Oil prices hold sharp losses with focus on secondary India tariffs

Introduction & Market Context

West Pharmaceutical Services Inc (NYSE:WST) released its first quarter 2025 financial results on April 24, showing modest sales growth but declining earnings per share compared to the same period last year. The pharmaceutical packaging and delivery systems manufacturer reported a slight increase in net sales amid challenging market conditions.

The quarterly results come after a difficult period for the company, which saw its stock drop significantly following its Q4 2024 earnings release despite beating analyst expectations. According to the latest fundamentals data, West Pharmaceutical (TADAWUL:2070)’s stock has begun to recover, trading up 3.13% in premarket activity at $225.00, still well below its 52-week high of $390.33.

Quarterly Performance Highlights

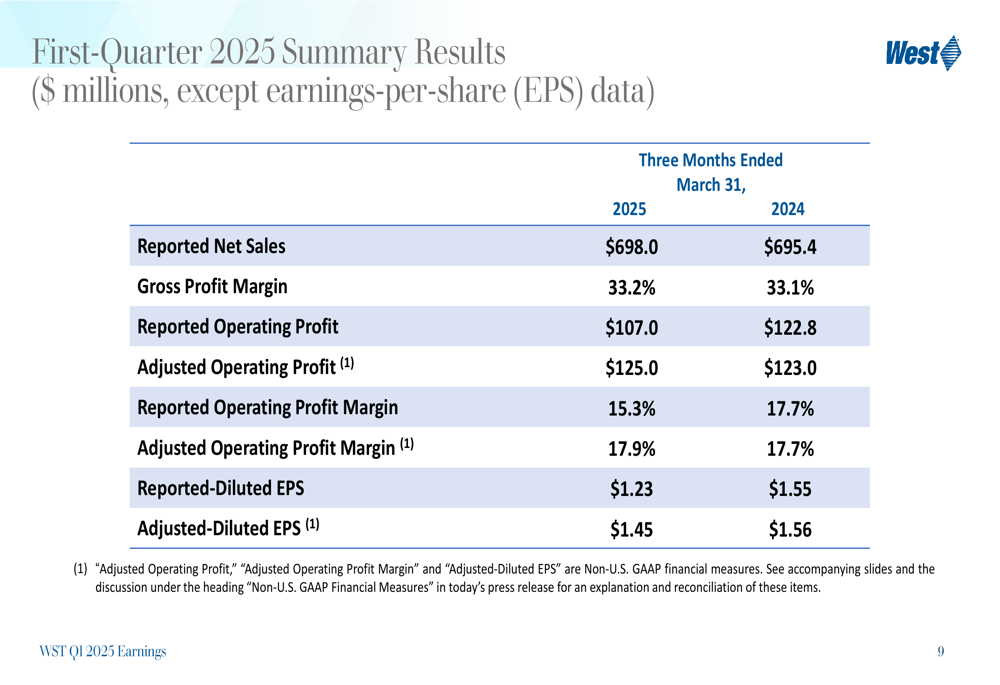

West Pharmaceutical reported first quarter 2025 net sales of $698.0 million, representing a modest 0.4% increase from the prior year, with organic net sales growth of 2.1% when excluding currency effects.

"We delivered a solid first quarter performance, exceeding our guidance, and capitalizing on areas of strength to improve margins and returns," said Eric M. Green, President, CEO and Chair of the Board. "We remain confident in achieving our guidance while closely monitoring political and macroeconomic impacts."

Despite the sales growth, the company’s profitability metrics showed some pressure. Reported diluted EPS came in at $1.23, down from $1.55 in Q1 2024, while adjusted diluted EPS was $1.45, compared to $1.56 in the same period last year.

The company’s gross profit margin showed a slight improvement at 33.2%, up from 33.1% in Q1 2024. However, reported operating profit decreased to $107.0 million from $122.8 million in the prior year, though adjusted operating profit increased marginally to $125.0 million from $123.0 million.

Segment Performance Analysis

West Pharmaceutical’s business segments showed mixed performance in the first quarter. The company’s organic net sales growth of 2.1% was driven by varying results across its four main segments.

The Biologics segment achieved mid-single digit growth, primarily driven by self-injection device platform sales, though partially offset by lower FluroTec® sales. The Pharma segment also posted mid-single digit growth, fueled by standard and Westar® product sales.

In contrast, the Generics segment experienced a mid-single digit decline, attributed to lower standard and FluroTec® sales. The Contract Manufacturing segment delivered low-single digit growth, supported by self-injection devices for obesity/diabetes applications, but partially offset by lower healthcare diagnostic device sales.

