As shown in the following financial summary:

The company maintained robust operational metrics with Adjusted NOI of $61.82 million (up 7.2% year-over-year) and an Adjusted NOI margin of 94.5%. Adjusted EBITDA increased by 9.0% to $55.00 million, with the margin improving to 84.1% from 82.7% in the prior year period.

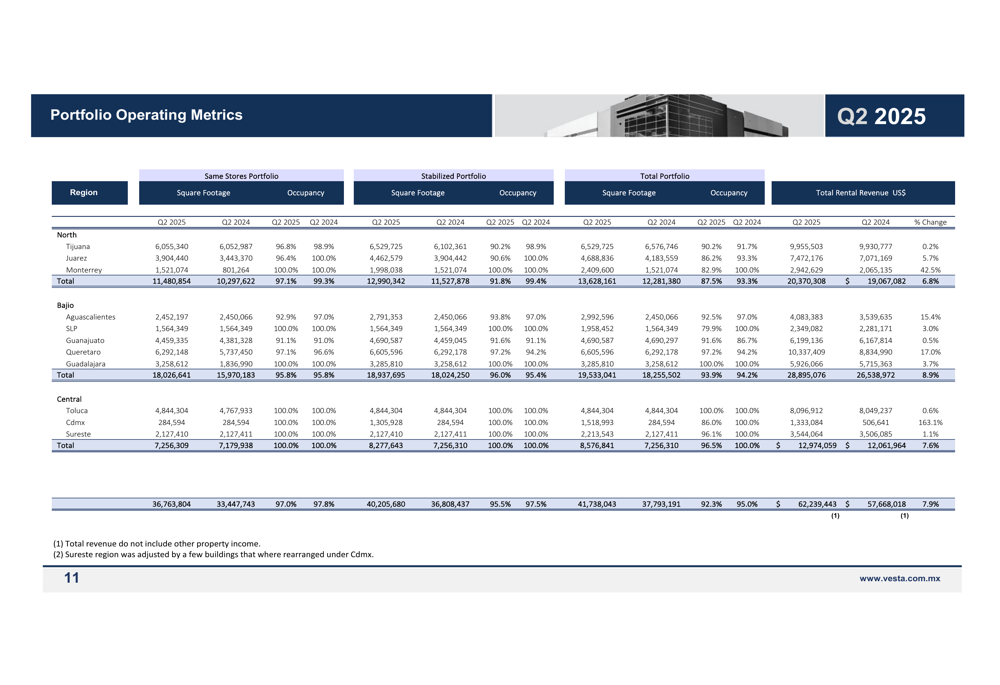

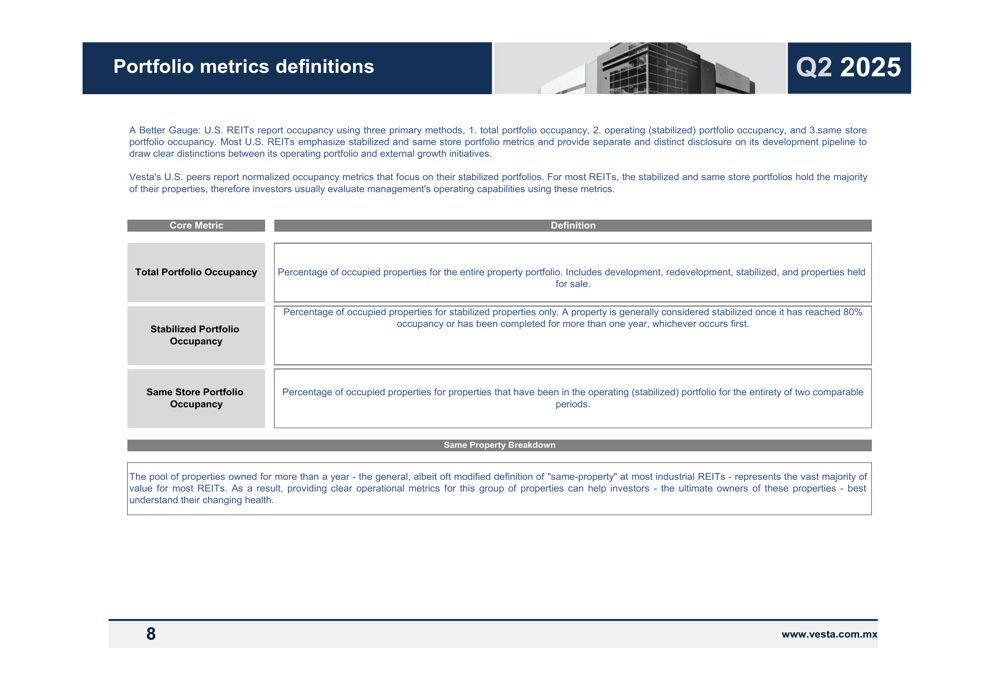

Vesta’s portfolio continues to show strong occupancy rates across all categories:

- Same Store Portfolio: 97.0% occupancy

- Stabilized Portfolio: 95.5% occupancy

- Total (EPA:TTEF) Portfolio: 92.3% occupancy

These high occupancy rates reflect sustained demand for industrial space in Mexico, particularly in key manufacturing and logistics corridors. The company’s geographic distribution across three regions provides diversification while focusing on high-growth areas.

