Oil prices hold sharp losses with focus on secondary India tariffs

Introduction & Market Context

Vontier Corporation (NYSE:VNT) released its second quarter 2025 earnings presentation on July 31, showcasing strong financial performance that exceeded market expectations. The mobility and transportation technology company reported double-digit core sales growth and significant margin expansion, building on the momentum seen in Q1 2025.

Following the earnings release, Vontier’s stock was trading near $39.74, close to its 52-week high of $40.99, reflecting investor confidence in the company’s execution and growth strategy.

Quarterly Performance Highlights

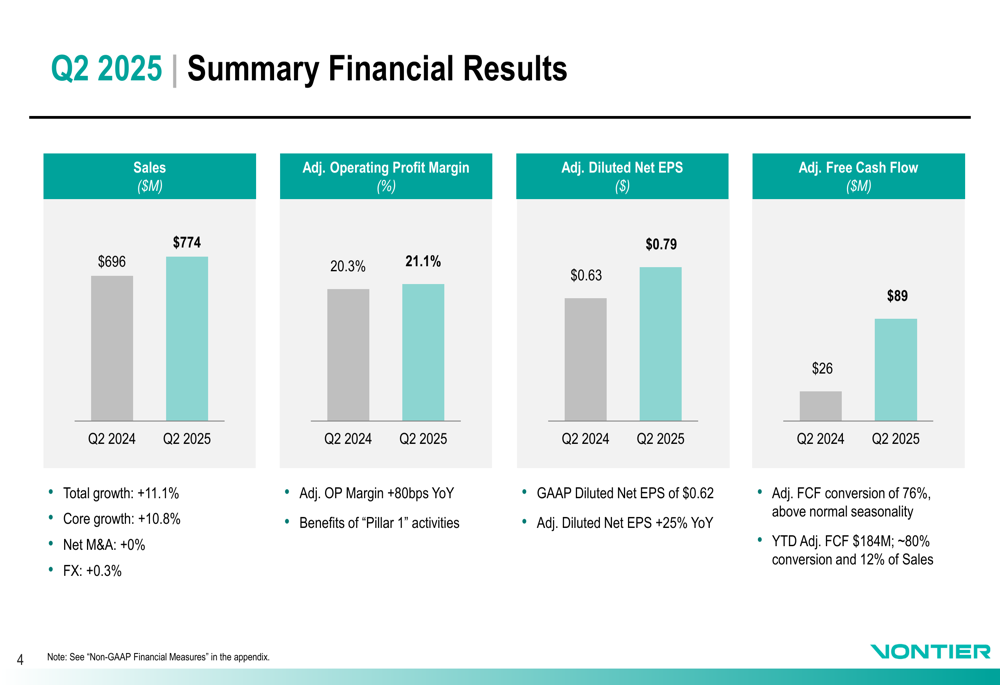

Vontier delivered impressive results in Q2 2025, with core sales growth of 11% and adjusted operating profit margin expanding 80 basis points to 21.1%. The company’s adjusted diluted earnings per share reached $0.79, representing a 25% increase compared to $0.63 in the same period last year.

As shown in the following summary of financial results:

Total (EPA:TTEF) sales grew to $774 million, up 11.1% compared to $696 million in Q2 2024. This growth was primarily driven by strong performance in the Environmental & Fueling Solutions (EFS) and Mobility Technologies (MT) segments, which grew 16.2% and 17.9% respectively.

The company’s adjusted free cash flow saw a dramatic improvement, reaching $89 million compared to $26 million in Q2 2024, with adjusted free cash flow conversion of 76%, which the company noted was above normal seasonality.

