Nuscale Power earnings missed by $0.02, revenue fell short of estimates

Introduction & Market Context

Workiva Inc (NYSE:WK) presented its Q2 2025 financial results on July 31, showcasing strong subscription revenue growth and customer expansion, despite which the stock closed down 4.02% at $66.50. The cloud-based compliance and reporting platform provider continues to capitalize on growing demand for integrated reporting solutions across financial, sustainability, and governance sectors.

The company’s presentation highlighted its position in a $35 billion total addressable market (TAM), with solutions spanning financial reporting, governance, risk and compliance (GRC), and sustainability management. Despite the positive quarterly performance, investors appeared cautious about the company’s outlook amid broader market uncertainty.

Quarterly Performance Highlights

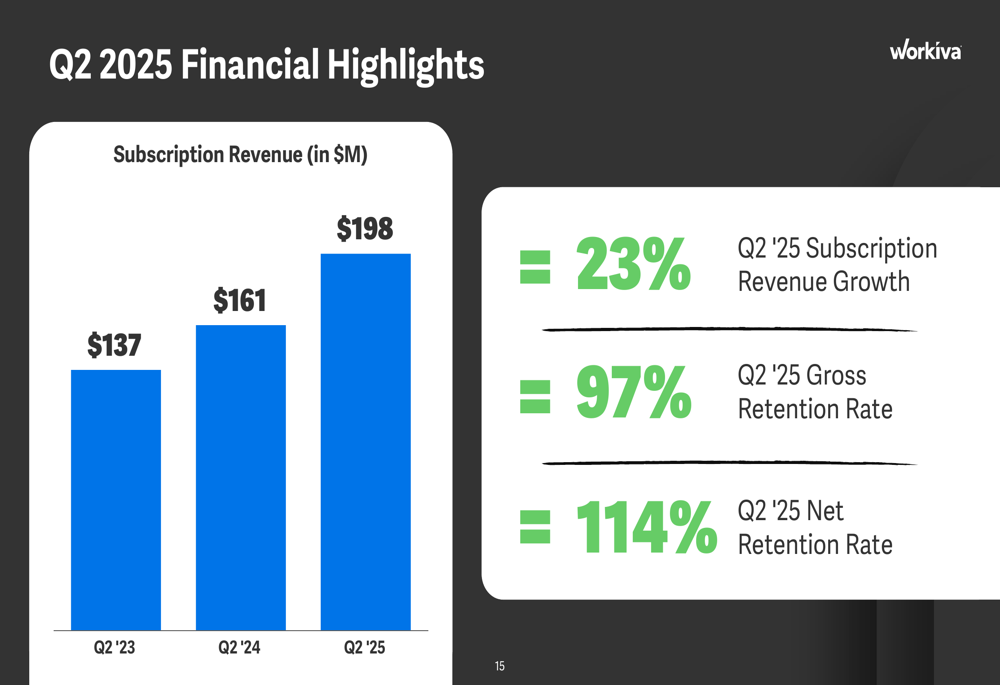

Workiva reported Q2 2025 subscription revenue of $198 million, representing a 23% year-over-year increase compared to $161 million in Q2 2024. The company maintained impressive customer retention metrics with a gross retention rate of 97% and net retention rate of 114%.

As shown in the following chart of quarterly subscription revenue growth:

