Two National Guard members shot near White House

Introduction & Market Context

Whitestone REIT (NYSE:WSR) released its Q3 2025 earnings presentation on October 30, highlighting the company's continued focus on high-value shop space in Sun Belt markets. The company reported revenue of $41 million, up 6% year-over-year, and Core FFO per share of $0.26, slightly above the $0.25 reported in Q3 2024. The stock rose 4.74% during regular trading hours to close at $12.04, though it dipped 1.58% in pre-market trading the following day.

Whitestone's strategy centers on smaller retail spaces (1,500-3,000 square feet) in high-growth markets across Texas and Arizona. This approach has yielded consistent leasing spreads and occupancy improvements, positioning the REIT favorably compared to its shopping center peers.

Quarterly Performance Highlights

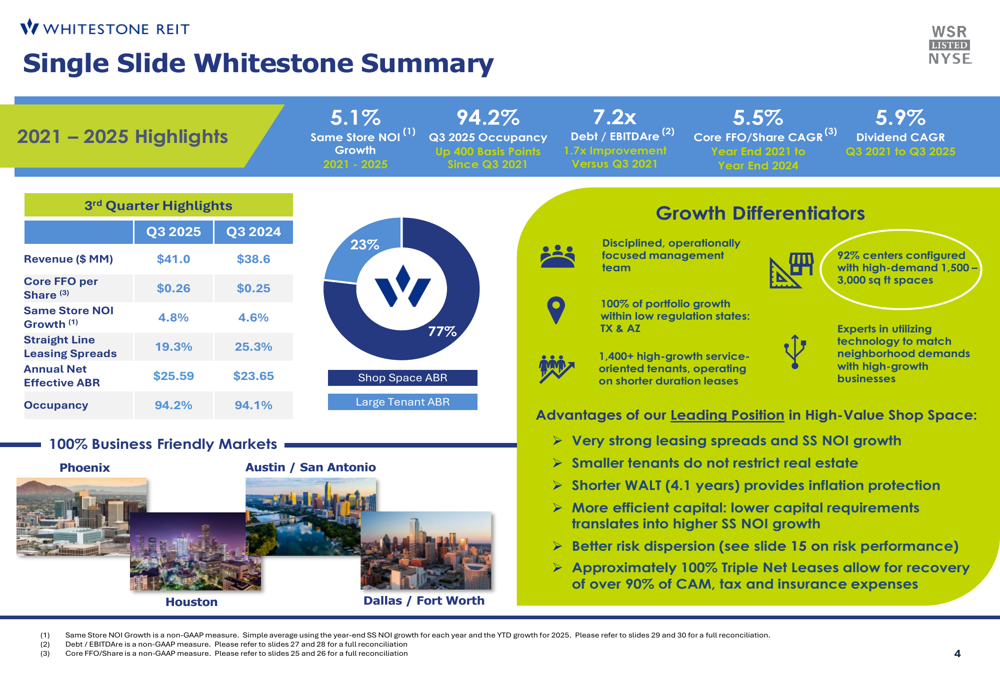

Whitestone's Q3 2025 results demonstrated solid growth across key metrics. Revenue increased to $41 million from $38.6 million in Q3 2024, while same-store NOI growth reached 4.8%, slightly outpacing the 4.6% reported in the same quarter last year.

