CVS Group shares surge over 10% after FY25 EBITDA beats estimates

Vishay Intertechnology Inc (NYSE:VSH) reported flat quarter-over-quarter revenue and compressed margins in its Q1 2025 earnings presentation on May 7, while maintaining an optimistic long-term outlook despite ongoing challenges from tariffs and acquisition integration costs.

Quarterly Performance Highlights

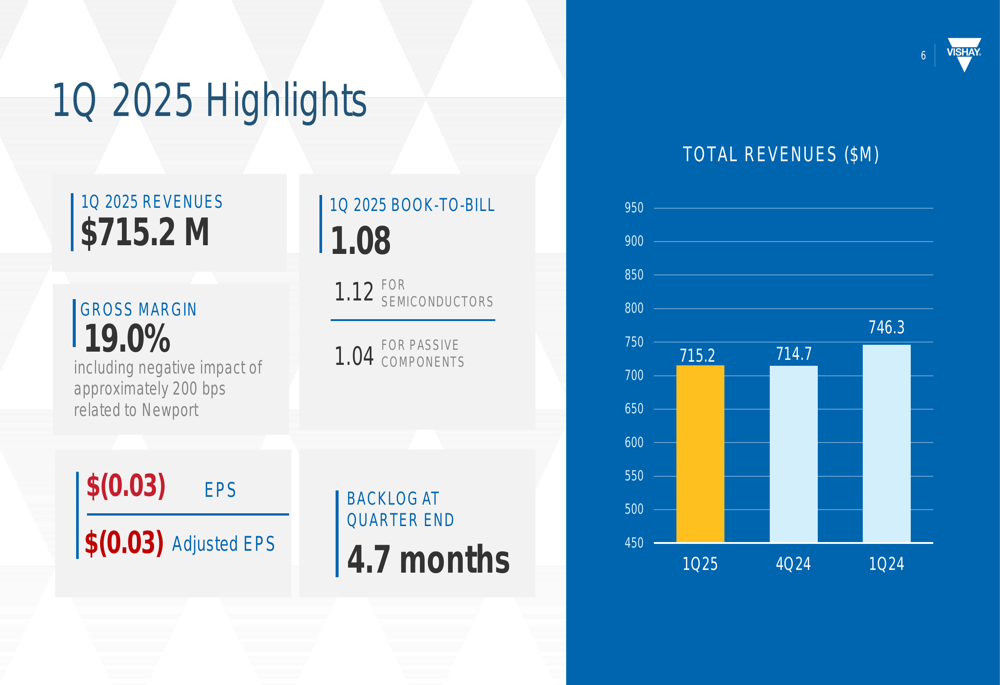

Vishay reported Q1 2025 revenue of $715.2 million, essentially unchanged from $714.7 million in Q4 2024 but down from $746.3 million in the same quarter last year. The company posted a loss per share of $0.03, improving from a loss of $0.49 in the previous quarter but down from earnings of $0.22 per share in Q1 2024.

As shown in the following quarterly highlights, Vishay’s book-to-bill ratio of 1.08 suggests potential future growth, with semiconductors showing stronger demand at 1.12 compared to passive components at 1.04:

Gross margin fell to 19.0% in Q1 2025, down from 19.9% in Q4 2024 and 22.8% in Q1 2024. The company noted that the Newport acquisition negatively impacted gross margin by approximately 200 basis points.

