Stock market today: S&P 500 climbs as health care, tech gain; Nvidia earnings loom

Western Midstream Partners LP (NYSE:WES) released its first-quarter 2025 results on May 7, showcasing record operational performance and continued distribution growth. The midstream energy company reported solid financial metrics while maintaining its focus on strategic expansion and capital discipline.

Quarterly Performance Highlights

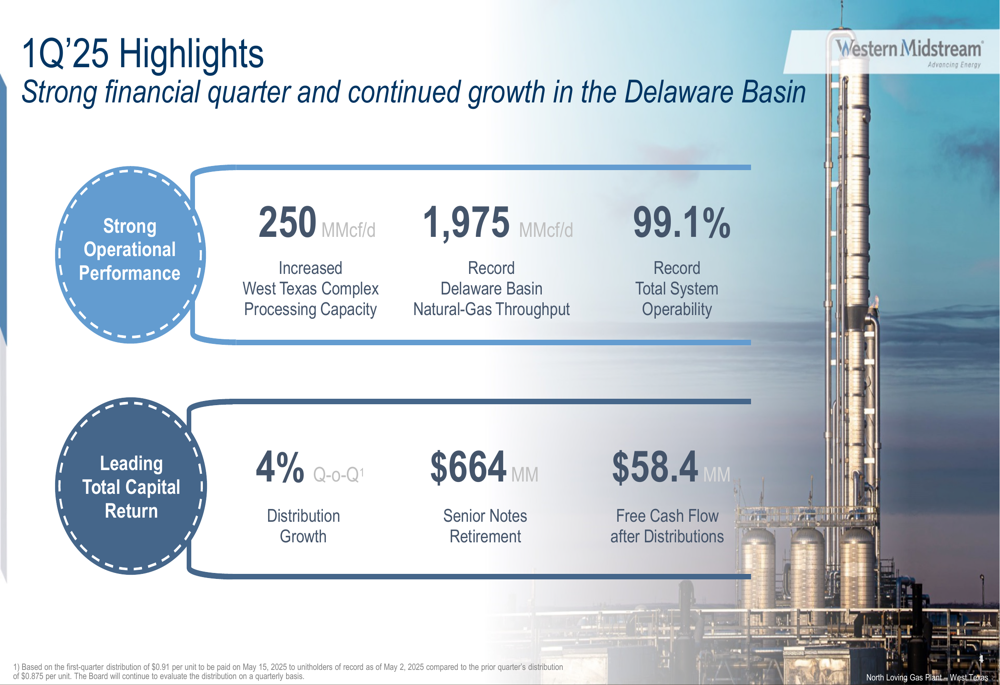

Western Midstream achieved notable operational milestones in the first quarter of 2025, including record Delaware Basin natural gas throughput of 1,975 MMcf/d and record total system operability of 99.1%. The company also increased its West Texas Complex processing capacity by 250 MMcf/d.

As shown in the following highlights from the company’s presentation:

