Stock market today: S&P 500 climbs as health care, tech gain; Nvidia earnings loom

Introduction & Market Context

Waystar Holding Corp (NYSE:WAY) released its second quarter 2025 financial results on July 30, showing continued momentum with double-digit growth across key metrics. The healthcare payments technology company reported 15% year-over-year revenue growth while maintaining strong profitability margins.

The stock closed at $35.69 on the day of the announcement and gained 1.15% in after-hours trading, reflecting positive investor sentiment toward the results and raised guidance. Over the past year, Waystar’s stock has traded between $20.74 and $48.11, demonstrating significant volatility despite the company’s consistent operational performance.

Quarterly Performance Highlights

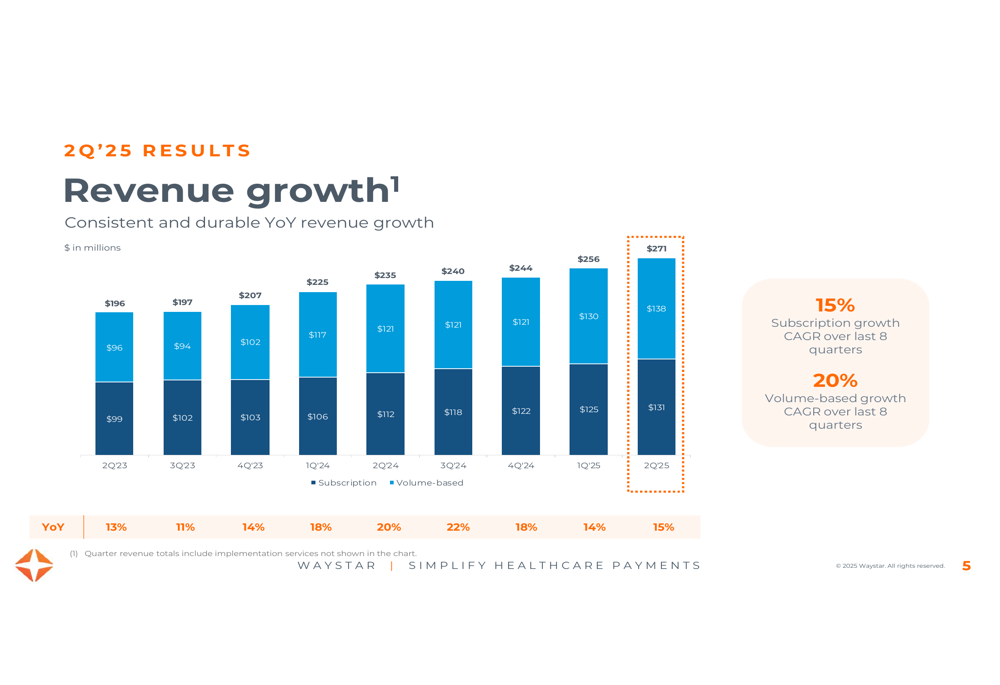

Waystar delivered robust second quarter results with revenue reaching $271 million, representing 15% growth compared to Q2 2024. The company maintained its strong profitability with adjusted EBITDA growing 20% year-over-year to $113 million, resulting in an impressive 42% margin.

As shown in the following chart of quarterly performance metrics:

The company’s revenue mix remained balanced between subscription-based and volume-based sources. Subscription revenue, which provides greater predictability, reached $138 million in Q2 2025, while volume-based revenue totaled $133 million. Both revenue streams have shown consistent growth, with subscription revenue achieving a 15% CAGR and volume-based revenue posting a 20% CAGR over the past eight quarters.

This revenue composition is illustrated in the following chart:

