Gold prices cool after hitting over 2-week high on Fed independence fears

Introduction & Market Context

Waystar Holding Corp (NYSE:WAY) presented its first quarter 2025 financial results on April 30, showcasing continued momentum with 14% year-over-year revenue growth. The healthcare revenue cycle management software provider has maintained its growth trajectory while significantly strengthening its balance sheet through substantial debt reduction.

The company’s stock has performed well, trading at $40.49 as of May 9, 2025, within a 52-week range of $20.26 to $48.11. Following the earnings announcement, the stock saw a 4.94% increase in after-hours trading, reflecting positive investor sentiment toward the company’s performance and raised guidance.

Quarterly Performance Highlights

Waystar delivered strong financial results across key metrics for the first quarter of 2025, continuing its pattern of consistent growth.

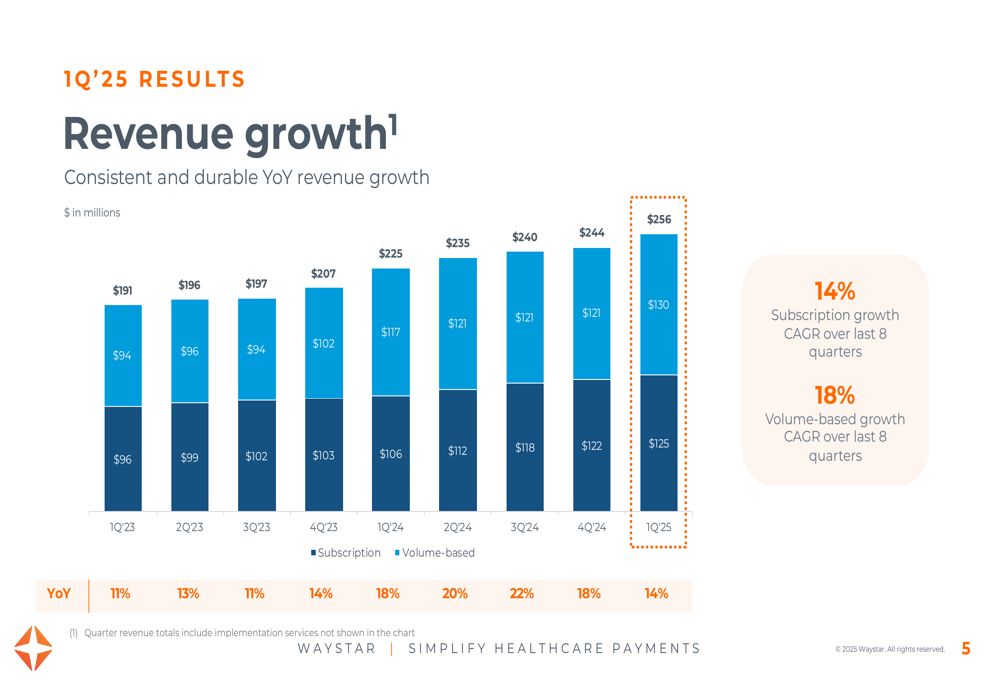

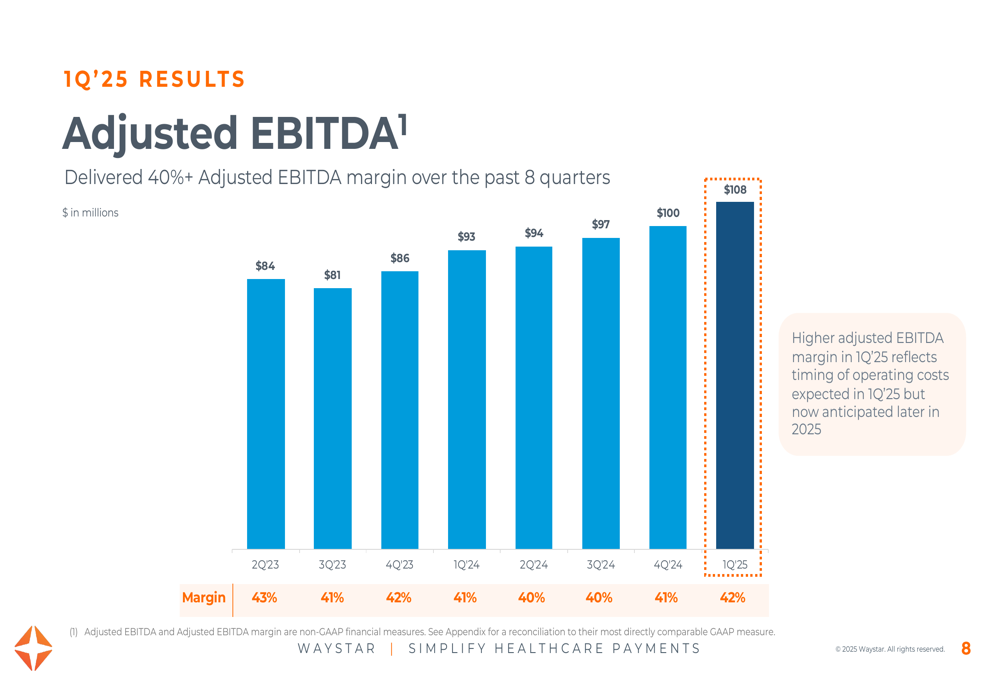

