Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Yara International ASA (OTC:YARIY) (OB:YAR) presented its first quarter 2025 results on April 25, showcasing a significant financial improvement amid favorable market conditions. The Norwegian fertilizer giant reported a substantial increase in earnings, driven by strong volumes, improved price realization, and successful cost reduction initiatives.

The company operates in a nitrogen market that has become increasingly demand-driven, with prices maintaining levels above historical averages. Yara’s global scale in ammonia production and its flexible European asset network have positioned the company to capitalize on these market dynamics.

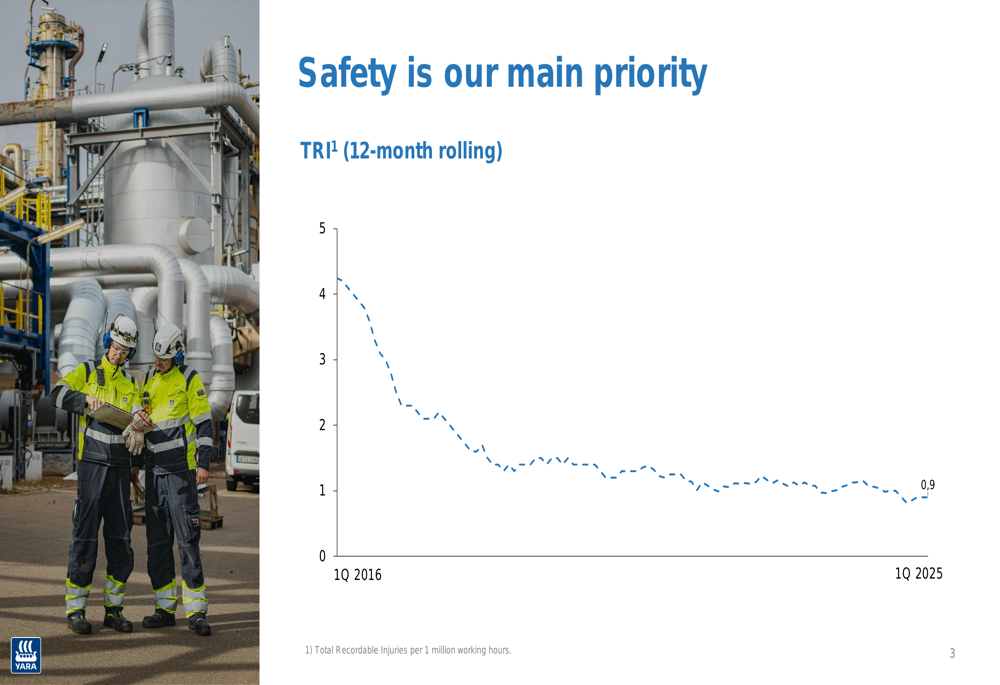

As shown in the following chart highlighting the company’s safety performance, Yara continues to prioritize workplace safety with its Total (EPA:TTEF) Recordable Injuries rate showing consistent improvement over the past decade:

Quarterly Performance Highlights

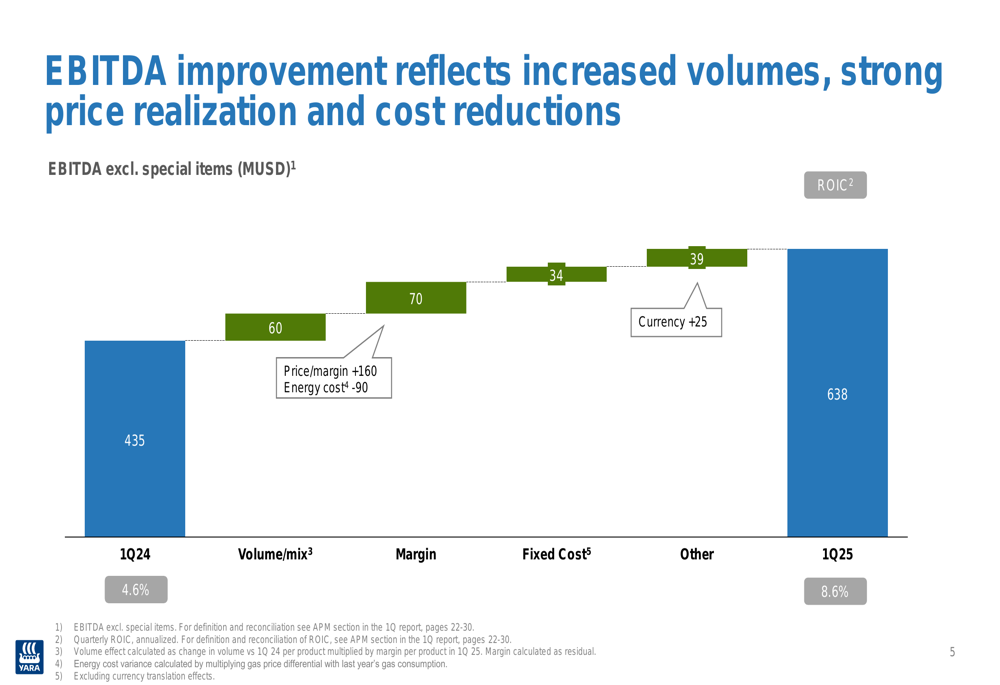

Yara delivered exceptional financial results in Q1 2025, with EBITDA excluding special items increasing by 47% to $638 million compared to $435 million in Q1 2024. This performance was underpinned by strong deliveries and margins across most business segments.

