Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

Westpac Banking Corporation (ASX:WBC) has released its investor presentation for the third quarter of fiscal year 2025, covering the three months ended June 30. The Australian banking giant reported solid financial performance with profit growth and improved credit quality metrics, maintaining a strong capital position despite ongoing economic uncertainties.

The presentation comes at a time when Australian banks face challenges from interest rate pressures and concerns about household financial stress, making Westpac’s resilient credit quality metrics particularly noteworthy.

Quarterly Performance Highlights

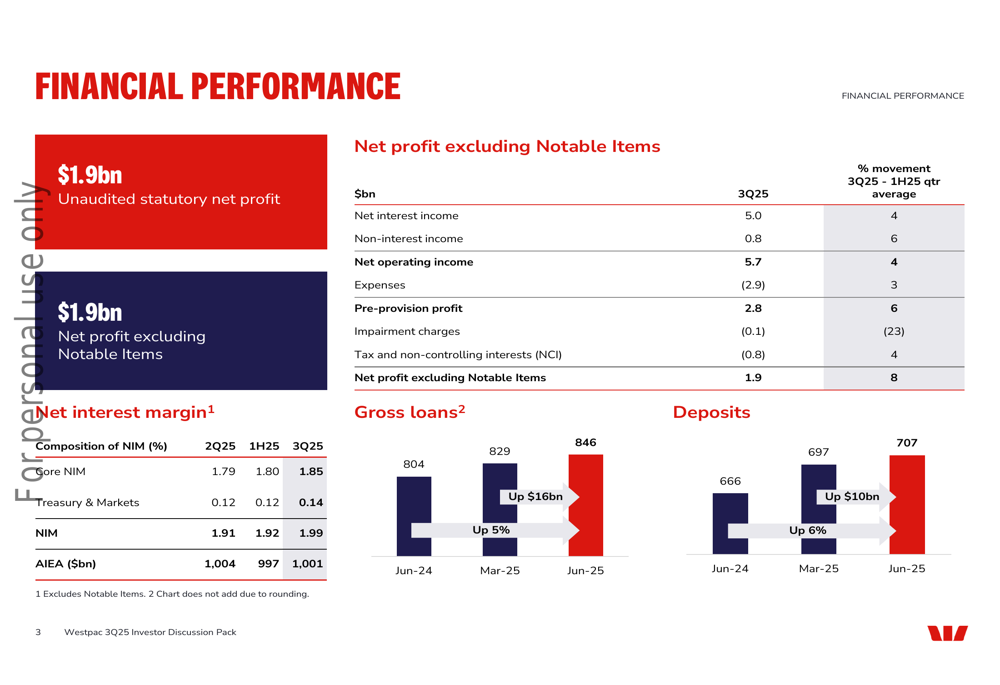

Westpac delivered sound financial results in Q3 2025, with statutory net profit reaching $1.9 billion, representing a 14% increase compared to the first half quarterly average. Net profit excluding notable items also showed healthy growth at $1.9 billion, up 8%.

Revenue increased by 4%, outpacing expense growth of 3%, resulting in positive jaws and improved operational efficiency. The bank’s net interest margin (NIM) stood at 1.99%, with core NIM improving by 5 basis points to 1.85%.

As shown in the following summary of key financial metrics:

The detailed breakdown of financial performance reveals that net interest income reached $5.0 billion, while non-interest income contributed $0.8 billion, resulting in total net operating income of $5.7 billion. Pre-provision profit was $2.8 billion, up 6% from the first half quarterly average.

Detailed Financial Analysis

Westpac’s balance sheet continued to strengthen, with gross loans increasing from $804 billion in June 2024 to $846 billion in June 2025. Similarly, deposits grew from $666 billion to $707 billion over the same period, maintaining a healthy deposit-to-loan ratio of 84.0%.

Impairment charges decreased by 1 basis point to 5 basis points, reflecting the bank’s prudent risk management and the relative resilience of its loan portfolio. This contributed to the strong bottom-line performance despite the challenging economic environment.

The bank’s average interest-earning assets (AIEA) reached $1,001 billion, providing a solid base for revenue generation. The growth in both loans and deposits indicates continued business momentum and customer trust in the Westpac brand.