Revenue reached $256.4 million, representing a 14% increase compared to Q1 2024. This growth was balanced across both subscription revenue ($130 million) and volume-based revenue ($125 million). Adjusted EBITDA grew 16% year-over-year to $108 million, with a margin of 42%.

As shown in the following chart of quarterly revenue performance, Waystar has maintained steady growth over the past two years:

The company’s profitability has shown consistent improvement, with Adjusted EBITDA reaching $108 million in Q1 2025, up from $93 million in Q1 2024. Management noted that the higher adjusted EBITDA margin in Q1 2025 reflects timing of operating costs that are now anticipated later in 2025.

Detailed Financial Analysis

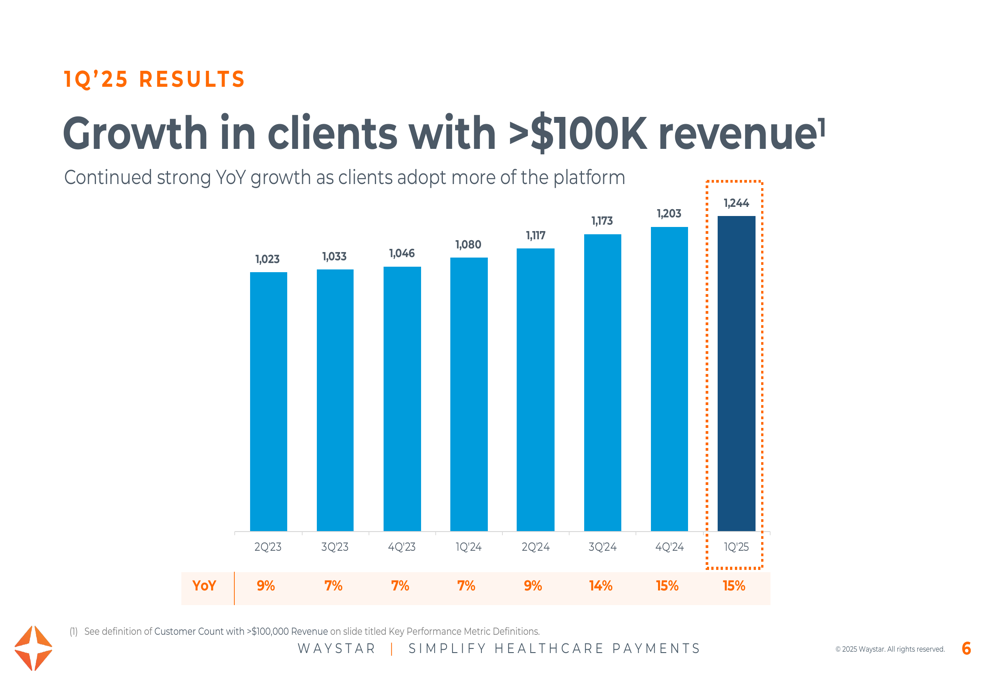

A key strength in Waystar’s business model is its ability to expand relationships with existing clients while adding new high-value customers. The number of clients generating over $100,000 in trailing twelve-month revenue increased by 15% year-over-year to 1,244 in Q1 2025.

