Texas Roadhouse earnings missed by $0.05, revenue topped estimates

Introduction & Market Context

Warrior Met Coal Inc (NYSE:HCC) released its second quarter 2025 results on August 6, showing operational resilience amid challenging market conditions. The company reported increased production and sales volumes, but faced significant headwinds from lower steelmaking coal prices that substantially impacted financial performance.

After reporting a net loss in Q1 2025, Warrior Met Coal returned to profitability in Q2 with a modest net income of $5.6 million, suggesting sequential improvement despite continued market challenges. The company’s stock responded positively in after-hours trading, rising 3.19% to $55.90 following the results.

Quarterly Performance Highlights

Warrior Met Coal achieved several operational milestones in Q2 2025, including the commercial sales of 239,000 short tons of Blue Creek steelmaking coal and a significant 18% reduction in cash cost of sales quarter-over-quarter to $101.17 per short ton.

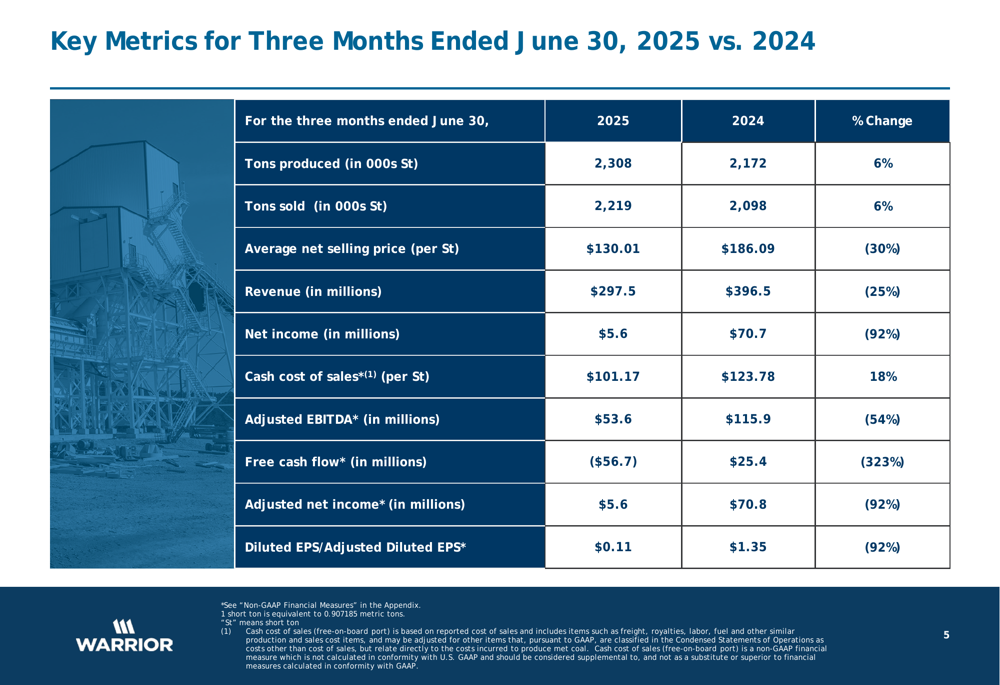

The company reported coal production of 2,308,000 short tons, a 6% increase from Q2 2024, while sales volumes also rose 6% year-over-year to 2,219,000 short tons. However, the average net selling price decreased 30% to $130.01 per short ton compared to $186.09 in the same period last year.

As shown in the following comparison of key financial metrics:

Revenue declined 25% year-over-year to $297.5 million, while net income fell 92% to $5.6 million compared to $70.7 million in Q2 2024. Adjusted EBITDA decreased 54% to $53.6 million, with the adjusted EBITDA margin contracting to 18.0% from 29.2% a year earlier.

