Bitcoin price today: steady near $92k after sharp losses; Fed caution weighs

Introduction & Market Context

Vishay Intertechnology Inc (NYSE:VSH) presented its third quarter 2025 results on November 5, 2025, reporting stronger-than-expected earnings despite ongoing challenges. The electronic components manufacturer posted an adjusted earnings per share of $0.04, exceeding analyst expectations of $0.03, while revenue reached $790.6 million, surpassing the forecasted $778.2 million.

Despite these positive results, Vishay's stock fell 7.14% during the trading session, closing at $16.10, before recovering 3.73% to $16.70 in premarket trading the following day. This market reaction suggests investors may be concerned about ongoing margin pressures and the company's ability to sustain growth momentum.

Quarterly Performance Highlights

Vishay reported revenue of $790.6 million for Q3 2025, representing a 4% increase quarter-over-quarter and a 7.5% rise year-over-year. The company achieved an adjusted earnings per share of $0.04, though GAAP earnings showed a loss of $(0.06) per share.

As shown in the following quarterly highlights chart:

Gross margin stood at 19.5%, which included a negative impact of approximately 150 basis points related to the company's Newport facility. The book-to-bill ratio was 0.97 (0.96 for semiconductors and 0.98 for passive components), indicating relatively balanced demand and supply.

Segment Analysis

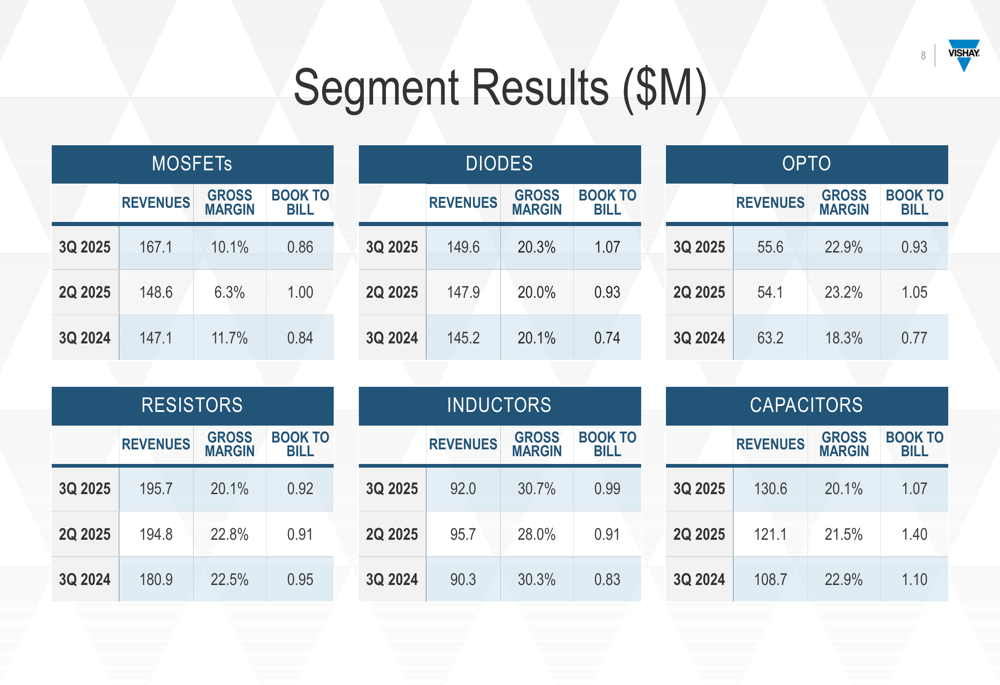

Vishay's performance varied across its product segments, with MOSFETs and capacitors showing the strongest sequential growth at 12.4% and 7.8% respectively. The company's segment breakdown reveals both strengths and challenges across its portfolio:

MOSFETs revenue increased to $167.1 million but faced margin pressure with gross margin at 10.1%, down from 11.7% in the prior year. Meanwhile, the capacitors segment showed robust growth to $130.6 million with a 20.1% gross margin, driven by demand for smart grid infrastructure projects in Europe and China.

Inductors continued to be the highest-margin segment at 30.7%, while the diodes segment maintained stable performance with a 20.3% gross margin.

