Bubble or no bubble, this is the best stock for AI exposure: analyst

Introduction & Market Context

W.W. Grainger (NYSE:GWW) delivered its Q3 2025 earnings presentation on October 31, showcasing results that exceeded analyst expectations despite ongoing tariff and inflationary pressures. The industrial supply company reported earnings per share of $10.21, beating the forecast of $9.95 by 2.61%, while revenue reached $4.7 billion, surpassing projections by 1.29%.

Despite the earnings beat, Grainger's stock saw minimal movement in pre-market trading, dipping just 0.03% to $956. The company's shares have traded within a 52-week range of $893.99 to $1,227.66, reflecting broader market uncertainty despite solid operational performance.

Quarterly Performance Highlights

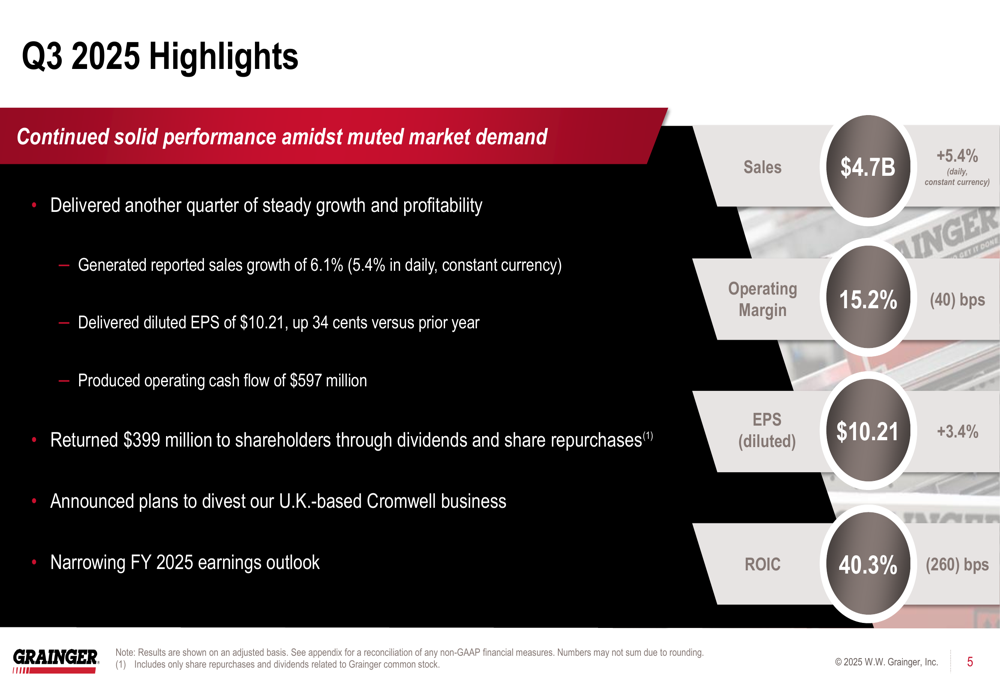

Grainger reported sales of $4.7 billion for Q3 2025, representing a 6.1% increase year-over-year, or 5.4% on a daily, constant currency basis. The company achieved an operating margin of 15.2%, up 40 basis points from the previous year, while diluted EPS grew 3.4% to $10.21.

As shown in the following chart of quarterly highlights:

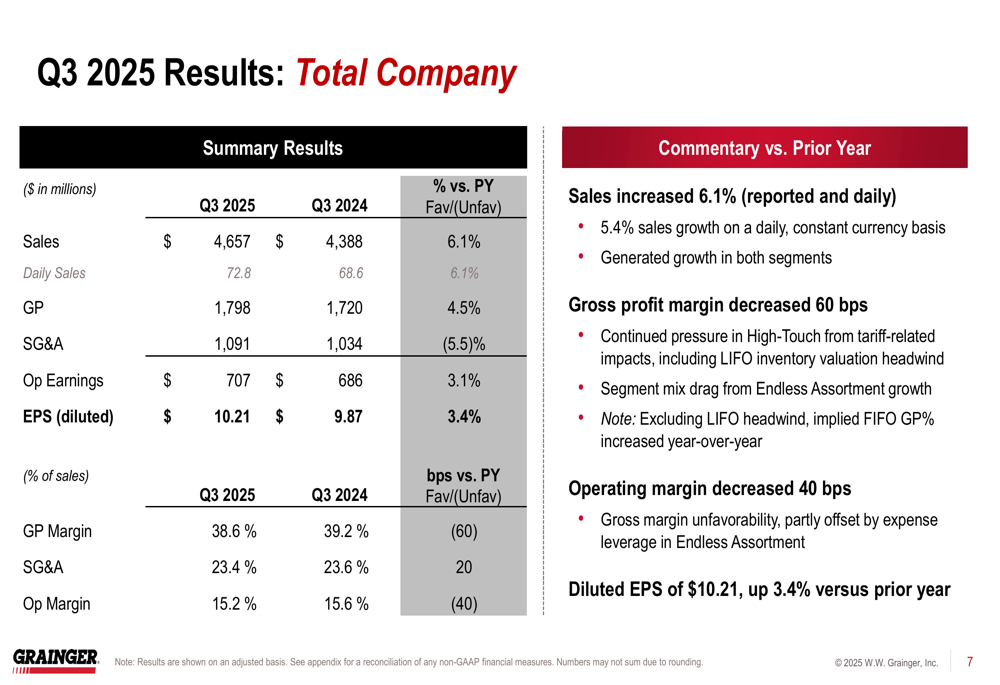

The company's performance was driven by growth across both business segments, though with notably different trajectories. The High-Touch Solutions North America segment, which accounts for approximately 78% of total sales, delivered modest growth of 3.4% to reach $3.6 billion. However, operating margin in this segment declined 40 basis points to 17.2%, primarily due to gross profit margin pressure from tariffs.

The detailed financial breakdown for the total company reveals the mixed impact on margins:

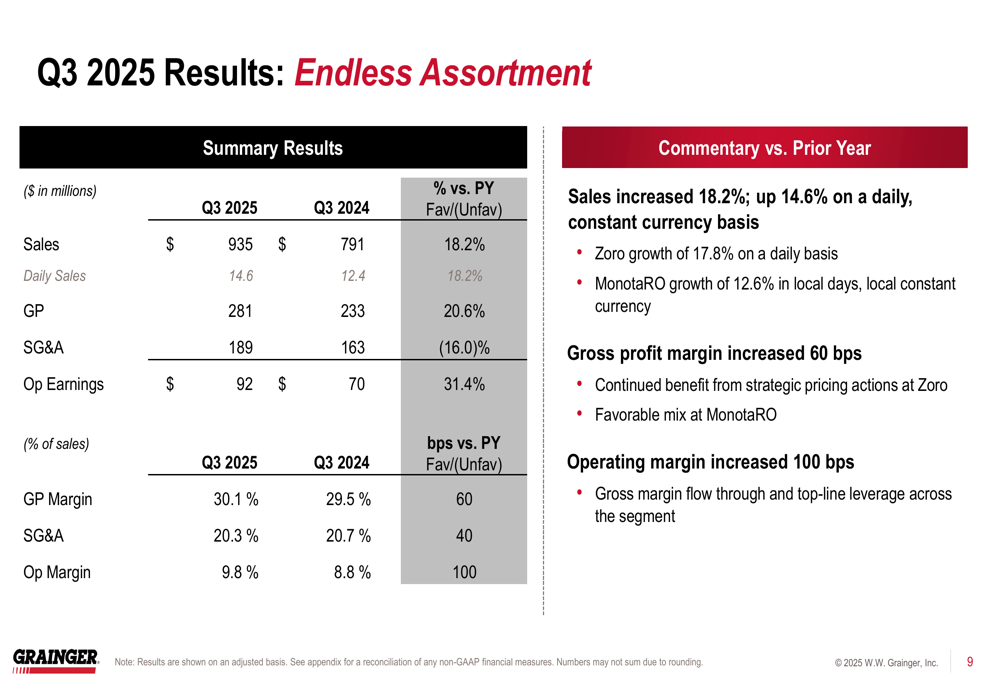

The standout performer was Grainger's Endless Assortment segment, which includes Zoro and MonotaRO. This segment saw impressive sales growth of 18.2% to $935 million, with operating earnings surging 31.4% and operating margin expanding by 100 basis points to 9.8%.

The following chart illustrates the strong performance of the Endless Assortment segment:

"We do think the opportunity is to grow in North America and in Japan with MonotaRO," said D.G. Macpherson, Chairman and CEO, highlighting the company's strategic focus on its highest-growth markets.

Strategic Initiatives

A key strategic announcement in the presentation was Grainger's plan to divest its UK-based Cromwell business. This move aligns with the company's focus on its core North American operations and the high-growth Japanese market through MonotaRO.