Detailed Financial Analysis

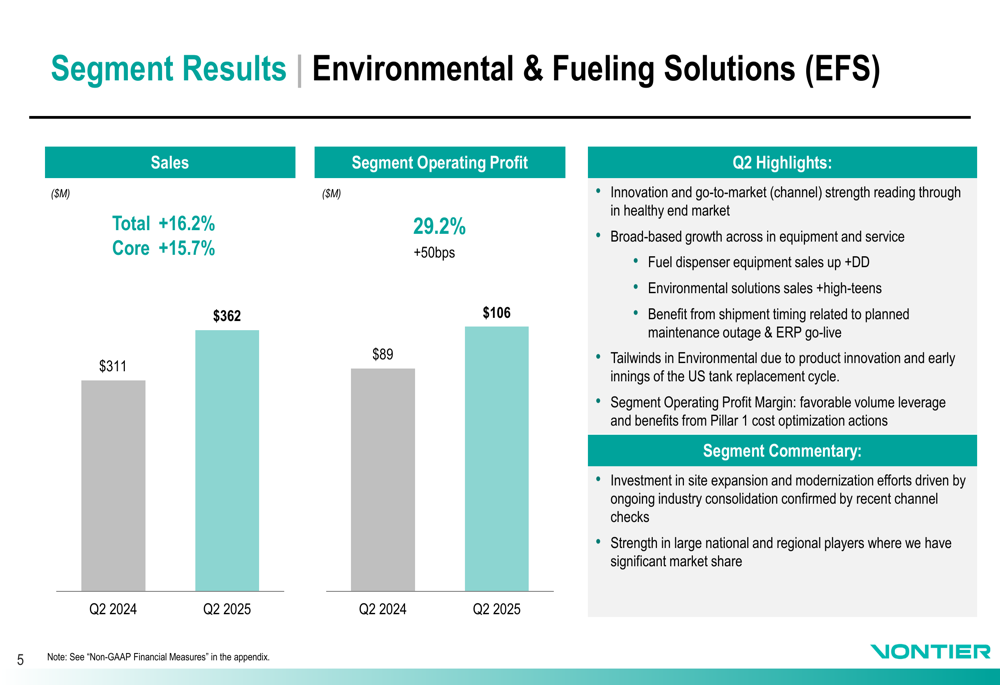

Vontier’s segment performance revealed varying dynamics across its business units. The Environmental & Fueling Solutions segment delivered exceptional results with sales increasing to $362 million and operating profit margin expanding by 50 basis points to 29.2%.

As illustrated in the EFS segment results:

The strong performance in EFS was attributed to innovation and channel strength in healthy end markets, with fuel dispenser equipment sales up by double digits and environmental solutions sales increasing by high teens. The company also noted tailwinds in environmental solutions due to product innovation and the early stages of the US tank replacement cycle.

