Gold prices cool after hitting over 2-week high on Fed independence fears

Introduction & Market Context

Woodward , Inc. (NASDAQ:WWD) released its third quarter fiscal year 2025 results on July 28, 2025, showcasing solid performance driven primarily by its aerospace segment. The company’s stock closed at $257.26 on the day of the announcement, near its 52-week high of $259.40, reflecting investor confidence in the company’s trajectory.

The industrial technology firm reported an 8% year-over-year increase in sales and earnings per share (EPS), despite facing headwinds in its industrial segment, particularly in China. The results continue a trend of strong performance, building on the momentum seen in Q2 2025 when the company also exceeded analyst expectations.

Quarterly Performance Highlights

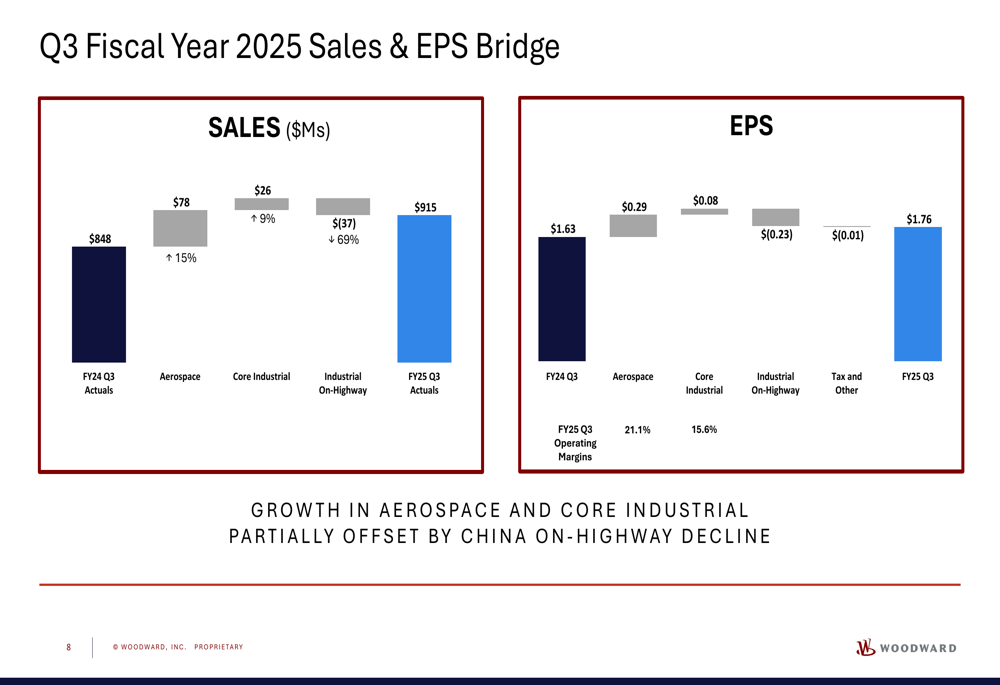

Woodward reported Q3 FY2025 sales of $915 million, an 8% increase from $848 million in the same period last year. Net earnings rose 6% to $108 million, while earnings per share increased 8% to $1.76, compared to $1.63 in Q3 FY2024.

As shown in the following consolidated results chart, the company’s performance was solid across key metrics, though free cash flow declined significantly:

The growth was primarily driven by the aerospace segment, with notable contributions from commercial services and defense OEM sales. This was partially offset by weakness in the industrial segment, particularly in China’s on-highway market.

Chairman and CEO Chip Blankenship commented on the results: "We delivered strong results in the third quarter underpinned by robust demand across our end markets, coupled with disciplined execution by our global teams. We remain focused on growth, operational excellence, and innovation, which continue to position Woodward to deliver sustained long-term shareholder value."

