e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Introduction & Market Context

WEX Inc (NYSE:WEX) released its second quarter 2025 financial results on July 24, 2025, showing a mixed performance with declining revenue but improved earnings per share. The payment solutions provider’s stock responded positively in premarket trading, rising 5.2% to $171.89, suggesting investors were encouraged by the company’s ability to grow earnings despite top-line challenges.

The results come against a backdrop of fluctuating fuel prices and shifting business dynamics across WEX’s three main segments. The company’s diversified business model continues to demonstrate resilience, with strong performance in its Benefits segment helping to offset challenges in Mobility and Corporate Payments.

Quarterly Performance Highlights

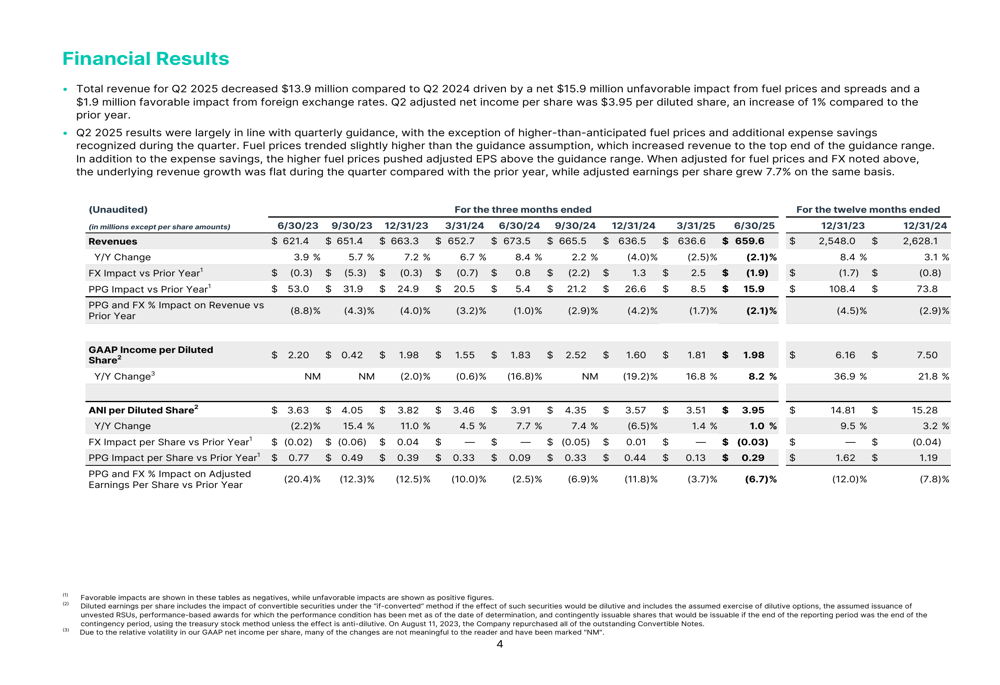

WEX reported total revenue of $659.6 million for Q2 2025, representing a 2.1% decrease compared to the same period last year. The decline was primarily attributed to a $15.9 million unfavorable impact from fuel prices and spreads, partially offset by a $1.9 million favorable impact from foreign exchange rates.

Despite the revenue decline, adjusted net income per diluted share reached $3.95, a 1% increase year-over-year, demonstrating the company’s ability to improve profitability even amid challenging conditions. GAAP income per diluted share showed stronger growth at 8.2% year-over-year.

As shown in the following comprehensive financial summary:

The sequential improvement from Q1 2025, when the company reported revenue of $636.6 million and EPS of $3.51, indicates positive momentum despite the year-over-year comparison challenges.