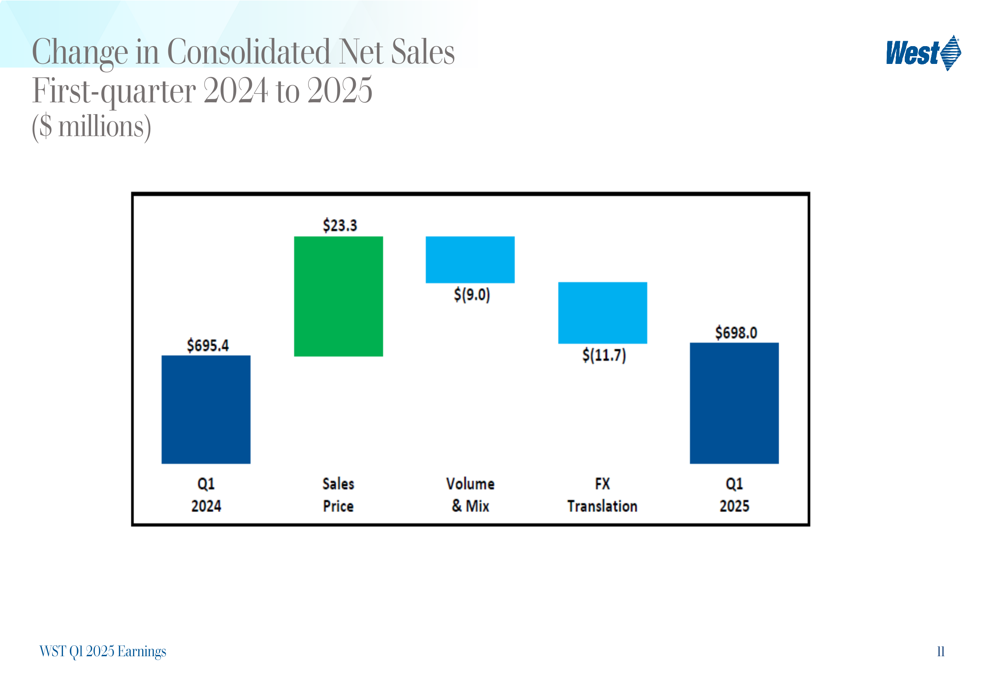

A closer examination of the factors affecting consolidated net sales reveals that positive pricing impact of $23.3 million was largely offset by negative volume and mix effects of $(9.0) million and unfavorable currency translation of $(11.7) million.

High-Value Products and Strategic Focus

West Pharmaceutical continues to emphasize its high-value products (HVP) as a key growth driver. The company noted that HVP components have grown at an impressive 13% CAGR over the past five years, with expectations for mid-single digit growth in 2025.

"We are capitalizing on opportunities in the GLP-1 market and making progress with biologic customers," management stated in the presentation. In Q1, Annex 1 revenues accounted for approximately 200 basis points of total revenues, highlighting the growing importance of this segment.

The company also reported continued volume ramp in its SmartDose® delivery devices during Q1 2025, while working to improve margins through scale and automation. In the contract manufacturing business, GLP-1 auto-injector growth is offsetting contract exits in continuous glucose monitoring (CGM) products.