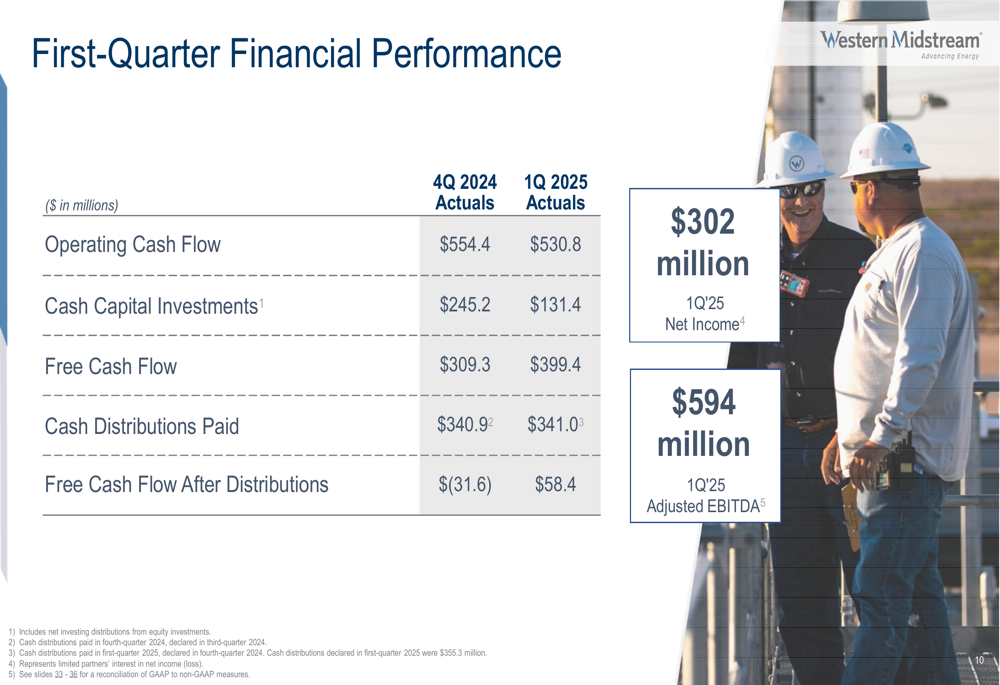

Financial performance for the quarter remained strong, with net income of $302 million and adjusted EBITDA of $594 million. This represents an improvement from the previous quarter’s adjusted EBITDA of $590.7 million. The company generated $530.8 million in operating cash flow and $399.4 million in free cash flow, resulting in $58.4 million of free cash flow after distributions.

The following slide details the company’s first-quarter financial performance compared to the previous quarter:

Financial Analysis and Capital Allocation

Western Midstream continues to prioritize capital discipline while maintaining a robust distribution program. The company increased its distribution by 4% quarter-over-quarter and retired $664 million in senior notes during the period. WES has maintained a leverage ratio below 3.0x, positioning it well for future growth opportunities.

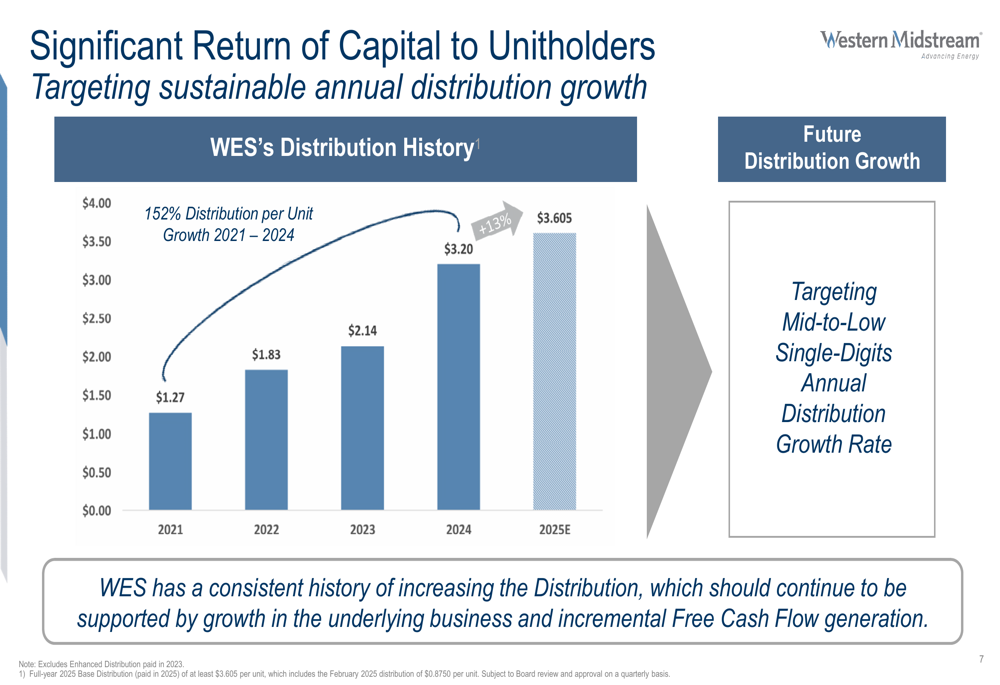

The company’s distribution history shows consistent growth, with a projected distribution of $3.605 per unit for 2025, representing a 13% increase from 2024 and a remarkable 152% growth since 2021.

The following chart illustrates Western Midstream’s distribution growth trajectory:

Western Midstream’s capital allocation strategy focuses on three key priorities: executing expansion opportunities with mid-teens unlevered rates of return, pursuing accretive M&A opportunities, and growing distributions at a mid-to-low single-digit annual rate. For 2025, approximately 65% of capital expenditures are allocated toward expansion projects.

