German construction sector still in recession, civil engineering only bright spot

Xcel Energy Inc (NASDAQ:XEL) reported a substantial increase in second-quarter earnings and reaffirmed its full-year guidance during its Q2 2025 earnings presentation on July 31, 2025. The utility provider demonstrated strong recovery after missing expectations in the first quarter.

Quarterly Performance Highlights

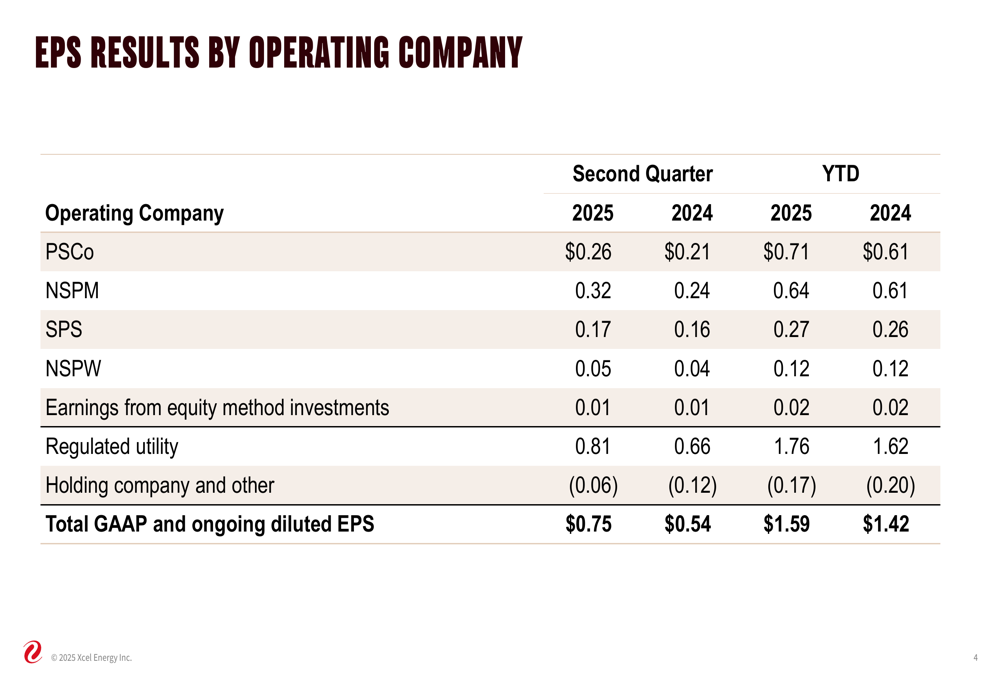

Xcel Energy reported Q2 2025 GAAP earnings per share of $0.75, a 38.9% increase from $0.54 in the same period last year. Year-to-date EPS reached $1.59, up 12% from $1.42 in 2024. The company reaffirmed its full-year EPS guidance of $3.75 to $3.85.

The following chart details the EPS results by operating company, showing improvements across all business segments:

