Asia FX weakens slightly, rupee recovers from record low as RBI holds rates

Western Digital Corporation (NASDAQ:WDC) presented its fourth quarter and full-year fiscal 2025 financial results on July 30, 2025, showcasing strong performance with significant year-over-year improvements in revenue, margins, and profitability. The storage solutions provider also announced its first dividend and a new share repurchase program.

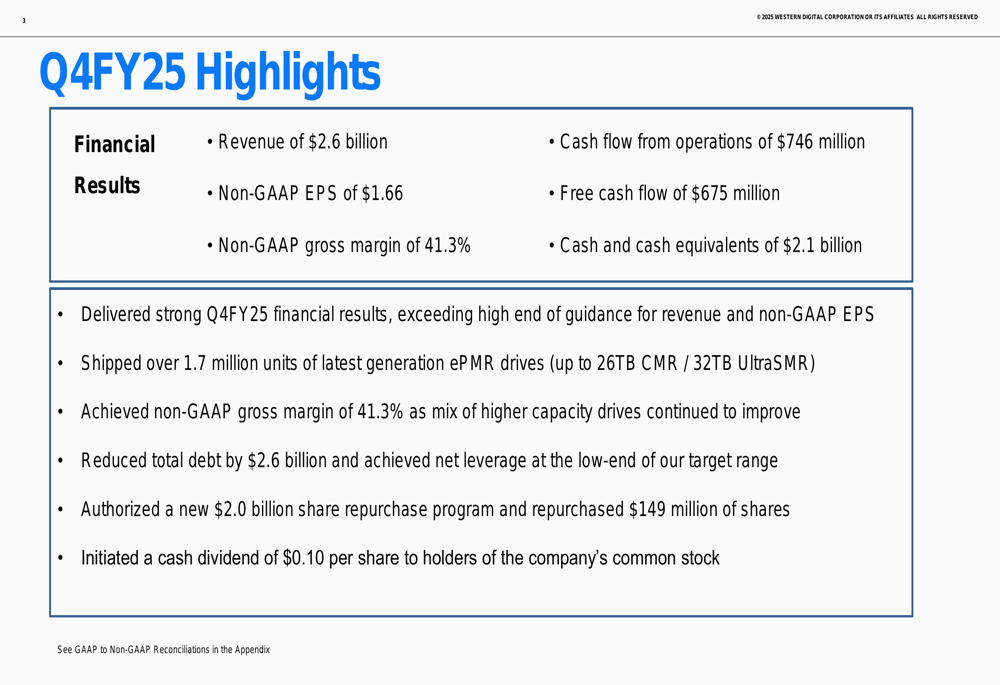

Quarterly Performance Highlights

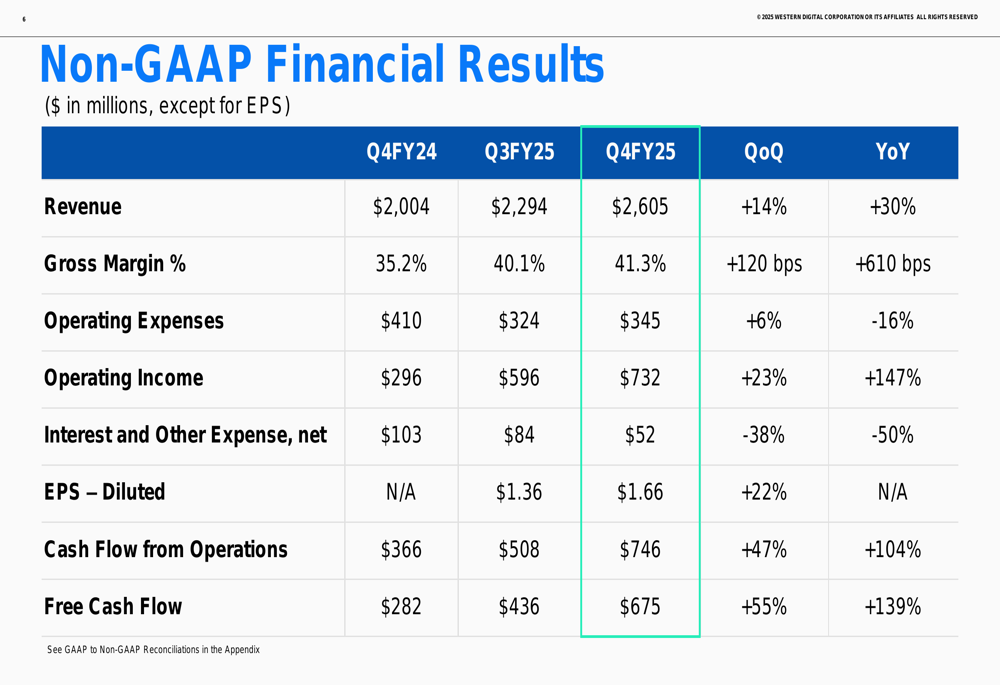

Western Digital reported Q4 revenue of $2.6 billion, exceeding the high end of its guidance and representing a 30% increase compared to the same period last year. Non-GAAP earnings per share reached $1.66, up 22% sequentially from $1.36 in Q3, demonstrating accelerating profitability.