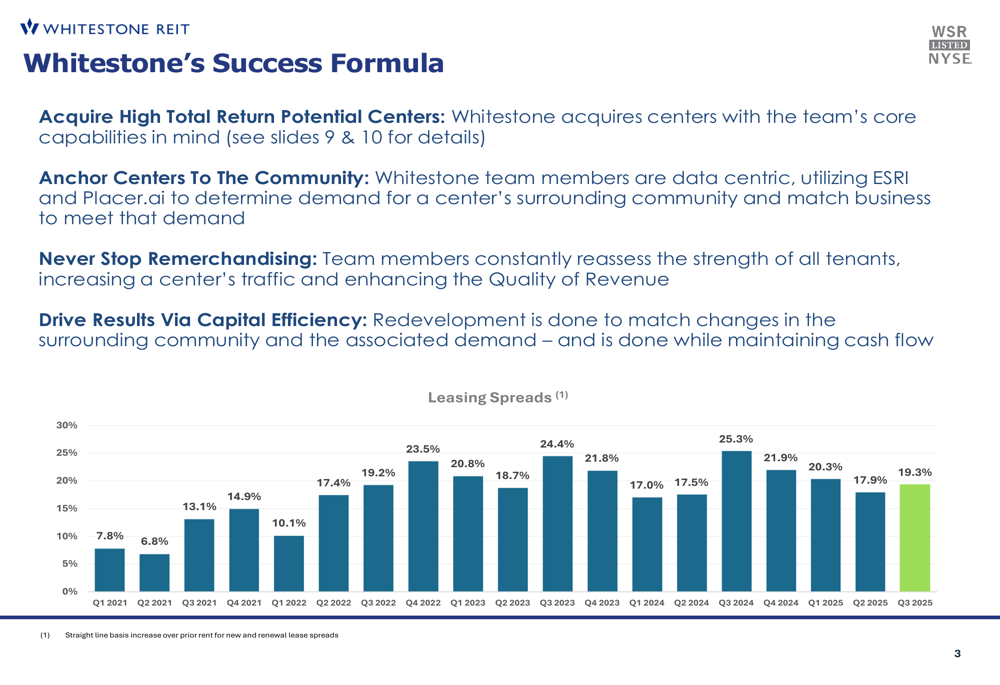

The company achieved leasing spreads of 19.3% in Q3 2025, continuing a pattern of double-digit spreads that has persisted since 2021. This performance reflects strong demand for Whitestone's retail spaces in its target markets.

As shown in the following chart of quarterly leasing spreads from 2021 through Q3 2025:

Occupancy remained strong at 94.2%, up slightly from 94.1% in Q3 2024 and representing a 400 basis point improvement since Q3 2021. Annual net effective ABR (average base rent) increased to $25.59 from $23.65 year-over-year, an 8.2% improvement.

The following slide provides a comprehensive overview of Whitestone's performance metrics and differentiators:

Strategic Initiatives

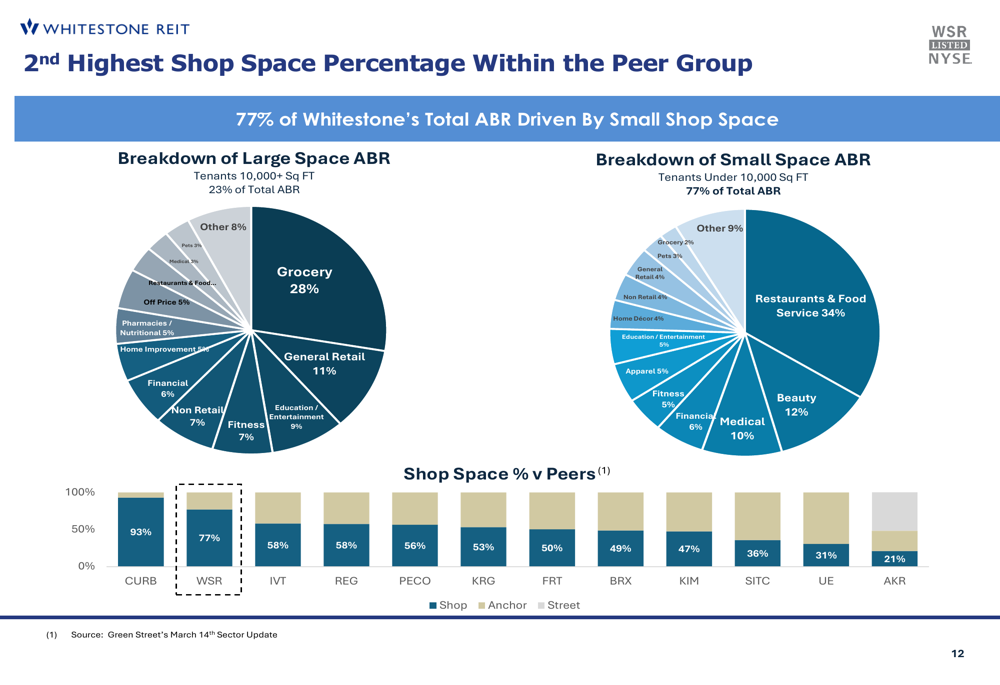

Whitestone's business model revolves around its focus on "shop spaces" – smaller retail units that command higher rents and offer more flexibility. According to the presentation, 77% of the company's ABR comes from shop space tenants, while only 23% comes from larger tenants occupying spaces over 10,000 square feet.

The company outlines its success formula as a four-step process: acquiring high total return potential centers, anchoring centers to the community using data analytics, continuously remerchandising tenant mix, and driving results through capital-efficient redevelopment.

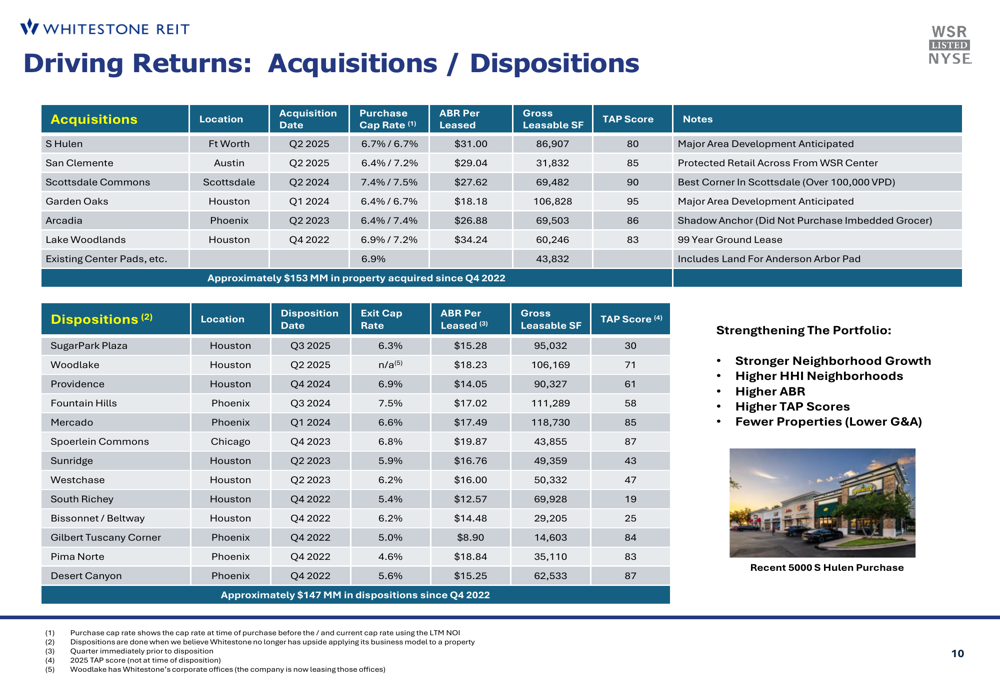

Since Q4 2022, Whitestone has acquired approximately $153 million in properties while disposing of about $147 million, effectively upgrading its portfolio quality. Recent acquisitions include properties in Fort Worth, Austin, Scottsdale, Houston, and Phoenix, with cap rates ranging from 6.4% to 7.4%.

The company's recent acquisition and disposition activity is detailed in the following slide:

Whitestone is also pursuing redevelopment opportunities to boost future NOI growth, with potential pad site developments planned for 2025-2026 at locations including Lion's Square (Houston), Williams Trace Plaza (Houston), Scottsdale Commons (Scottsdale), Arcadia (Scottsdale), and Terravita. The company expects these redevelopment efforts to add up to 1% to same-store NOI growth.