The following image illustrates Vesta’s regional presence and portfolio metrics:

Strategic Initiatives

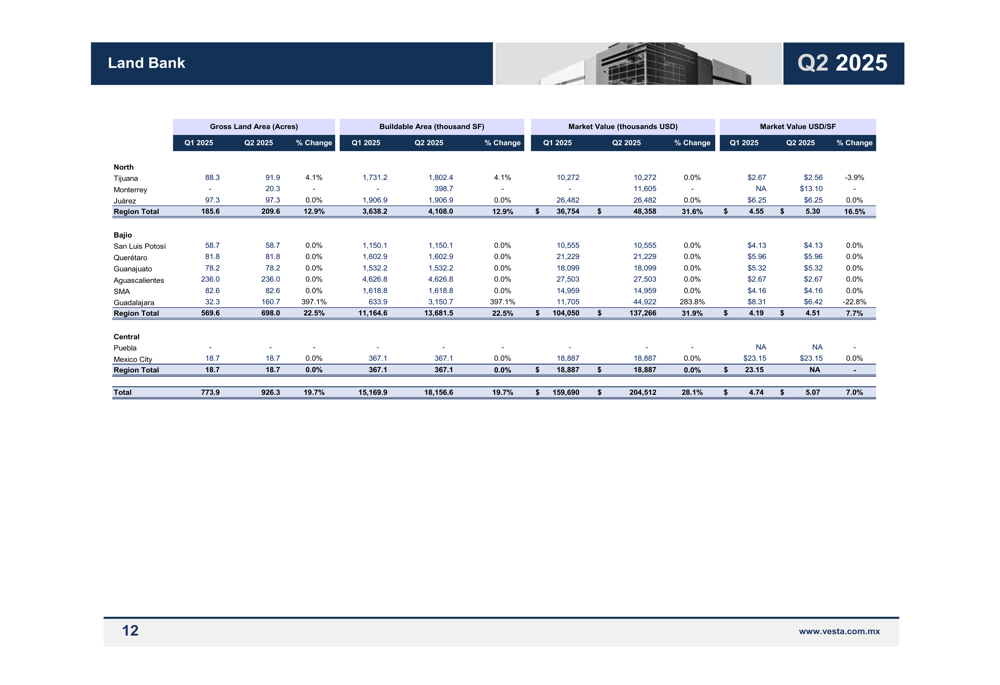

During Q2 2025, Vesta continued its strategic land acquisition program, expanding its land bank by 19.7% compared to Q1 2025. The total land bank now stands at 926.3 acres with a market value of $204.51 million, providing significant runway for future development.

The company’s land bank expansion strategy is illustrated in this breakdown:

Vesta’s development pipeline remains active with 1.29 million square feet under construction and a total expected investment of $90.96 million. These development projects are strategically located across the North and Bajio regions, aligning with nearshoring trends and increasing demand for manufacturing space.

The following development portfolio breakdown shows the company’s ongoing projects:

Detailed Financial Analysis

While Vesta’s operational performance remained strong, the company’s profit for the period decreased significantly to $27.72 million in Q2 2025 from $109.30 million in Q2 2024. This decline was primarily due to lower gains on property revaluation ($7.81 million in Q2 2025 versus $100.08 million in Q2 2024) rather than operational issues.

The company’s balance sheet remains solid with total assets of $4.02 billion and a conservative leverage ratio (debt to total assets) of 22.4%. Total debt outstanding was $900.36 million as of June 30, 2025.