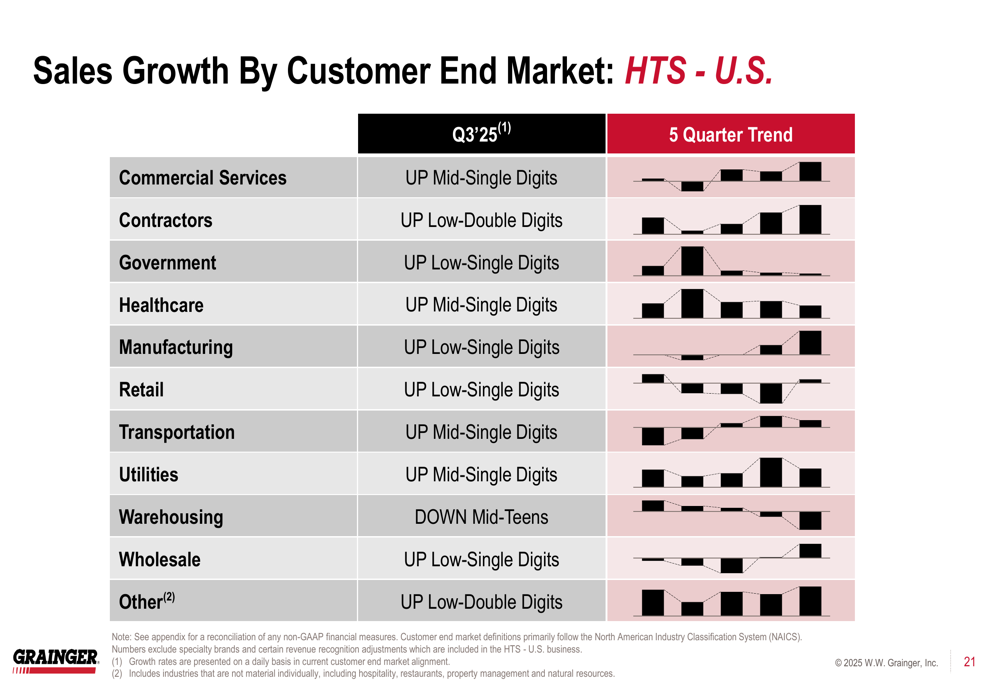

The company's customer end market performance in the High-Touch Solutions U.S. segment showed varied results, with particularly strong growth in the Contractors segment (up low-double digits) and Commercial Services (up mid-single digits). However, the Warehousing segment experienced a significant decline in the mid-teens.

The following breakdown illustrates the performance across different customer end markets:

In the Endless Assortment segment, Grainger continues to expand its digital footprint, with Zoro U.S. reaching 10.8 thousand registered users and approximately 12.8 million active SKUs. MonotaRO achieved approximately 6.1 thousand registered users, demonstrating the segment's growing scale.

Financial Analysis

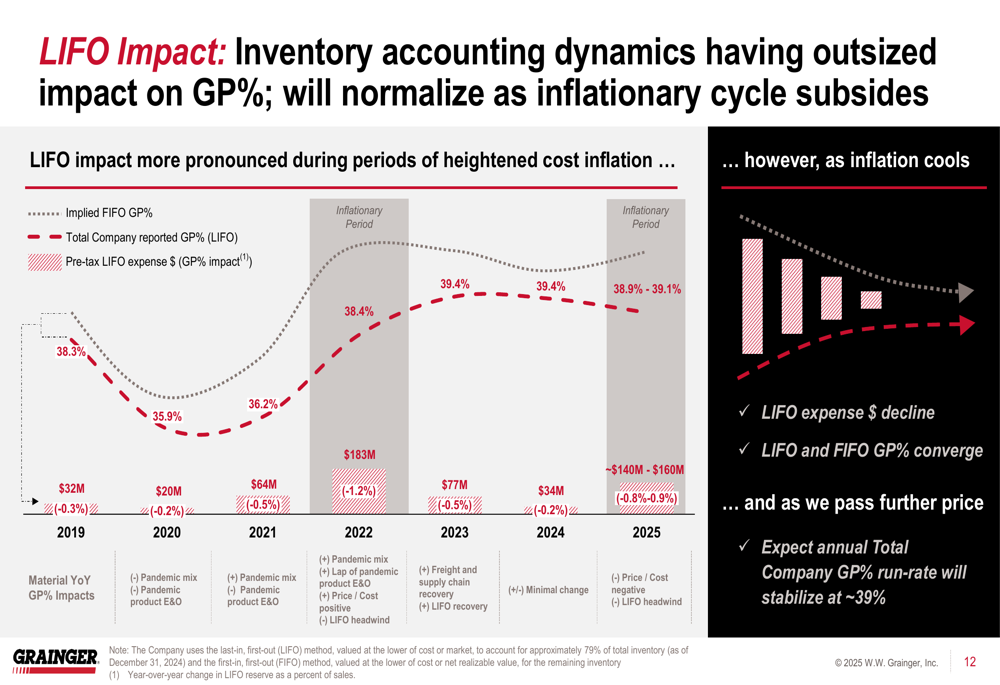

A significant factor affecting Grainger's financial performance has been the impact of tariffs and the resulting LIFO (Last-In, First-Out) accounting effects. The company has taken pricing actions over the past two quarters as tariffs went into effect and continues to engage with suppliers to manage costs.