2025 Guidance and Strategic Outlook

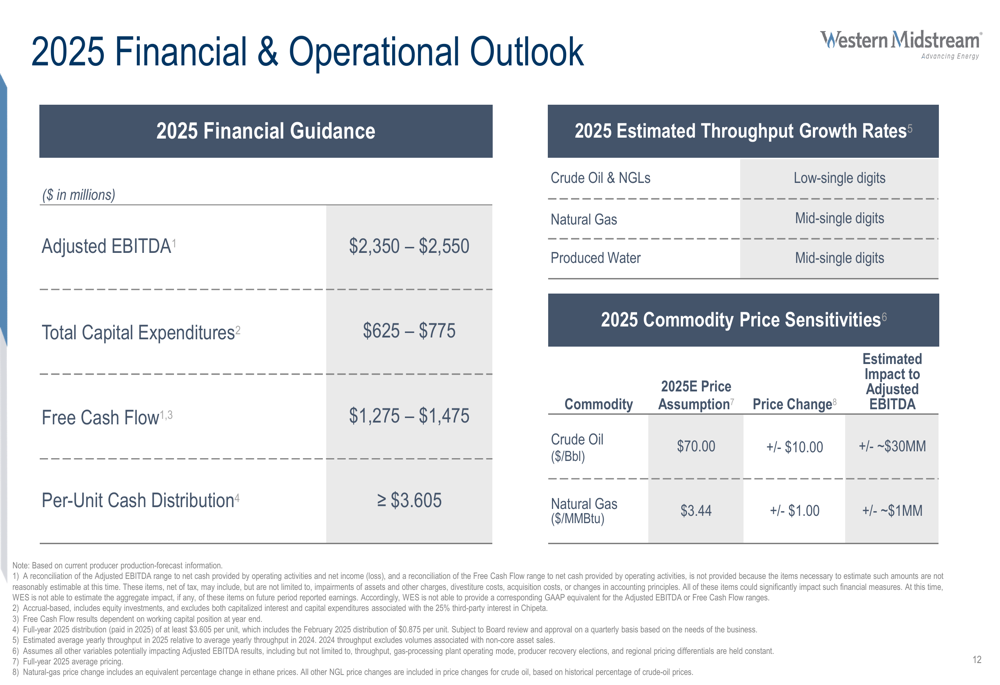

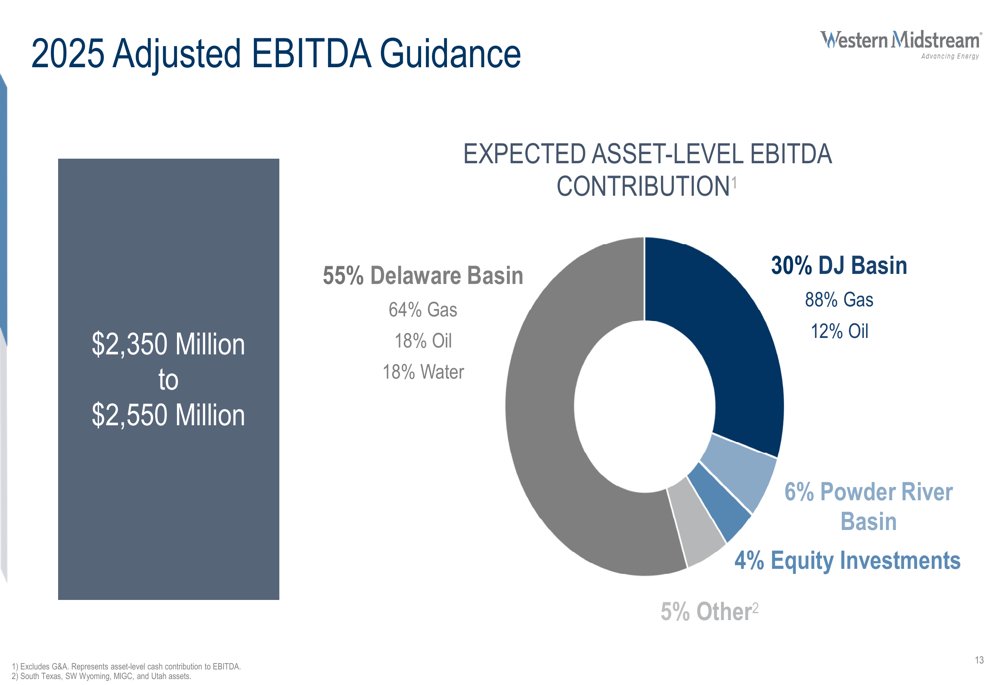

Western Midstream reaffirmed its 2025 financial guidance, projecting adjusted EBITDA between $2,350 million and $2,550 million, total capital expenditures between $625 million and $775 million, and free cash flow between $1,275 million and $1,475 million. The company expects throughput growth in the mid-single digits for natural gas and produced water, with low-single-digit growth for crude oil and NGLs.