The company’s gross margin expanded significantly to 41.3%, an improvement of 610 basis points year-over-year, driven by a more favorable product mix with higher-capacity drives. Operating income surged 147% compared to Q4FY24, reaching $732 million.

As shown in the following financial results summary:

Cash generation remained robust with $746 million in operating cash flow (up 104% year-over-year) and $675 million in free cash flow (up 139% year-over-year). This strong cash performance supported the company’s debt reduction efforts and new shareholder return initiatives.

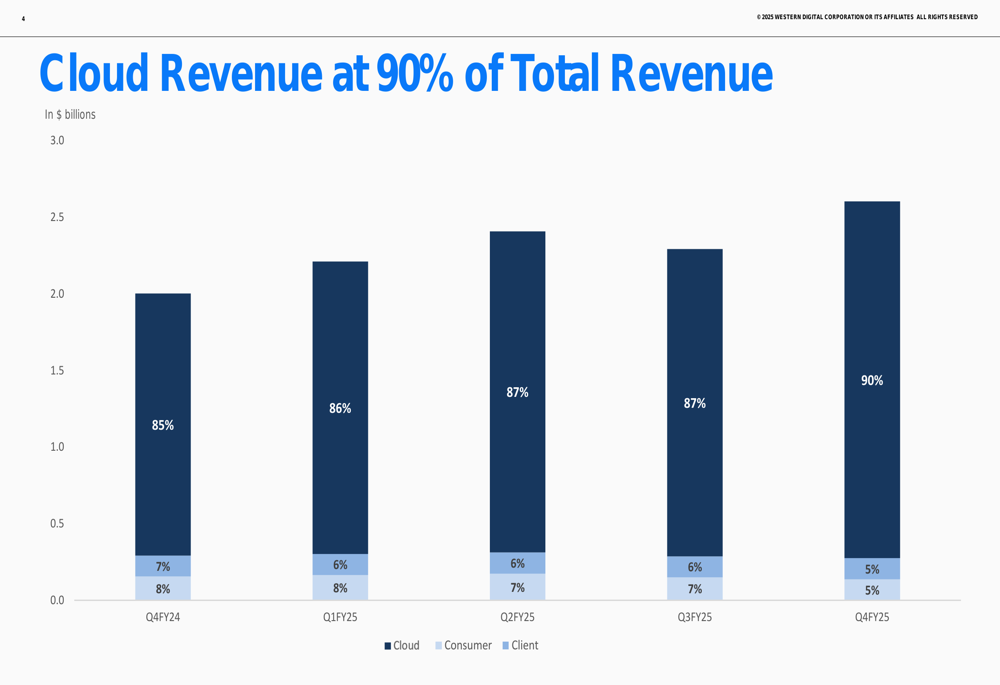

Cloud Dominance and Product Mix

Western Digital’s strategic focus on cloud storage solutions has paid off dramatically, with cloud revenue now accounting for 90% of total revenue in Q4FY25, up from 85% in the same quarter last year. This shift represents a significant transformation of the company’s business model toward higher-growth segments.