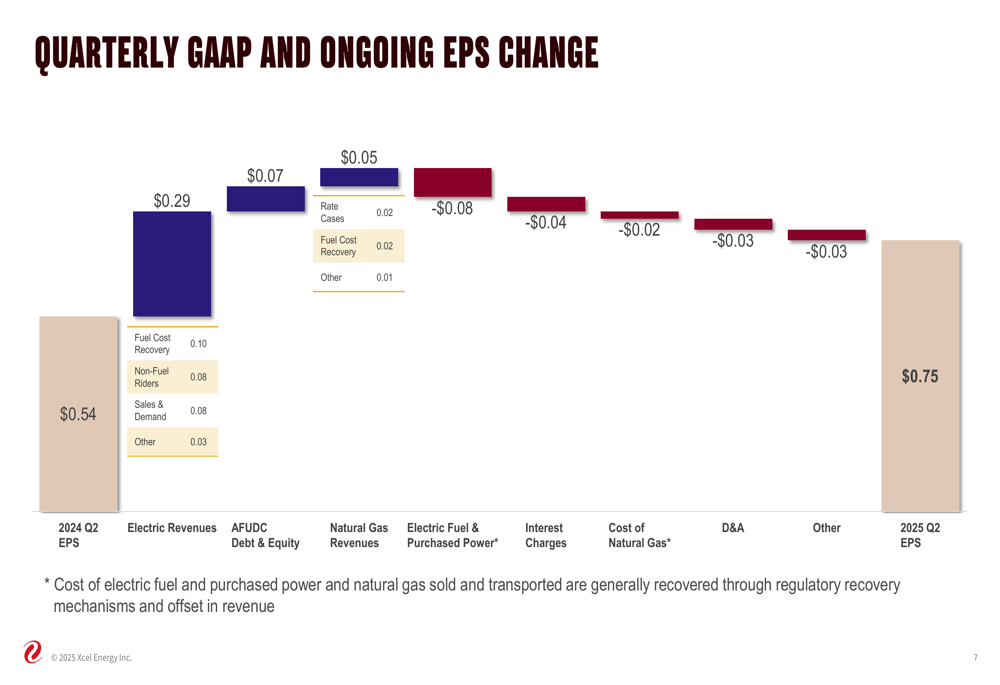

Electric revenues were the primary driver of the quarterly improvement, contributing $0.29 to the EPS increase, while AFUDC debt and equity added another $0.07. These gains were partially offset by decreases in natural gas revenues (-$0.08) and increases in electric fuel and purchased power costs (-$0.04).

As shown in the following waterfall chart illustrating the key factors affecting quarterly EPS performance:

The company reported weather-adjusted retail electric sales growth of 2.7% year-to-date, with SPS (Southwestern Public Service Company) leading the way with 7.3% growth. Customer growth remained steady at approximately 1% across its service territories.