Segment Performance Analysis

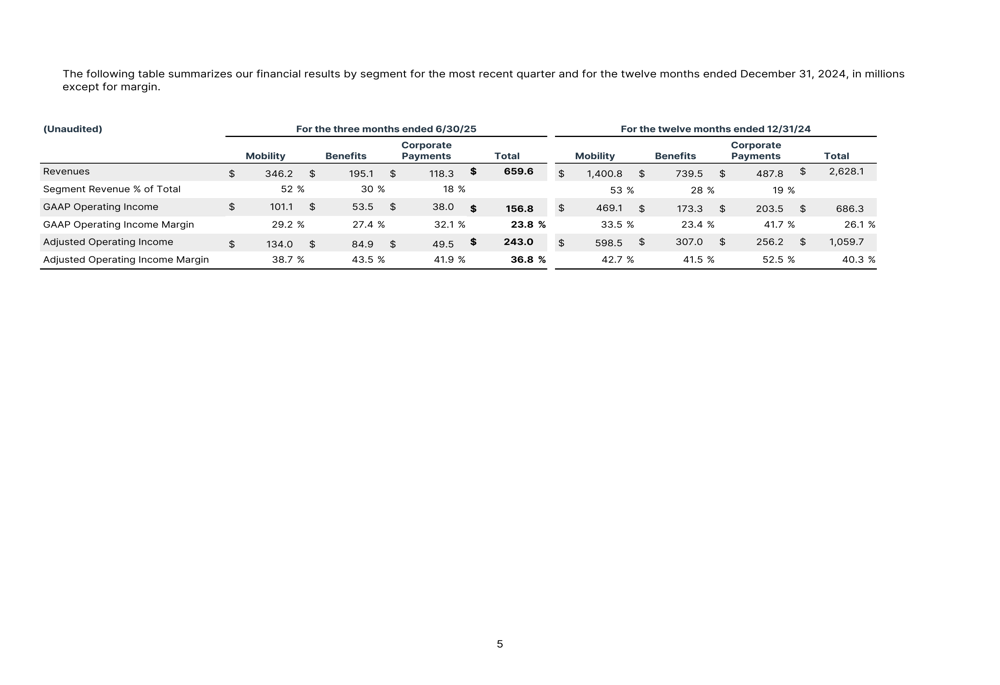

WEX’s performance varied significantly across its three business segments, with Benefits showing strong growth while Mobility and Corporate Payments faced headwinds.

The segment breakdown reveals the relative contribution and performance of each business unit:

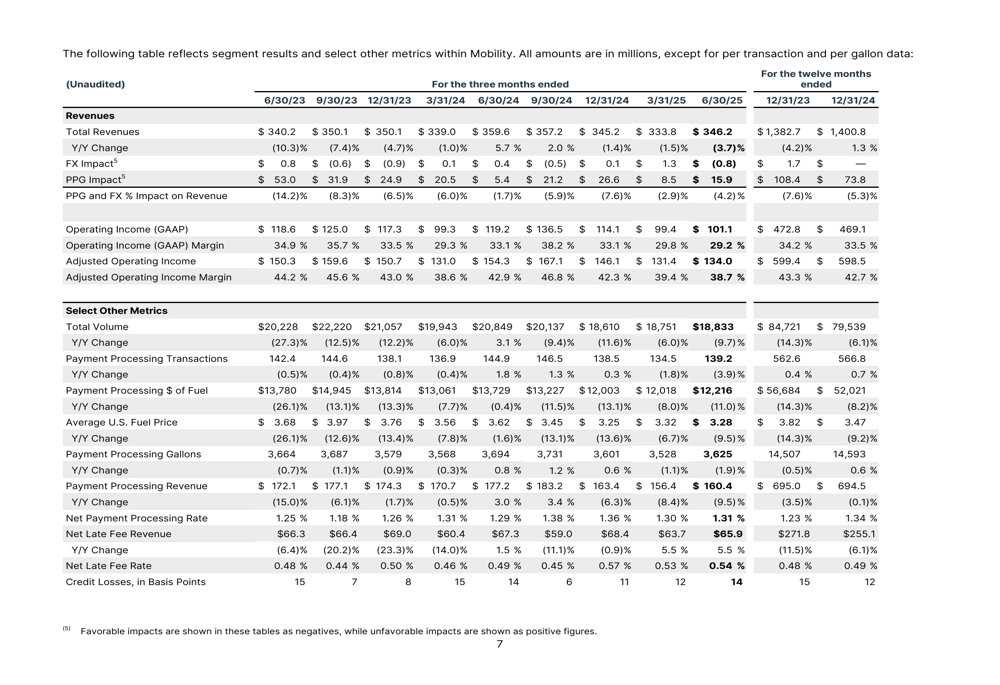

The Mobility segment, WEX’s largest revenue generator, experienced a 3.7% decline in revenue to $346.2 million. This decrease was primarily driven by lower fuel prices and a 3.9% reduction in payment processing transactions. The average domestic fuel price in Q2 2025 was $3.28, contributing to the revenue pressure. Despite these challenges, the segment maintained strong profitability with a GAAP operating income margin of 29.2% and an adjusted operating income margin of 38.7%.