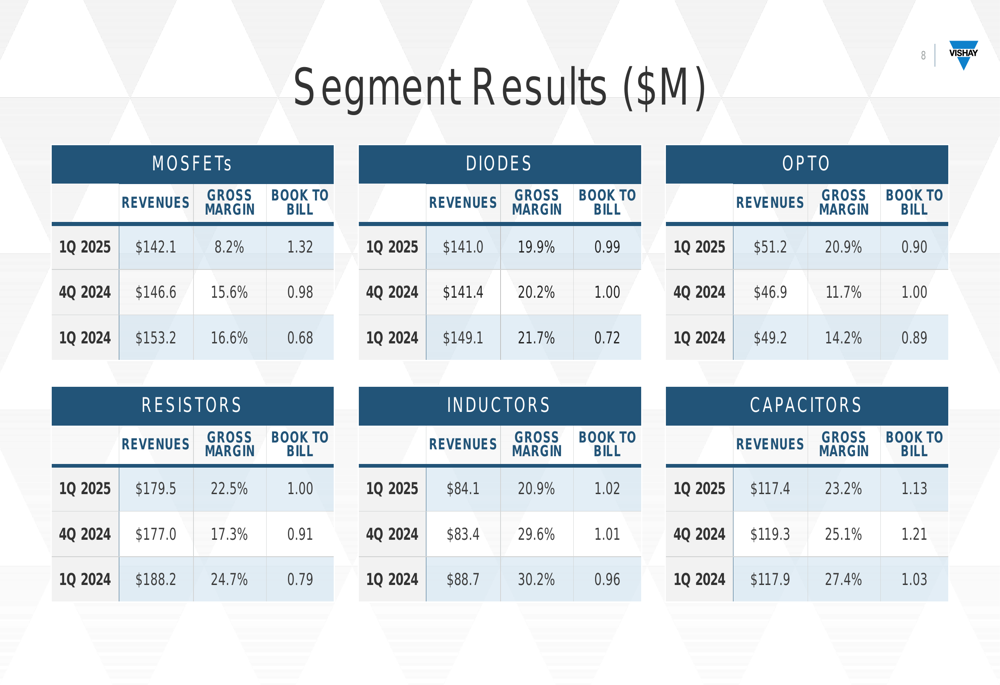

The segment results reveal significant challenges in the MOSFETs business, where gross margin collapsed to 8.2% from 16.6% a year earlier, despite a relatively modest revenue decline. Other segments showed mixed performance, with Opto products showing margin improvement while Inductors experienced a significant margin decline:

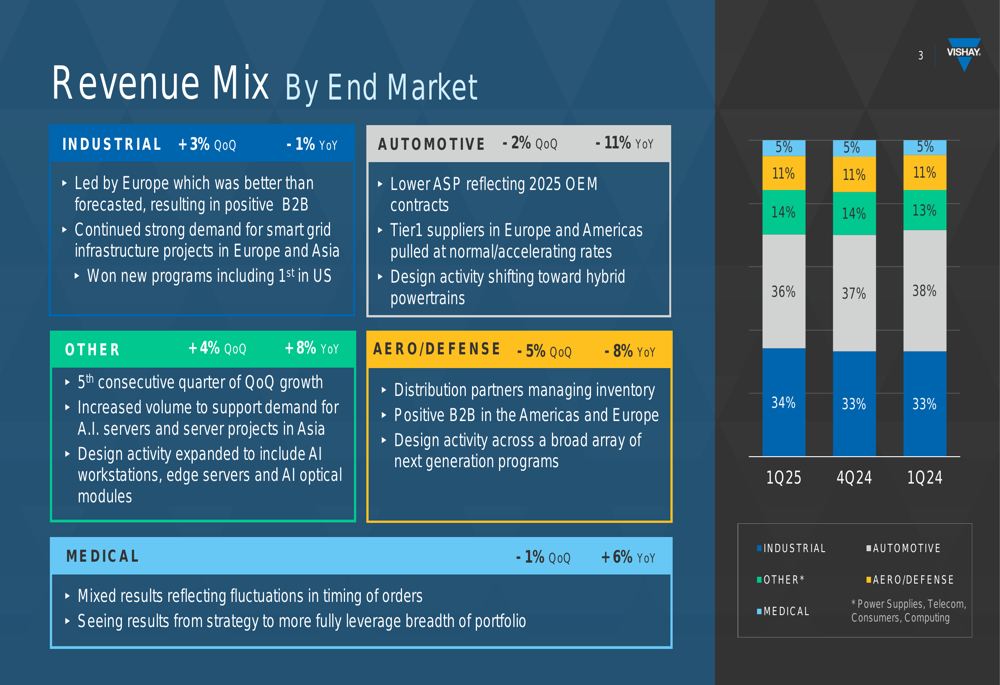

Vishay’s revenue mix by end market shows relatively stable distribution, with slight shifts quarter-over-quarter. The company highlighted strength in industrial markets led by Europe, particularly in smart grid projects, while noting that automotive revenue declined due to lower average selling prices:

Cash Flow and Capital Allocation

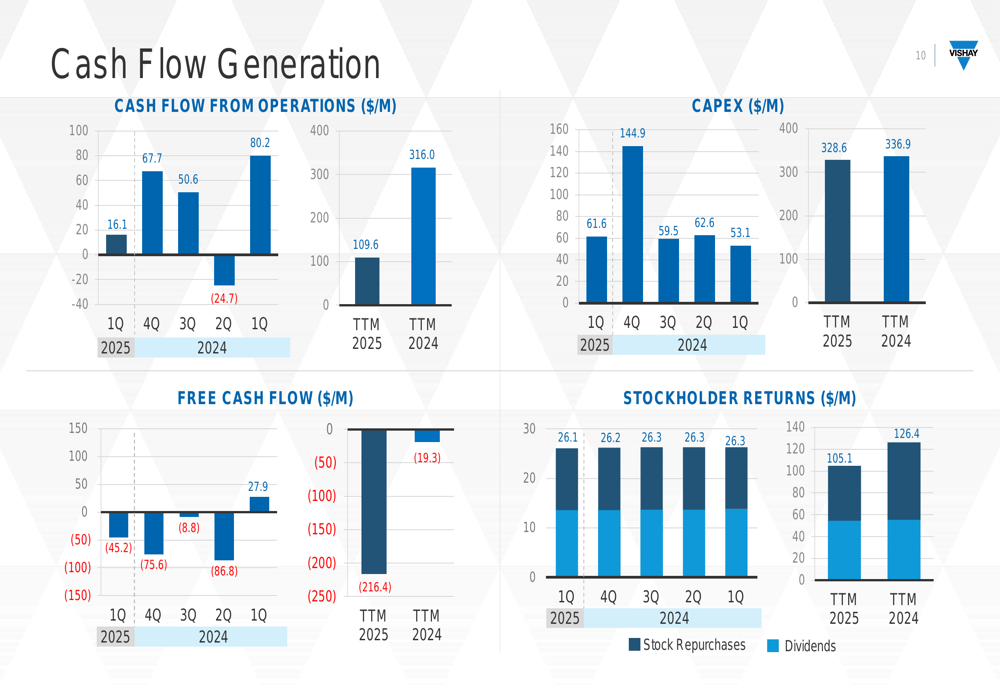

Vishay’s cash flow from operations declined significantly to $16.1 million in Q1 2025 from $67.7 million in Q4 2024. Free cash flow remained negative at -$45.2 million, though this represented an improvement from -$75.6 million in the previous quarter. The negative free cash flow reflects substantial capital expenditures of $61.6 million during the quarter.

The following chart illustrates Vishay’s cash flow generation and capital allocation priorities:

The company’s cash conversion cycle extended slightly to 129 days in Q1 2025 from 128 days in Q4 2024 and 124 days in Q1 2024, primarily due to increased inventory days.

Tariff Impact and Guidance

A significant focus of the presentation was the impact of new U.S. tariffs on Chinese-manufactured products. Vishay disclosed that products manufactured in China and sold in the U.S. now face tariffs of 70% for semiconductors and 170% for passive components. However, the company noted that Chinese-origin products sold to U.S. customers represent less than 4% of consolidated sales.

For Q2 2025, Vishay expects these tariffs to increase revenue by approximately 1-2% compared to Q1, with a neutral impact on gross profit but a negative impact of about 30 basis points on gross margin percentage.