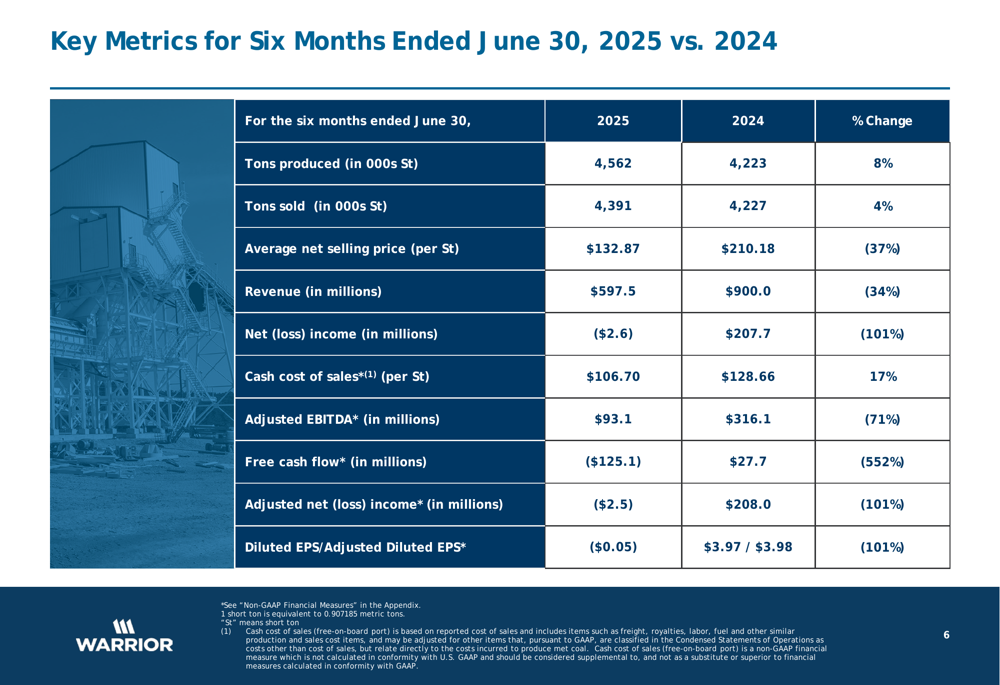

Looking at the first half of 2025, the financial picture shows similar challenges:

Detailed Financial Analysis

The company’s cost control measures have shown positive results, with cash cost of sales (free-on-board port) per short ton decreasing to $101.17 in Q2 2025, an 18% improvement from $123.78 in the previous quarter. This operational efficiency helped partially offset the impact of lower selling prices.