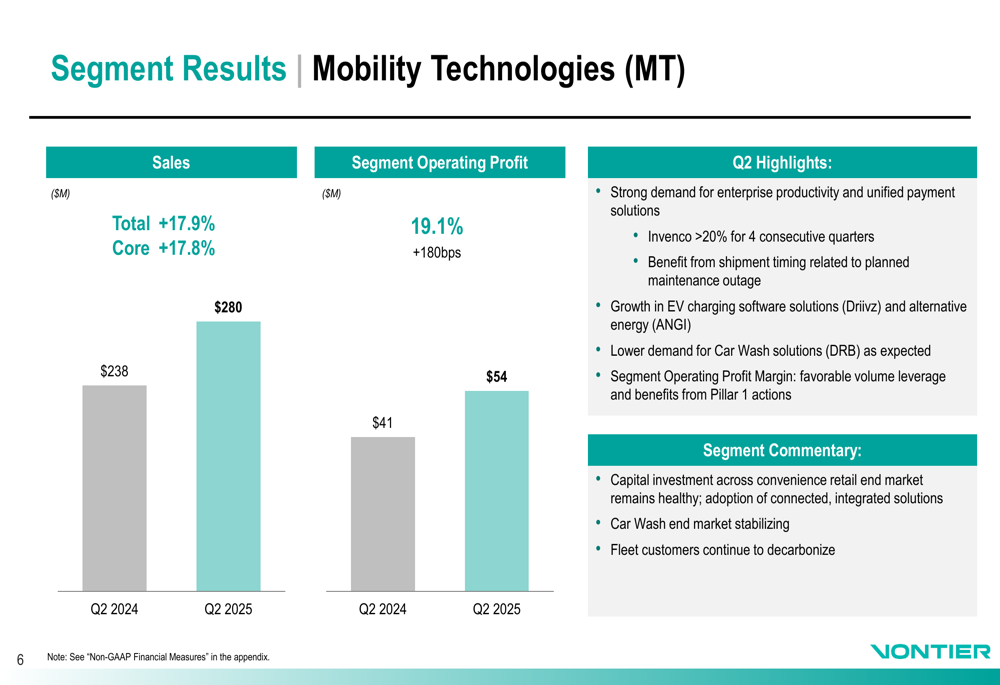

Similarly, the Mobility Technologies segment showed robust growth:

MT segment sales increased to $280 million, with operating profit margin expanding significantly by 180 basis points to 19.1%. The company highlighted strong demand for enterprise productivity and unified payment solutions, with Invenco growing over 20% for four consecutive quarters. Growth in EV charging software solutions (Driivz) and alternative energy (ANGI) also contributed positively, though this was partially offset by lower demand for Car Wash solutions.

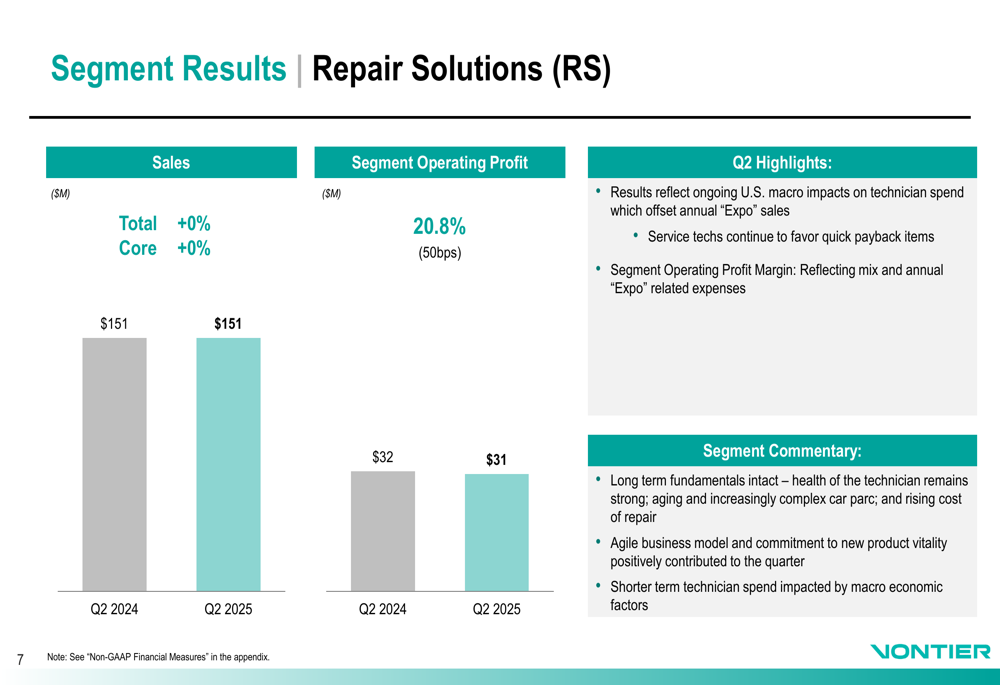

In contrast, the Repair Solutions segment faced challenges:

Repair Solutions sales remained flat at $151 million, with operating profit margin contracting by 50 basis points to 20.8%. The company attributed this to ongoing U.S. macroeconomic impacts on technician spending, though it maintained that long-term fundamentals remain intact.