Credit Quality and Risk Management

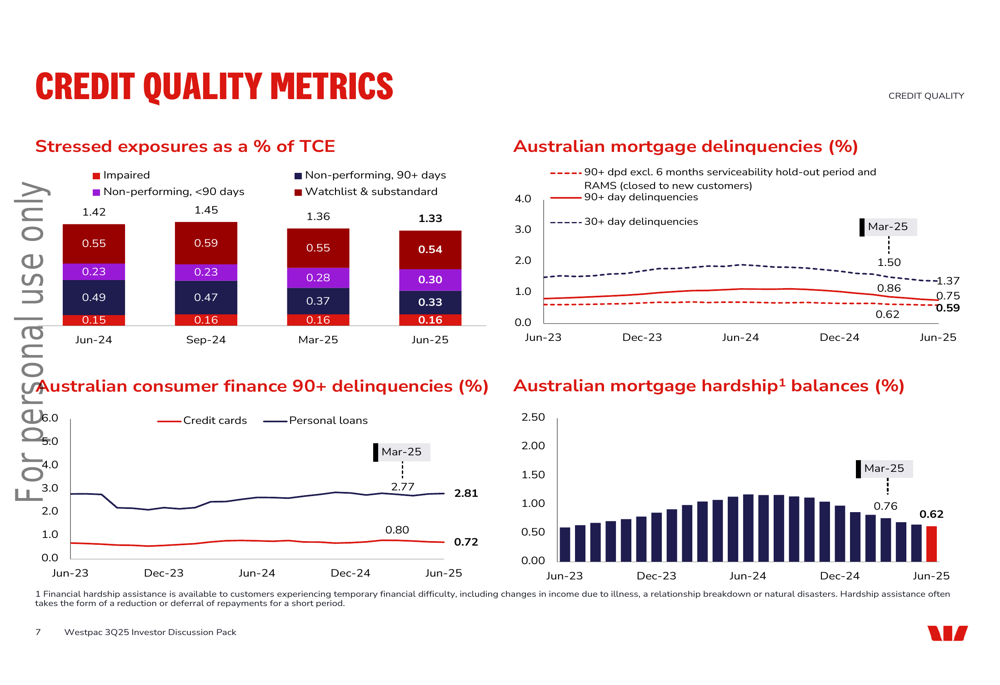

Westpac’s credit quality metrics showed improvement across multiple dimensions. Stressed assets to total committed exposures (TCE) decreased by 3 basis points to 1.33%, while Australian mortgage 90+ day delinquencies fell by 3 basis points to 0.59%.

The following chart illustrates the positive trends in credit quality metrics:

Total provisions for expected credit losses remained stable at $5.1 billion, with the bank increasing its weighting to downside economic scenarios by 2.5 percentage points to 47.5%, demonstrating a prudent approach to potential economic challenges ahead.

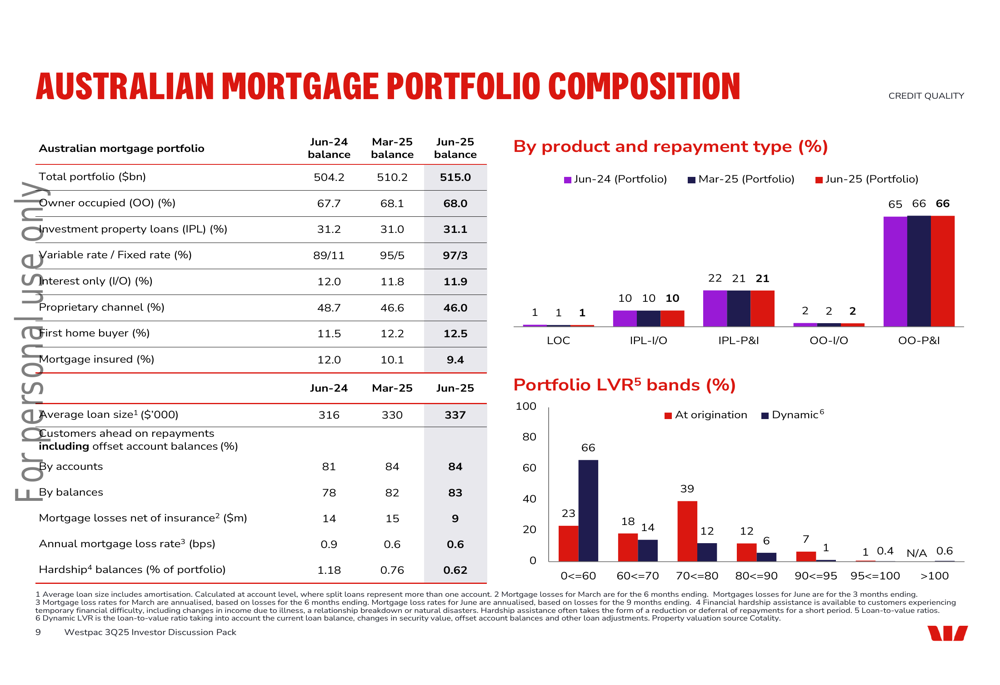

The Australian mortgage portfolio, which represents a significant portion of Westpac’s loan book at $515.0 billion, showed strong fundamentals with 68.0% in owner-occupied loans and only 11.9% in interest-only products. The portfolio’s loan-to-value ratio (LVR) distribution indicates limited exposure to high-risk lending.

