Trump announces trade deal with EU following months of negotiations

Introduction & Market Context

Western Digital Corporation (NASDAQ:WDC) released its fiscal third quarter 2025 financial results on April 30, 2025, showcasing strong year-over-year growth despite sequential declines across its business segments. The company’s stock, which closed at $40.62 on April 29, saw a significant premarket jump of 11.23% to $45.18 following the earnings announcement, indicating positive investor sentiment toward the results and strategic developments.

The quarter marked a significant milestone for Western Digital with the completion of its Flash business separation, allowing the company to focus on its core hard disk drive (HDD) business while also introducing a new dividend program.

Executive Summary

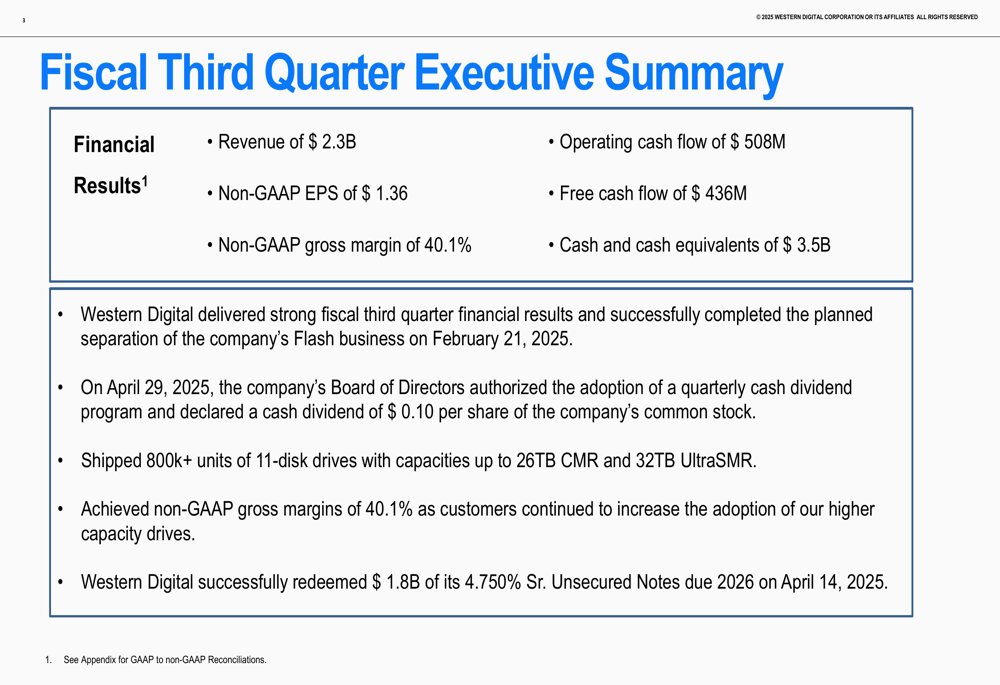

Western Digital reported revenue of $2.3 billion for the third quarter of fiscal 2025, representing a 31% increase year-over-year despite a 5% sequential decline. The company delivered non-GAAP earnings per share of $1.36, up 15% from the previous quarter, while achieving a non-GAAP gross margin of 40.1%, an improvement of 1.7 percentage points sequentially and 10 percentage points year-over-year.

As shown in the following executive summary slide, the company generated strong cash flows with operating cash flow of $508 million and free cash flow of $436 million, while maintaining a solid cash position of $3.5 billion:

Other notable achievements during the quarter included the shipment of over 800,000 units of 11-disk drives and the redemption of $1.8 billion of unsecured notes due in 2026, reflecting the company’s focus on operational excellence and balance sheet management.