The following chart illustrates this consistent growth in high-value clients:

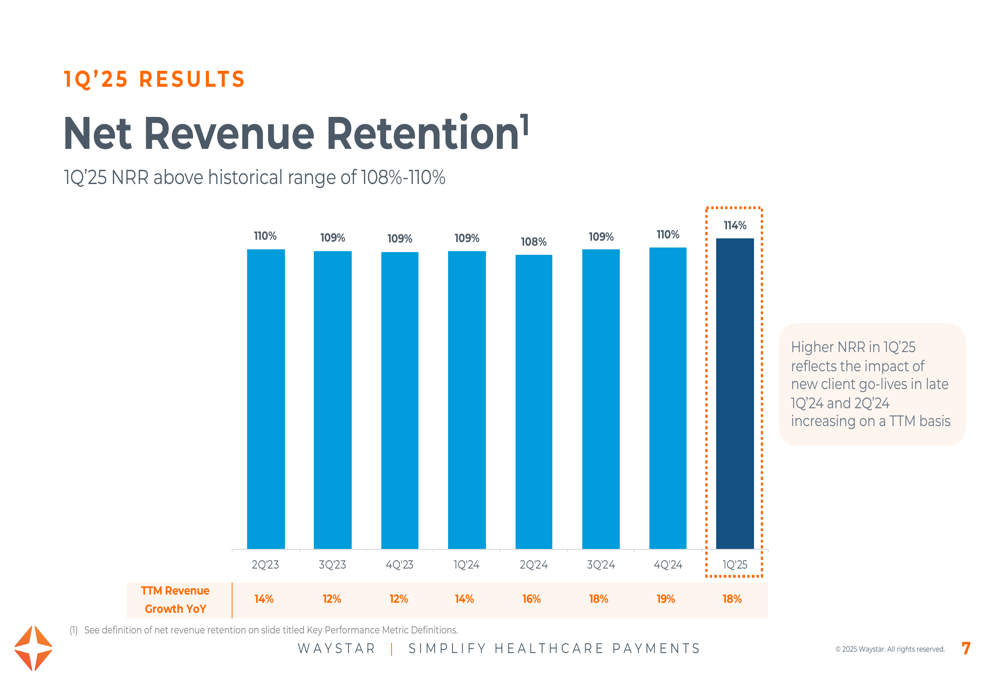

Net revenue retention rate, a critical metric indicating the company’s ability to retain and grow revenue from existing customers, improved to 114% in Q1 2025, up from 109% in the same period last year. Management attributed this improvement to new client go-lives in late Q1 2024 and Q2 2024 increasing on a trailing twelve-month basis.