Strategic Initiatives and Capital Investment

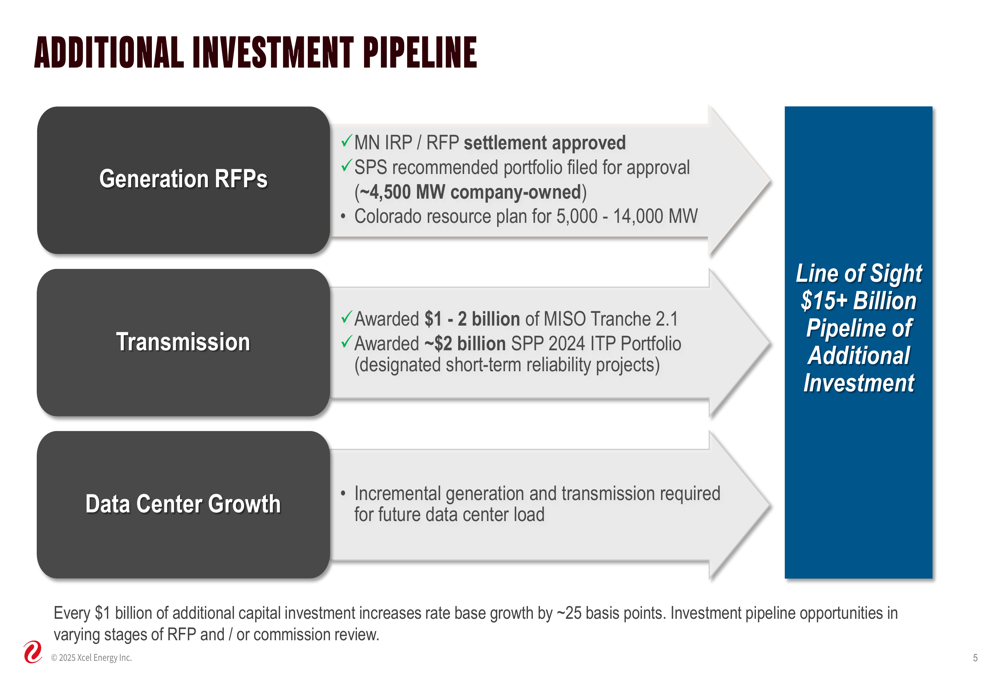

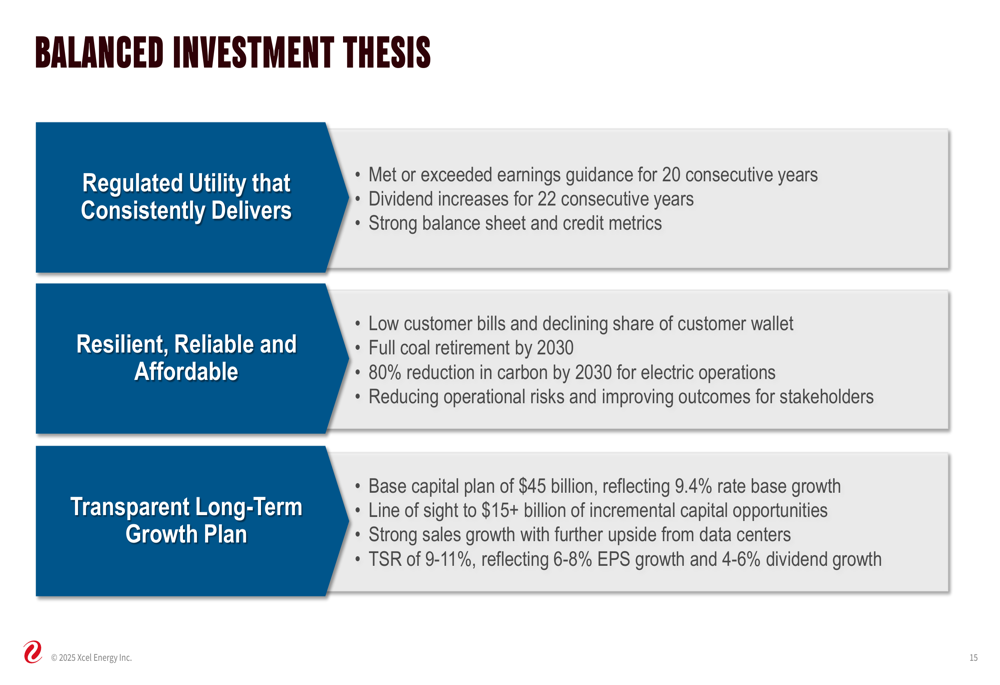

Xcel Energy outlined an ambitious capital investment program, with a base plan of $45 billion reflecting a 9.4% rate base growth. Additionally, the company identified over $15 billion in potential incremental capital opportunities, largely driven by generation and transmission projects to support growing data center demand.

The following slide illustrates the additional investment pipeline opportunities:

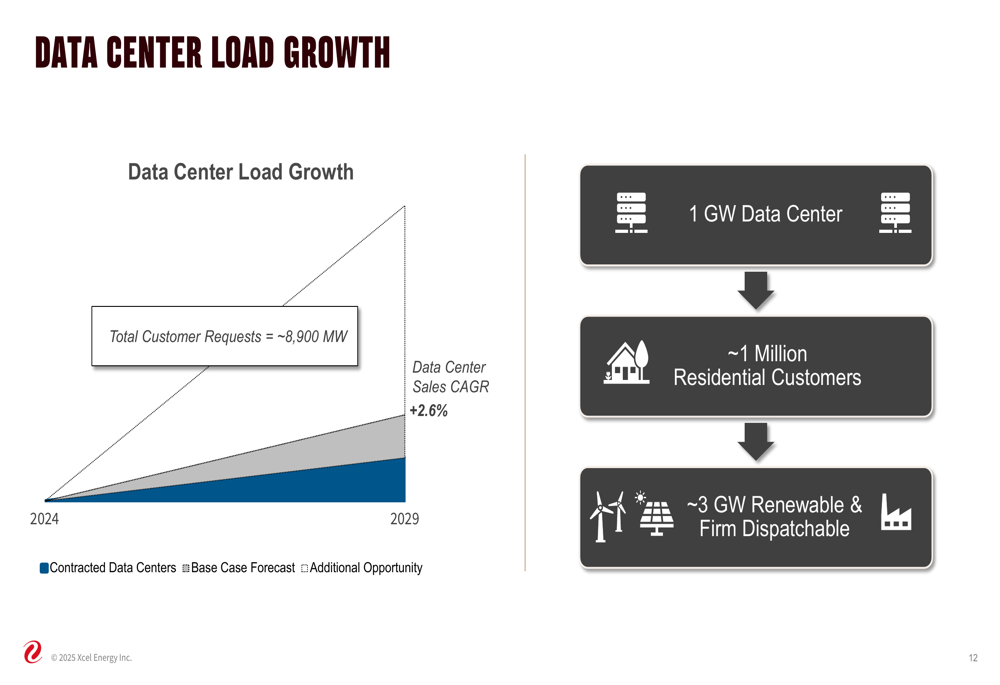

Data center growth represents a significant opportunity for Xcel Energy, with customer requests totaling approximately 8,900 MW. The company noted that a single 1 GW data center requires approximately 3 GW of renewable and firm dispatchable generation capacity.