End Market and Regional Performance

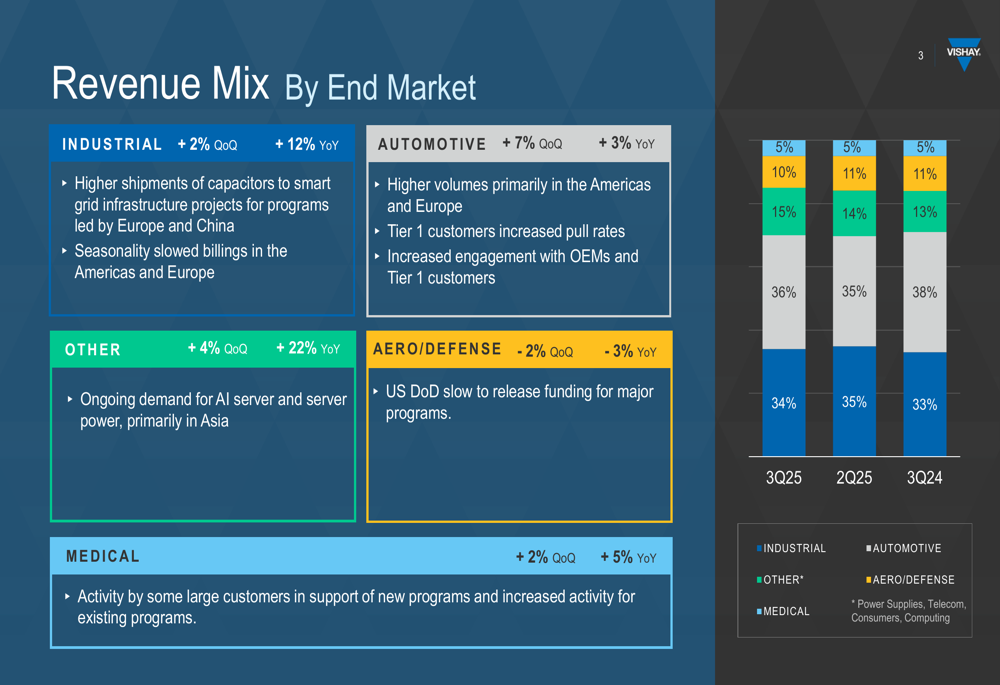

Vishay's revenue mix by end market shows strength in automotive and industrial sectors, with notable growth in AI-related applications:

The automotive segment grew 7% quarter-over-quarter and 3% year-over-year, driven by higher volumes in the Americas and Europe. The industrial segment increased 2% sequentially and 12% year-over-year, benefiting from higher shipments of capacitors to smart grid infrastructure projects.

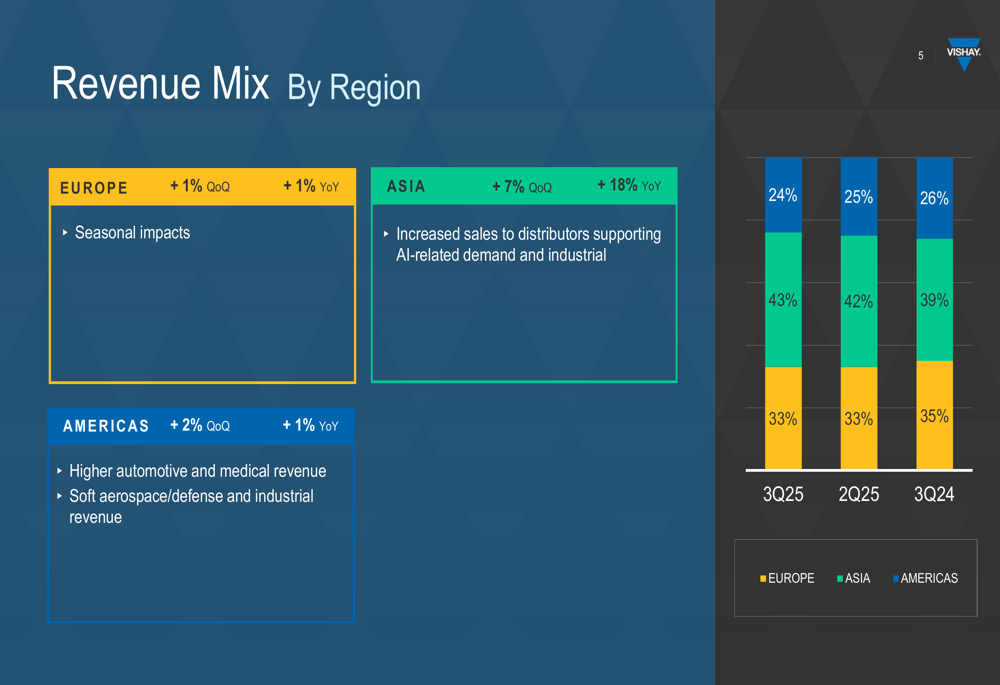

Regionally, Asia led growth with a 7% quarterly increase and an impressive 18% year-over-year gain, primarily due to AI-related demand:

The company's distribution channel, which represents 57% of total revenue, grew 4% quarter-over-quarter and 10% year-over-year, with most of that growth coming from Asia due to AI servers, industrial, and smart grid infrastructure projects.