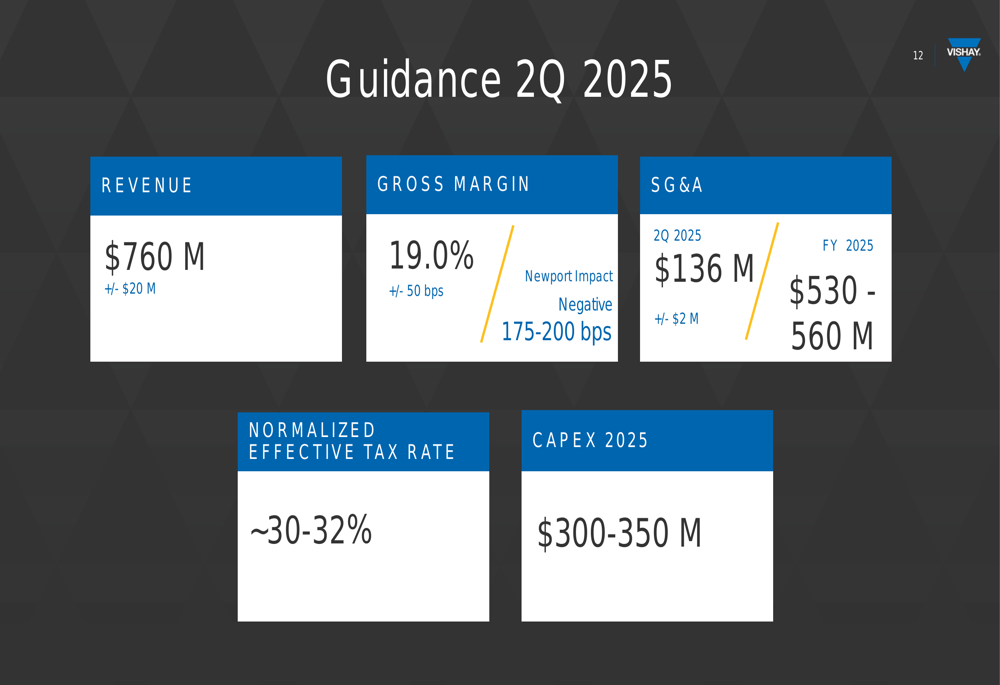

The company provided the following guidance for Q2 2025:

Vishay expects Q2 2025 revenue of $760 million (±$20 million), representing a sequential increase of approximately 6.3% at the midpoint. Gross margin is projected to remain at 19.0% (±50 basis points), with the Newport acquisition continuing to have a negative impact of 175-200 basis points.

Strategic Initiatives and Long-Term Outlook

Despite near-term challenges, Vishay maintains an optimistic long-term outlook. The company presented its strategic growth levers, focusing on both served markets (through capacity expansion and manufacturing footprint optimization) and portfolio broadening (through innovation, channel management, and M&A).

Vishay also highlighted its broad customer base across multiple industries, showcasing logos of major OEMs, EMS providers, and distributors that rely on its components:

The company emphasized its product breadth, noting that in power applications, it can populate approximately 80% of customers’ bill of materials:

Looking further ahead, Vishay outlined ambitious financial goals for 2028, including:

- Revenue growth at a 9-11% CAGR from 2023’s $3.4 billion

- Gross margin improvement to 31-33% from 28.6% in 2023

- Operating margin expansion to 19-21% from 14.3% in 2023

- Adjusted EBITDA margin of 25-27% compared to 19.5% in 2023

These targets represent a significant improvement from current performance levels and will require successful execution of the company’s strategic initiatives.

Market Reaction and Outlook

Vishay’s stock showed positive movement in premarket trading, up 4.17% to $14.00 after closing at $13.44 on May 6, 2025. This suggests investors may be focusing on the improved book-to-bill ratio and sequential guidance rather than the current margin challenges.

The company’s Q1 results continue a challenging period that was evident in previous quarters. In its Q3 2024 earnings, Vishay had reported a GAAP loss per share of $0.14 amid inventory destocking and sluggish demand, particularly in Europe.

While Vishay faces significant near-term headwinds from margin pressure, tariff impacts, and integration costs, the company’s long-term strategic focus on growth markets like AI, smart grid infrastructure, and automotive, combined with its broad product portfolio and customer base, provides potential pathways for recovery as market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.