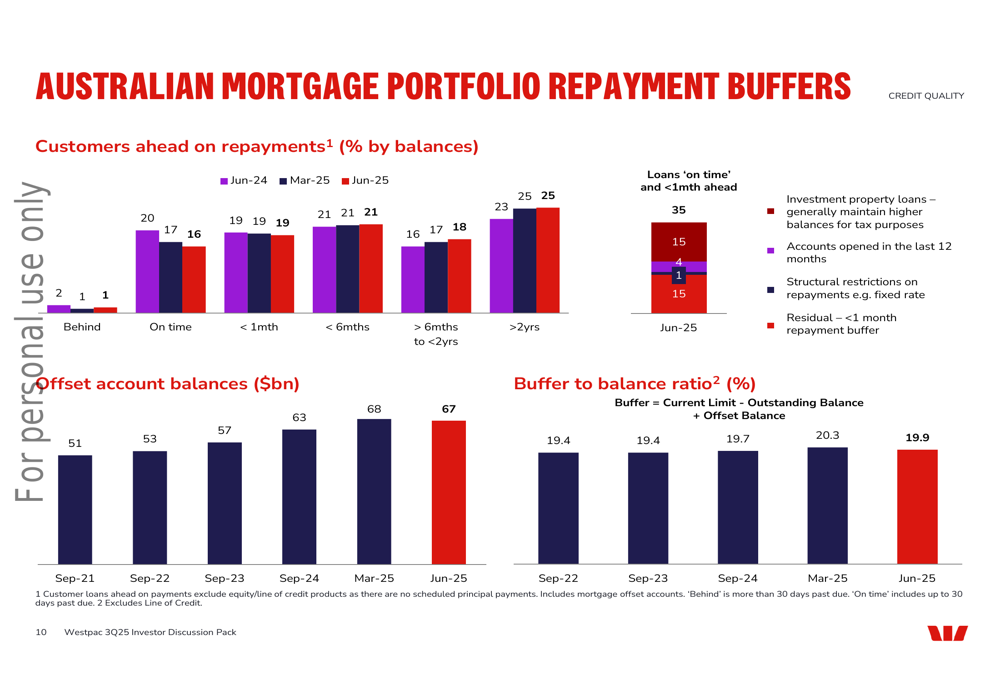

Customer resilience is further evidenced by strong repayment buffers, with a significant portion of mortgage customers ahead on their repayments. This buffer provides protection against potential financial stress and contributes to the bank’s overall credit quality.