The following bridge chart illustrates how different segments contributed to the overall sales and EPS growth:

Segment Analysis

Woodward’s aerospace segment delivered exceptional results in Q3 FY2025, with sales increasing 15% to $596 million and segment earnings rising 24% to $126 million. The segment’s operating margin improved by 140 basis points to 21.1%.

The aerospace performance is clearly illustrated in the following chart:

Within the aerospace segment, commercial services sales increased by 30%, while defense OEM sales surged by 56%. However, commercial OEM sales decreased by 8%, which the company attributed to ongoing industry supply chain challenges and inventory management by OEMs. Defense services sales also declined by 16%, though the company noted a solid demand environment.

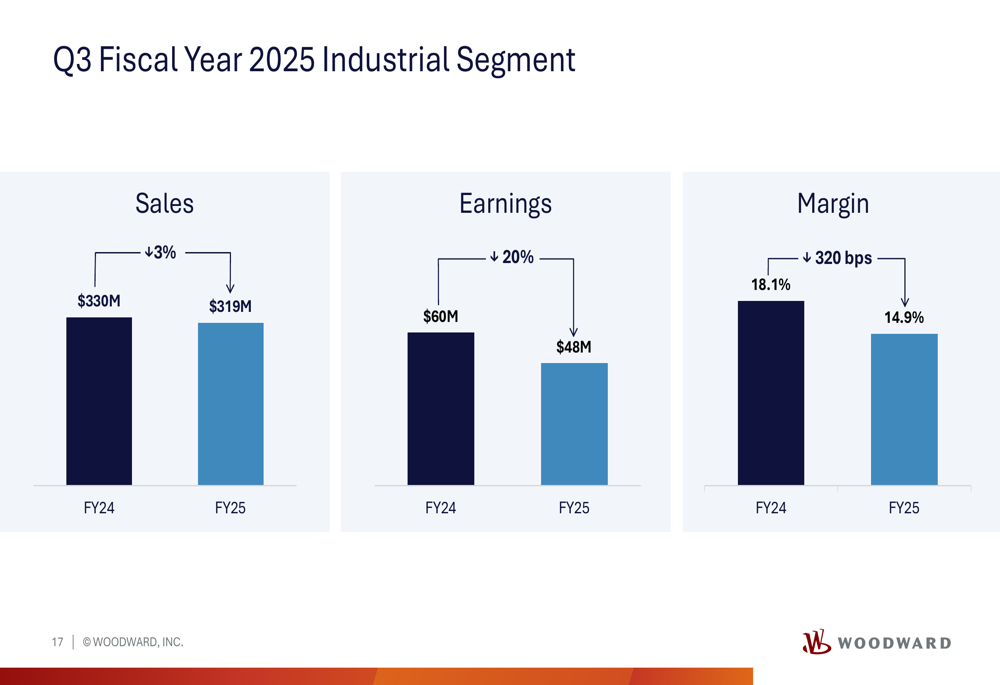

In contrast, Woodward’s industrial segment faced challenges, with overall sales decreasing by 3% to $319 million and segment earnings declining by 20% to $48 million. The segment’s operating margin contracted by 320 basis points to 14.9%.

The following chart details the industrial segment’s performance:

However, when excluding the struggling China on-highway business, Woodward’s core industrial segment showed strength, with sales increasing by 9% to $303 million and earnings rising by 16% to $47 million. The core industrial margin improved by 90 basis points to 15.6%.

The core industrial performance is highlighted in this chart:

Strategic Initiatives and Acquisitions

Woodward highlighted several strategic wins that position the company for long-term growth, particularly in the aerospace sector. The company secured a contract with Airbus for the A350 spoiler actuation system, marking Woodward’s first primary flight control on a commercial platform. This win includes actuation systems for 12 of the 14 aircraft spoilers and positions the company for opportunities on future single-aisle aircraft.