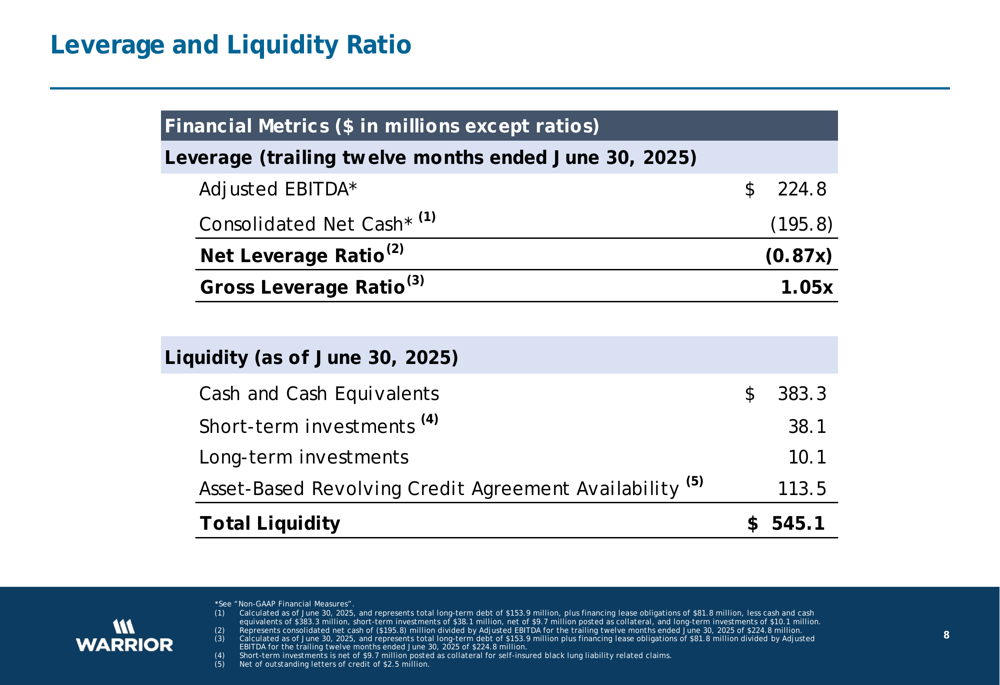

Warrior Met Coal maintained its financial strength with total liquidity of $545.1 million as of June 30, 2025, including $383.3 million in cash and cash equivalents. The company’s balance sheet remains solid with a net leverage ratio of -0.87x, indicating more cash than debt.

The following slide illustrates the company’s strong financial position:

Despite operational improvements, free cash flow turned negative at -$56.7 million for Q2 2025, compared to positive $25.4 million in Q2 2024, primarily due to continued investment in the Blue Creek project and lower operating cash flows from reduced coal prices.

Strategic Initiatives

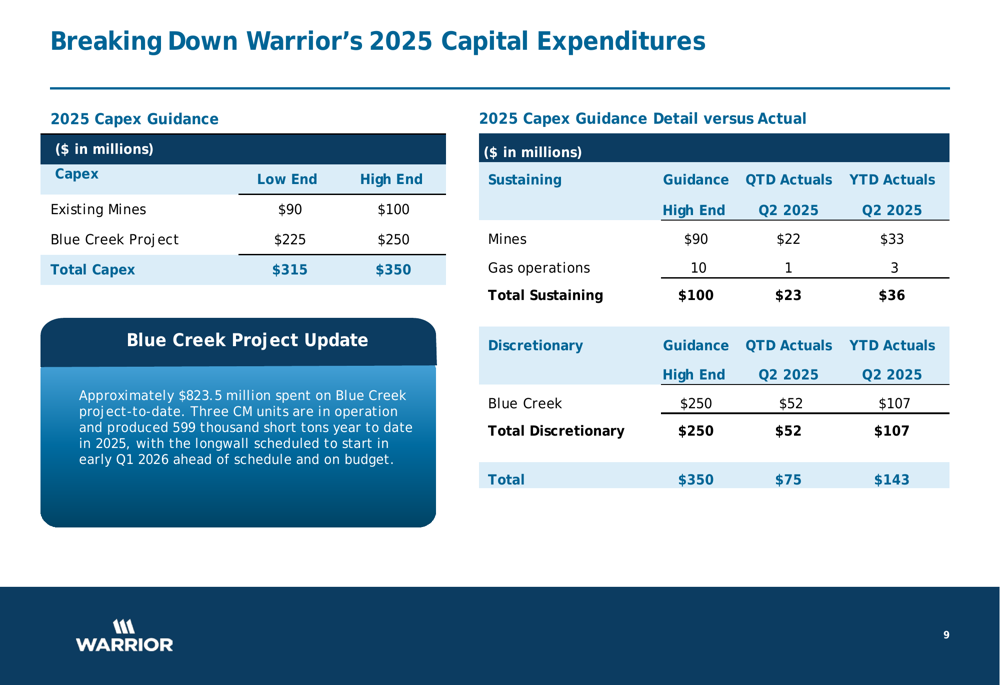

The Blue Creek project remains Warrior Met Coal’s key strategic growth initiative, with the company announcing an acceleration of the longwall startup to early first quarter of 2026. The project is progressing ahead of schedule while staying on budget, with total capital expenditure estimates maintained at $995 million to $1.075 billion.

As of June 30, 2025, Warrior Met Coal has invested $823.5 million in the Blue Creek project, including $51.8 million in Q2 alone. The company highlighted that three continuous miner units are in operation and produced 599,000 short tons year-to-date in 2025.