The following chart explains the LIFO impact on inventory and gross profit margins:

Grainger expects its gross profit margin to stabilize at approximately 39% as the tariff landscape normalizes. The company anticipates a sequential improvement in gross profit percentage in Q4 2025 due to improving price/cost dynamics and normal seasonal favorability.

"We are having very good conversations with our customers," noted CFO Dee Merriwether during the earnings call, suggesting that pricing actions have been well-received despite the challenging environment.

Forward-Looking Statements

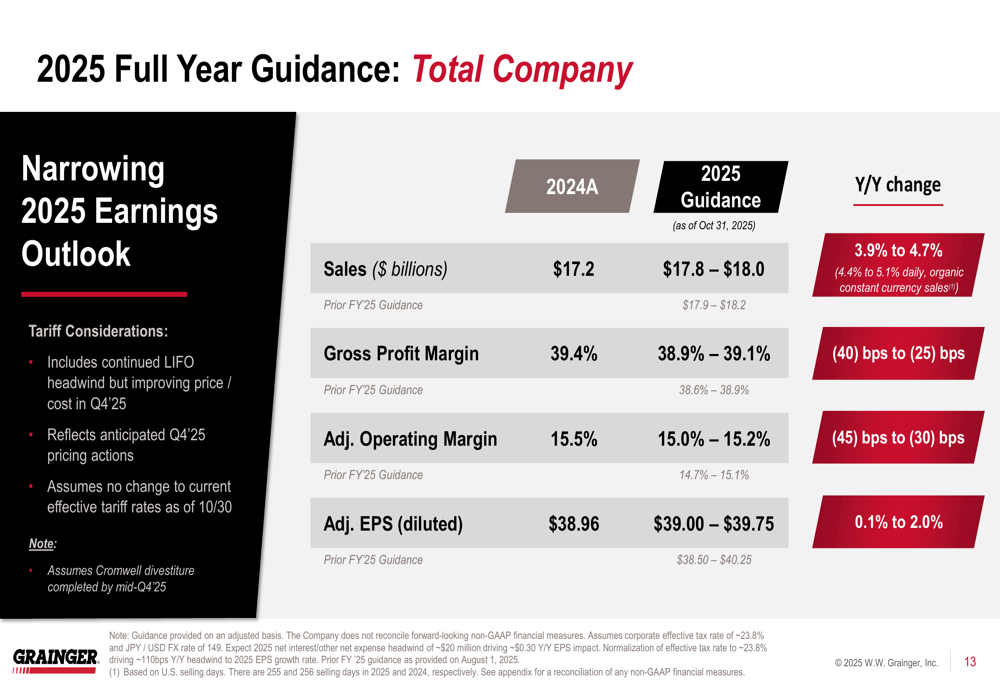

Grainger narrowed its full-year 2025 guidance, projecting sales between $17.8 billion and $18.0 billion, representing year-over-year growth of 3.9% to 4.7%. The company expects adjusted earnings per share between $39.00 and $39.75, reflecting growth of 0.1% to 2.0% compared to 2024.

The detailed 2025 guidance is presented in the following chart:

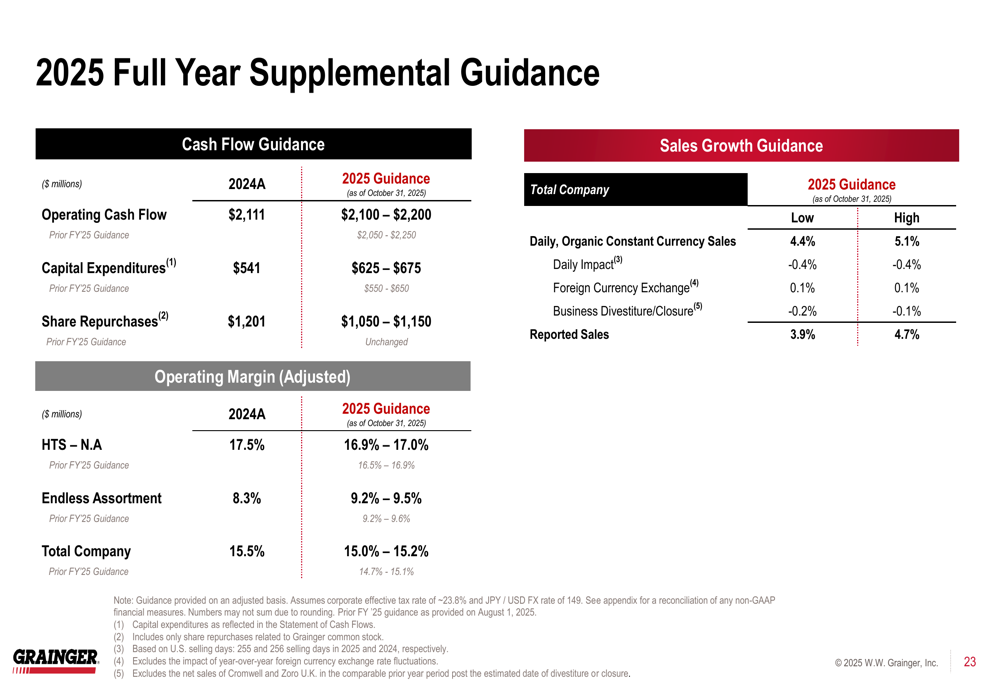

The company also provided supplemental guidance on cash flow and capital allocation:

Grainger expects to generate operating cash flow between $2.1 billion and $2.2 billion for the full year, with capital expenditures ranging from $625 million to $675 million. The company plans to return $1.05 billion to $1.15 billion to shareholders through share repurchases, demonstrating its commitment to shareholder returns despite ongoing investments in growth.

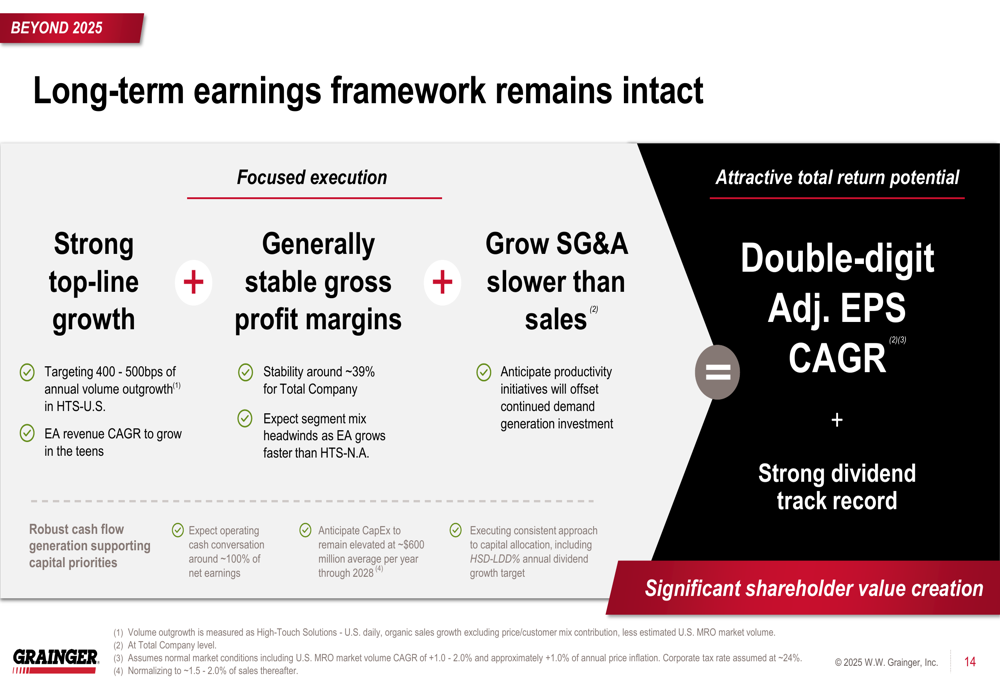

Looking beyond 2025, Grainger maintains its long-term earnings framework, which targets double-digit adjusted EPS compound annual growth rate. The company anticipates capital expenditures to remain elevated at approximately $600 million per year through 2028 as it continues to invest in growth initiatives.

Despite near-term challenges from tariffs and inflation, Grainger's strategic focus on high-growth markets and digital transformation, particularly through its Endless Assortment segment, positions the company well for continued growth in the industrial supply sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.