Competitive Industry Position

Whitestone positions itself as having the second-highest shop space percentage among its peer group at 77%, behind only CURB at 93%. This focus on smaller spaces is a key differentiator in the shopping center REIT sector.

The company's shop space composition compared to peers is illustrated in this chart:

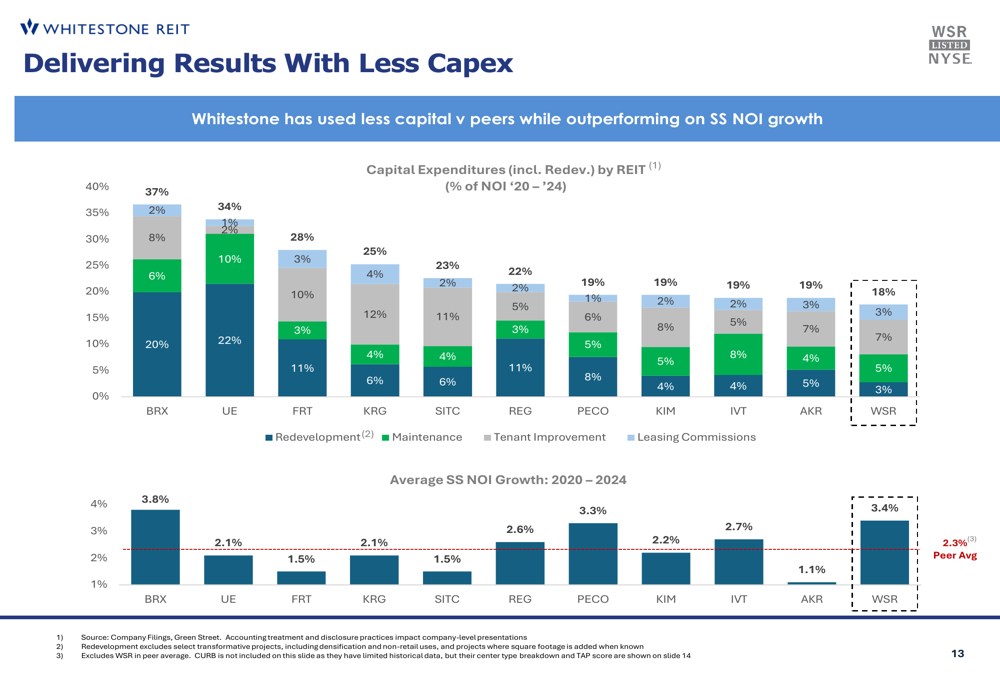

A notable competitive advantage highlighted in the presentation is Whitestone's capital efficiency. The company reports using less capital expenditure as a percentage of NOI compared to peers while delivering above-average same-store NOI growth of 3.4% from 2020-2024, compared to the peer average of 2.3%.

This capital efficiency is demonstrated in the following comparison:

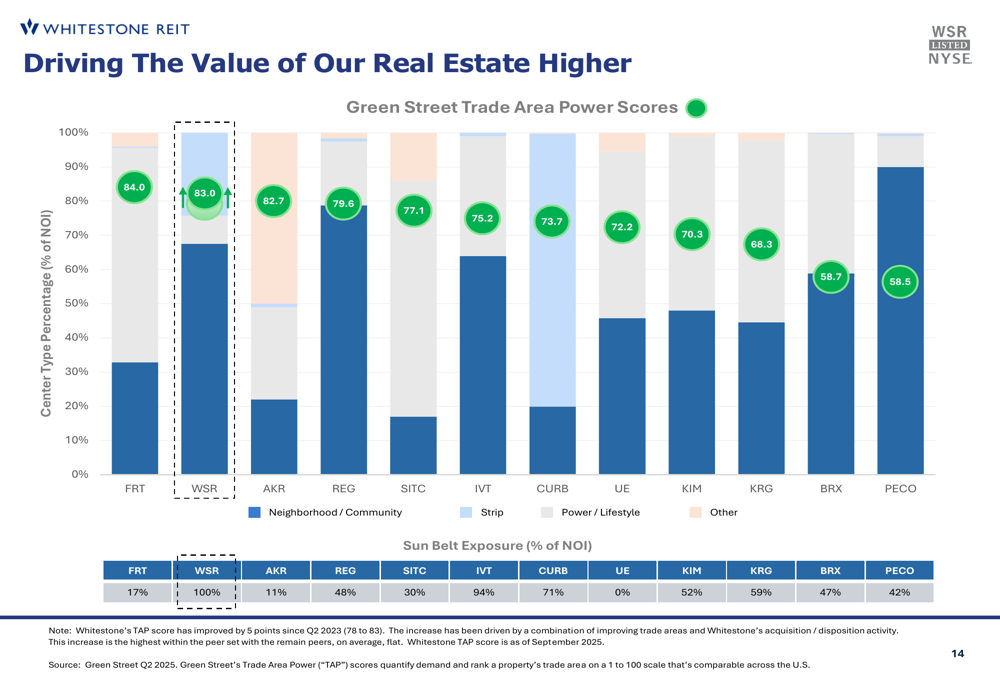

Whitestone also ranks second among peers in Green Street's Trade Area Power Scores with a score of 83.0, just behind Federal Realty Investment Trust (NYSE:FRT) at 84.0. The company stands out with 100% of its portfolio located in Sun Belt markets (Texas and Arizona), significantly higher than most peers.

The company's market positioning is illustrated in this comparative analysis:

Forward-Looking Statements

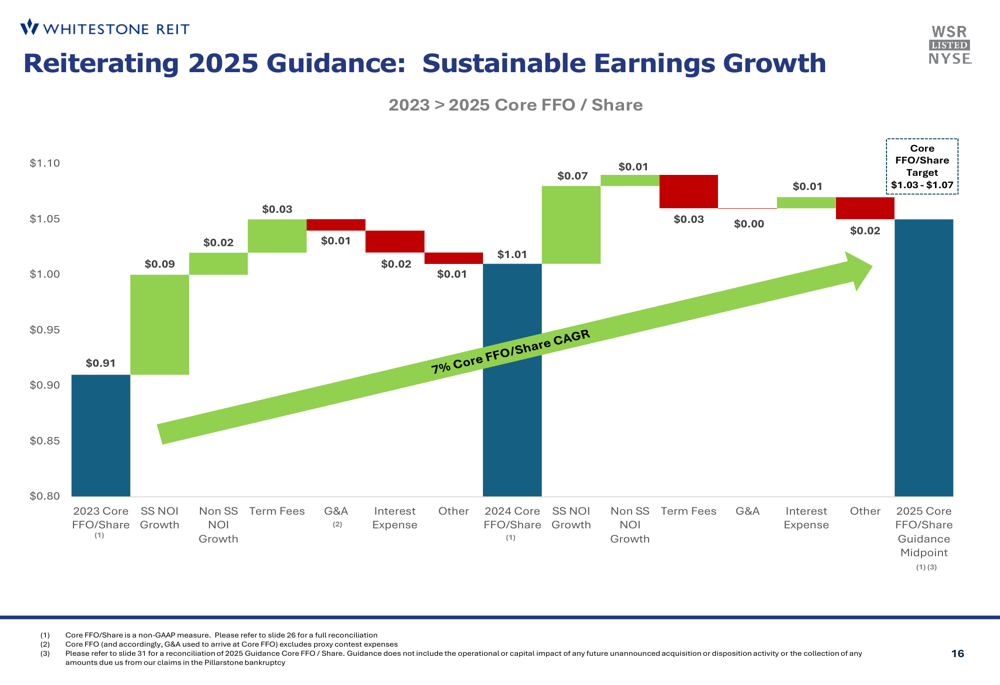

Whitestone reiterated its 2025 Core FFO per share guidance of $1.03-$1.07, representing continued growth from the 2023 base of $0.91 per share. The company expects to achieve this through a combination of same-store NOI growth, strategic acquisitions, and redevelopment initiatives.