Cash Flow and Balance Sheet Strength

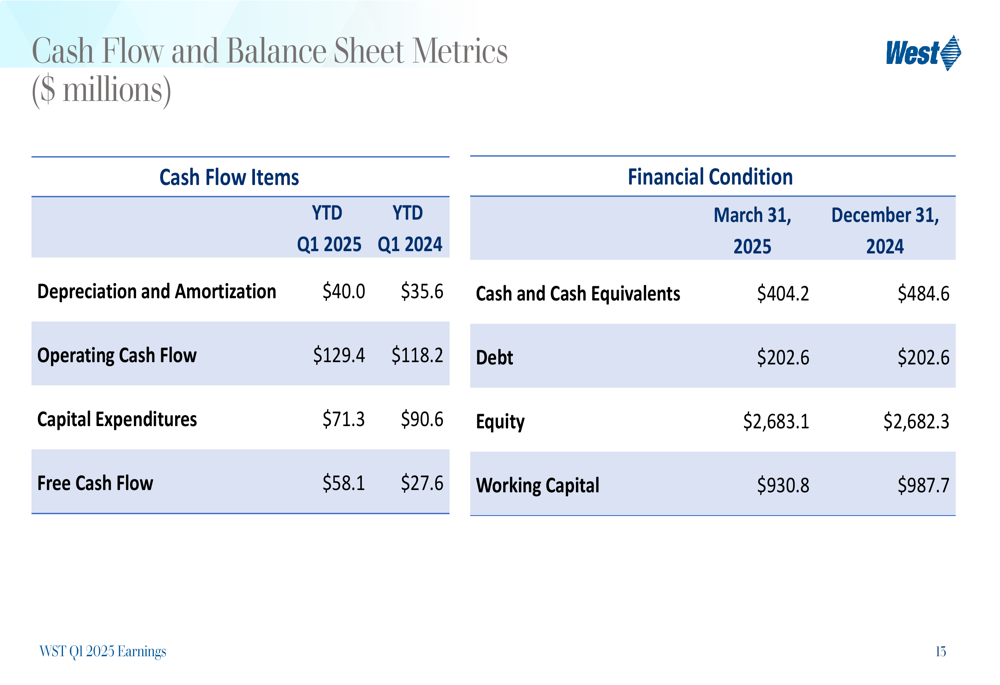

Despite the earnings pressure, West Pharmaceutical demonstrated improved cash flow metrics in Q1 2025. Operating cash flow increased to $129.4 million from $118.2 million in Q1 2024, while capital expenditures decreased to $71.3 million from $90.6 million.

This combination resulted in free cash flow of $58.1 million, more than double the $27.6 million generated in the same period last year. The company’s balance sheet remains solid with $404.2 million in cash and cash equivalents as of March 31, 2025, though down from $484.6 million at the end of 2024. Debt remained stable at $202.6 million, with total equity of $2,683.1 million.

Forward Guidance and Strategic Focus

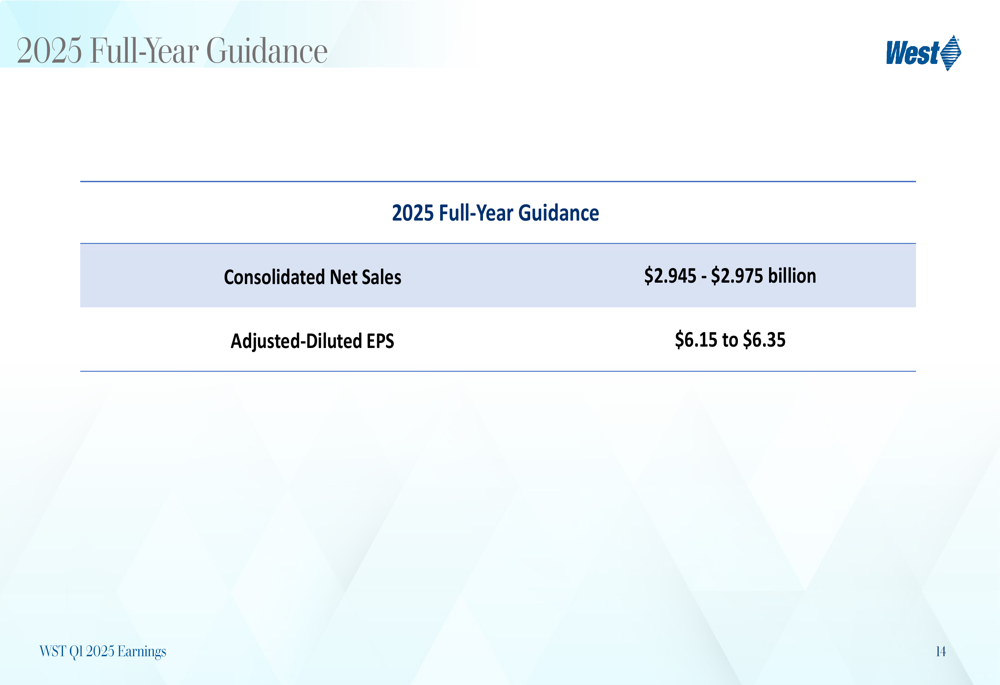

Looking ahead, West Pharmaceutical maintained its full-year 2025 guidance, projecting consolidated net sales between $2.945 billion and $2.975 billion, with adjusted diluted EPS expected to range from $6.15 to $6.35.

This guidance is slightly higher than what was previously indicated in the company’s Q4 2024 earnings release, which had projected EPS of $6.00 to $6.20, suggesting some improvement in the company’s outlook.

West Pharmaceutical continues to focus on strategic growth areas, including expanding its presence in the GLP-1 market, improving manufacturing efficiency, and shifting toward higher-margin drug handling in its contract manufacturing business. The company is also working to capitalize on its high-value products, which have historically delivered stronger growth and better margins than standard components.

As the pharmaceutical packaging and delivery systems market evolves, West Pharmaceutical appears positioned to navigate current challenges while building on its established market presence. However, investors will likely continue to monitor the company’s ability to translate modest sales growth into improved profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.