BofA’s Hartnett says concentrated U.S. stock returns are likely to persist

Introduction & Market Context

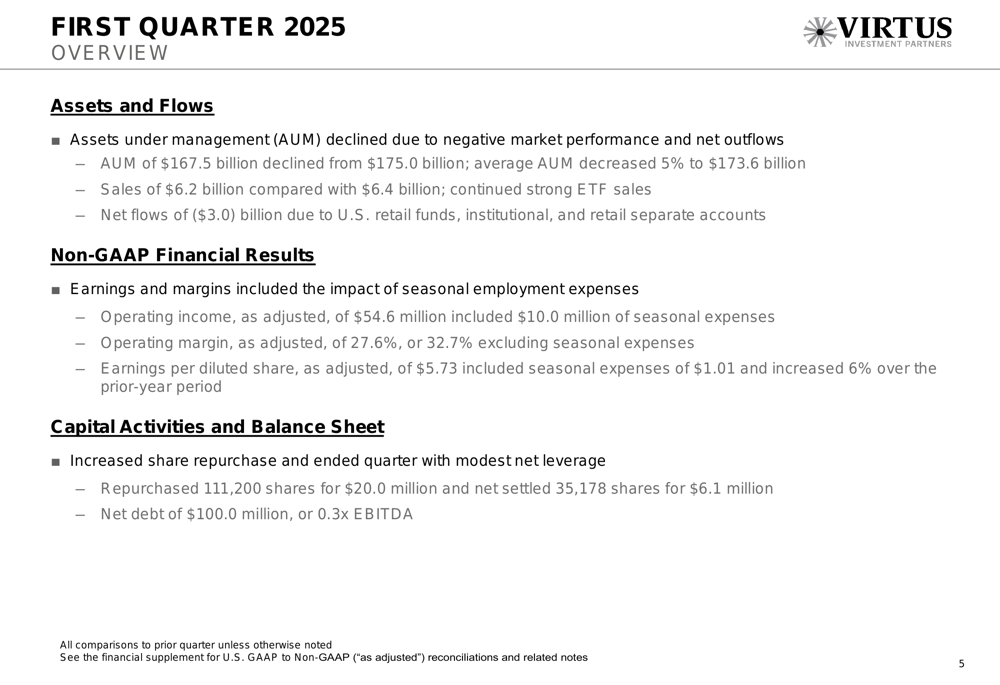

Virtus Investment Partners (NASDAQ:NYSE:VRTS) released its first quarter 2025 earnings presentation on April 25, revealing mixed results as assets under management (AUM) declined while year-over-year earnings showed improvement. The investment manager reported that its AUM fell to $167.5 billion from $175.0 billion in the previous quarter, impacted by both negative market performance and continued net outflows.

The company’s stock closed at $156.84 on April 24, up 1.9% for the day, with a modest decline of 0.31% in premarket trading following the earnings release. Virtus shares have been trading well below their 52-week high of $252.82, reflecting ongoing challenges in the asset management industry.

