Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Introduction & Market Context

Xometry Inc (NASDAQ:XMTR), a leading digital manufacturing marketplace, presented its Q3 2025 earnings on November 4, 2025, revealing robust growth across key metrics. The company’s shares surged 15.03% following the announcement, reaching $55.87, approaching its 52-week high of $58.03.

The presentation highlighted Xometry’s continued momentum in digitizing manufacturing processes through its AI-powered marketplace platform, which connects buyers with a global network of suppliers. The company’s transition to positive Adjusted EBITDA marks a significant milestone in its growth trajectory.

Quarterly Performance Highlights

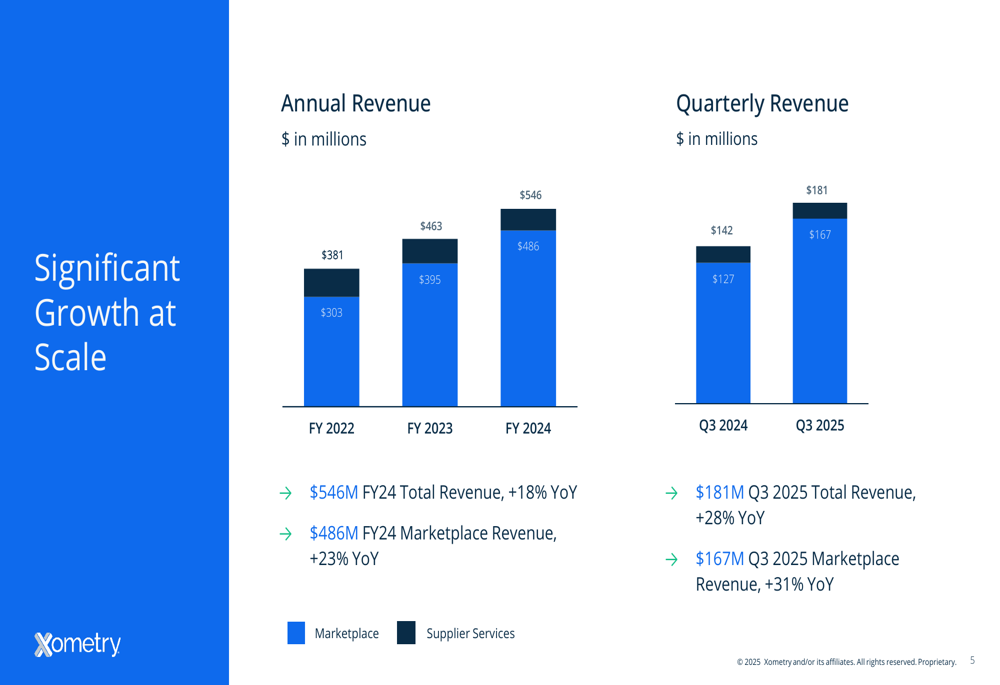