Quarterly Performance Highlights

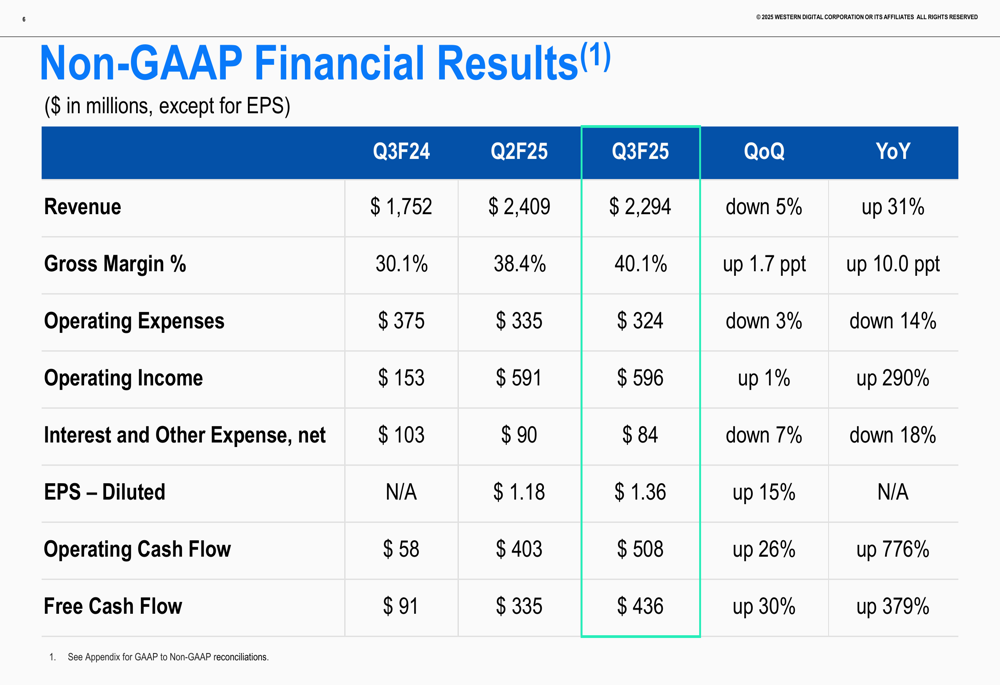

Western Digital’s financial performance showed significant improvement on a year-over-year basis across key metrics, despite modest sequential declines in some areas. The company’s non-GAAP operating income reached $596 million, up 290% year-over-year and 1% sequentially, while operating expenses decreased by 14% year-over-year and 3% quarter-over-quarter to $324 million.

The following table provides a comprehensive view of Western Digital’s non-GAAP financial results, highlighting the substantial year-over-year improvements:

The company’s gross margin expansion to 40.1% demonstrates Western Digital’s ability to maintain pricing discipline and operational efficiency despite market challenges. This margin improvement, combined with reduced operating expenses, contributed significantly to the 15% sequential increase in earnings per share.