The following slide provides details on the company’s capital expenditures and Blue Creek project progress:

The Blue Creek project represents a significant expansion of Warrior Met Coal’s production capacity, with the company emphasizing its high-quality asset base:

Management noted that the project scope was proactively expanded by $130 million in 2023 to improve the transportation plan by adding an overland belt and rail loadout, enhancing the company’s ability to deliver product to the Port of Mobile via multiple channels.

Forward-Looking Statements

Warrior Met Coal provided updated guidance for 2025, projecting coal sales between 8.8-9.5 million short tons and coal production between 8.3-9.1 million short tons. Cash cost of sales is expected to range between $110-$120 per short ton.

The company’s capital expenditure guidance remains unchanged, with $90-100 million allocated for existing mines and $225-250 million for the Blue Creek project. Total (EPA:TTEF) capital expenditures for 2025 are projected between $315-350 million.

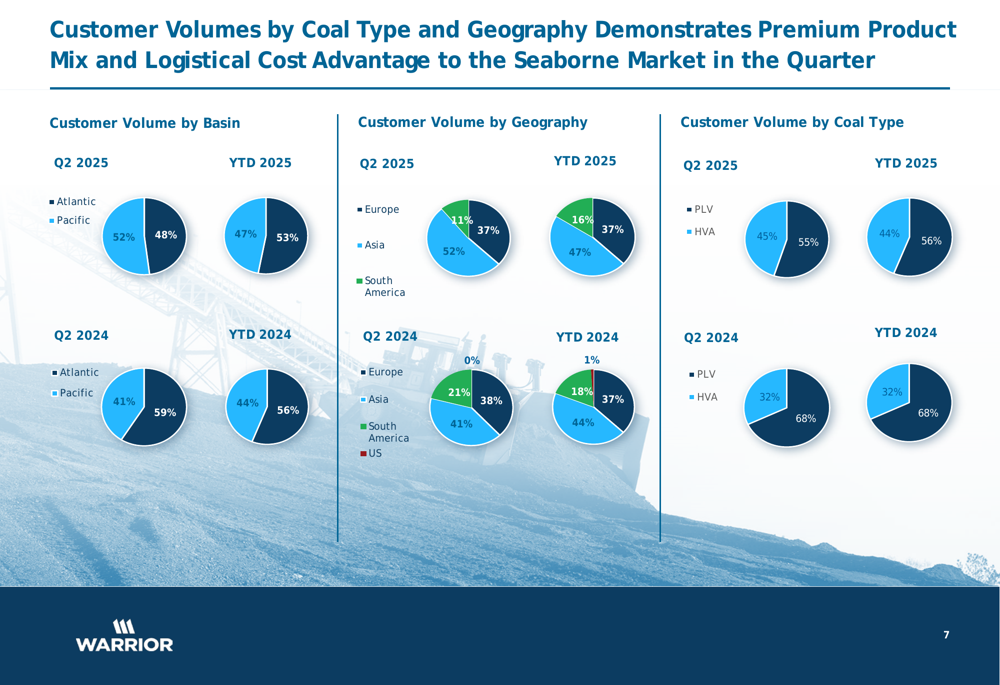

The company’s customer base continues to evolve, with increased sales to Europe and Asia compared to previous periods:

Executive Summary

Warrior Met Coal’s Q2 2025 results demonstrate the company’s ability to navigate challenging market conditions through operational improvements and strategic investments. While financial performance has been significantly impacted by lower steelmaking coal prices, the company has maintained production growth, reduced costs, and continued to advance its key growth project ahead of schedule.

The acceleration of the Blue Creek project timeline suggests confidence in the long-term market outlook despite current price pressures. With a strong balance sheet and substantial liquidity, Warrior Met Coal appears well-positioned to weather the current market environment while investing for future growth.

The company’s return to profitability in Q2 after reporting a loss in Q1 2025 indicates sequential improvement, though year-over-year comparisons remain challenging due to the significant decline in coal prices. Investors will likely focus on the company’s ability to continue optimizing operations while advancing the Blue Creek project toward completion in early 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.