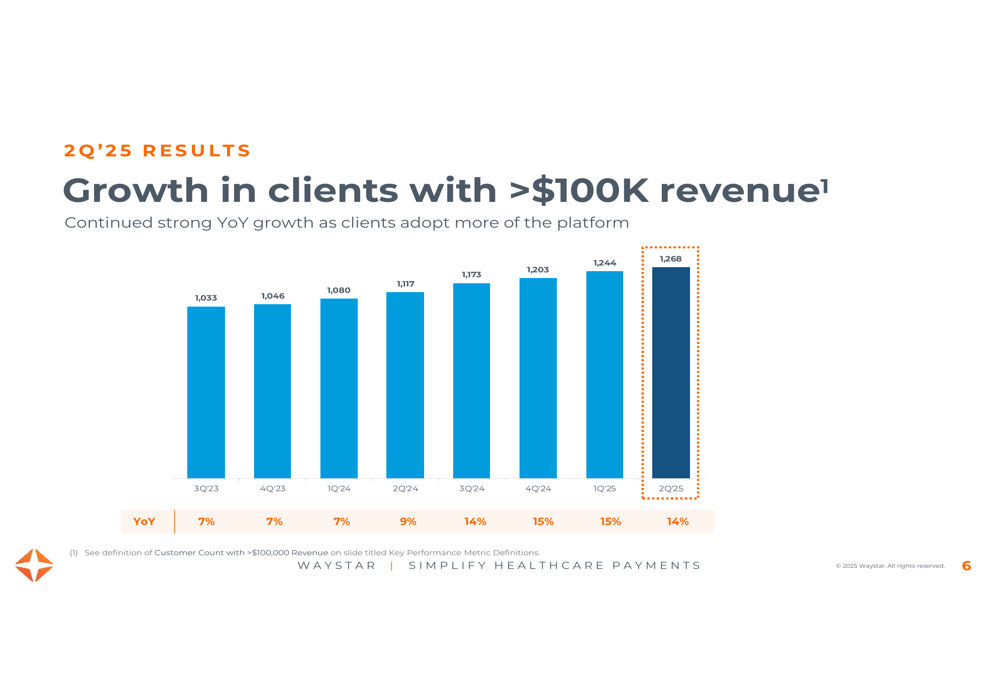

Waystar’s client base continues to expand, with the number of customers generating over $100,000 in trailing twelve-month revenue increasing 14% year-over-year to 1,268. This metric serves as an important indicator of the company’s ability to attract and retain larger, more profitable clients.

The growth trend in high-value clients is shown here:

Detailed Financial Analysis

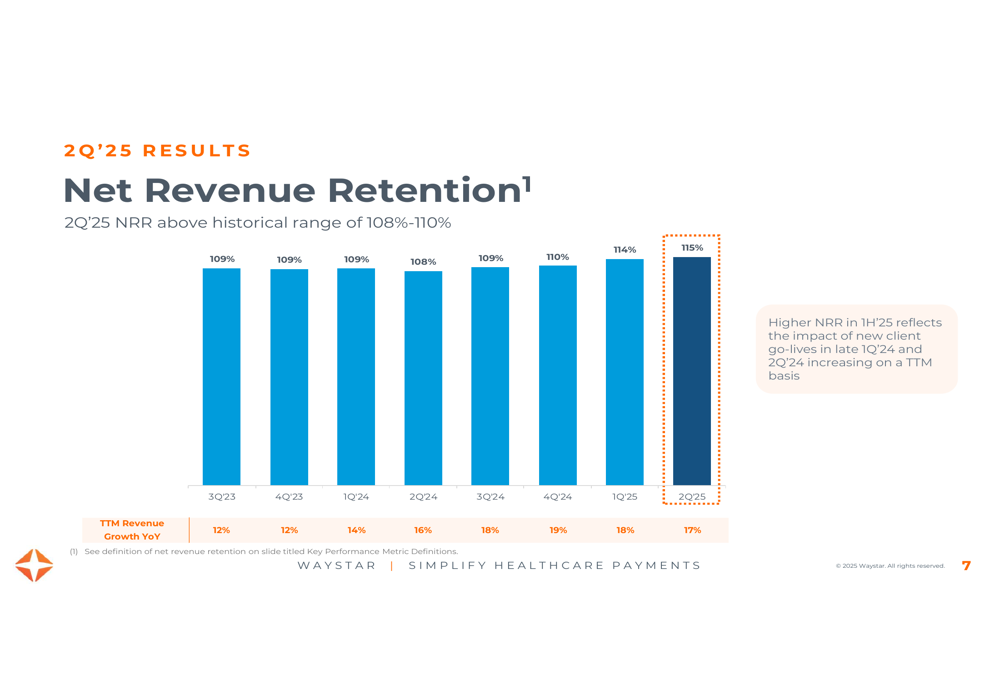

Net revenue retention, a critical measure of Waystar’s ability to expand relationships with existing clients, reached 115% in Q2 2025, exceeding the company’s historical range of 108-110%. Management attributed this improvement to new client implementations that began in late Q1 and Q2 of 2024, which are now fully reflected in trailing twelve-month calculations.