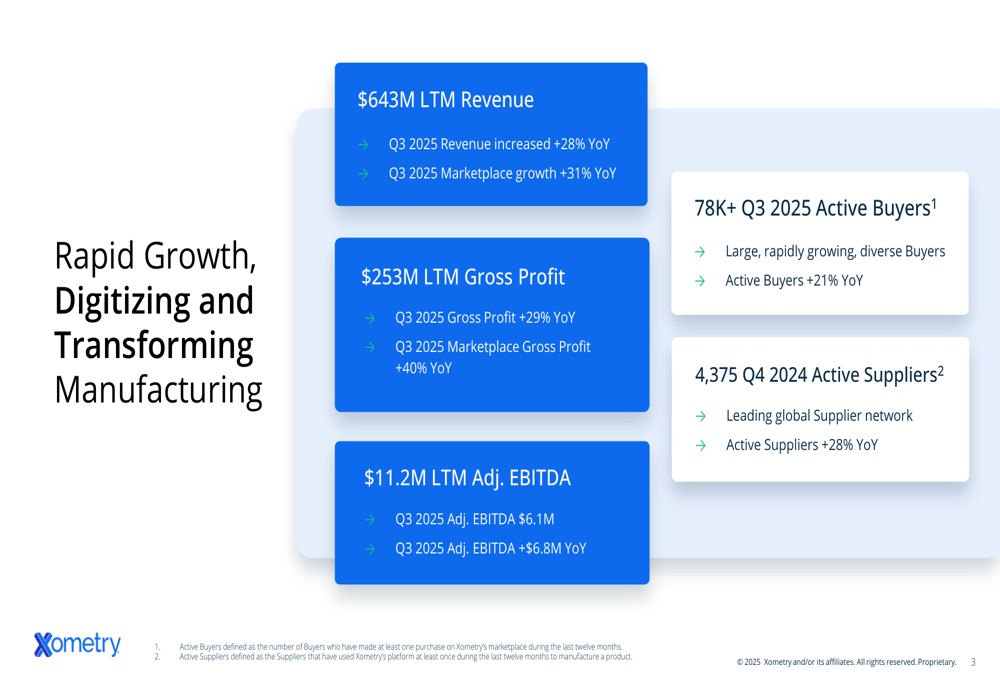

Xometry reported record Q3 2025 revenue of $181 million, representing a 28% year-over-year increase, driven primarily by 31% growth in its core marketplace business. The company also posted record gross profit of $72 million, up 29% compared to the same period last year.

As shown in the following chart of quarterly revenue growth:

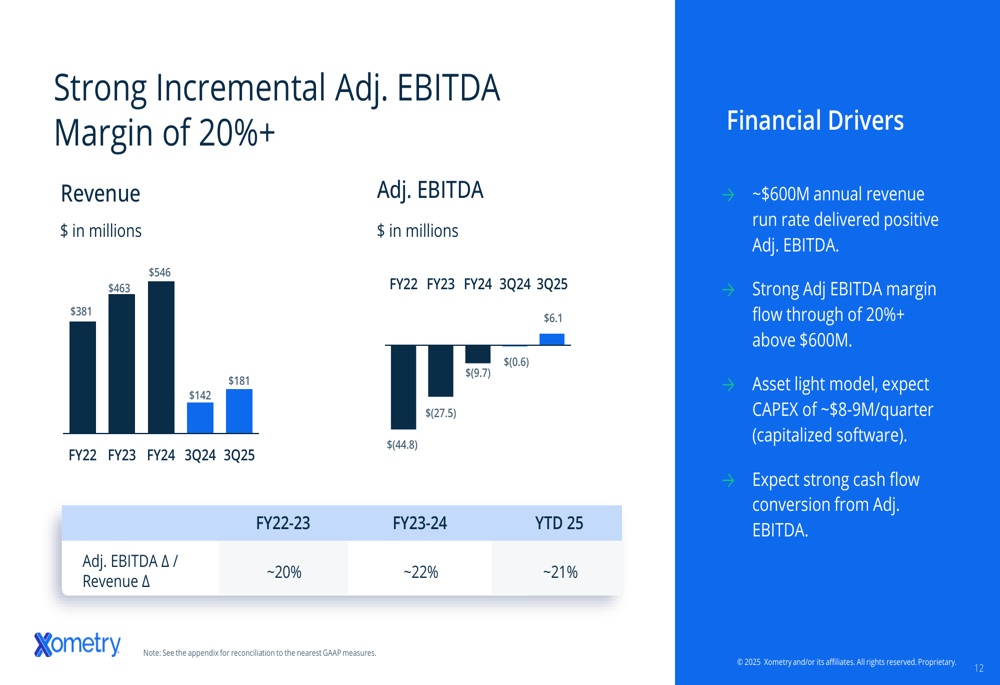

Notably, Xometry achieved positive Adjusted EBITDA of $6.1 million in Q3 2025, a substantial improvement of $6.8 million compared to the $0.6 million loss reported in Q3 2024. This represents 3.4% of revenue, demonstrating the company’s progress toward sustainable profitability.

The company’s key financial metrics show consistent improvement across multiple dimensions:

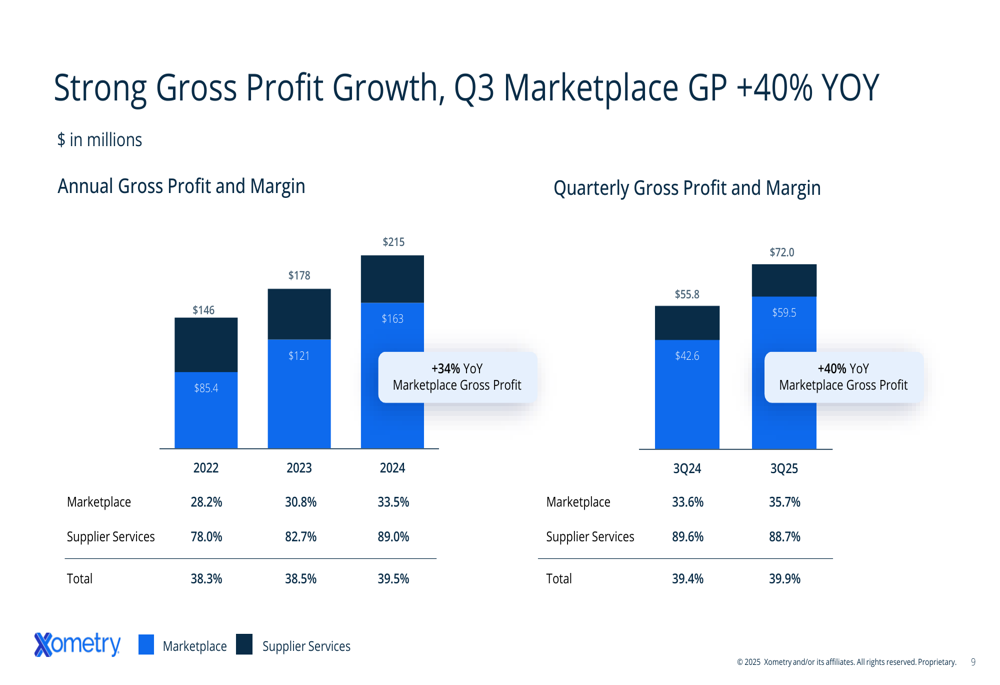

Marketplace gross margin expanded to 35.7% in Q3 2025, an increase of 210 basis points year-over-year, which the company attributes to its AI-powered pricing and selection capabilities. Meanwhile, supplier services maintained a strong gross margin of 88.7%, primarily through Thomas core advertising.

The following chart illustrates Xometry’s gross profit growth trajectory:

Marketplace Growth and Expansion

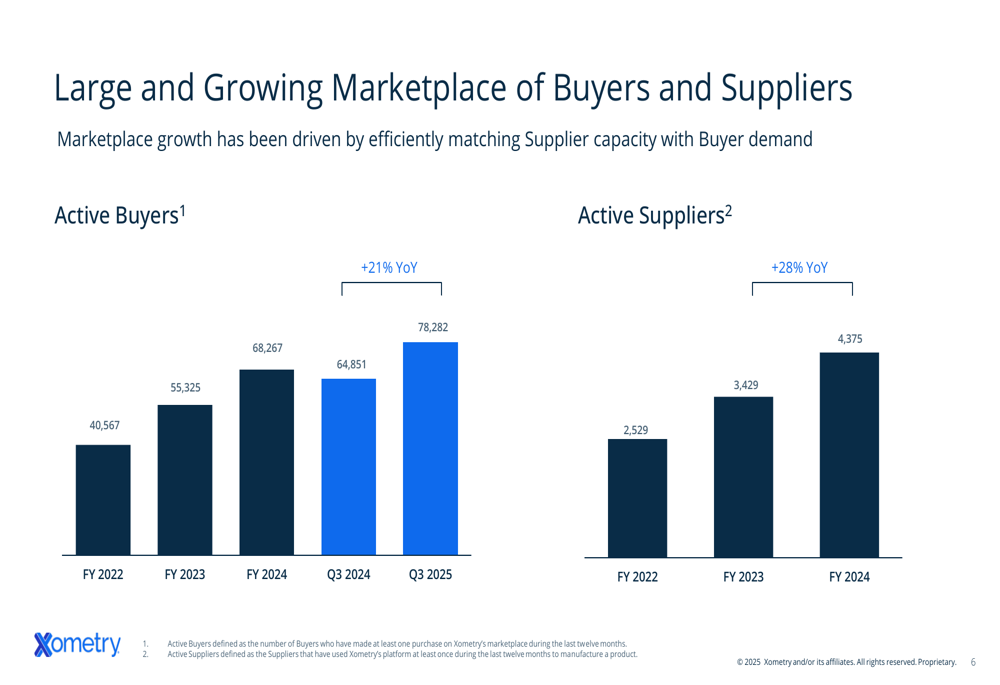

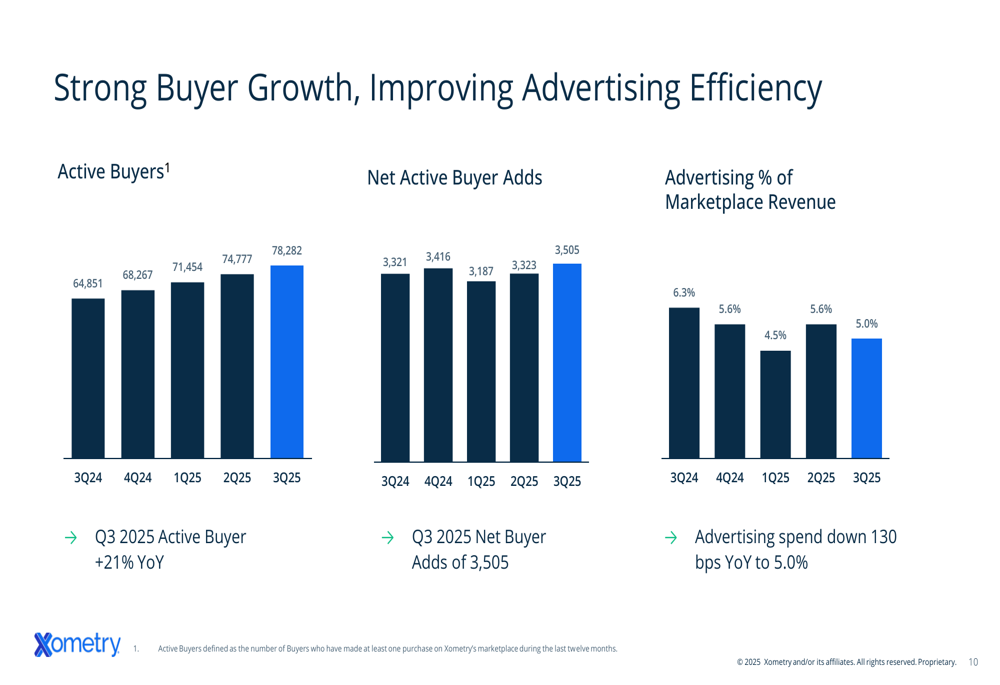

Xometry’s marketplace continues to show strong network effects, with active buyers increasing 21% year-over-year to 78,282 in Q3 2025. The company also reported 28% year-over-year growth in active suppliers to 4,375 for fiscal year 2024.

This expanding network is visualized in the following chart:

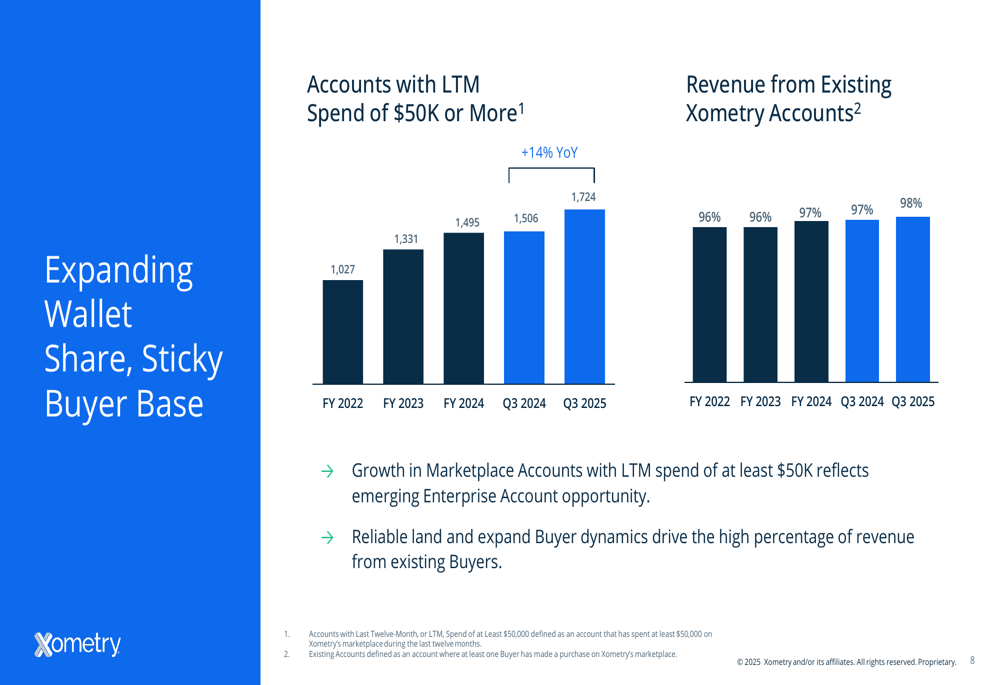

The company is successfully increasing wallet share from existing customers, with accounts spending over $50,000 in the last twelve months growing 14% year-over-year to 1,724 in Q3 2025. Even more impressive, 98% of Q3 2025 revenue came from existing accounts, demonstrating strong customer retention and expanding relationships.