The following chart illustrates this steady progression toward cloud dominance:

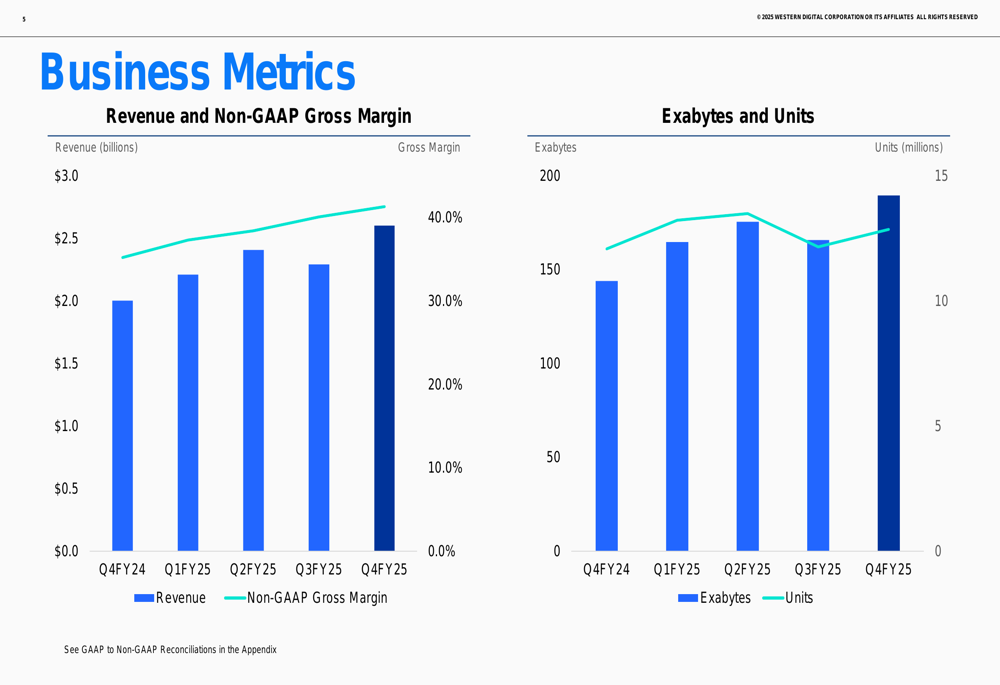

The company reported shipping over 1.7 million units of its latest generation ePMR drives, which offer capacities up to 26TB CMR and 32TB UltraSMR. Total (EPA:TTEF) exabytes shipped increased to 190 in Q4, up from 144 in the year-ago quarter, while unit shipments remained relatively stable at approximately 12 million.

The business metrics chart below shows the company’s improving revenue, margins, and capacity shipments:

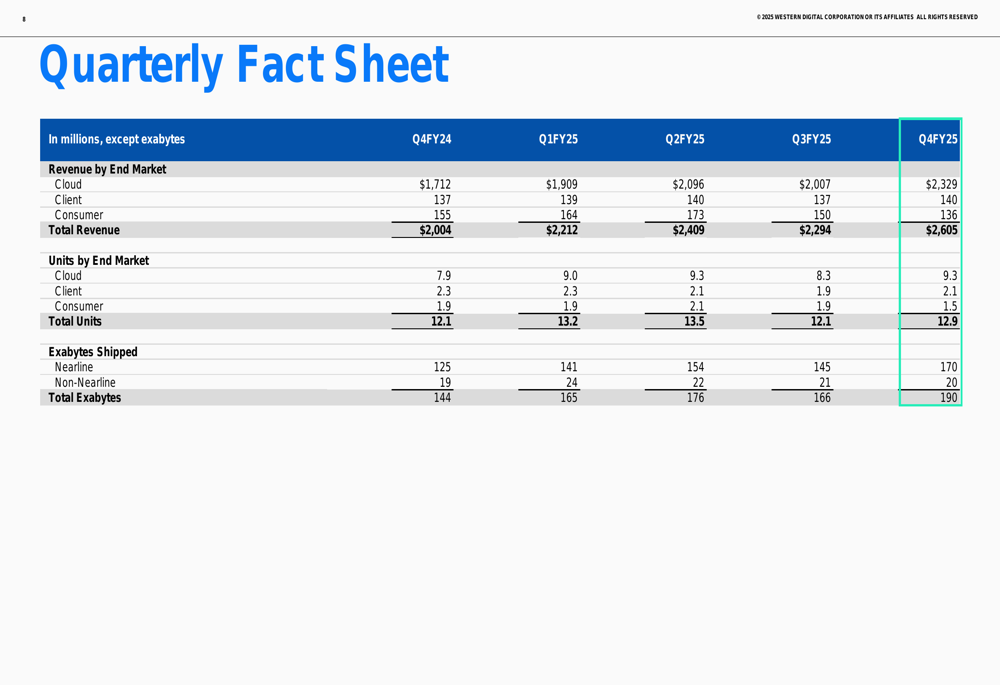

The quarterly fact sheet provides additional detail on the company’s performance across different market segments:

Capital Allocation and Shareholder Returns

In a significant development for investors, Western Digital announced the initiation of a quarterly cash dividend of $0.10 per share, marking the company’s first regular dividend. Additionally, the board authorized a new $2.0 billion share repurchase program, under which the company has already repurchased $149 million worth of shares.