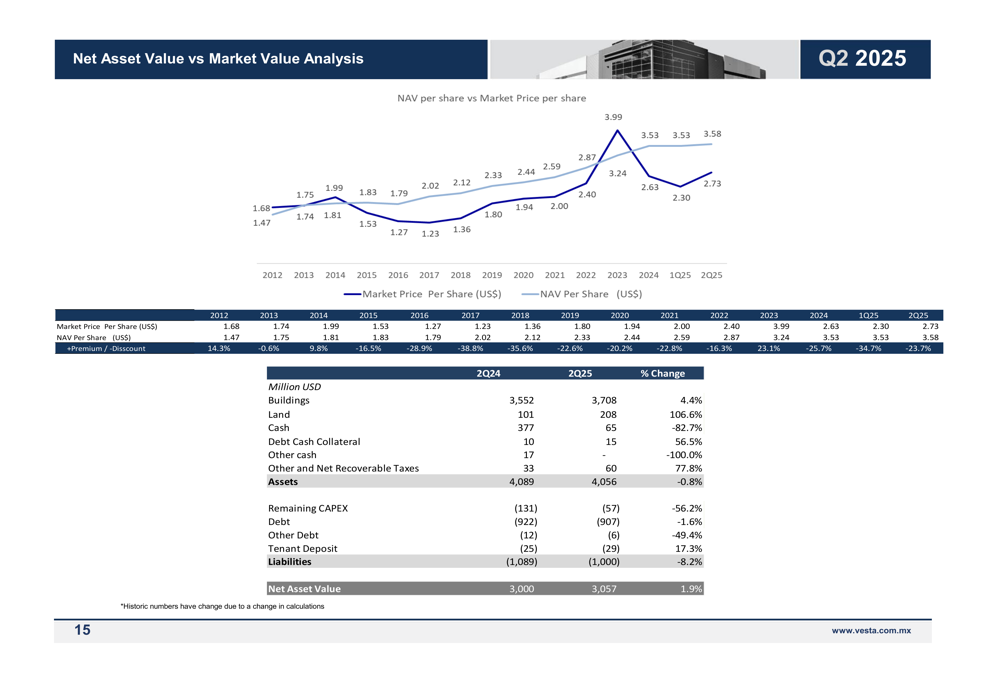

The following Net Asset Value analysis provides insight into Vesta’s valuation metrics:

Leasing activity remained robust with 1.81 million square feet of total leasing activity during Q2 2025, including 344,000 square feet of new leases and 1.4 million square feet of renewals. This strong leasing performance demonstrates continued demand for Vesta’s industrial properties.

The company’s leasing activity is detailed in the following breakdown:

Forward-Looking Statements

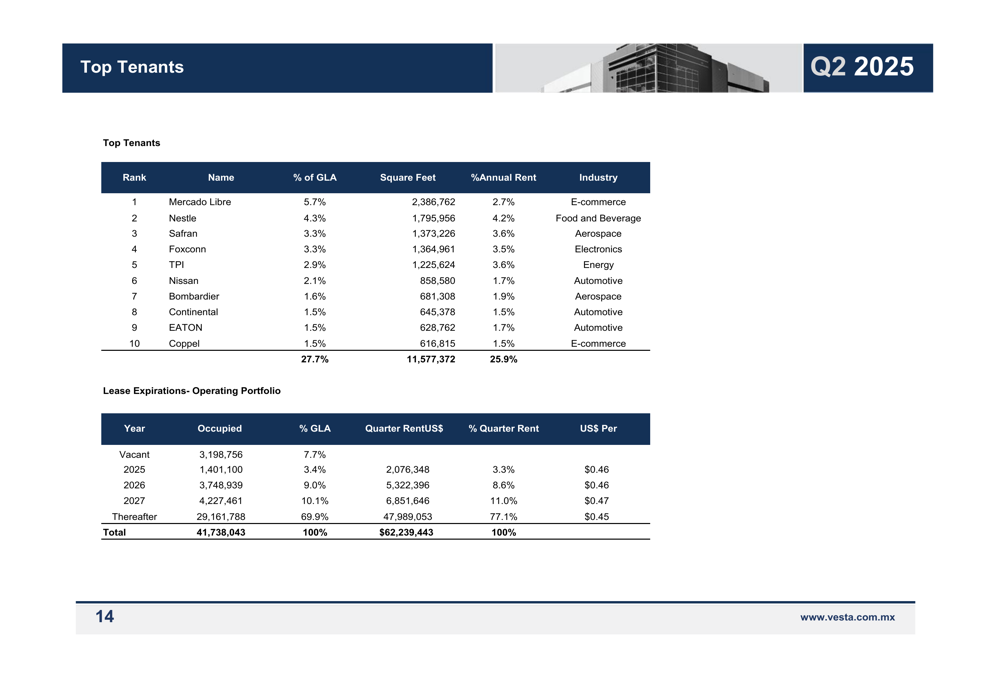

Vesta’s tenant roster remains well-diversified, with e-commerce giant Mercado Libre as its largest tenant representing 5.7% of GLA. This tenant mix provides stability while positioning the company to benefit from continued e-commerce growth in Mexico.

Analyst sentiment remains largely positive, with most analysts maintaining "Buy" ratings and price targets ranging from 43.00 to 72.90. This reflects confidence in Vesta’s growth strategy and market positioning.

Building on comments from the Q1 2025 earnings call, where CEO Lorenzo Dominique Perron expressed optimism about the U.S.-Mexico relationship and highlighted Vesta’s readiness with "high-quality buildings in key corridors," the company appears well-positioned to capitalize on nearshoring trends and increased industrial demand in Mexico.

The historical portfolio metrics demonstrate Vesta’s consistent growth trajectory and ability to maintain high occupancy rates across market cycles:

With its strategic land bank expansion, active development pipeline, and strong operational performance, Vesta continues to execute on its growth strategy while maintaining financial discipline. The significant increase in FFO (12.9% year-over-year) highlights the company’s ability to generate growing cash flows from its expanding portfolio, despite temporary fluctuations in property valuation gains.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.