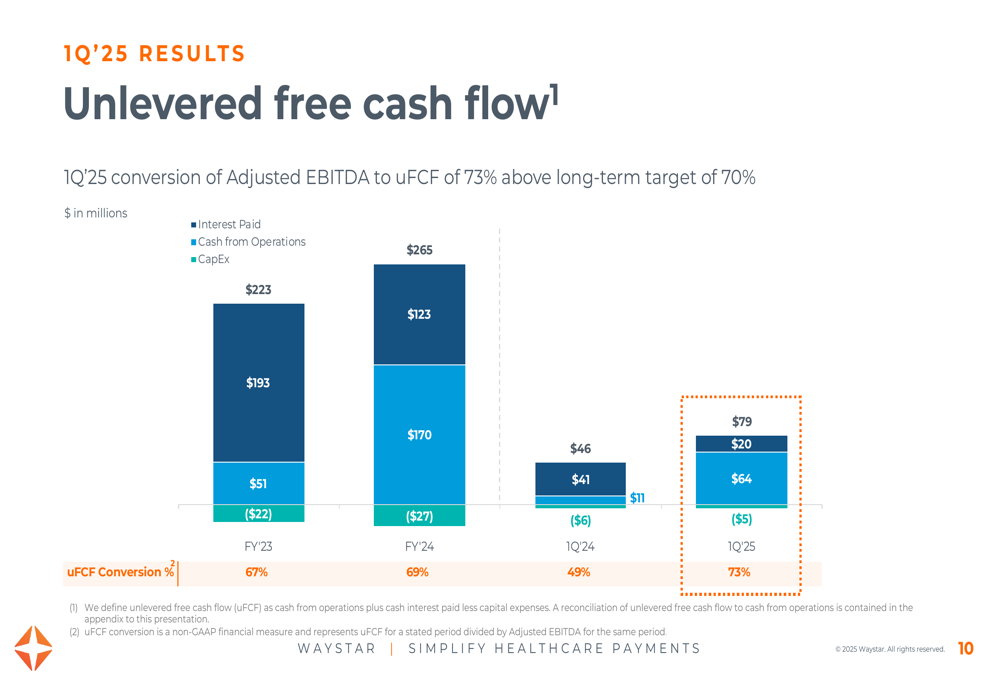

Waystar’s cash flow generation has also strengthened considerably. Unlevered free cash flow reached $79 million in Q1 2025, representing a 73% conversion rate of Adjusted EBITDA to unlevered free cash flow – exceeding the company’s long-term target of 70%.

Strategic Initiatives & Debt Management

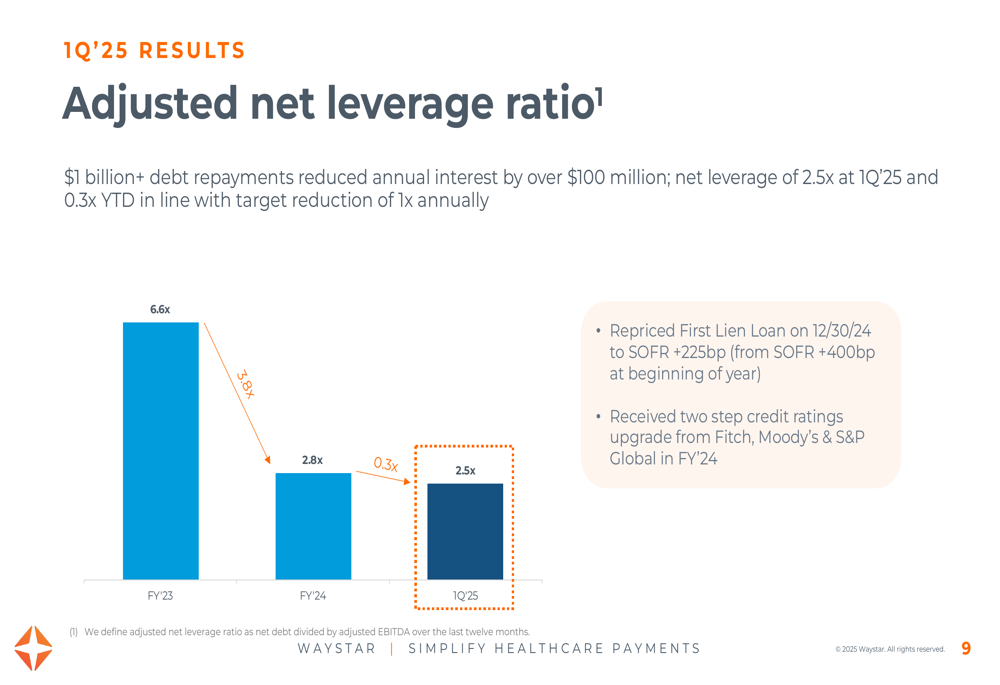

Perhaps the most significant improvement in Waystar’s financial position has been its substantial debt reduction. The company has reduced its adjusted net leverage ratio from 6.6x in FY 2023 to just 2.5x in Q1 2025, representing a dramatic strengthening of its balance sheet.