Cash Flow and Financial Position

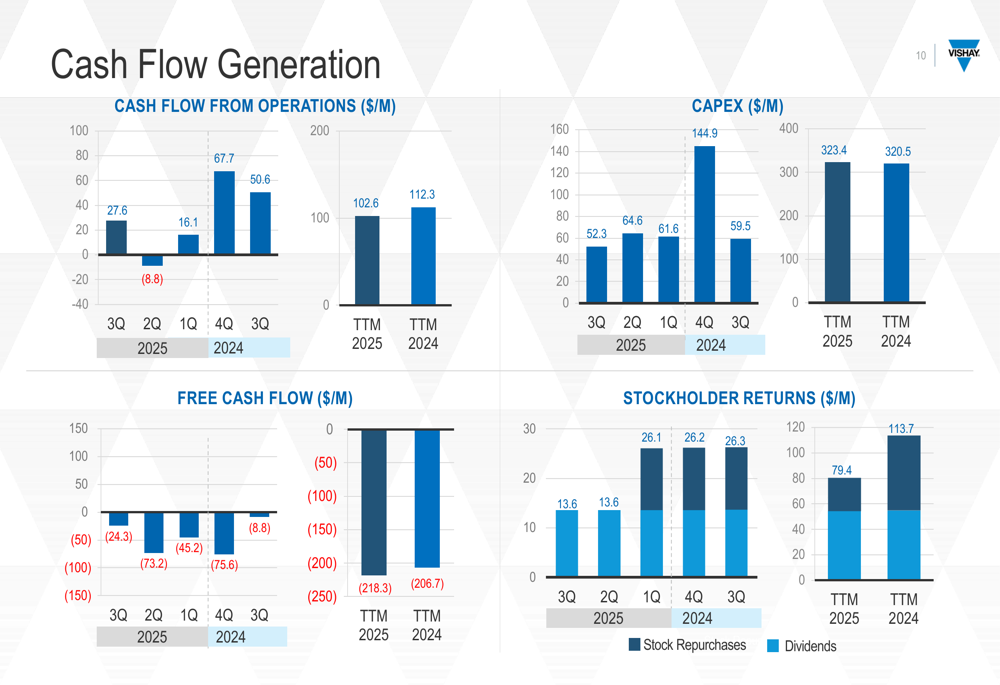

Vishay's cash flow metrics reveal ongoing investment in capacity expansion, resulting in negative free cash flow:

The company generated $27.6 million in cash from operations during Q3 2025 but reported negative free cash flow of $(24.3) million due to capital expenditures of $52.3 million. On a trailing twelve-month basis, free cash flow was $(218.3) million, reflecting Vishay's significant investments in growth initiatives.

The cash conversion cycle remained stable at 130 days, unchanged from the previous quarter but slightly higher than the 127 days reported in Q3 2024.