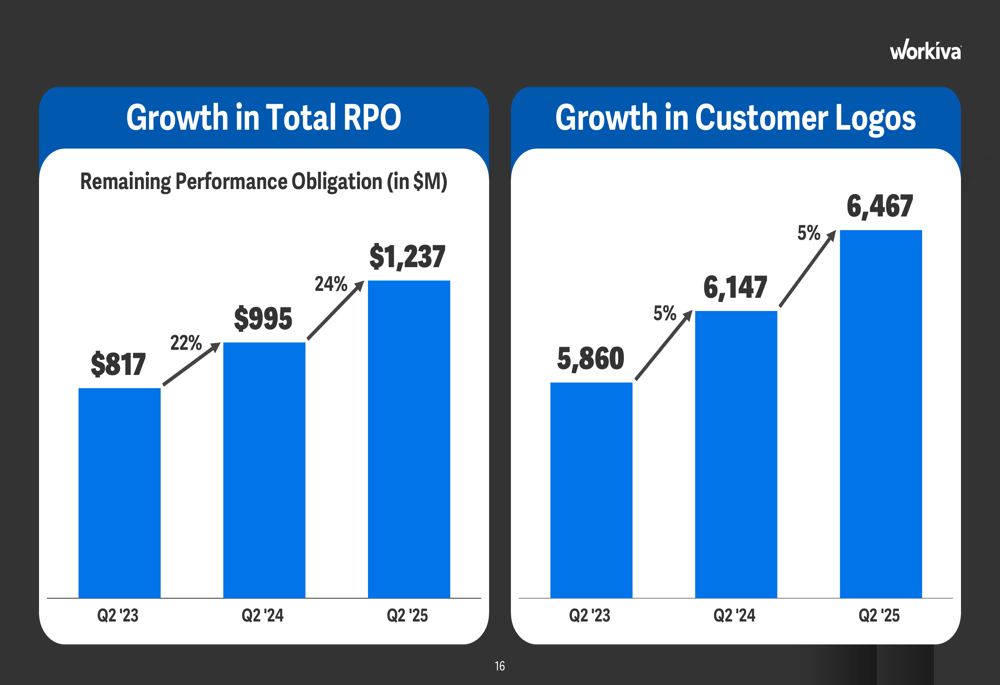

Total (EPA:TTEF) remaining performance obligations (RPO) reached $1.237 billion, up 24% from $995 million in Q2 2024. The company’s customer base expanded to 6,467, a 5% increase from 6,147 in the same period last year. This represents an addition of 82 customers since Q1 2025, when the company reported 6,385 customers.

The following chart illustrates Workiva’s growth in both RPO and customer logos:

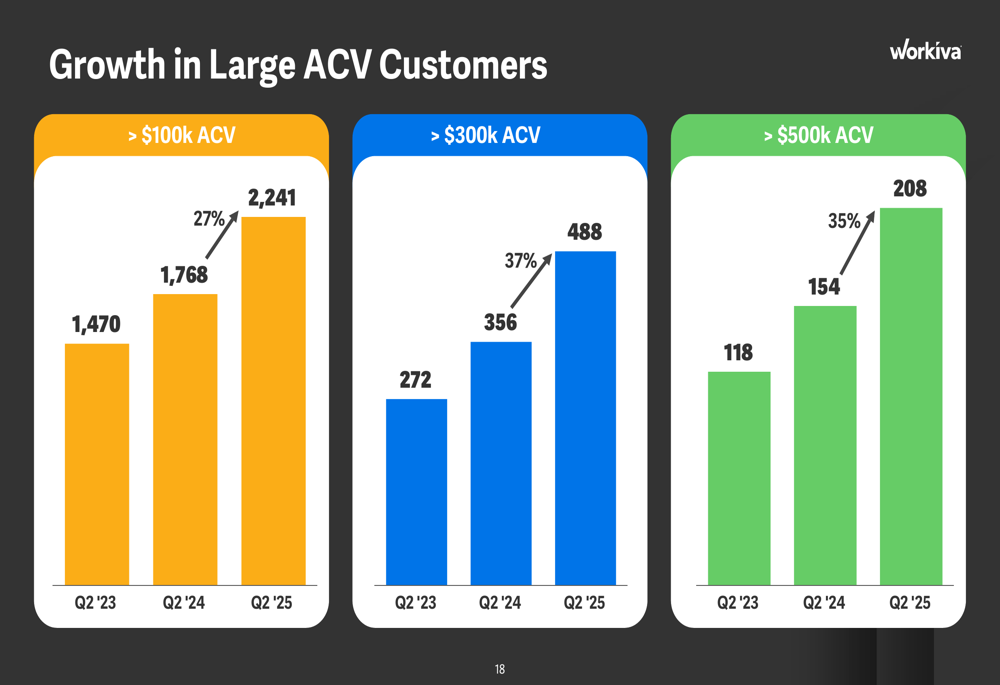

Particularly notable was the company’s success in expanding its base of high-value customers. Workiva reported significant growth across all tiers of annual contract value (ACV) customers:

Strategic Initiatives

Workiva’s platform strategy continues to gain traction, with 71% of subscription revenue now coming from multi-solution customers, up from 67% in Q2 2024 and 62% in Q2 2023. This trend underscores the company’s successful execution of its cross-selling strategy and the increasing value customers are finding in adopting multiple Workiva solutions.

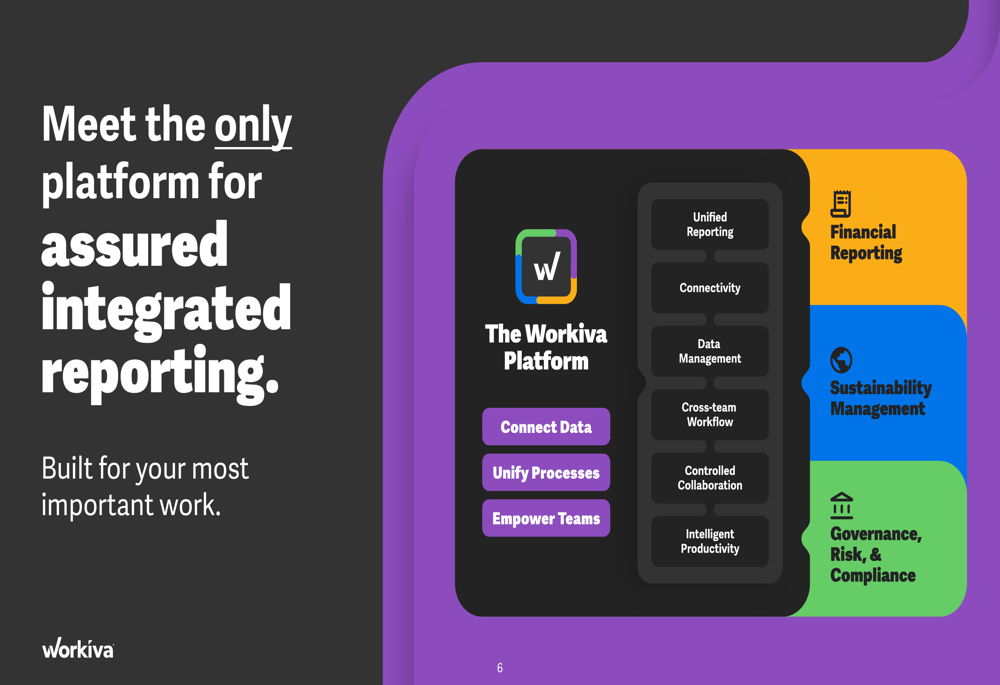

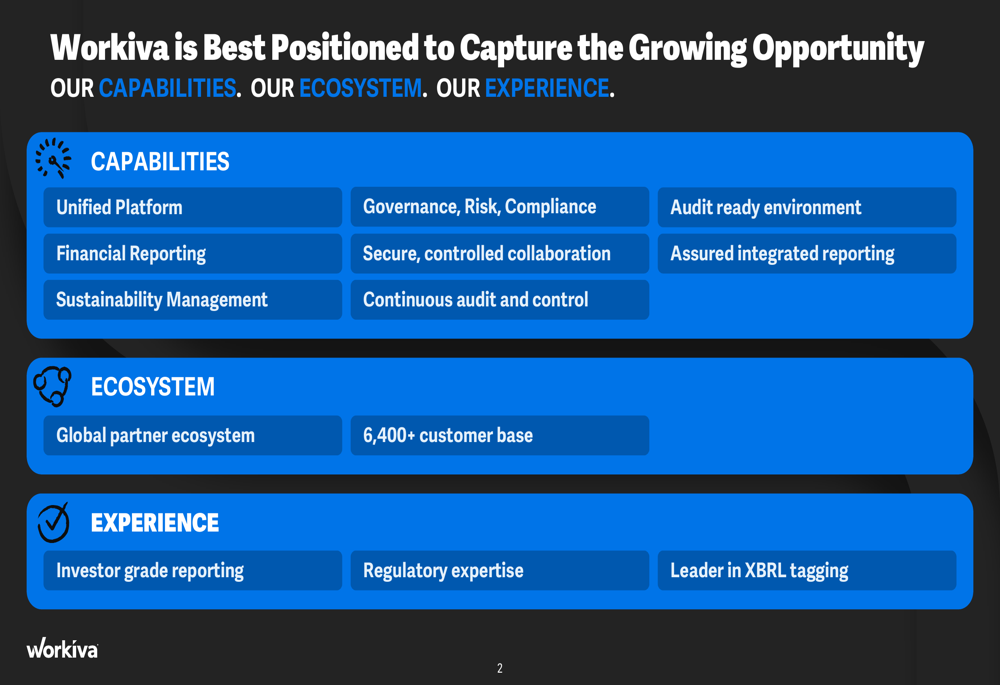

The company’s platform approach addresses the growing complexity in reporting requirements across financial, governance, risk, compliance, and sustainability domains. Workiva positions itself as the only solution for assured integrated reporting, as illustrated in their platform overview:

Workiva’s market opportunity spans multiple domains, with capabilities in unified platform solutions, secure collaboration, continuous audit control, and assured integrated reporting. The company leverages its experience in investor-grade reporting and regulatory expertise to serve over 6,400 customers globally.

Forward-Looking Statements

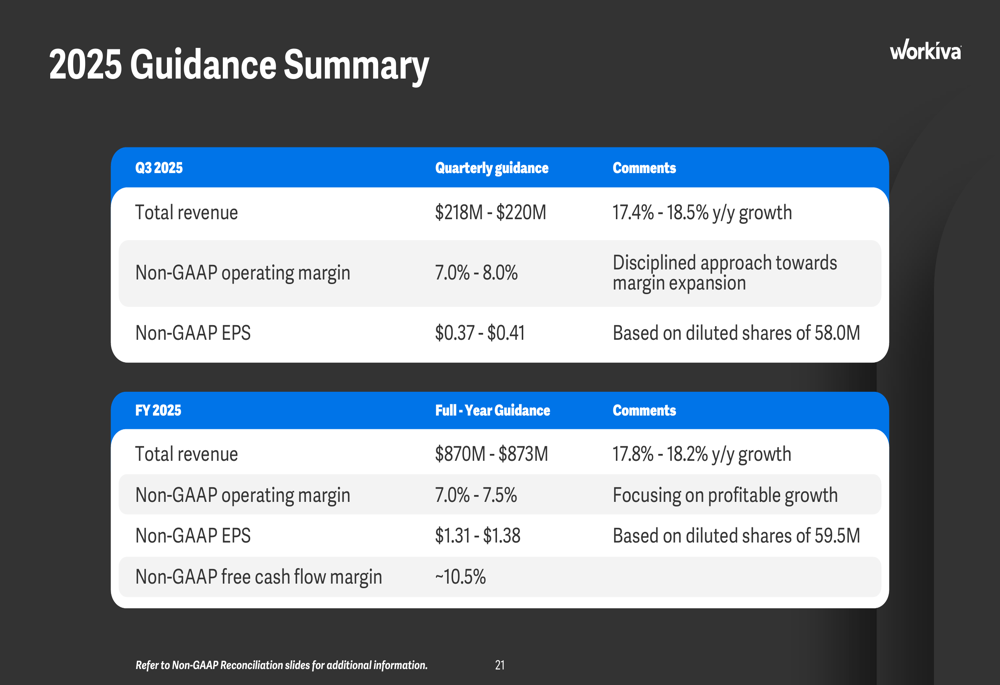

For Q3 2025, Workiva expects total revenue between $218 million and $220 million, representing 17.4% to 18.5% year-over-year growth. The company projects a non-GAAP operating margin of 7.0% to 8.0% and non-GAAP earnings per share between $0.37 and $0.41.