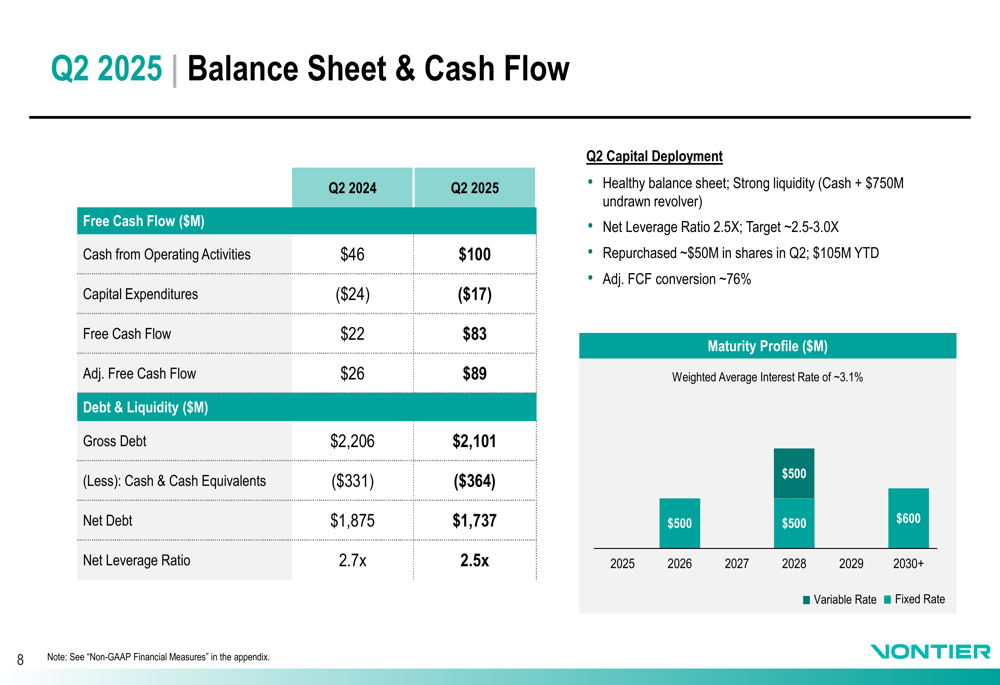

Balance Sheet and Capital Allocation

Vontier continued to strengthen its balance sheet while returning capital to shareholders. The company’s net leverage ratio improved to 2.5x from 2.7x in Q2 2024, with net debt decreasing to $1,737 million.

The following chart illustrates the company’s improved cash flow and balance sheet position:

During Q2 2025, Vontier repurchased approximately $50 million in shares, bringing the year-to-date total to $105 million. The company maintained strong liquidity with $364 million in cash plus a $750 million undrawn revolver.