The detailed metrics for the Mobility segment illustrate the impact of transaction volume and fuel price changes:

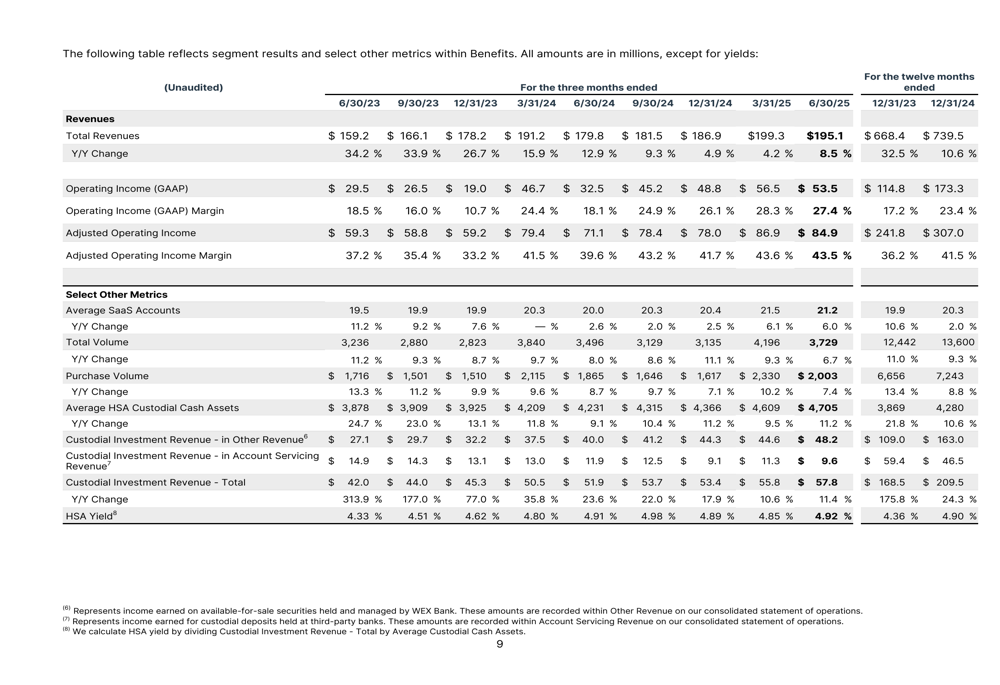

In contrast, the Benefits segment delivered strong growth, with revenue increasing 8.5% to $195.1 million. This performance was driven by a 6.0% year-over-year increase in average SaaS accounts to 21.2 million, 7% growth in HSA accounts, and a 7.4% increase in benefits purchase volume. The segment’s average custodial cash assets grew 11.2% year-over-year to $4.7 billion, generating $57.8 million in revenue.

The Benefits segment’s consistent growth trajectory is evident in the following metrics:

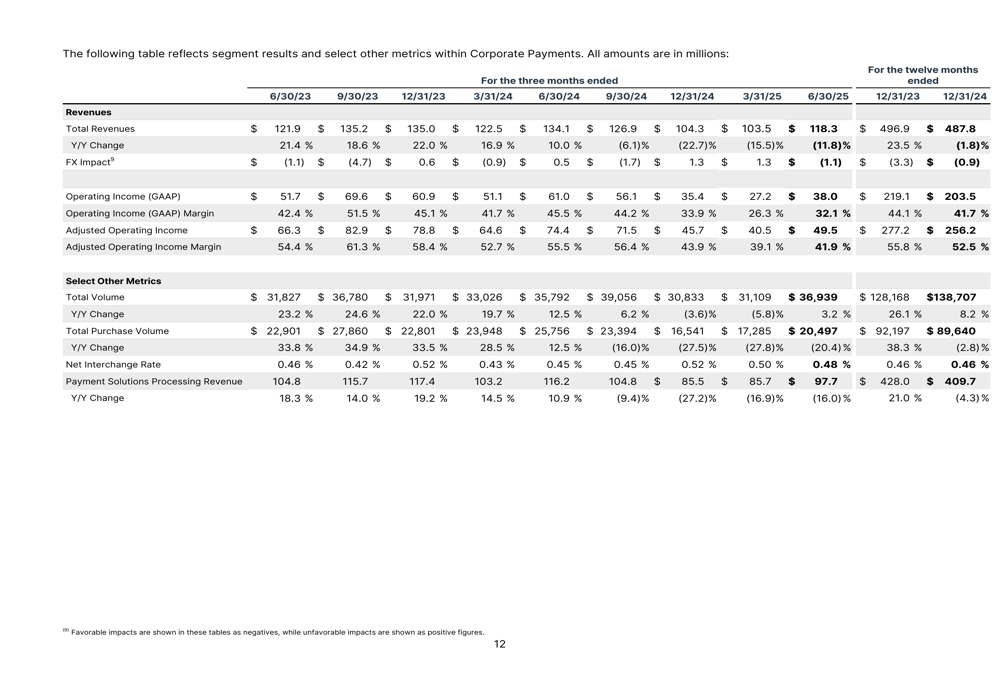

The Corporate Payments segment faced the most significant challenges, with revenue declining 11.8% to $118.3 million. This decrease was primarily attributed to changes in the revenue model for a major online travel agency customer. Total (EPA:TTEF) purchase volumes issued by WEX decreased 20.4%, though the segment maintained strong profitability with a GAAP operating income margin of 32.1% and an adjusted operating income margin of 41.9%.