Segment Performance

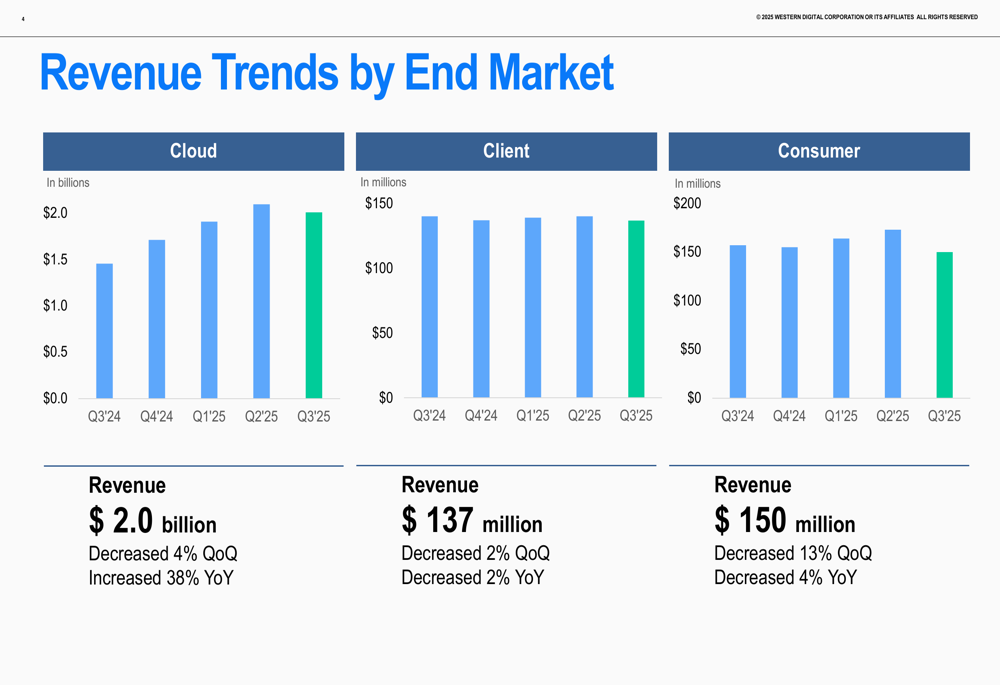

Western Digital’s revenue performance varied across its three main end markets: Cloud, Client, and Consumer. The Cloud segment remained the dominant revenue driver, accounting for approximately 87% of total revenue in Q3 FY25.

As illustrated in the following revenue trends chart, the Cloud segment generated $2.0 billion in revenue, representing a 38% increase year-over-year despite a 4% sequential decline:

The Client segment, which contributed $137 million in revenue, experienced modest declines of 2% both sequentially and year-over-year. Meanwhile, the Consumer segment saw the largest sequential drop at 13%, with revenue falling to $150 million, down 4% year-over-year.

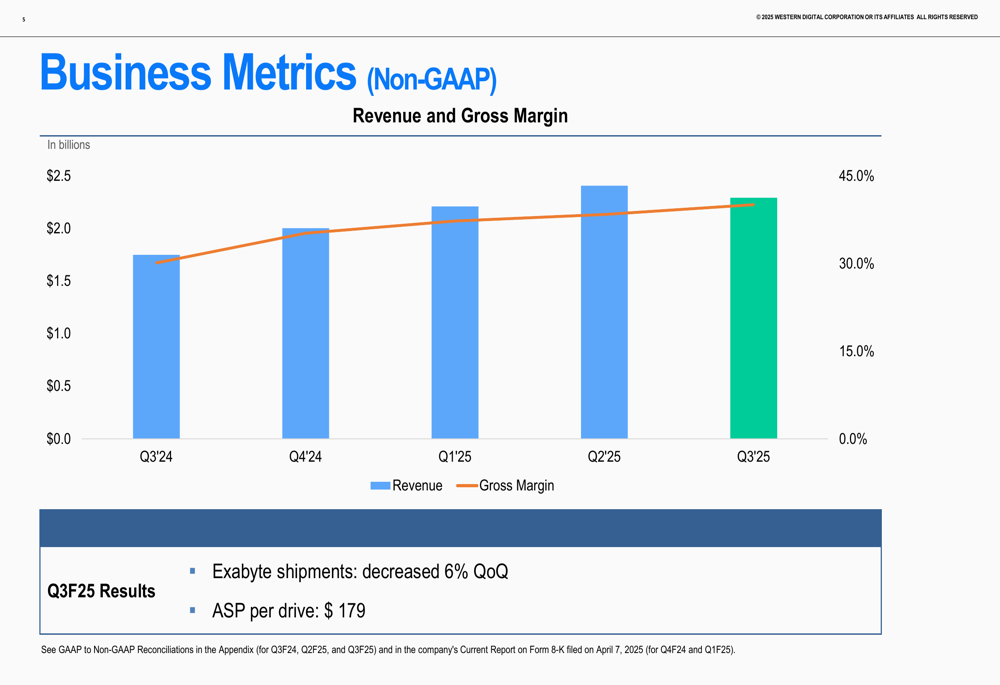

The company’s business metrics reveal that exabyte shipments decreased by 6% quarter-over-quarter, while the average selling price per drive was $179:

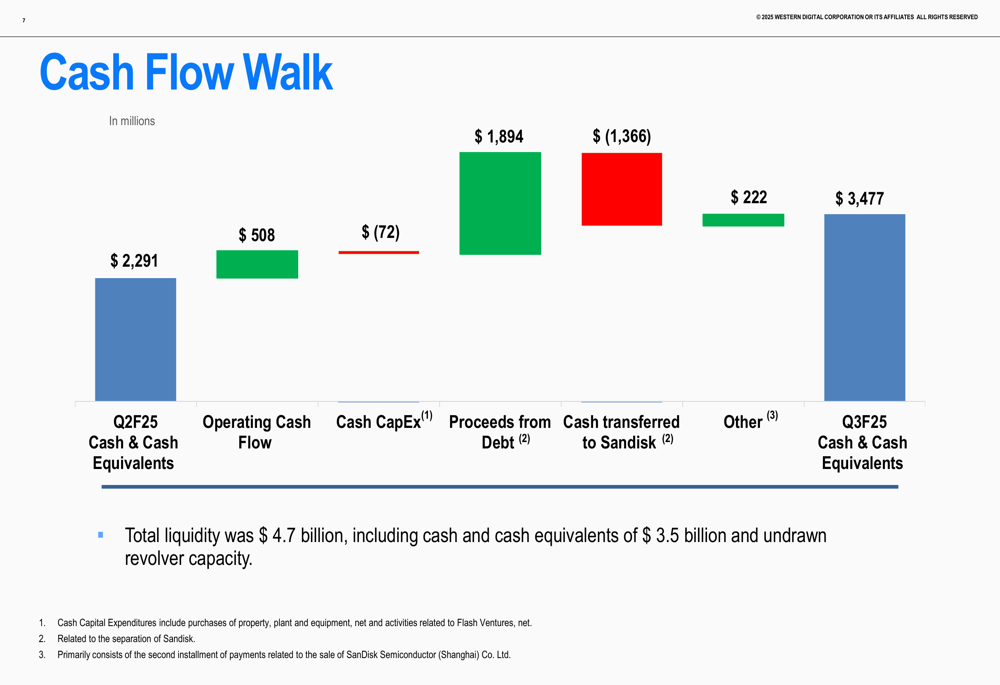

Cash Flow and Capital Structure

Western Digital significantly strengthened its financial position during the quarter, with cash and cash equivalents increasing to $3.5 billion. The company’s cash flow walk illustrates the various components contributing to this improvement:

Operating cash flow of $508 million represented a substantial increase of 776% year-over-year and 26% sequentially. Free cash flow also showed impressive growth, rising 379% year-over-year and 30% sequentially to $436 million. These improvements reflect Western Digital’s enhanced operational efficiency and disciplined capital management.

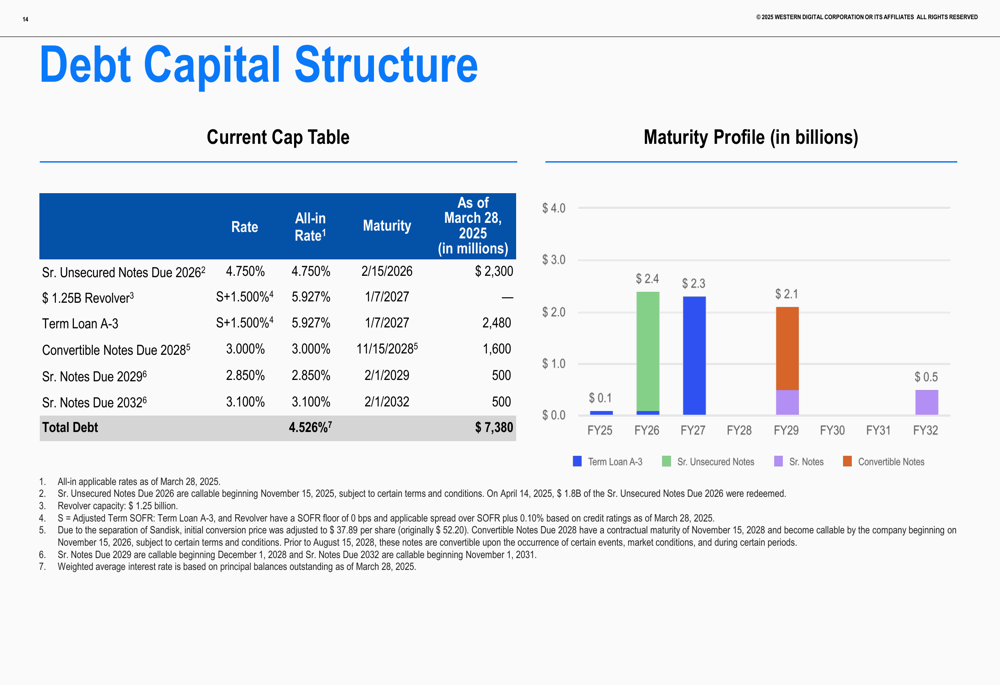

The company’s debt capital structure has also evolved, with a clear maturity profile extending through fiscal year 2032:

Total (EPA:TTEF) liquidity reached $4.7 billion, including cash and cash equivalents of $3.5 billion and undrawn revolver capacity. This strong liquidity position provides Western Digital with financial flexibility to pursue strategic initiatives while returning value to shareholders.

