Berkshire Hathaway reveals $4.3 billion stake in Alphabet, cuts Apple

Introduction & Market Context

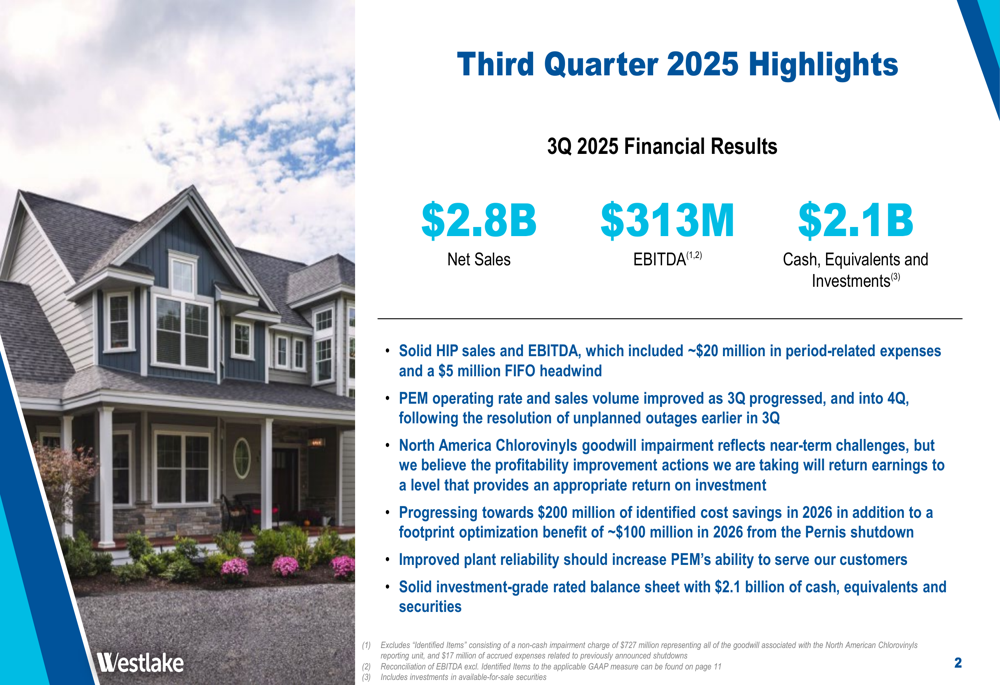

Westlake Chemical Corporation (NYSE:WLK) presented its third-quarter 2025 earnings on October 30, revealing the impact of challenging macroeconomic conditions on its financial performance. The chemical manufacturer reported net sales of $2.8 billion and EBITDA of $313 million, while facing a significant non-cash impairment charge related to its North American chlorovinyls business. The company’s stock remained stable at $66.21 following the announcement.

Amid sluggish global economic conditions and softening demand in North American residential construction, Westlake emphasized its focus on cost reduction initiatives and operational improvements to navigate the challenging environment.

