Texas Roadhouse earnings missed by $0.05, revenue topped estimates

West Fraser Timber Co Ltd (NYSE:WFG) presented its second-quarter 2025 results on July 24, revealing a significant decline in profitability amid challenging market conditions in the wood products sector. The company’s presentation highlighted both near-term challenges and long-term strategic initiatives designed to enhance resilience through product and geographic diversification.

Quarterly Performance Highlights

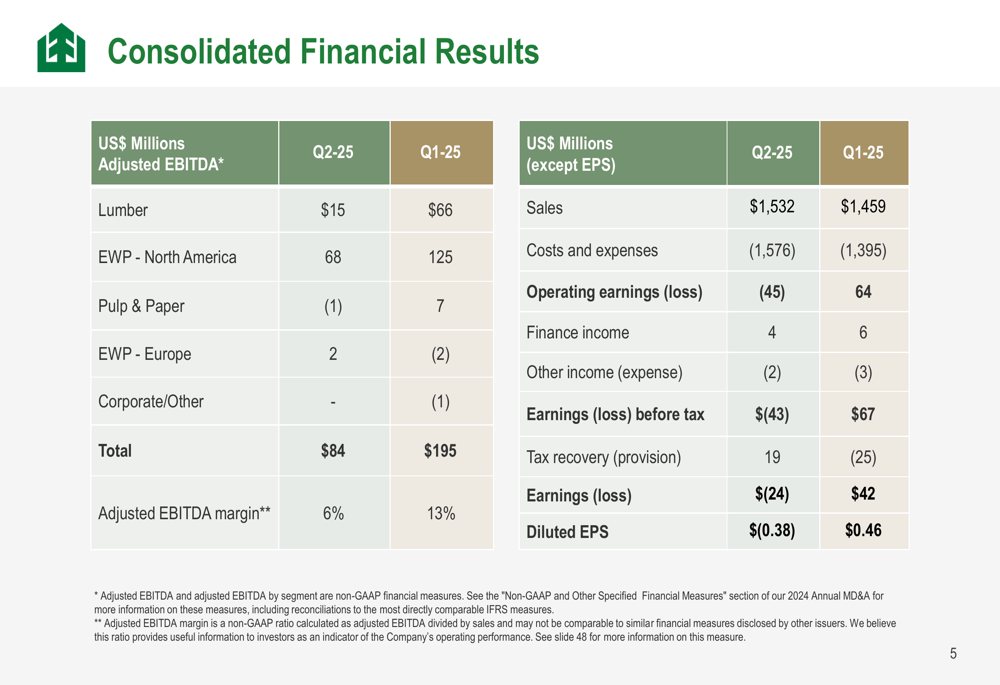

West Fraser reported a substantial decline in adjusted EBITDA to $84 million in Q2 2025, down from $195 million in the previous quarter, representing a 57% decrease. The adjusted EBITDA margin contracted to 6% from 13% in Q1. The company posted an operating loss of $45 million compared to operating earnings of $64 million in Q1, resulting in a diluted loss per share of $0.38 versus earnings of $0.46 in the previous quarter.

As shown in the following financial results comparison:

The earnings decline came despite a modest increase in sales to $1,532 million from $1,459 million in Q1. This revenue growth was driven by higher shipment volumes across all product segments, with lumber shipments increasing by 137 MMfbm to 1,376 MMfbm and North American OSB shipments rising by 207 MMsf to 1,710 MMsf.

The company’s performance fell significantly short of market expectations, with the reported EPS of -$0.38 missing analysts’ forecasts of $0.88 by a wide margin. Following the earnings announcement, West Fraser’s stock declined by 5.95% to close at $70.95, approaching its 52-week low of $69.48.