Quarterly Performance Highlights

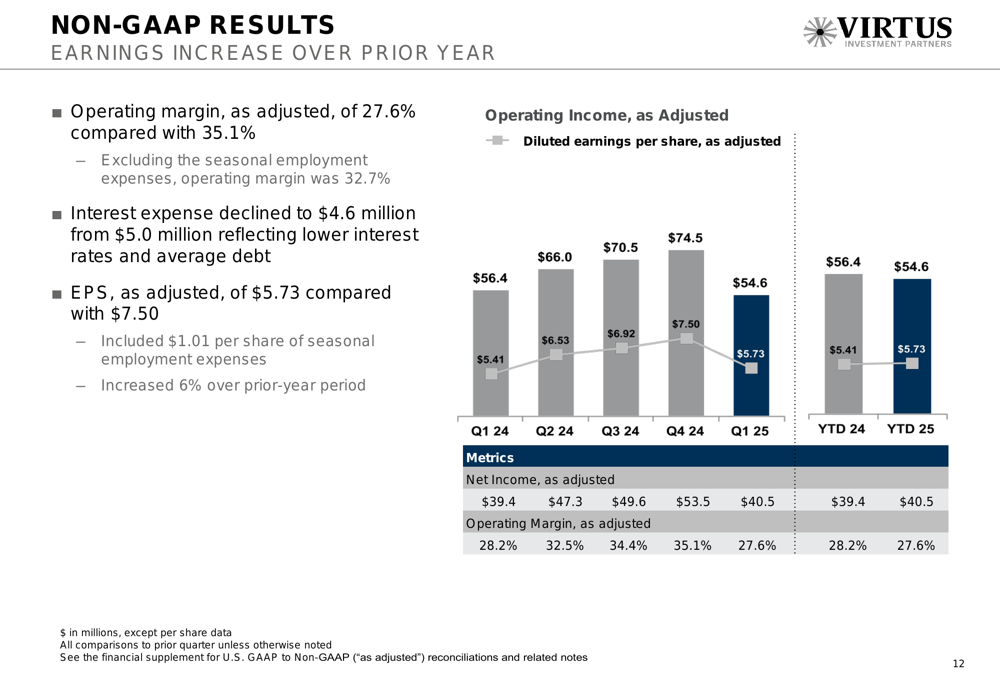

Virtus reported adjusted earnings per share of $5.73 for Q1 2025, which included $1.01 of seasonal expenses. While this represented a 23.6% decrease from Q4 2024’s $7.50, it marked a 6% increase over the prior-year period. The company’s operating income, as adjusted, came in at $54.6 million, including $10.0 million of seasonal expenses.

As shown in the following comprehensive overview of the quarter’s performance:

The operating margin, as adjusted, was 27.6%, or 32.7% excluding seasonal expenses. This represents a significant decrease from the 35.1% reported in Q4 2024, primarily due to the impact of seasonal employment expenses that typically affect first-quarter results.

Asset Management and Flows

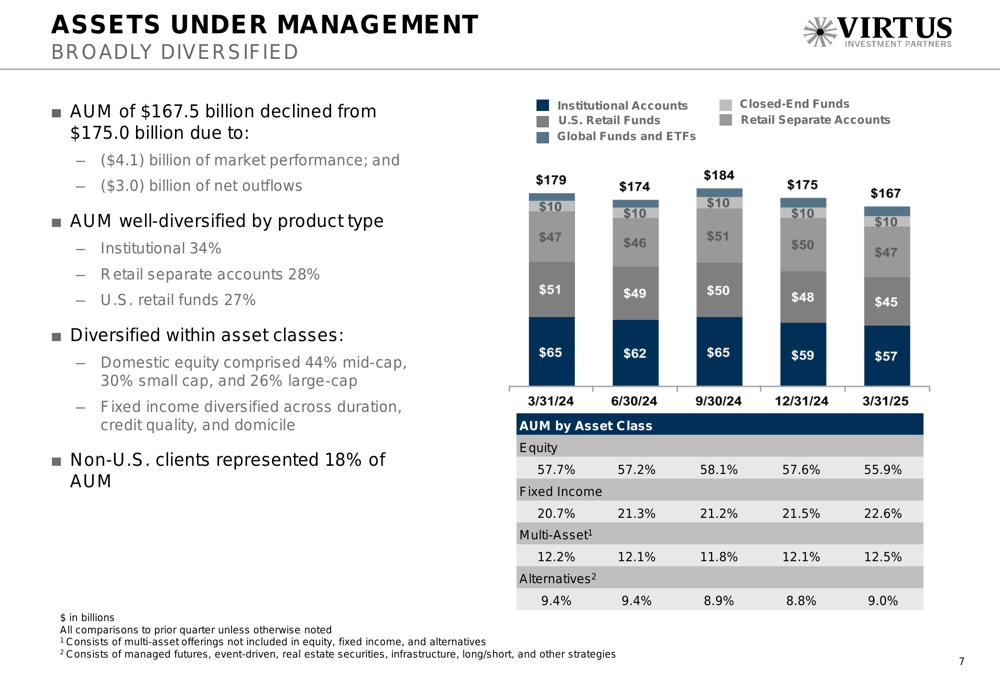

Virtus experienced a $7.5 billion decrease in AUM during the quarter, attributable to $4.1 billion in negative market performance and $3.0 billion in net outflows. The company’s AUM remains well-diversified across product types, with institutional accounts representing 34%, retail separate accounts 28%, and U.S. retail funds 27% of total assets.

The following chart illustrates the company’s diversified asset base across various account types and asset classes:

By asset class, equity investments comprised 55.9% of AUM, followed by fixed income at 22.6%, multi-asset strategies at 12.5%, and alternatives at 9.0%. The company noted that 18% of its AUM came from non-U.S. clients, highlighting its international reach.