Quarterly Performance Highlights

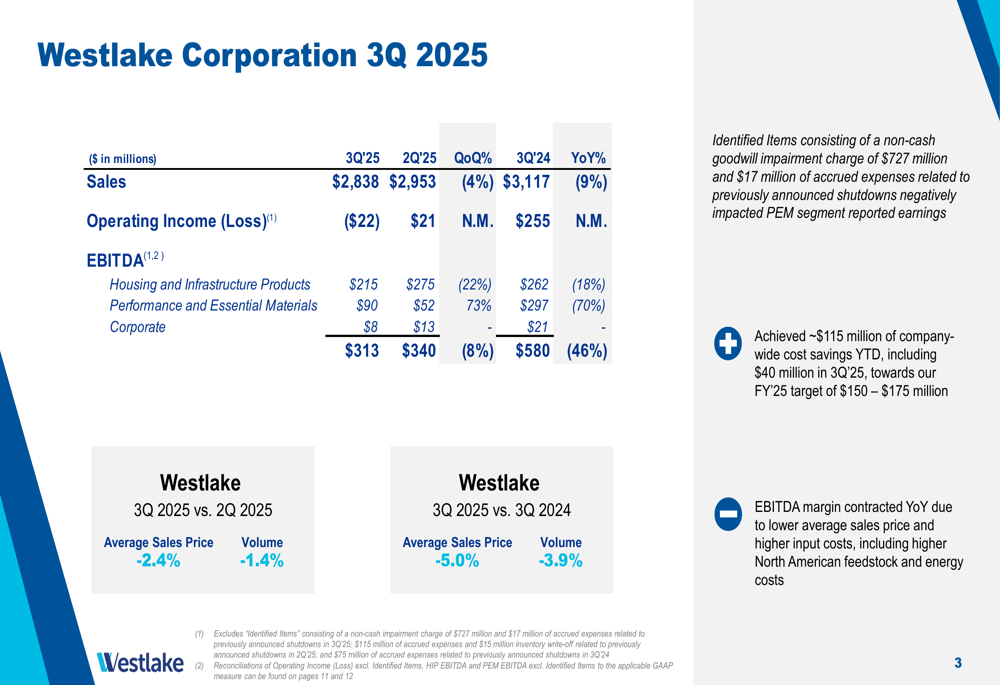

Westlake’s third quarter results showed a year-over-year decline across key metrics, with net sales of $2.8 billion representing a 9% decrease compared to Q3 2024. The company reported an EBITDA of $313 million, down 46% from the same period last year, while maintaining a strong liquidity position with $2.1 billion in cash, equivalents, and investments.

The quarter was significantly impacted by a $727 million non-cash impairment charge related to the company’s North American chlorovinyls business, resulting in an operating loss of $22 million. Excluding this identified item, the company’s performance reflected ongoing market challenges and operational adjustments.

As illustrated in the following financial performance overview, both sales and EBITDA showed sequential quarterly declines:

Segment Analysis

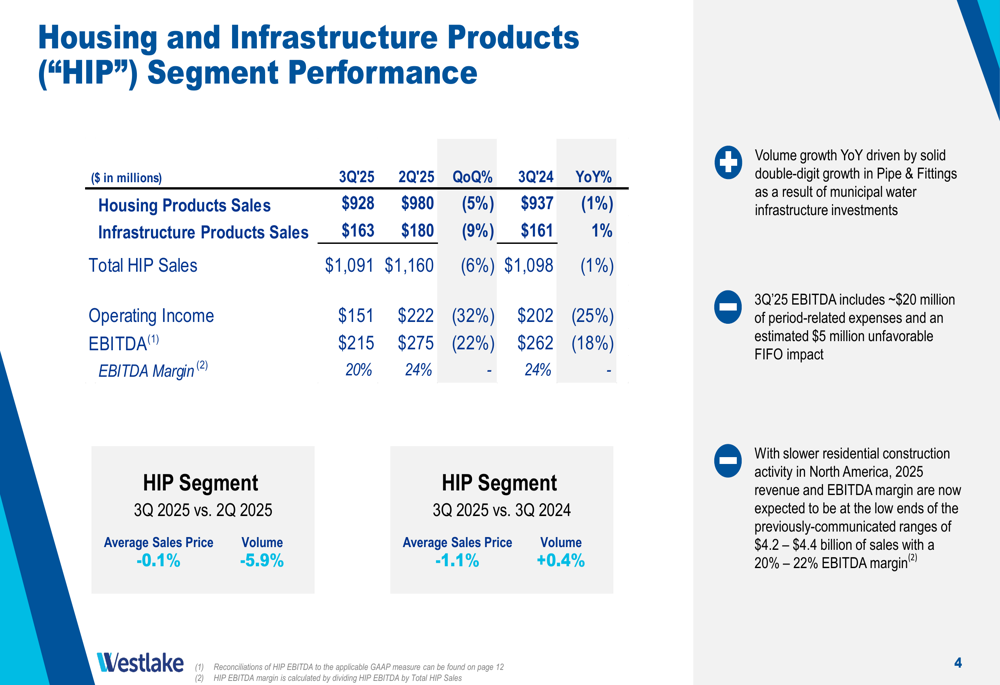

Housing and Infrastructure Products (HIP)

Westlake’s HIP segment demonstrated resilience despite market headwinds, with sales of $1.091 billion representing only a 1% year-over-year decline. While EBITDA for the segment fell 18% compared to Q3 2024 to $215 million, the company noted that HIP’s sales growth outpaced the broader market, which has seen U.S. single-family housing starts and residential construction spending trending below prior year levels.

The detailed segment performance shows the relative stability of the HIP business compared to the more volatile PEM segment:

Strong demand for municipal pipe drove sales volume growth in the infrastructure products division, partially offsetting weakness in housing-related products. Westlake emphasized that longer-term housing fundamentals remain strong despite current market challenges.