The Corporate Payments segment’s performance metrics highlight the impact of the customer model change:

Financial Position and Cash Flow

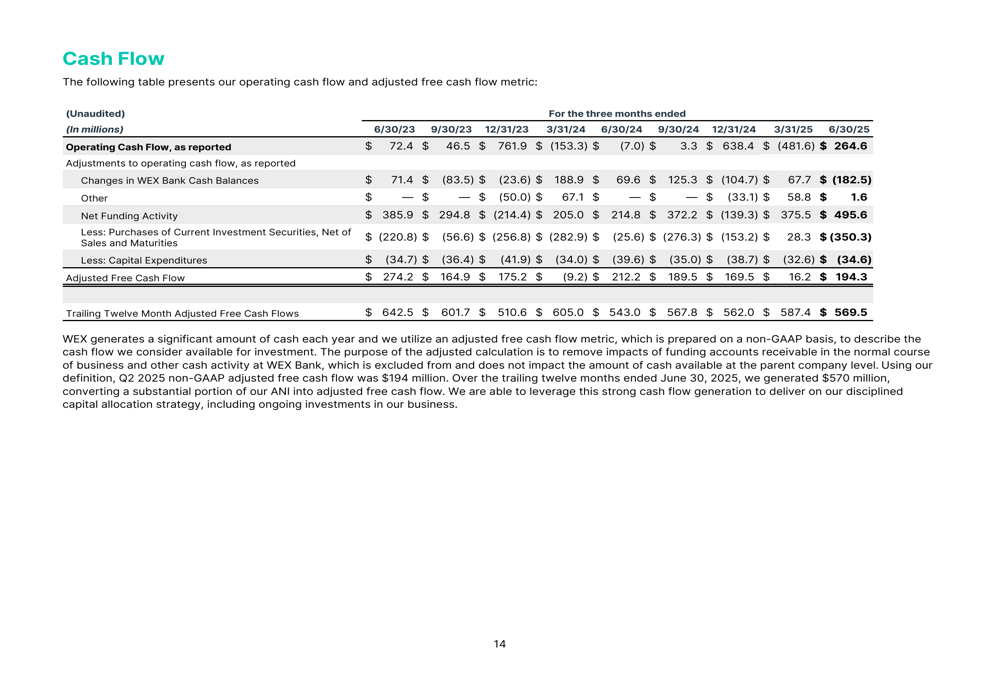

WEX maintained a strong financial position in Q2 2025, generating $194.3 million in adjusted free cash flow. The company’s trailing twelve-month adjusted free cash flow reached $569.5 million, demonstrating consistent cash generation capability.

The cash flow performance provides insight into WEX’s operational efficiency:

On the capital allocation front, WEX completed a significant share repurchase through a modified Dutch auction tender offer on March 31, 2025, with a cash payment of $750.0 million. This strategic move reflects management’s confidence in the company’s long-term prospects and commitment to returning value to shareholders.