Long-term, Whitestone aims to deliver consistent Core FFO growth of 4-6%, with potential to reach 5-7% when including accretive acquisitions. The company projects sustainable same-store NOI growth of 3-5%, driven by contractual rent escalators (2.3% blended average), strong leasing spreads (0.8-1.8%), and redevelopment contributions (up to 1.0%).

The bridge to Whitestone's 2025 Core FFO target is illustrated in this chart:

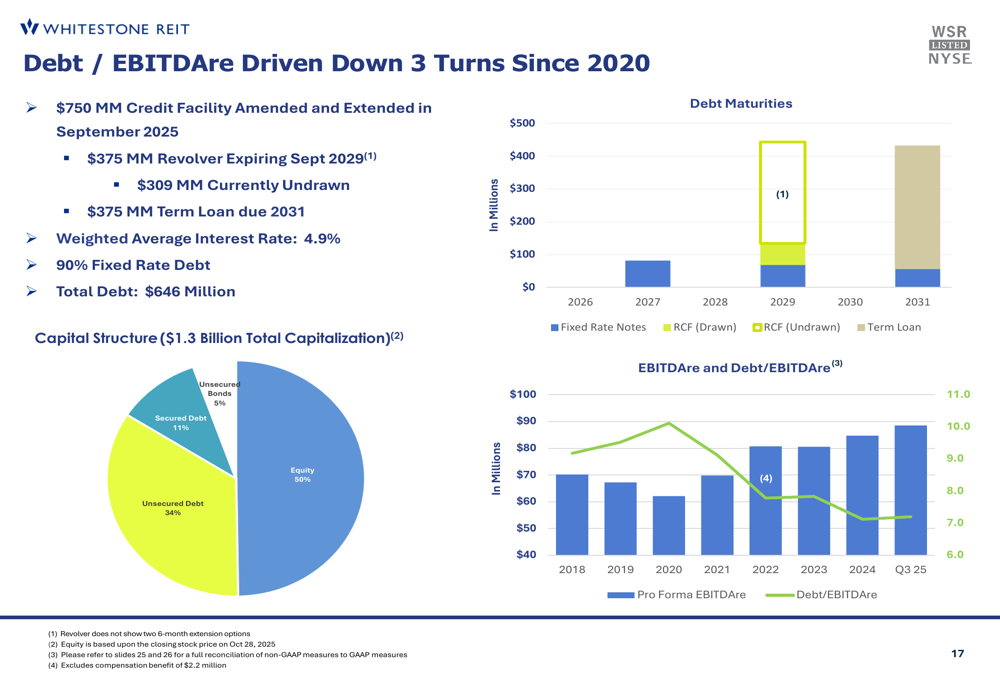

The company has also made significant progress in strengthening its balance sheet, reducing its Debt/EBITDAre ratio by approximately 3 turns since 2020. As of Q3 2025, Whitestone reports 90% fixed-rate debt with a weighted average interest rate of 4.9% and $309 million currently undrawn from its credit facility.

This debt reduction trend is shown in the following slide:

Market Outlook

Whitestone's markets are expected to outperform the broader U.S. economy, with projected five-year job growth of 1.1% CAGR compared to the U.S. average of 0.7%. Population growth in these markets is also projected to be double the national average.

The company cites favorable supply/demand dynamics, with strip center supply growth expected to remain flat through 2029, supporting continued rent growth. Whitestone's focus on service-oriented tenants also provides some insulation from e-commerce competition.

CEO Dave Holeman emphasized the company's clear path forward during the earnings call, stating, "Our path forward is clear. Deliver on consistent earnings growth." This aligns with the presentation's focus on sustainable growth drivers and capital-efficient operations.

As Whitestone continues to execute its high-value shop space strategy in high-growth Sun Belt markets, the company appears well-positioned to maintain its trajectory of steady revenue and NOI growth, though investors will be watching closely to see if the REIT can deliver on its ambitious 2025 guidance targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.