The following chart shows Xometry’s success in expanding customer wallet share:

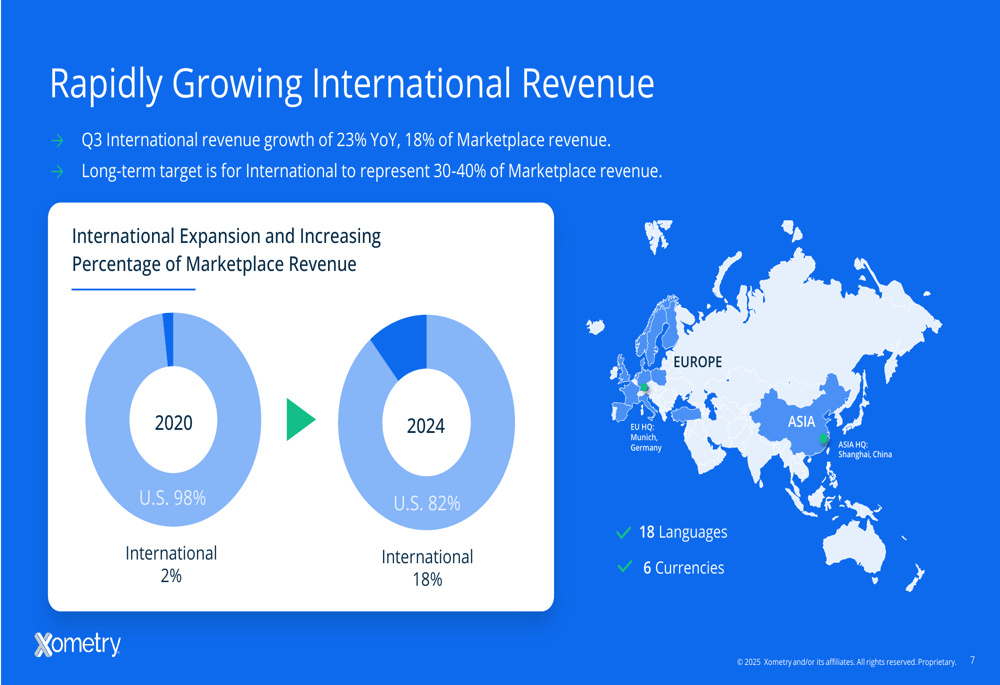

International expansion remains a key growth driver, with international revenue increasing 23% year-over-year and now representing 18% of marketplace revenue. The company has established headquarters in Munich, Germany for European operations and Shanghai, China for Asia Pacific, supporting transactions in 18 languages and 6 currencies.

As illustrated in the following geographic breakdown:

Strategic Initiatives and Outlook

Xometry highlighted several strategic initiatives driving its growth, including increased enterprise penetration, Teamspace adoption, and the launch of new capabilities such as the Workcenter mobile app and Injection Molding Auto Quoting. The company has enhanced its AI-powered Design for Manufacturing (DFM) capabilities and implemented a new Thomas advertising model with dynamic ad serving technology.

Operational efficiency continues to improve, with advertising spend as a percentage of marketplace revenue decreasing 130 basis points year-over-year to 5.0% in Q3 2025, while still adding 3,505 net new active buyers during the quarter.

The following chart demonstrates Xometry’s improving advertising efficiency:

The company is also showing strong operating leverage, with non-GAAP operating expenses as a percentage of revenue decreasing across all categories. Total non-GAAP operating expenses declined to 36.6% of revenue in Q3 2025, down from 40.0% in Q3 2024.

Financial Outlook

Xometry raised its full-year 2025 guidance, now expecting revenue between $676-678 million and Adjusted EBITDA of $16-17 million. For Q4 2025, the company forecasts revenue of $182-184 million, representing 23-24% growth year-over-year, and Adjusted EBITDA of $6-7 million.

The company emphasized its path to achieving $1 billion in revenue with a target of 20% incremental Adjusted EBITDA margins. This financial trajectory is illustrated in the following chart:

CEO Randy Altschuler stated during the earnings call, "We are proving that a superior experience for both buyers and suppliers, fueled by the power of marketplace dynamics, is delivering sustainable growth and value." CFO James Milne added, "As we scale towards $1 billion of revenue, we expect to deliver improving profitability even as we continue to invest in our growth initiatives."

With its asset-light marketplace model, low capital expenditure requirements, and improving cash flow conversion, Xometry appears well-positioned to continue its growth trajectory while progressing toward sustainable profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.