As shown in the data center load growth illustration:

The company’s resource plan updates include substantial generation capacity additions across its service territories:

- Colorado: Forecasted need of 5,000-14,000 MW of new capacity from 2028 to 2031

- Minnesota: Approximately 4,200 MW of additional resources approved

- SPS: Recommended portfolio of approximately 5,200 MW resources (4,500 MW company-owned)

Regulatory Updates and Risk Management

Xcel Energy reported significant progress in its wildfire risk mitigation efforts, with regulatory approvals in multiple states:

- Colorado commission approval of a settlement for the Colorado Wildfire Mitigation Plan

- Texas commission approval of a settlement for the SPS System Resiliency Plan

- Constructive wildfire legislation passed in Texas and North Dakota

The company also provided updates on ongoing litigation related to the Smokehouse Creek Fire and Marshall Wildfire. For the Smokehouse Creek Fire, Xcel Energy has accrued $290 million and committed $176 million in finalized settlement agreements, with $500 million of insurance coverage. The company noted it "is unable to reasonably estimate an upper end of the loss range."

Forward-Looking Statements and Investment Thesis

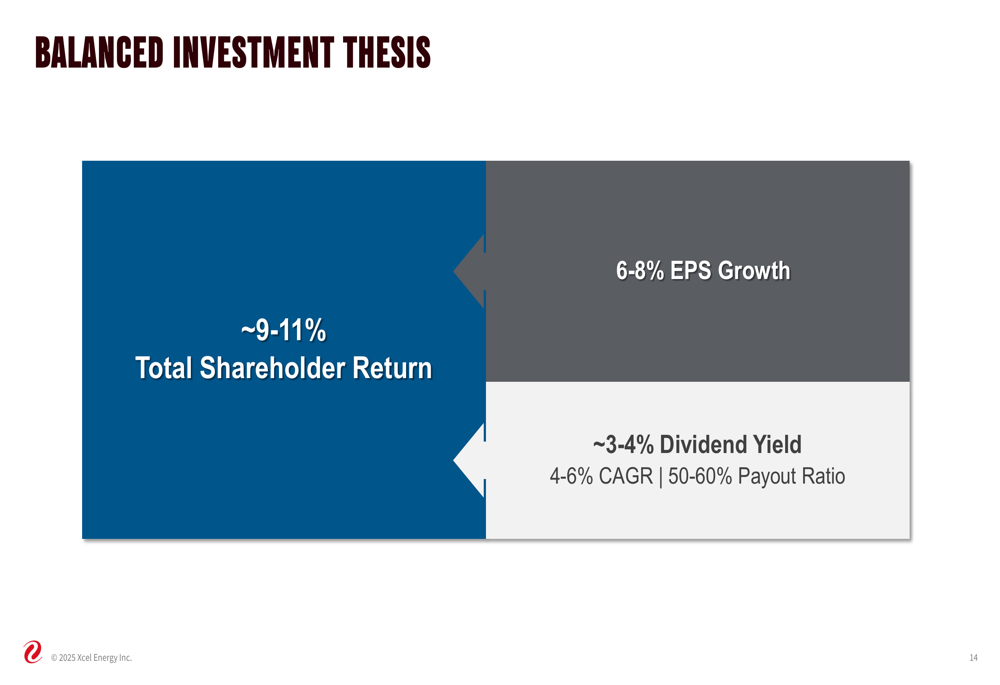

Xcel Energy presented a balanced investment thesis targeting 9-11% total shareholder return, comprised of 6-8% EPS growth and a 3-4% dividend yield (with 4-6% dividend growth and a 50-60% payout ratio).

The company’s investment thesis is illustrated in the following slide:

Management emphasized its track record of meeting or exceeding earnings guidance for 20 consecutive years and increasing dividends for 22 consecutive years. The company also highlighted its efforts to keep customer bills low, with residential electric bills 28% below the national average and natural gas bills 12% below the national average.

The detailed investment thesis is further explained in this comprehensive overview:

Market Context

Xcel Energy’s strong Q2 performance represents a significant recovery after its Q1 2025 results, which showed an EPS of $0.84, falling short of the forecasted $0.93. Despite the Q1 miss, the company’s reaffirmation of its full-year guidance suggests confidence in its ability to execute its strategic plans.

The stock closed at $72.39 on July 30, 2025, near the upper end of its 52-week range of $56.69 to $73.56, indicating investor confidence in the company’s long-term prospects despite the earlier earnings miss. With a market capitalization of approximately $40.41 billion, Xcel Energy continues to position itself as a leader in the clean energy transition while maintaining strong financial performance.

Key assumptions for the 2025 outlook include weather-adjusted retail electric sales growth of approximately 3%, capital riders (net of PTCs) increasing $255-265 million, and O&M expenses increasing by approximately 4%. The company also anticipates increases in depreciation expense ($210-220 million), property taxes ($45-55 million), and interest expense ($160-170 million).

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.