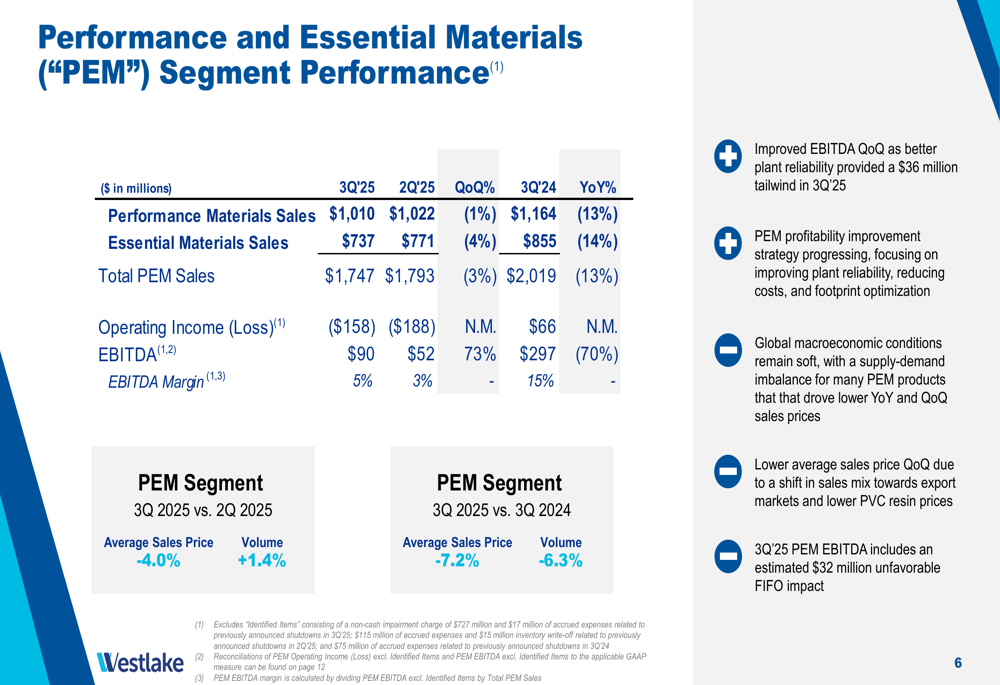

Performance and Essential Materials (PEM)

The PEM segment faced more significant challenges, with sales declining 13% year-over-year to $1.747 billion and EBITDA falling 70% compared to Q3 2024 to $90 million. However, the segment showed sequential improvement with EBITDA increasing 73% compared to Q2 2025, suggesting that recovery initiatives are beginning to yield results.

The following chart illustrates the PEM segment’s performance metrics:

Westlake attributed the PEM segment’s challenges to global macroeconomic conditions and an elevated level of planned turnarounds and unplanned plant outages that affected earnings. The company expects PEM segment profitability to improve following the planned closure of its Pernis site.

Strategic Initiatives

Westlake outlined several strategic initiatives aimed at improving profitability and operational efficiency. The company is targeting $200 million in structural cost reductions for 2026, with approximately $100 million expected to come from the closure of the Pernis site alone. Management reported progress toward these targets and highlighted improved plant reliability as a key achievement during the quarter.

These cost-cutting measures align with Westlake’s broader strategy to enhance profitability in a challenging market environment. The company also mentioned the acquisition of ACI’s global compound solutions business, expanding its product portfolio to include silicone and crosslink polyethylene compounds.

Forward-Looking Statements

Looking ahead, Westlake projects HIP revenue of $4.2 to $4.4 billion for 2025, with an EBITDA margin of 20-22%. The company plans to invest approximately $900 million in capital expenditures this year and anticipates 5-7% long-term organic sales growth in its HIP segment.

Management expressed optimism about the company’s future despite current challenges. Jean-Marc Gilson, President and CEO, stated, "We remain very positive on HIP’s long-term growth outlook," while emphasizing the company’s proactive approach to improving financial performance.

Key risks and challenges facing Westlake include softening demand in North American residential construction, global supply-demand imbalances in the chlorovinyl chain, market saturation in polyethylene and caustic soda sectors, and macroeconomic pressures affecting housing affordability.

Westlake’s strategic focus on cost reduction, operational improvements, and targeted acquisitions reflects its efforts to position the company for future growth despite the current challenging quarter impacted by significant impairment charges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.