Detailed Financial Analysis

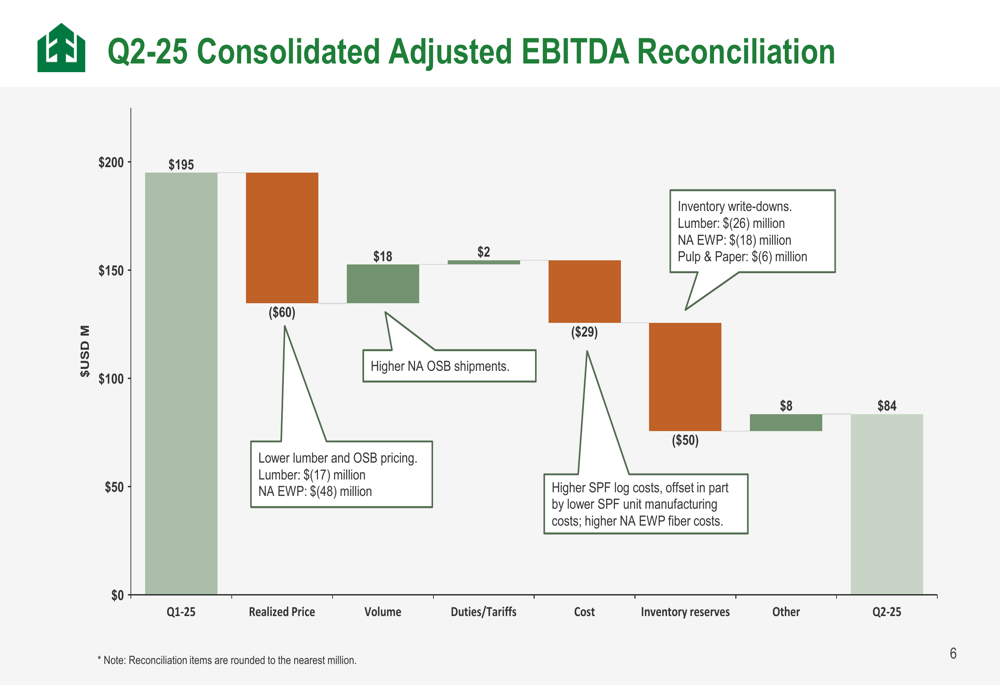

West Fraser’s presentation provided a detailed reconciliation of the quarter-over-quarter decline in adjusted EBITDA, attributing the $111 million decrease to several key factors:

Lower realized prices for lumber and oriented strand board (OSB) reduced EBITDA by $60 million, with North American engineered wood products (EWP) accounting for $48 million of this decline. Cost increases further reduced EBITDA by $29 million, driven by higher SPF log costs and North American EWP fiber costs. Notably, inventory write-downs had a substantial $50 million negative impact, affecting the Lumber (-$26M), North American EWP (-$18M), and Pulp & Paper (-$6M) segments.

These negative factors were partially offset by an $18 million benefit from higher shipment volumes, particularly in the North American OSB segment, which saw seasonally stronger consumption.

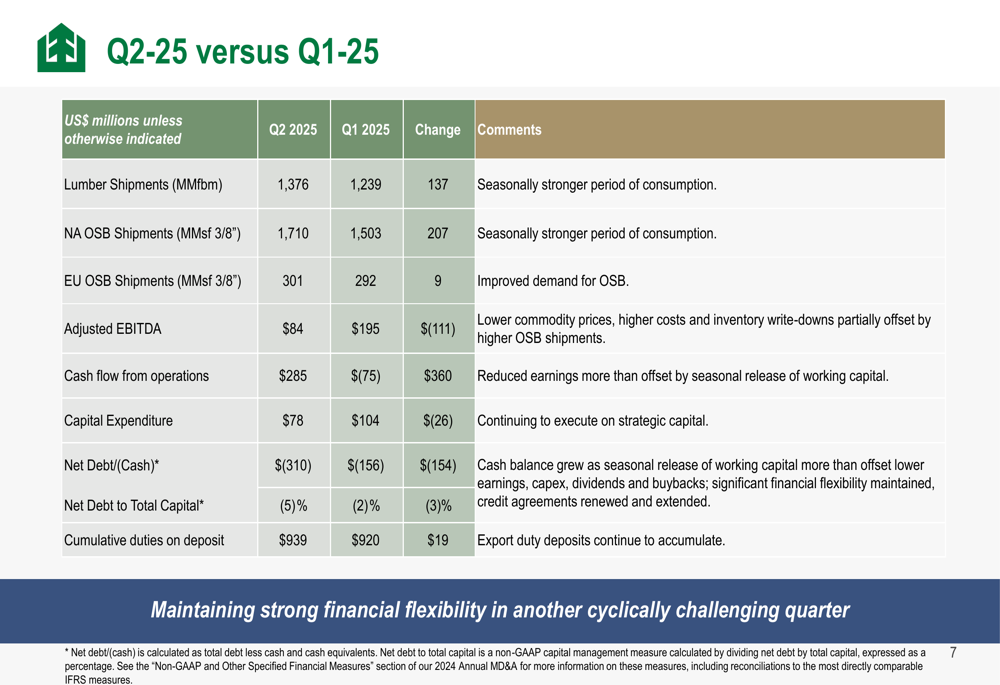

Despite the earnings decline, West Fraser strengthened its financial position during the quarter. Cash flow from operations improved dramatically to $285 million from -$75 million in Q1, driven by a seasonal release of working capital. The company’s net cash position increased to $310 million from $156 million in the previous quarter, providing significant financial flexibility.