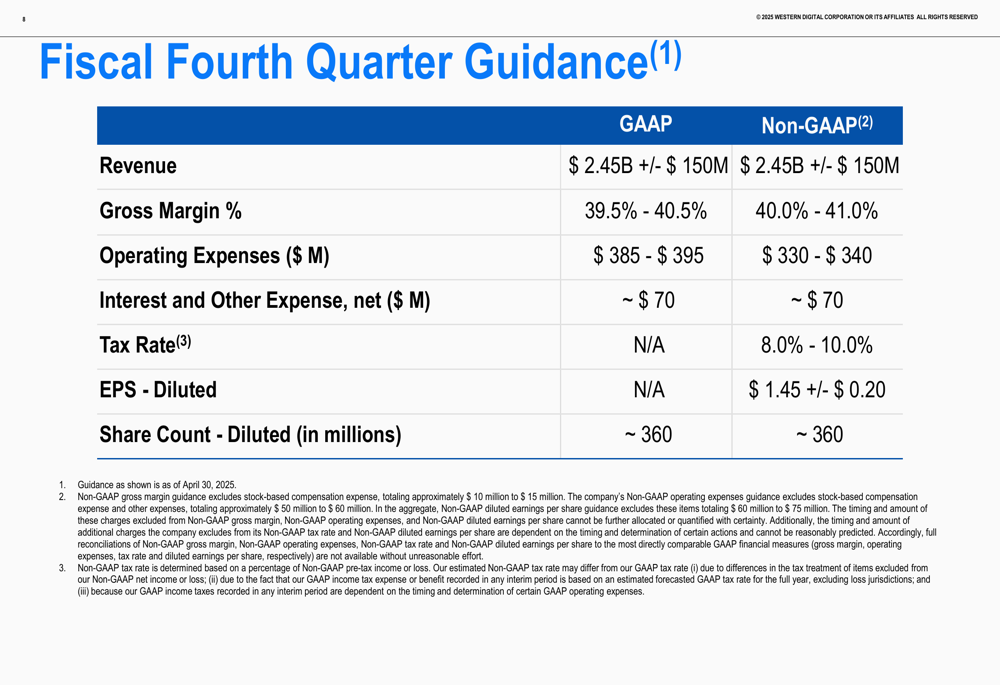

Forward Guidance

Looking ahead to the fiscal fourth quarter of 2025, Western Digital provided a positive outlook, projecting revenue of $2.45 billion (plus or minus $150 million) and non-GAAP earnings per share of $1.45 (plus or minus $0.20).

The company expects to maintain its strong gross margin performance, with non-GAAP gross margin projected to be between 40.0% and 41.0%, as shown in the following guidance slide:

Operating expenses are expected to remain well-controlled, with non-GAAP operating expenses projected between $330 million and $340 million. The company anticipates interest and other expenses of approximately $70 million and a non-GAAP tax rate between 8.0% and 10.0%.

Strategic Initiatives

The completion of the Flash business separation represents a pivotal strategic milestone for Western Digital. This separation, which resulted in the transfer of $1.366 billion in cash to Sandisk, allows the company to focus on its core HDD business while optimizing its capital structure.

In a significant move for shareholders, Western Digital’s Board of Directors authorized a cash dividend program of $0.10 per share, signaling confidence in the company’s financial stability and future cash generation capabilities.

The company also made progress in strengthening its balance sheet by redeeming $1.8 billion of unsecured notes due in 2026, reducing its overall debt burden and improving its financial flexibility.

Western Digital’s continued innovation in high-capacity drives, evidenced by the shipment of over 800,000 units of 11-disk drives during the quarter, underscores its commitment to maintaining technological leadership in the storage industry, particularly for cloud and data center applications where demand for high-capacity storage continues to grow.

The combination of strong financial performance, strategic focus following the Flash business separation, and shareholder-friendly capital allocation policies positions Western Digital well for sustainable growth in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.