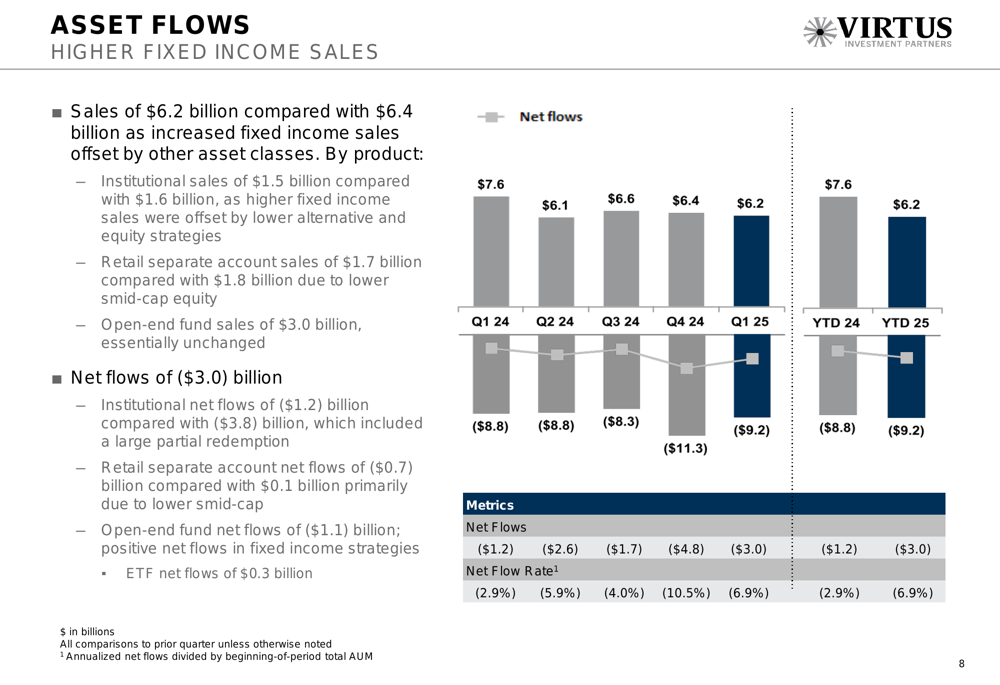

Despite overall net outflows, Virtus reported increased fixed income sales, which partially offset declines in other asset classes. The company’s sales totaled $6.2 billion for the quarter, compared to $6.4 billion in the previous quarter, with continued strength in ETF sales.

The following chart details the company’s asset flows, showing the trend of outflows over recent quarters:

Detailed Financial Analysis

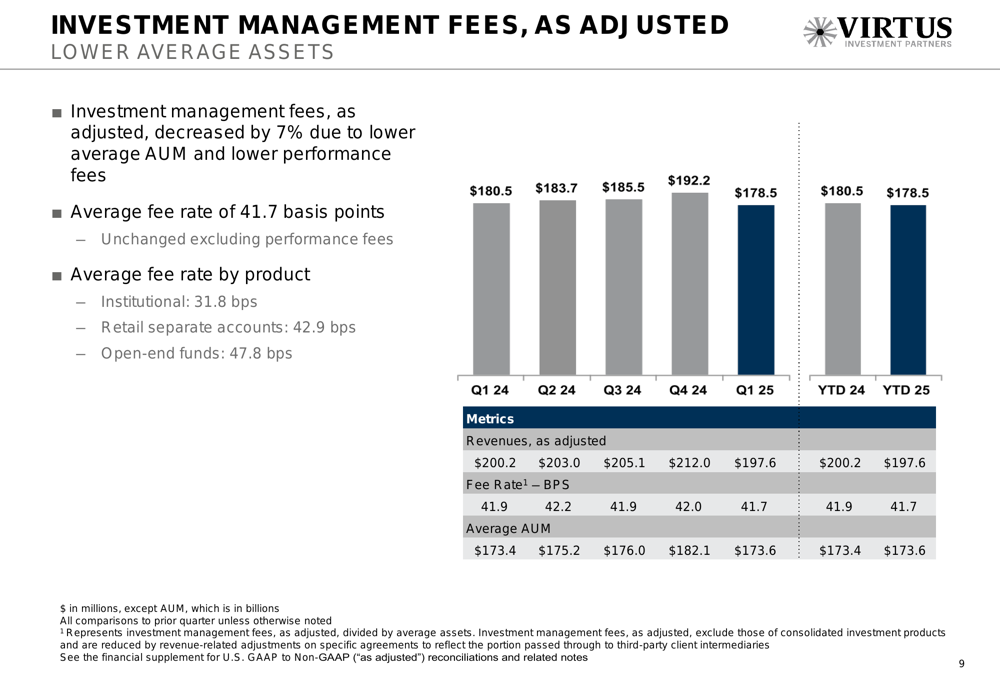

Investment management fees, as adjusted, decreased by 7% to $178.5 million, primarily due to lower average AUM and reduced performance fees. The company maintained its average fee rate at 41.7 basis points, unchanged when excluding performance fees.