As shown in this key metrics comparison:

Strategic Initiatives

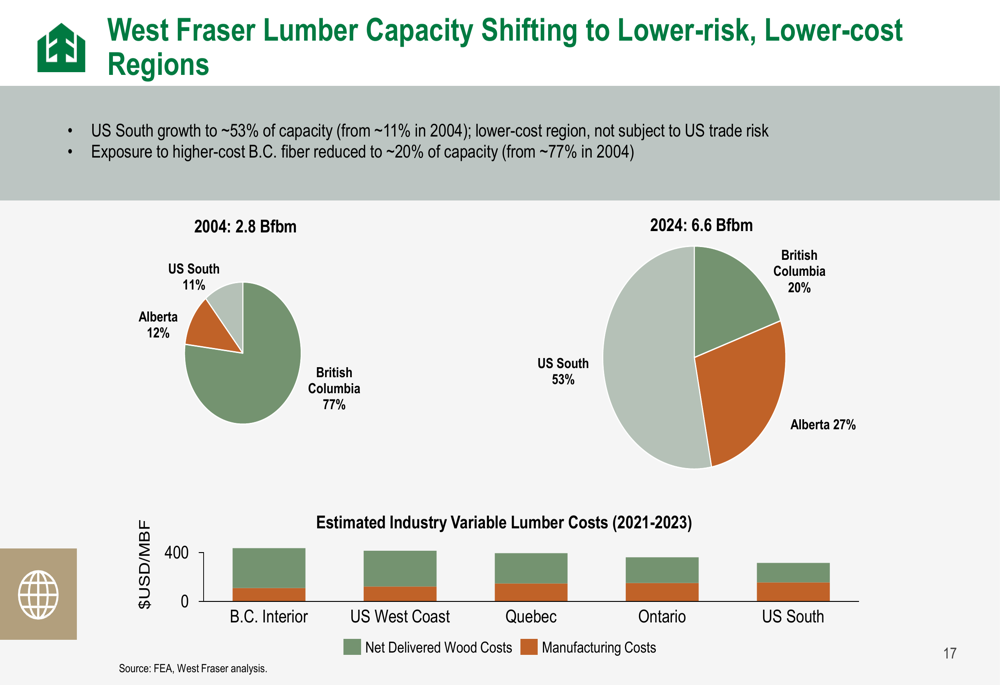

West Fraser’s presentation emphasized its ongoing strategic shift toward lower-risk, lower-cost regions, particularly the U.S. South. This geographic diversification strategy has substantially transformed the company’s production footprint over the past two decades.

The following chart illustrates this strategic shift:

The U.S. South now accounts for approximately 53% of West Fraser’s lumber capacity, up from just 11% in 2004. Conversely, exposure to higher-cost British Columbia fiber has been reduced to 20% of capacity from 77% in 2004. This transformation positions the company to better withstand market cycles and cost pressures.