For the full fiscal year 2025, Workiva guided for:

- Total revenue of $870 million to $873 million (17.8% to 18.2% year-over-year growth)

- Non-GAAP operating margin of 7.0% to 7.5%

- Non-GAAP earnings per share of $1.31 to $1.38

- Non-GAAP free cash flow margin of approximately 10.5%

The detailed guidance is presented in the following slide:

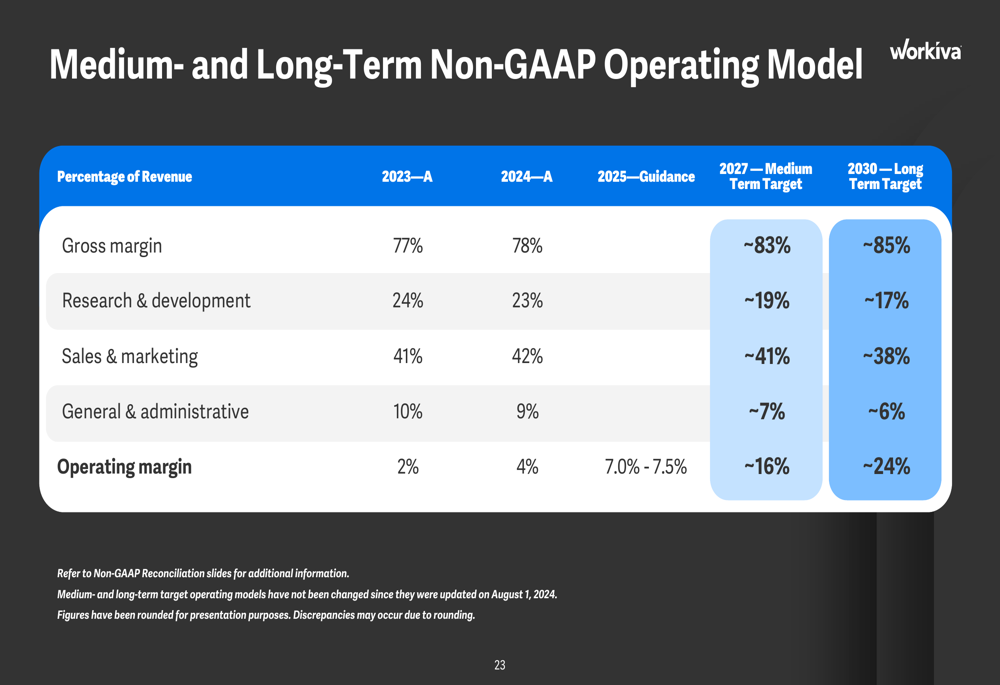

Looking further ahead, Workiva outlined its medium and long-term financial targets, projecting non-GAAP operating margins to expand to approximately 16% by 2027 and 24% by 2030, driven by gross margin improvements and operating expense efficiencies:

Market Reaction & Conclusion

Despite the strong quarterly results and positive guidance, Workiva’s stock declined 4.02% on July 31, closing at $66.50. The stock saw a slight recovery of 0.54% in after-hours trading, reaching $66.86. The negative market reaction may reflect broader concerns about technology valuations or potential growth deceleration, as the company’s projected 17.8%-18.2% revenue growth for FY 2025 represents a slowdown from the 23% subscription revenue growth reported in Q2.

Workiva’s stock remains well below its 52-week high of $116.83, though above its 52-week low of $60.50. The company’s consistent customer retention, expanding high-value customer base, and growing multi-solution adoption suggest strong underlying business fundamentals despite the stock’s recent performance.

With its platform strategy gaining traction and expansion into high-growth areas like sustainability reporting, Workiva appears well-positioned to capitalize on increasing regulatory complexity and reporting requirements across global markets. However, investors may be looking for acceleration in overall revenue growth and faster progress toward the company’s long-term margin targets before driving the stock back toward its previous highs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.