These shareholder-friendly moves come alongside substantial debt reduction, with the company paying down $2.6 billion in total debt to achieve net leverage at the low end of its target range. The combined actions signal management’s confidence in sustainable cash generation and a balanced approach to capital allocation.

As highlighted in the company’s quarterly summary:

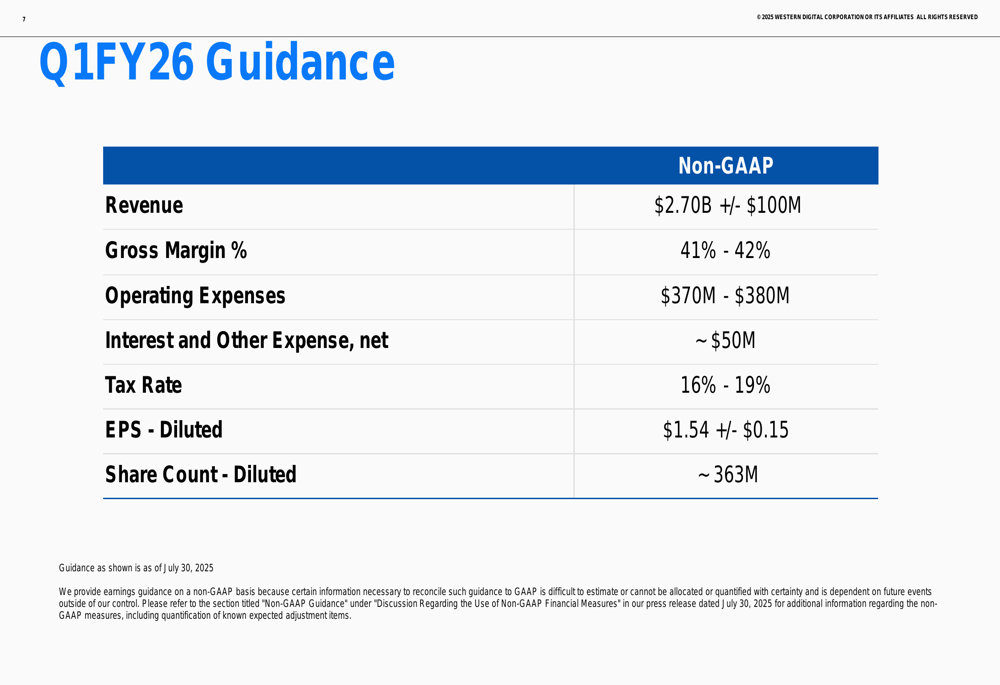

Forward Guidance and Outlook

Looking ahead to the first quarter of fiscal 2026, Western Digital provided an optimistic outlook with revenue expected to reach $2.70 billion (plus or minus $100 million), representing continued sequential growth. The company projects non-GAAP gross margin to remain strong at 41-42%, while non-GAAP EPS is forecasted at $1.54 (plus or minus $0.15).

The guidance suggests Western Digital expects to maintain its momentum despite typical seasonal patterns, likely driven by continued strong demand in cloud storage:

Market Context and Competitive Position

Western Digital’s Q4 results continue the positive momentum seen in Q3, when the company reported EPS of $1.36 and revenue of $2.3 billion. The sequential improvement in both metrics demonstrates the company’s ability to capitalize on growing demand for high-capacity storage solutions, particularly in data center and cloud environments.

The company’s stock reacted to the earnings announcement with a 1.84% decline in after-hours trading, despite the strong results and forward guidance. This may reflect some profit-taking after the stock’s significant rise over the past year, having traded as low as $28.83 before reaching recent highs above $70.

Western Digital’s strategic focus on cloud storage and high-capacity drives positions it well in a market increasingly driven by AI and data center expansion. The company’s improving margins and strong cash generation, coupled with its new shareholder return programs, suggest management is confident in its competitive position and future growth prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.