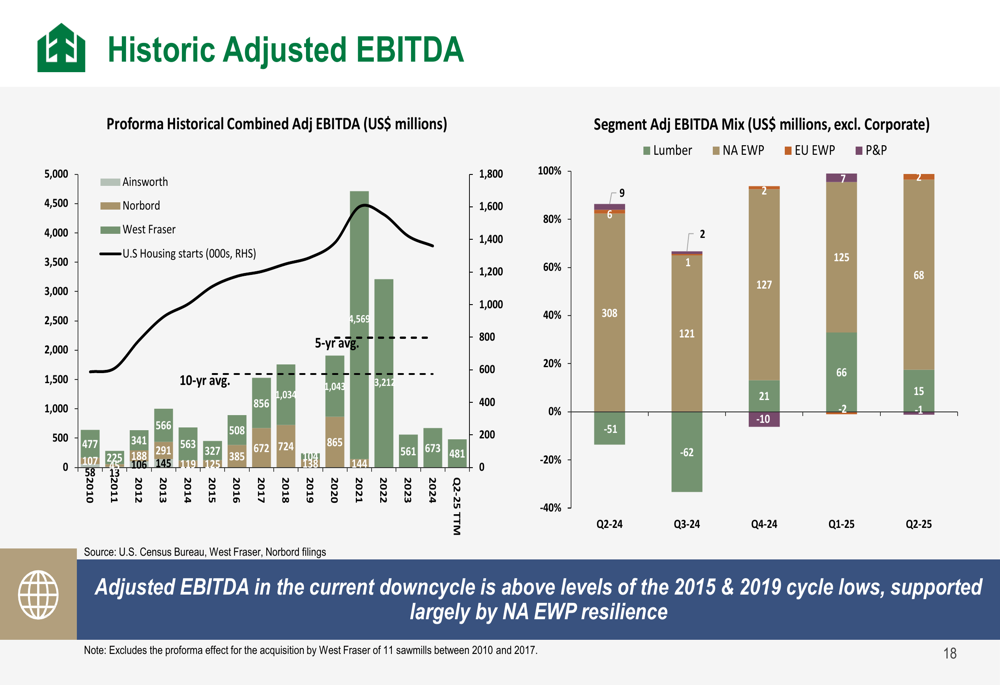

West Fraser also highlighted the diversity of its product portfolio and end markets as a source of resilience. The company’s historical adjusted EBITDA performance demonstrates how different segments can support overall results during various market cycles:

The presentation outlined six key pillars that form the foundation of West Fraser’s investment case, emphasizing its position as one of the world’s largest producers of sustainable wood-based building products:

Forward-Looking Statements

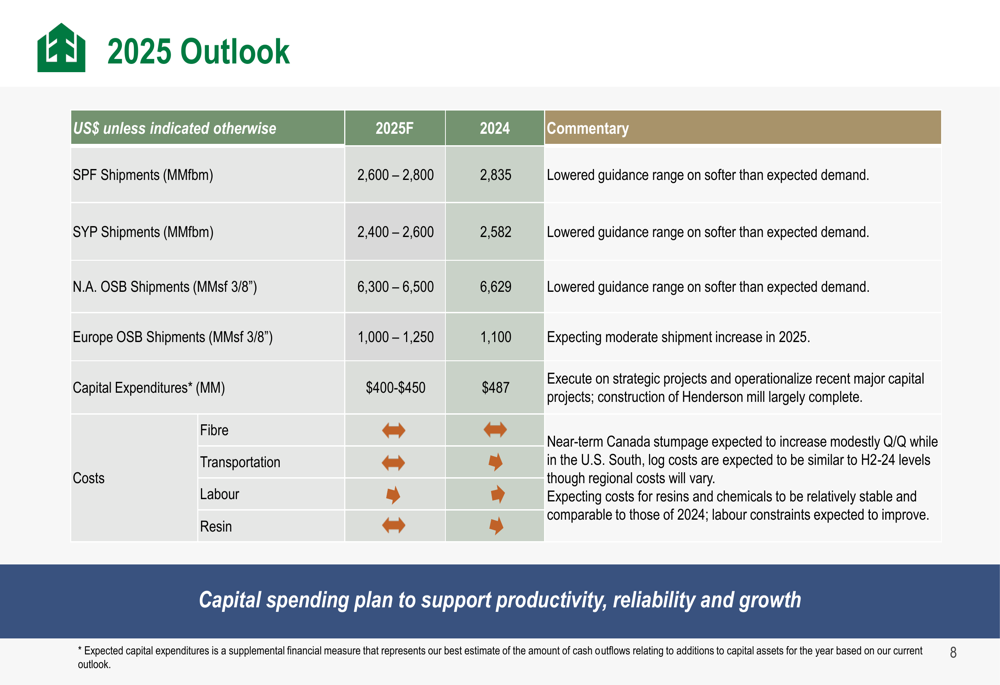

Looking ahead, West Fraser has adjusted its 2025 outlook in response to softer-than-expected demand. The company lowered its shipment guidance across multiple segments:

SPF shipments are now projected at 2,600-2,800 MMfbm (down from previous guidance), SYP shipments at 2,400-2,600 MMfbm, and North American OSB shipments at 6,300-6,500 MMsf. Capital expenditures are expected to range from $400-$450 million as the company continues to execute strategic projects, including the largely completed Henderson mill modernization.

Cost pressures remain a concern, with the company anticipating increases in fiber, transportation, labor, and resin costs throughout 2025.

During the earnings call, CEO Sean McLaren maintained an optimistic long-term outlook despite acknowledging near-term challenges: "We aim to deliver strong financial results through the business cycle." CFO Chris Vorostik added, "It’s in our DNA to deal with the cycles that we have and to drive cash flow even in difficult markets."

The company continues to face uncertainty related to softwood lumber duties, with cumulative duties on deposit increasing to $939 million in Q2. Management indicated openness to potential lumber export quota discussions as a potential resolution to ongoing trade disputes.

Despite the challenging quarter, West Fraser maintained its shareholder returns, declaring a quarterly dividend of $0.32 per share and repurchasing approximately 0.45 million shares under its Normal Course Issuer Bid program, demonstrating confidence in its long-term strategy and financial strength.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.