Forward Guidance and Outlook

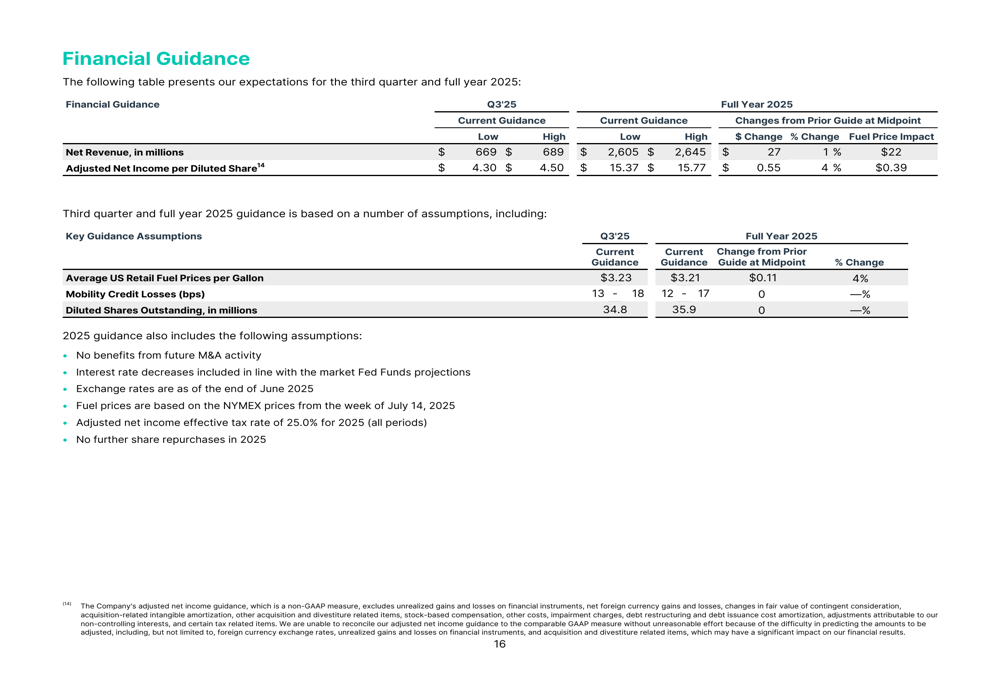

Looking ahead, WEX provided guidance for both Q3 and full-year 2025. For the full year, the company projects net revenue in the range of $2,605 to $2,645 million and adjusted net income per diluted share between $15.37 and $15.77. These projections are based on an expected average U.S. retail fuel price of $3.21 per gallon.

The detailed financial guidance provides insight into management’s expectations:

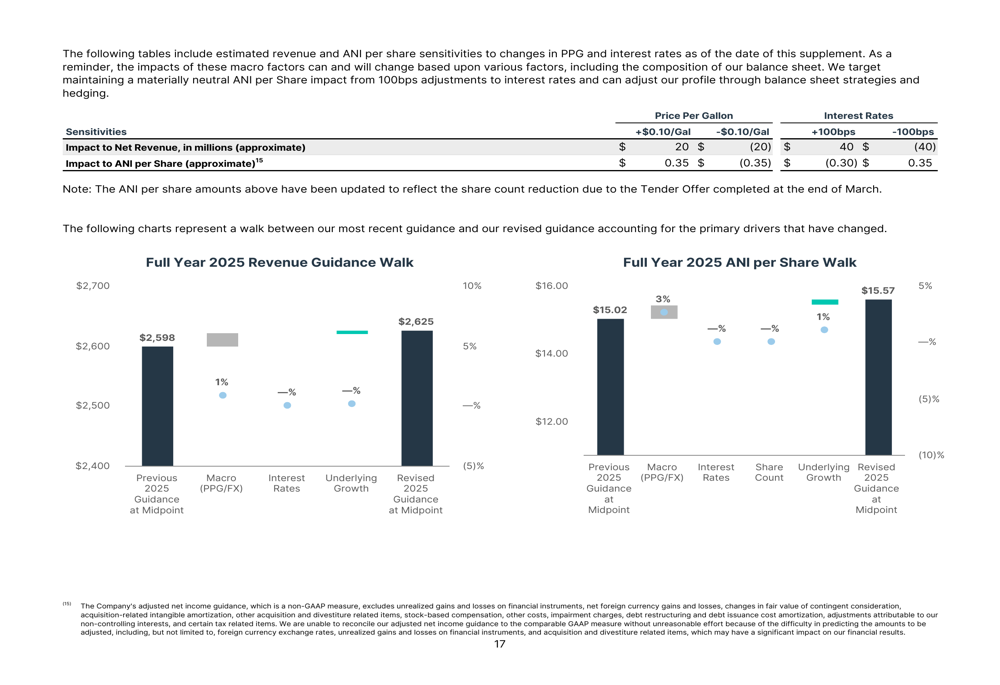

WEX also provided sensitivity analysis to help investors understand the potential impact of fuel price fluctuations and interest rate changes on its financial results. A $0.10 per gallon change in fuel prices would impact net revenue by approximately $20 million and adjusted net income per share by $0.35.

The sensitivity analysis illustrates key factors that could affect WEX’s performance:

The company’s guidance suggests confidence in its ability to navigate the current market environment while continuing to invest in growth opportunities. The Benefits segment is expected to remain a key growth driver, while management anticipates stabilization in the Mobility segment and eventual recovery in Corporate Payments in the coming quarters.

With a diversified business model and strong cash flow generation, WEX appears well-positioned to weather near-term challenges while pursuing long-term growth opportunities across its three core segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.