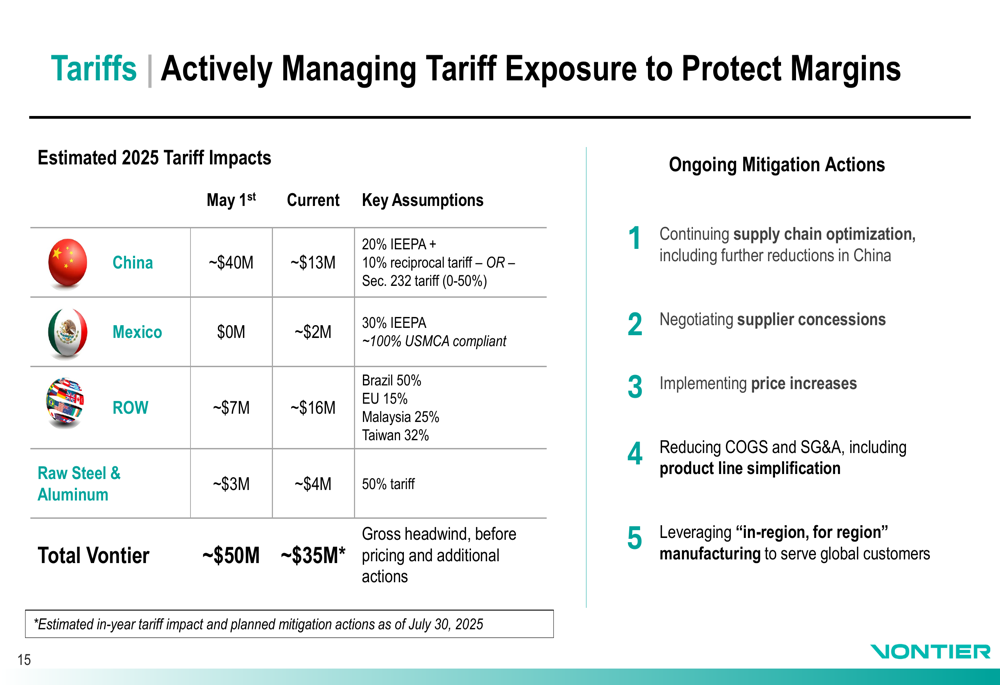

Strategic Initiatives

Vontier highlighted its ongoing strategic focus on driving above-market growth through innovation and its Connected Mobility strategy. The company is actively managing tariff exposure to protect margins, a concern that was also raised during the Q1 2025 earnings call.

The following slide details Vontier’s approach to tariff management:

The company has reduced its estimated 2025 tariff impact from approximately $50 million to $35 million through various mitigation actions, including supply chain optimization, supplier concessions, price increases, and cost reductions. This proactive approach demonstrates management’s ability to navigate challenging macroeconomic conditions.

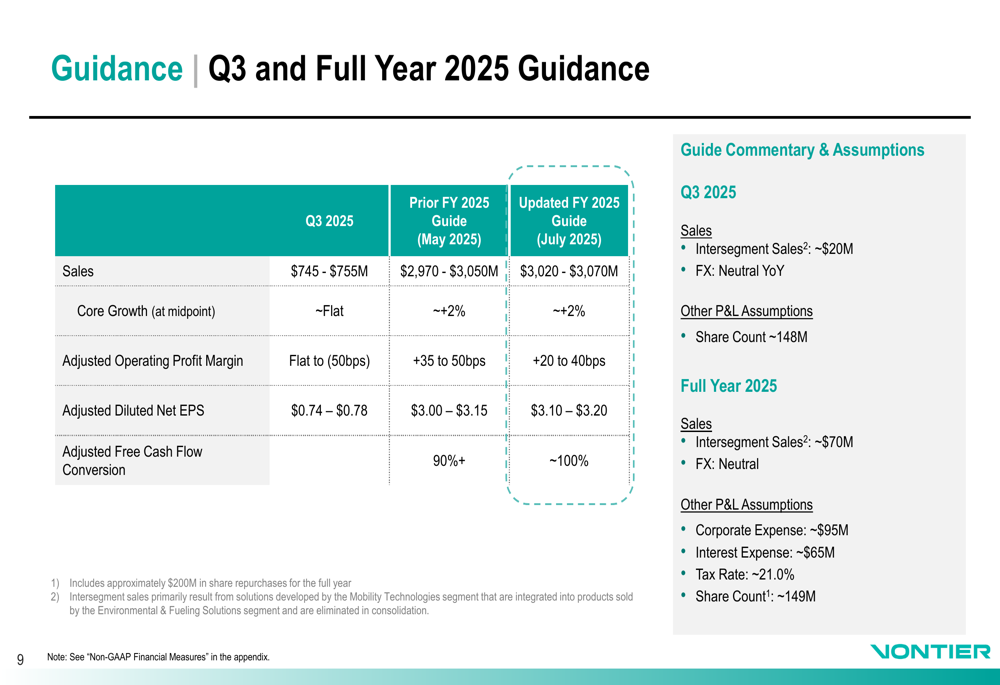

Forward-Looking Statements

Following strong first-half results, Vontier raised its full-year 2025 guidance:

The updated guidance projects full-year sales of $3,020-$3,070 million (up from $2,970-$3,050 million) and adjusted diluted EPS of $3.10-$3.20 (up from $3.00-$3.15). The company also expects adjusted free cash flow conversion of approximately 100%, up from the previous guidance of 90%+.