Capital and Liquidity Position

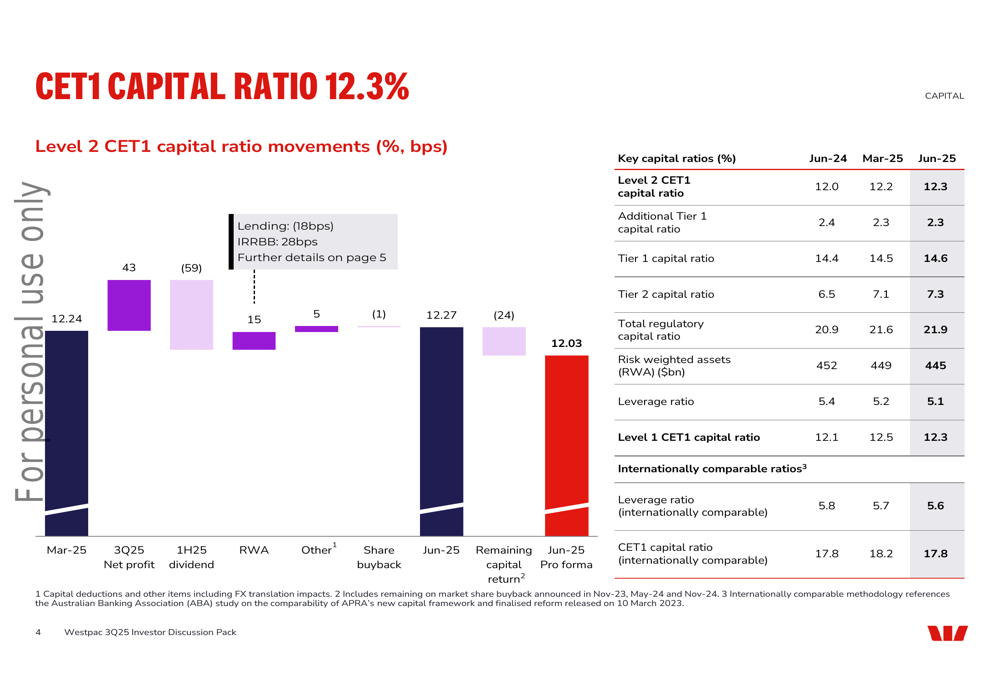

Westpac maintained a robust capital position with a Common Equity Tier 1 (CET1) capital ratio of 12.3%, well above its target operating range of 11.0-11.5%. This strong capital buffer provides flexibility for the bank to navigate economic uncertainties and support future growth.

The following chart breaks down the movements in Westpac’s CET1 capital ratio:

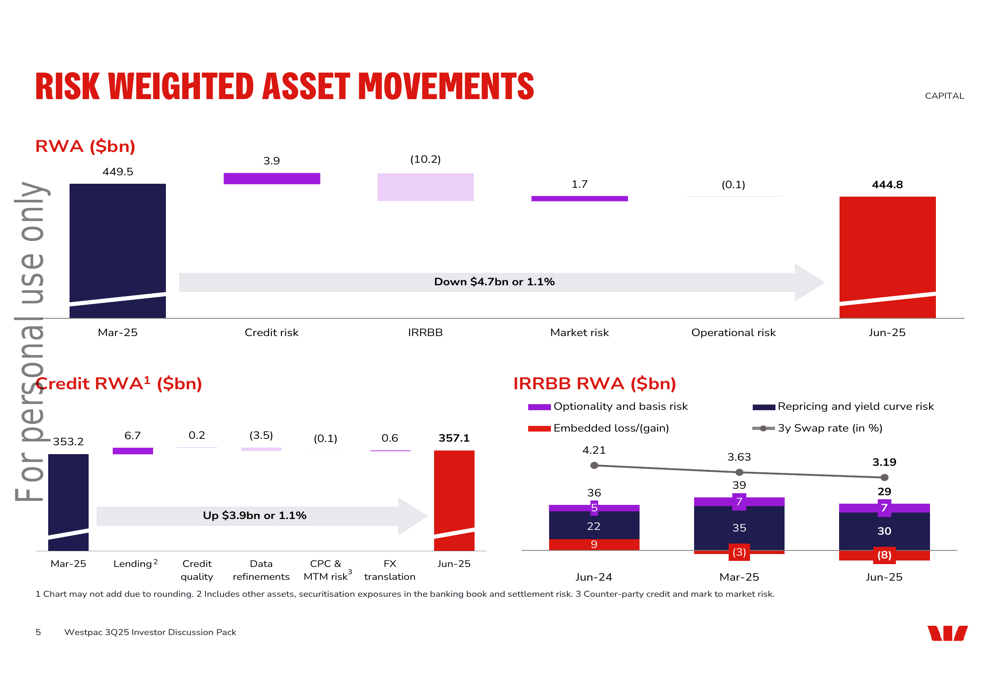

Risk-weighted assets (RWA) decreased by $4.7 billion or 1.1% to $444.8 billion, primarily driven by a reduction in interest rate risk in the banking book (IRRBB), partially offset by increases in credit risk and market risk.