The following slide provides a comprehensive overview of Western Midstream’s 2025 financial and operational outlook:

The company’s expected EBITDA contribution by asset shows the Delaware Basin accounting for 55% of the total, followed by the DJ Basin at 30%, with the remainder coming from the Powder River Basin and equity investments.

As illustrated in the following asset-level EBITDA contribution breakdown:

Western Midstream continues to invest in strategic growth projects, including the Pathfinder Pipeline, a 42-mile, 30-inch poly-lined steel transportation pipeline with more than 800 MBbls/d of initial throughput capacity. This project, expected to be in service by January 1, 2027, will enable access to high-quality pore space and represents a significant expansion of the company’s water handling capabilities in the Delaware Basin.

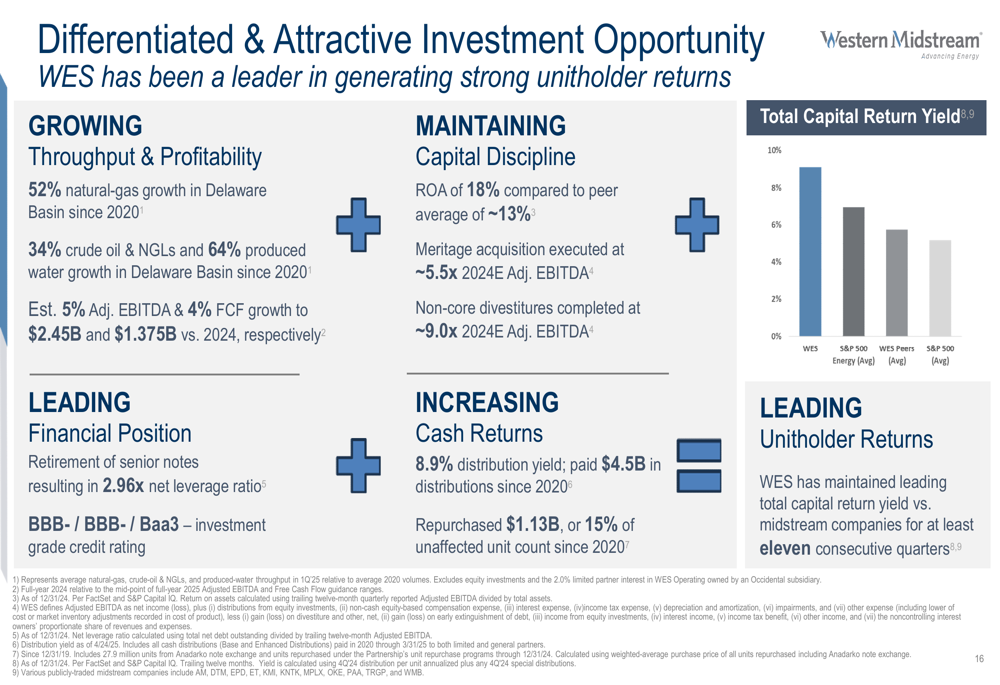

Competitive Positioning and Investment Thesis

Western Midstream positions itself as a differentiated investment opportunity in the midstream sector, highlighting its growing throughput and profitability, capital discipline, and increasing cash returns. The company notes that it has maintained a leading total capital return yield compared to midstream peers for at least eleven consecutive quarters.

The following slide summarizes Western Midstream’s investment opportunity:

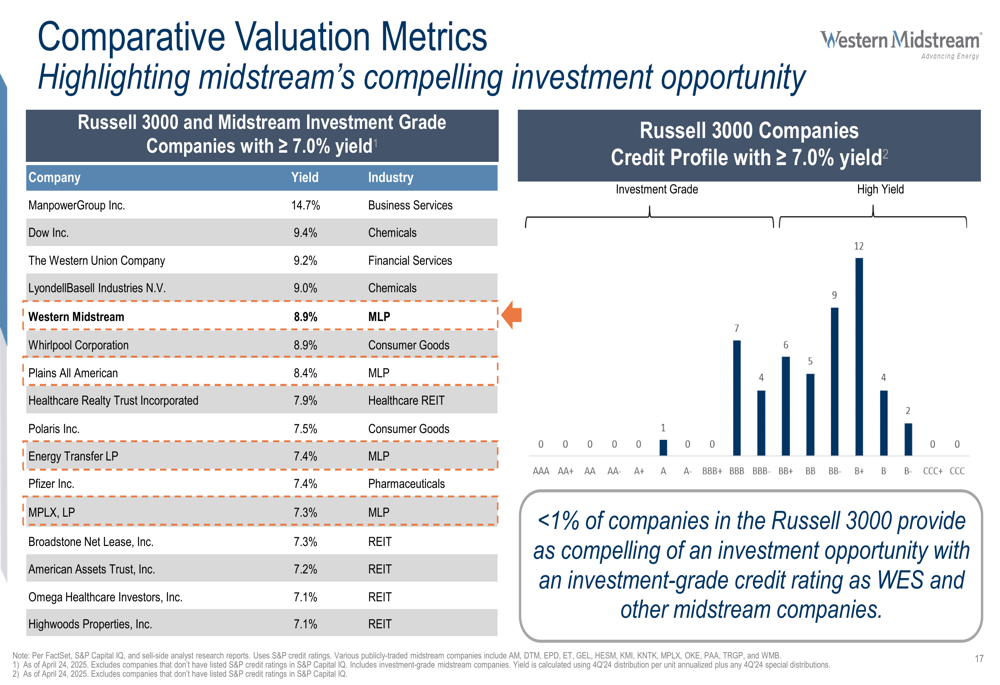

With an 8.9% distribution yield, Western Midstream offers one of the highest yields among Russell 3000 companies with investment-grade credit ratings. The company emphasizes that less than 1% of companies in the Russell 3000 provide a similar combination of high yield and investment-grade credit profile.

As shown in the comparative valuation metrics:

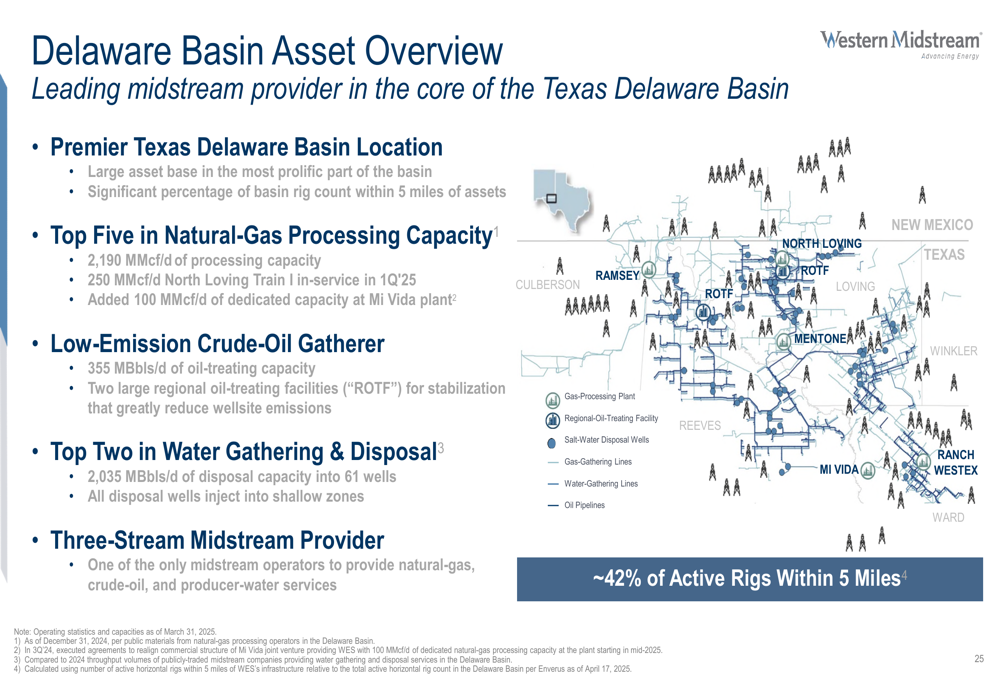

Western Midstream’s Delaware Basin assets represent a core component of its growth strategy. The company has established itself as a top-five player in natural gas processing capacity (2,190 MMcf/d) and a top-two provider in water gathering and disposal (2,035 MBbls/d of disposal capacity) in the basin. As one of the only midstream operators providing three-stream services (natural gas, crude oil, and produced water), WES is well-positioned to capture growth in the region, with approximately 42% of active rigs operating within five miles of its assets.

The following slide provides an overview of Western Midstream’s Delaware Basin assets:

Western Midstream Partners closed at $35.95 on May 7, 2025, up 0.84% for the day. The stock has traded between $33.60 and $43.33 over the past 52 weeks. In aftermarket trading, shares were down slightly by 0.28% to $35.85.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.