The following chart demonstrates this positive trend:

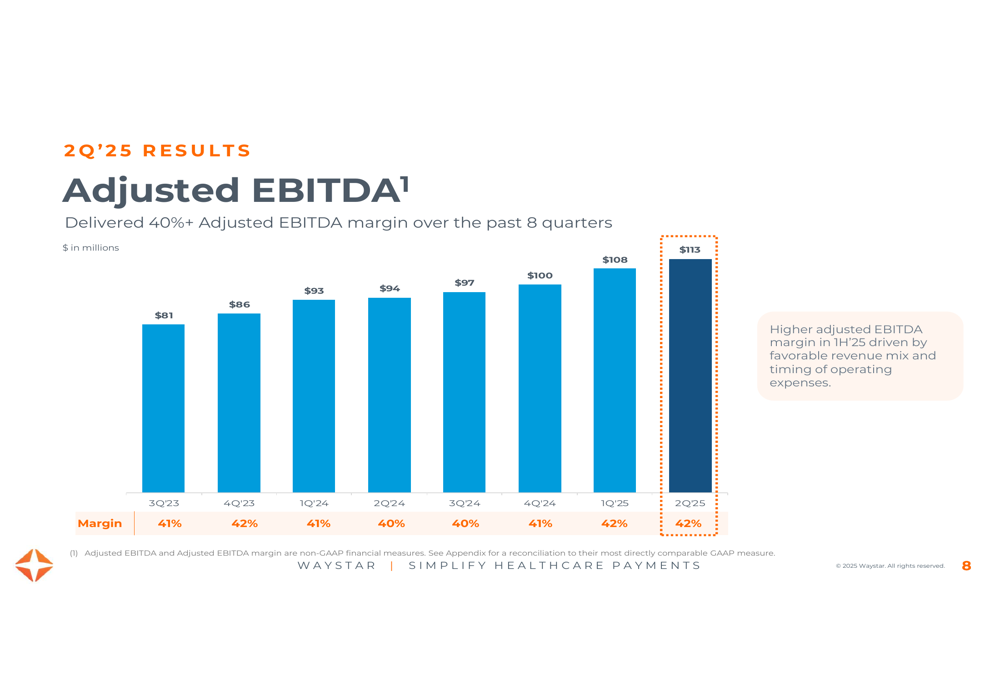

Waystar’s profitability remains a key strength, with adjusted EBITDA margins consistently exceeding 40% over the past eight quarters. In Q2 2025, the company achieved a 42% adjusted EBITDA margin, driven by favorable revenue mix and timing of operating expenses.

The adjusted EBITDA performance is illustrated here:

Cash flow generation has been equally impressive, with unlevered free cash flow conversion reaching 86% of adjusted EBITDA in the first half of 2025, significantly above the company’s long-term target of 70%. However, management noted that this performance benefited from the deferral of approximately $27 million in federal tax payments to Q4 2025.

Strategic Initiatives & Forward Outlook

Waystar continues to make significant progress on its deleveraging strategy. The company has reduced its adjusted net leverage ratio from 6.6x at the end of fiscal 2023 to 2.2x by Q2 2025. This improvement follows over $1 billion in debt repayment during 2024, which reduced annual interest expenses by more than $100 million.

The company also successfully repriced its First Lien Loan in December 2024, reducing the interest rate from SOFR +400bp to SOFR +225bp, and received multiple credit rating upgrades from major agencies including Fitch, Moody’s, and S&P Global.

Looking ahead, Waystar expects its leverage ratio to increase to approximately 3.5x following the closure of its previously announced acquisition of Iodine Software (ETR:SOWGn), which is expected to complete by the end of 2025. While specific details about the acquisition’s strategic benefits weren’t highlighted in the presentation, this move appears aligned with the company’s growth strategy.