Additionally, Woodward acquired Safran (EPA:SAF)’s North America Electromechanical Actuation business, which brings advanced electromechanical products and control units, including the A350 Horizontal Stabilizer Trim Actuation system. This acquisition strengthens Woodward’s relationships with key aircraft manufacturers including Airbus, Embraer, Gulfstream, and Dassault.

In the industrial segment, despite overall challenges, the company reported 16% growth in oil and gas sales, while power generation sales remained flat. Transportation sales declined by 12%, primarily due to weakness in the China on-highway market.

Revised Guidance and Outlook

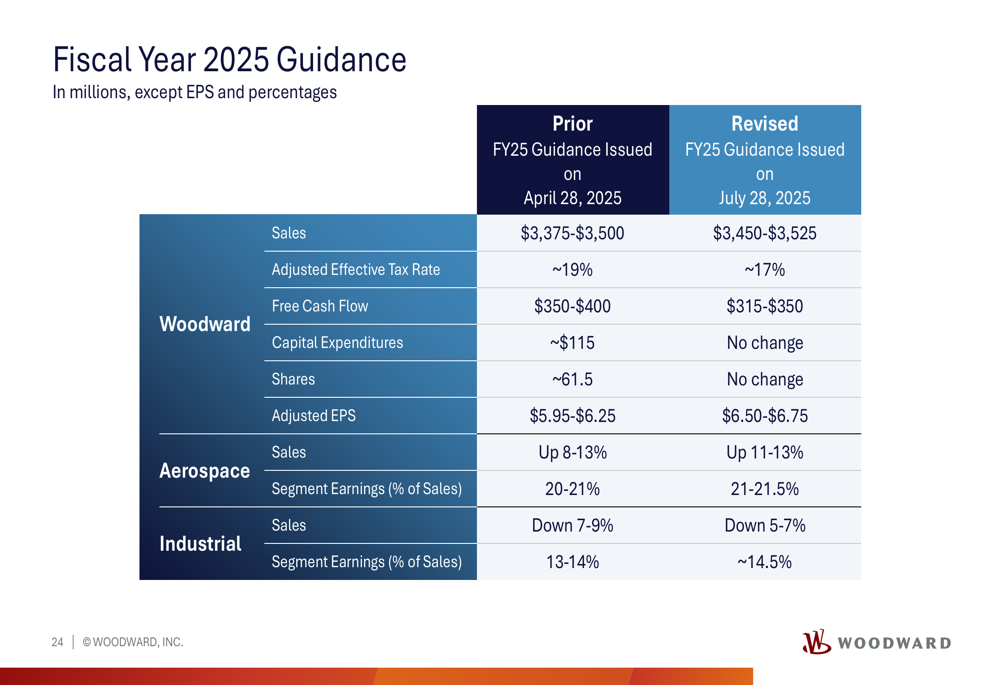

Based on the strong Q3 results and positive outlook, Woodward raised its fiscal year 2025 guidance. The company now expects:

- Sales of $3,450-$3,525 million, up from the previous guidance of $3,375-$3,500 million

- Adjusted EPS of $6.50-$6.75, significantly higher than the previous guidance of $5.95-$6.25

- Aerospace sales growth of 11-13%, up from the previous guidance of 8-13%

- Industrial sales decline of 5-7%, improved from the previous guidance of a 7-9% decline

The following table details the revised guidance compared to the prior outlook:

The company did lower its free cash flow guidance to $315-$350 million from the previous $350-$400 million, and now expects an adjusted effective tax rate of approximately 17%, down from the previous estimate of 19%.

Woodward’s balance sheet remains strong, with a leverage ratio of 1.5 times EBITDA and year-to-date free cash flow of $159 million, positioning the company well for continued strategic investments and shareholder returns.

The revised guidance reflects Woodward’s confidence in its ability to navigate challenges in the industrial segment while capitalizing on strong demand in aerospace, particularly in defense and commercial aftermarket services. With strategic wins and acquisitions strengthening its market position, Woodward appears well-positioned for continued growth through the remainder of fiscal year 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.