For Q3 2025, Vontier anticipates sales of $745-$755 million with flat core growth and adjusted diluted EPS of $0.74-$0.78. The company explained that the flat growth outlook for the second half of 2025 is partly due to shipment timing benefits in Q2 that will impact Q3, as well as ongoing market pressure in the Repair Solutions segment.

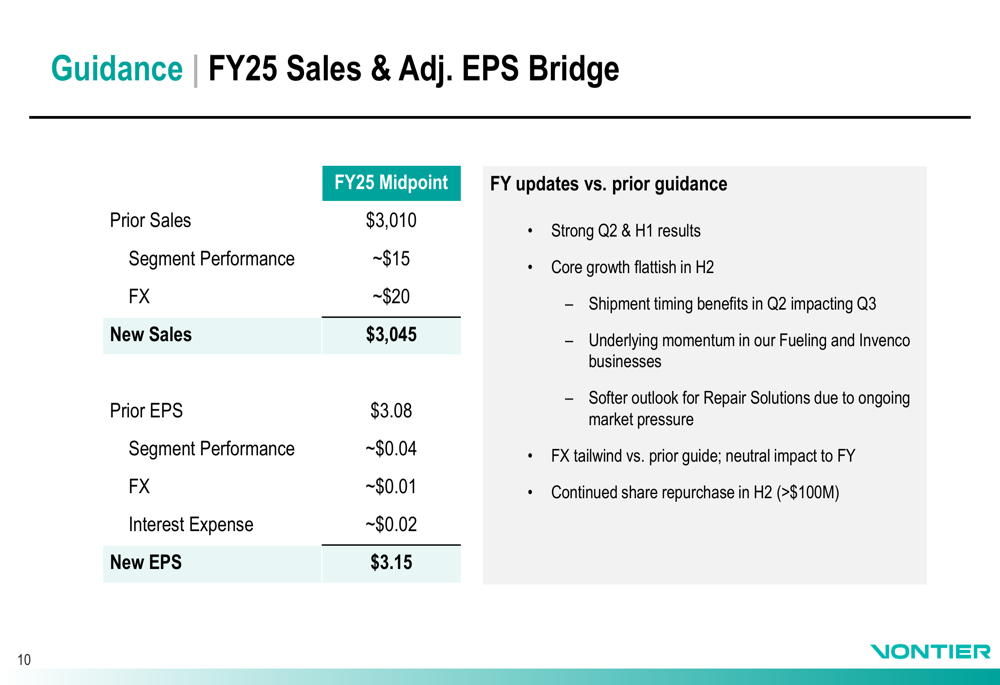

The bridge from prior to updated guidance shows the key drivers of the improved outlook:

The guidance update reflects strong Q2 and first-half results, with segment performance contributing approximately $15 million to sales and $0.04 to EPS. Foreign exchange is expected to provide a modest tailwind compared to prior guidance, contributing about $20 million to sales and $0.01 to EPS.

Conclusion

Vontier’s Q2 2025 presentation demonstrates the company’s ability to execute effectively in a dynamic environment, with strong performance in its Environmental & Fueling Solutions and Mobility Technologies segments offsetting challenges in Repair Solutions. The raised guidance reflects management’s confidence in the company’s strategic direction and operational execution.

The company’s proactive approach to tariff management and focus on innovation and connected mobility solutions position it well for continued growth. However, investors should monitor the ongoing macroeconomic pressures affecting the Repair Solutions segment and potential impacts from global trade tensions.

With improved cash flow generation, a stronger balance sheet, and continued share repurchases, Vontier appears well-positioned to deliver on its updated 2025 financial targets while navigating the evolving market landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.