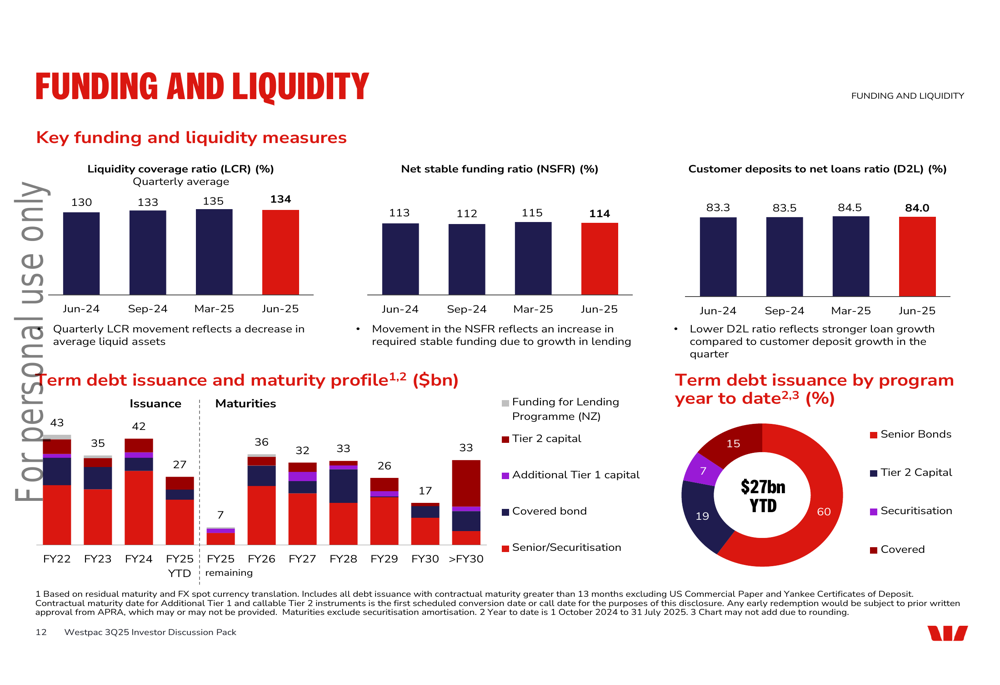

Liquidity metrics remained strong with a Liquidity Coverage Ratio (LCR) of 134% and a Net Stable Funding Ratio (NSFR) of 114%, both well above regulatory requirements. These metrics underscore Westpac’s solid funding and liquidity position, essential for maintaining financial stability.

Forward-Looking Statements

While the presentation does not provide explicit forward guidance, Westpac’s increased weighting to downside economic scenarios (now at 47.5%) suggests a cautious outlook. The bank appears well-positioned to navigate potential economic challenges with its strong capital position, robust credit quality, and significant customer repayment buffers.

The resilience of the Australian mortgage portfolio, particularly the decreasing delinquency rates and substantial repayment buffers, indicates that Westpac has taken appropriate measures to manage risks in its largest lending segment.

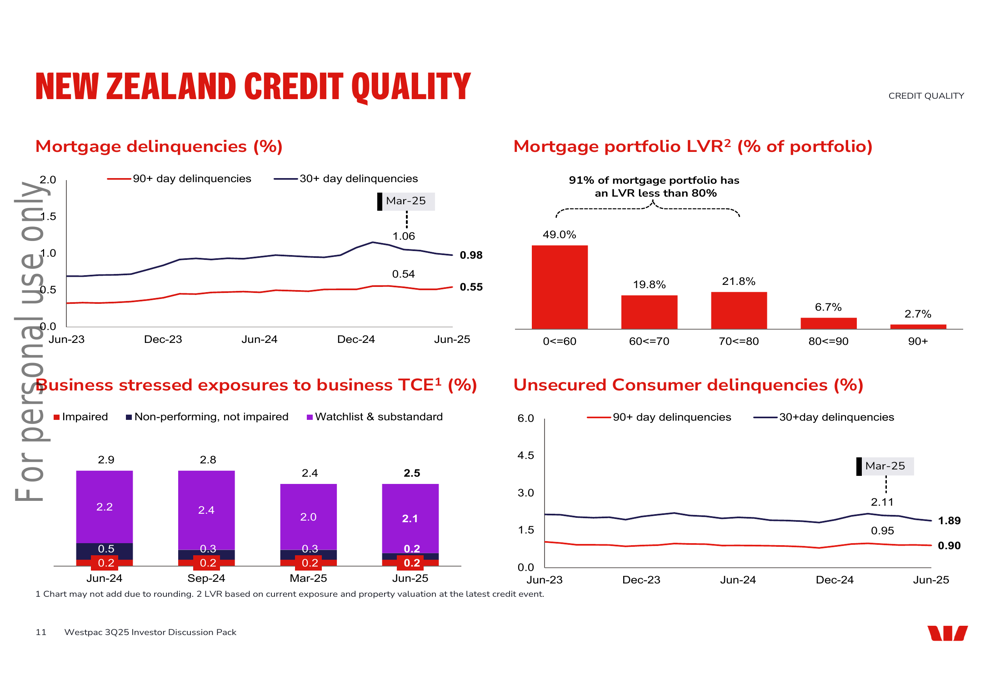

The New Zealand operations also show stable credit quality metrics, contributing to the overall strength of the bank’s international portfolio.

Westpac’s Q3 2025 results demonstrate the bank’s ability to deliver solid financial performance while maintaining prudent risk management practices. The combination of profit growth, improved credit metrics, and strong capital position provides a solid foundation for sustainable performance in the coming quarters, even as economic uncertainties persist.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.