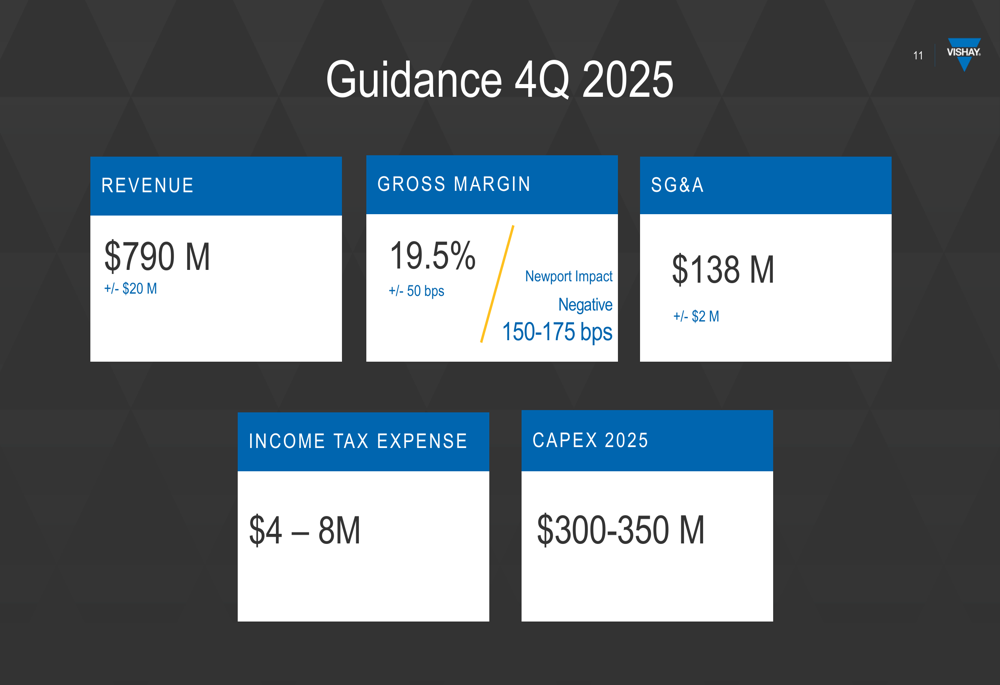

Guidance and Future Outlook

For the fourth quarter of 2025, Vishay provided the following guidance:

The company expects Q4 2025 revenue to remain relatively flat at $790 million (±$20 million) with gross margin holding steady at 19.5% (±50 basis points), still including a negative Newport impact of 150-175 basis points.

Looking further ahead, Vishay has established ambitious financial goals for 2028:

The company is targeting a revenue CAGR of 9-11% from 2023 to 2028, with significant margin improvements. Vishay aims to increase gross margin from 28.6% in 2023 to 31-33% by 2028, and operating margin from 14.3% to 19-21%.

Strategic Initiatives

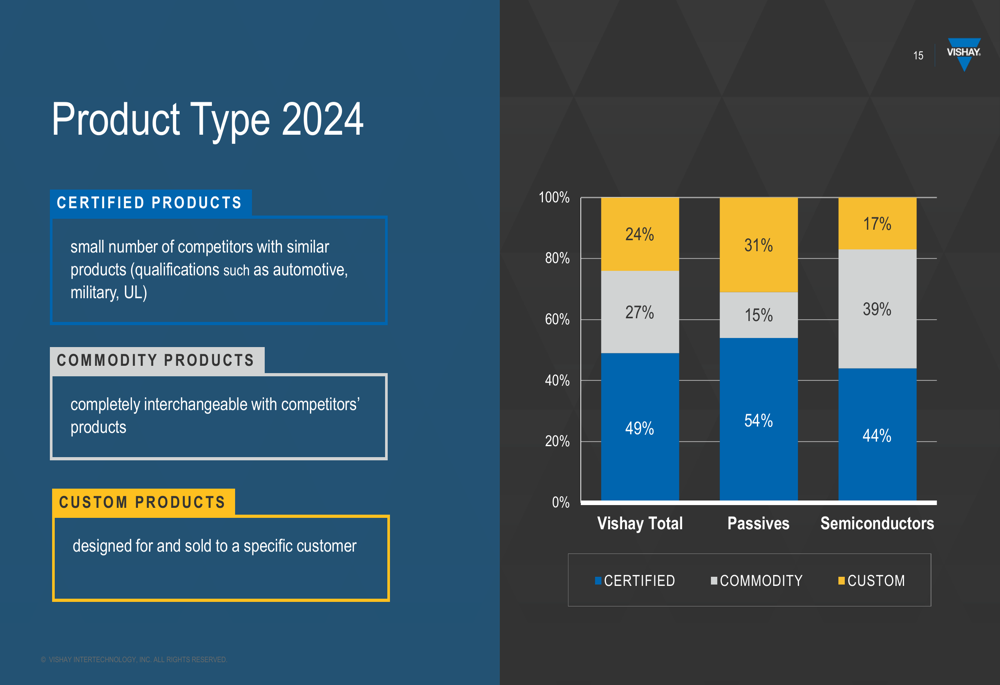

Vishay's product portfolio strategy focuses on a balanced mix of certified, commodity, and custom products:

Nearly half (49%) of Vishay's total revenue comes from custom products designed for specific customers, with certified products accounting for 24% and commodity products making up 27%. This strategy helps the company maintain differentiation and potentially higher margins in competitive markets.

According to CEO Joel Smejkal during the earnings call, the company is focusing on optimizing its Newport facility, aiming to make it margin neutral by the end of Q1 2026. This improvement would address a significant drag on current profitability.

While Vishay faces near-term challenges with margins and free cash flow, its strategic investments and focus on high-growth segments like automotive and AI position the company for potential long-term growth. However, investors appear cautious about the timeline and execution of these initiatives, as reflected in the stock's recent performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.