This chart shows the trend in investment management fees over recent quarters:

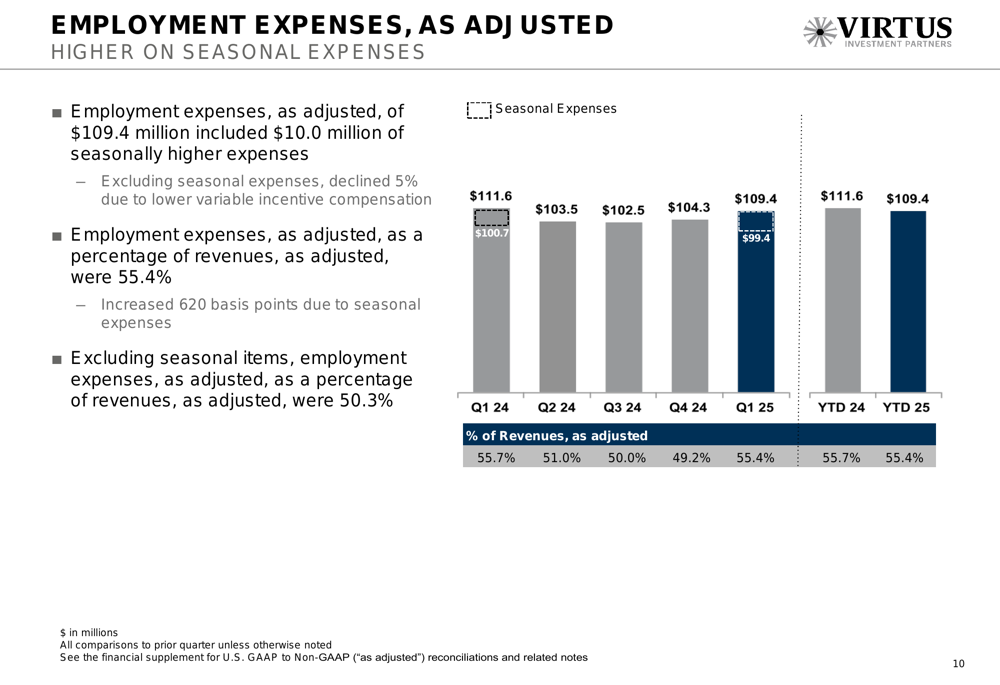

Employment expenses, as adjusted, totaled $109.4 million, including $10.0 million of seasonally higher expenses. As a percentage of adjusted revenues, employment expenses were 55.4%, higher than the 49-51% range the company had previously indicated as its target. The following chart illustrates the impact of seasonal expenses:

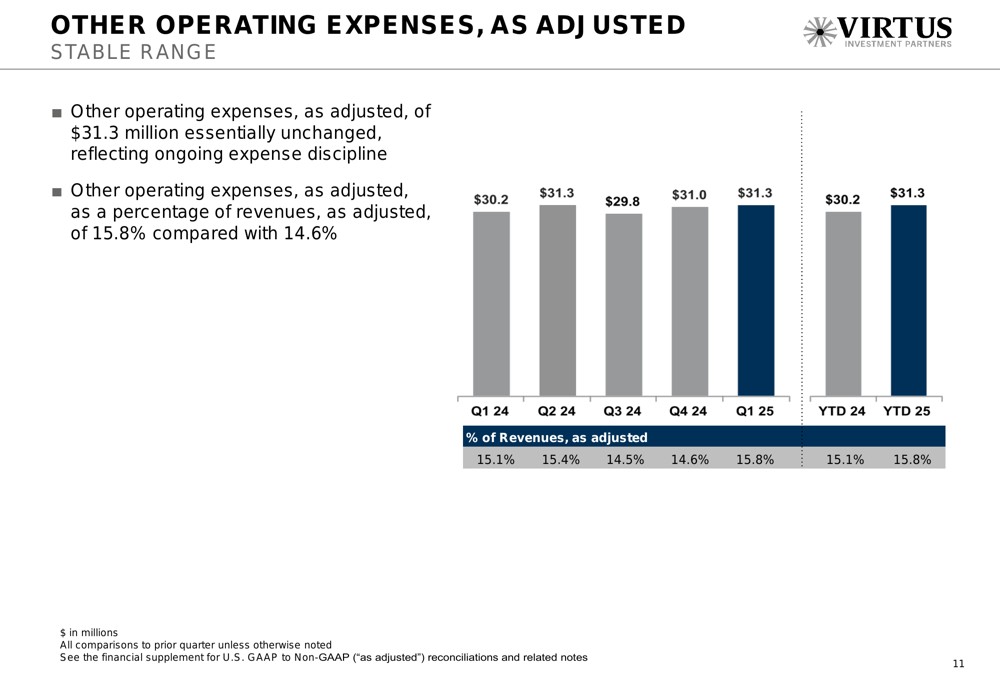

Other operating expenses remained well-controlled at $31.3 million, essentially unchanged from previous quarters, reflecting the company’s ongoing expense discipline:

The company’s non-GAAP results show the earnings trajectory over recent quarters, with Q1 2025 showing improvement over the same period last year despite the sequential decline from Q4 2024:

Capital Management & Balance Sheet

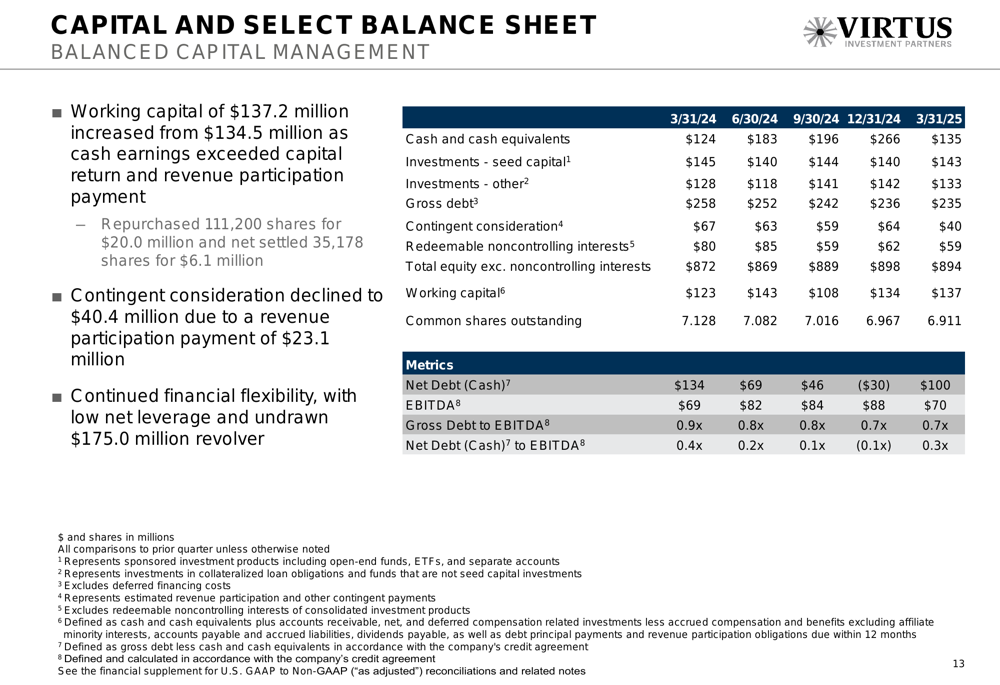

Virtus continued its share repurchase program, buying back 111,200 shares for $20.0 million and net settling 35,178 shares for $6.1 million during the quarter. The company ended the period with net debt of $100.0 million, representing a modest leverage ratio of 0.3x EBITDA.

Working capital increased to $137.2 million from $134.5 million, as cash earnings exceeded capital returned to shareholders and revenue participation payments. The company’s contingent consideration declined to $40.4 million due to a revenue participation payment of $23.1 million.

The following slide details the company’s capital position and balance sheet strength:

Forward-Looking Statements

While the presentation did not include explicit forward guidance, Virtus emphasized its continued financial flexibility with low net leverage and an undrawn $175.0 million revolving credit facility. This positions the company to pursue strategic opportunities while navigating market challenges.

Based on the previous quarter’s earnings call, Virtus had anticipated an average fee rate of 41-42 basis points, which aligns with the 41.7 basis points reported for Q1 2025. However, employment expenses as a percentage of revenues came in higher than the previously indicated 49-51% range, likely due to the seasonal impact in the first quarter.

The company’s focus on product diversification, particularly in ETFs and fixed income offerings, appears to be continuing, as evidenced by the increased fixed income sales despite overall outflows. Virtus had previously expressed interest in potential mergers and acquisitions, particularly in private market capabilities, though no specific transactions were mentioned in this quarter’s presentation.

Virtus faces ongoing challenges from market volatility and competitive pressures in the asset management industry, as reflected in the continued net outflows. However, its diversified product mix and international client base provide some resilience against these headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.