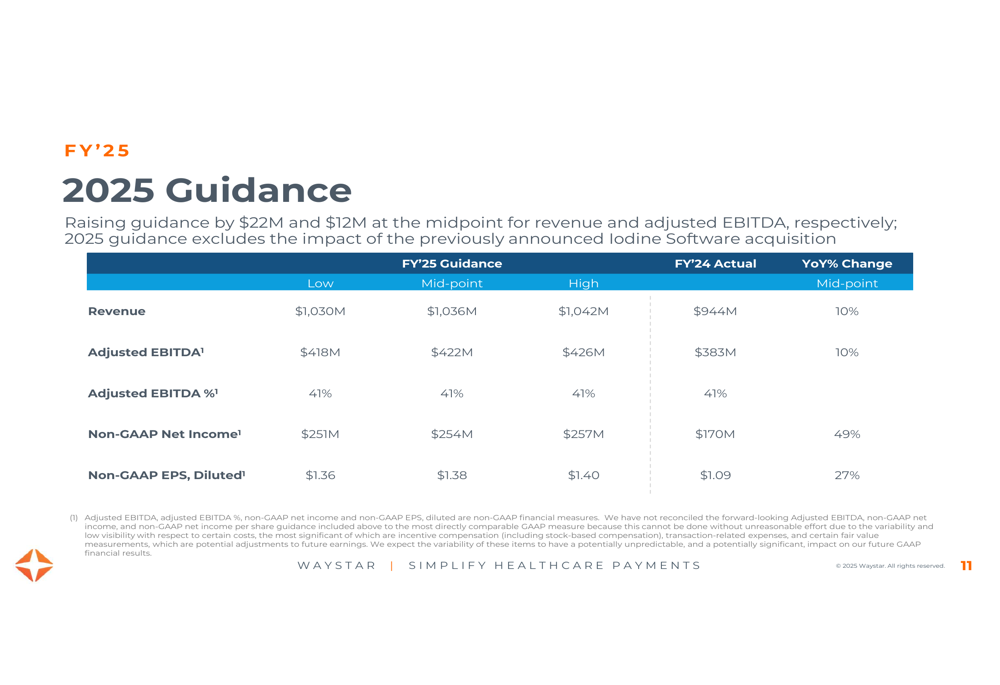

Guidance Update

Based on strong first-half performance, Waystar raised its full-year 2025 guidance by $22 million for revenue and $12 million for adjusted EBITDA at the midpoint. The updated guidance, which excludes the impact of the pending Iodine Software acquisition, projects:

As shown in the following guidance table:

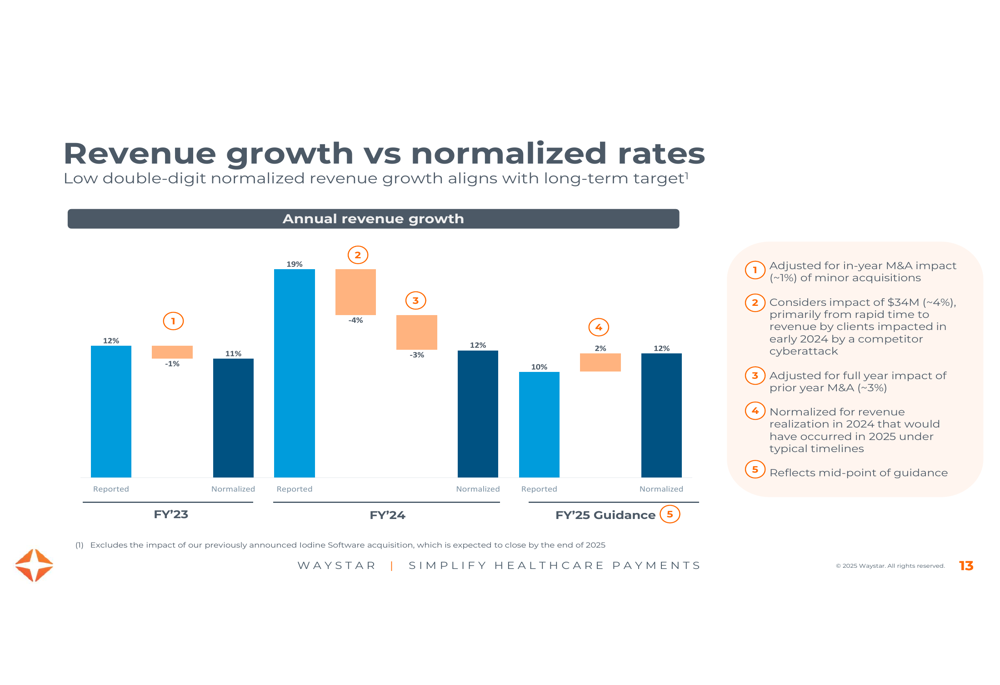

The new midpoint revenue guidance of $1,036 million represents 10% year-over-year growth. When normalized for one-time factors, including the impact of accelerated revenue in 2024 from clients affected by a competitor’s cyberattack, the underlying growth rate is approximately 12%, which aligns with the company’s long-term target of low double-digit growth.

This normalized view of revenue growth is illustrated in the following chart:

Management’s guidance assumptions include approximately $41 million in stock-based compensation expense, $72 million in net interest expense (based on a 1-month SOFR base rate of 4.3%), and a non-GAAP effective tax rate of approximately 21% on adjustable items.

With consistent revenue growth, strong margins, improving client metrics, and a healthier balance sheet, Waystar appears well-positioned to deliver on its 2025 financial targets while continuing to execute on its long-term strategic objectives in the healthcare payments technology sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.