This debt reduction has been achieved through over $1 billion in debt repayments, which has reduced annual interest expenses by more than $100 million. The company also successfully repriced its First Lien Loan on December 30, 2024, to SOFR +225bp, down from SOFR +400bp at the beginning of the year.

As shown in the following chart, Waystar’s leverage reduction has been substantial:

These financial improvements have been recognized by major credit rating agencies, with Waystar receiving two-step credit ratings upgrades from Fitch, Moody’s, and S&P Global in FY 2024.

Forward-Looking Statements & Guidance

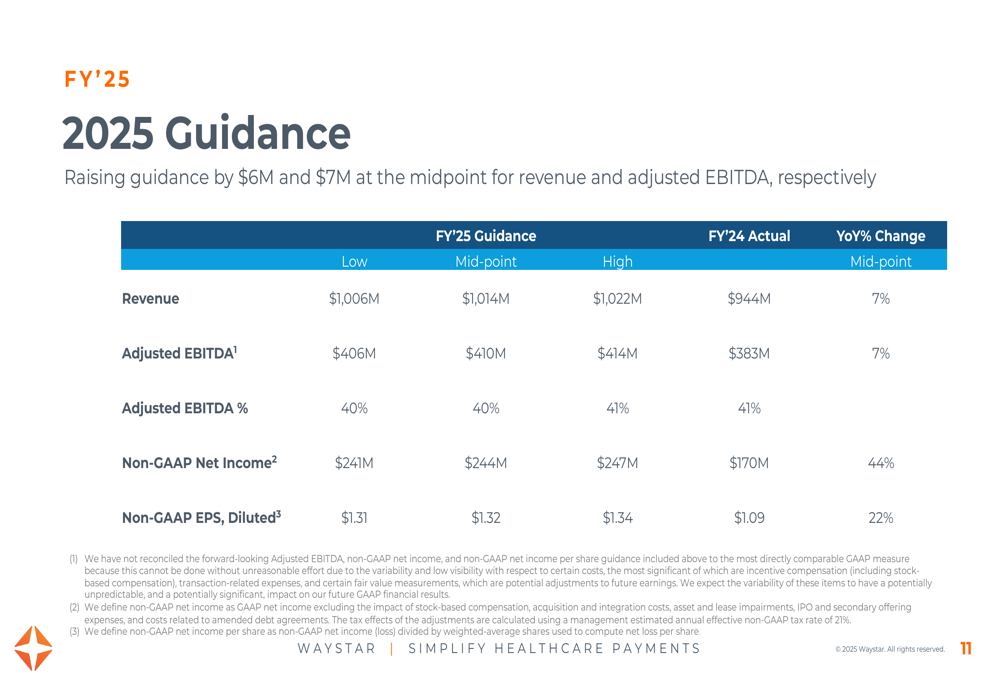

Based on its strong Q1 performance, Waystar raised its full-year 2025 guidance by $6 million for revenue and $7 million for adjusted EBITDA at the midpoint. The company now expects:

- Revenue between $1,006 million and $1,022 million (midpoint:$1,014 million, representing 7% year-over-year growth)

- Adjusted EBITDA between $406 million and $414 million (midpoint:$410 million, 7% growth)

- Non-GAAP EPS between $1.31 and $1.34 (midpoint:$1.32, 22% growth)

The detailed guidance is presented in the following table:

CEO Matt Hawkins (NASDAQ:HWKN) emphasized the company’s transition from "AI hype to ROI reality," highlighting the tangible benefits of Waystar’s mission-critical software platform. During the earnings call, Hawkins expressed confidence in Waystar’s ability to be a "net winner during this economic cycle."

The company’s guidance assumptions include approximately $26 million in stock-based compensation expense, $73 million in net interest expense, a 21% non-GAAP effective tax rate, and approximately 184 million fully diluted weighted average shares outstanding for FY 2025.

Waystar’s consistent performance and improved financial health position it well for continued growth in the healthcare revenue cycle management market, with its focus on AI and automation capabilities expected to drive further innovation and market expansion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.