Earnings per share excluding currency and special items rose dramatically from $0.21 to $1.01 per share, while Return On Invested Capital (ROIC) improved from 2.5% to 6.0%. Cash from operations increased substantially from $58 million to $329 million year-over-year.

The company’s strong performance was driven by several key factors as outlined in this overview slide:

A detailed breakdown of the EBITDA improvement reveals that volume/mix contributed positively by $60 million, while margin effects added $70 million after accounting for price improvements and energy costs. Currency impact and other factors provided additional positive contributions of $25 million and $39 million respectively.

Detailed Financial Analysis

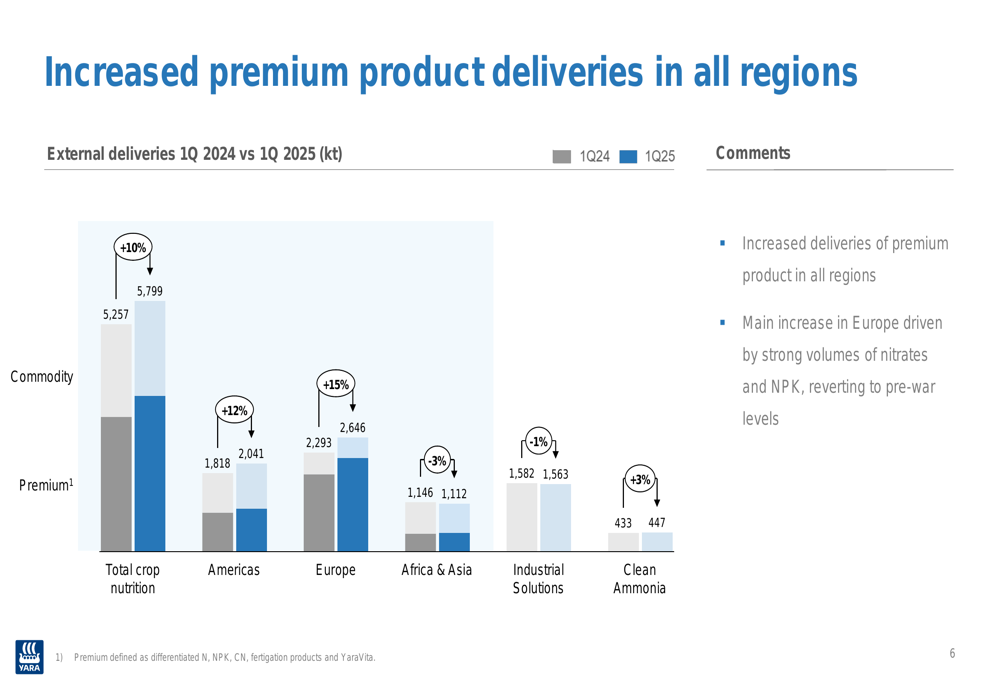

Yara reported increased premium product deliveries across all regions, with total crop nutrition deliveries up 10% compared to Q1 2024. The Americas region saw a 12% increase, while Europe experienced a substantial 15% growth. The company’s premium products, which include differentiated nitrogen products, NPK, CN, fertigation products, and YaraVita, showed particularly strong performance.

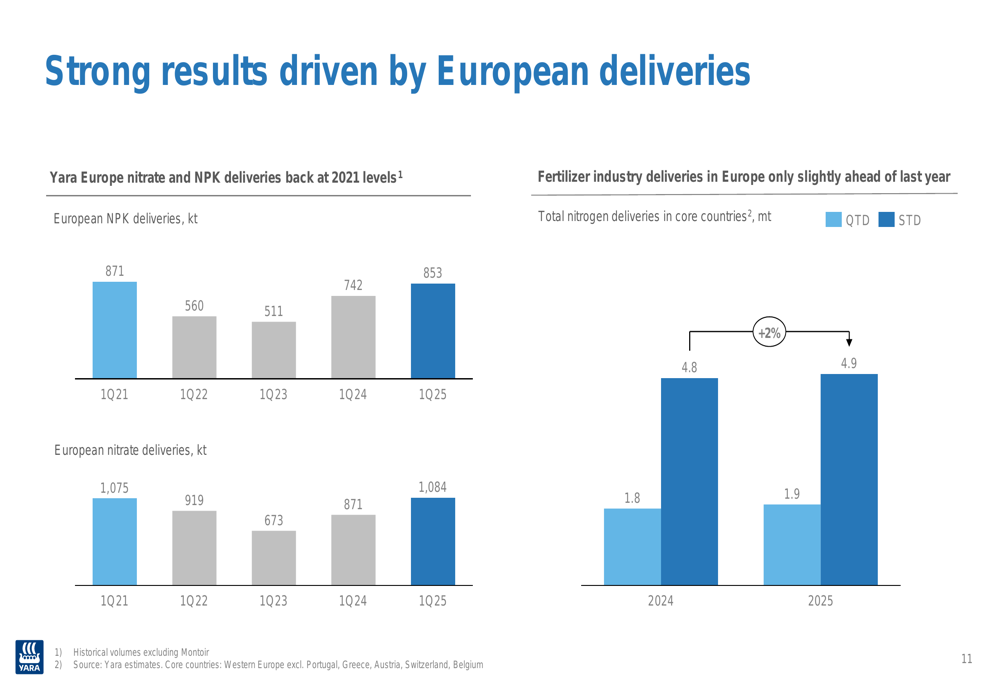

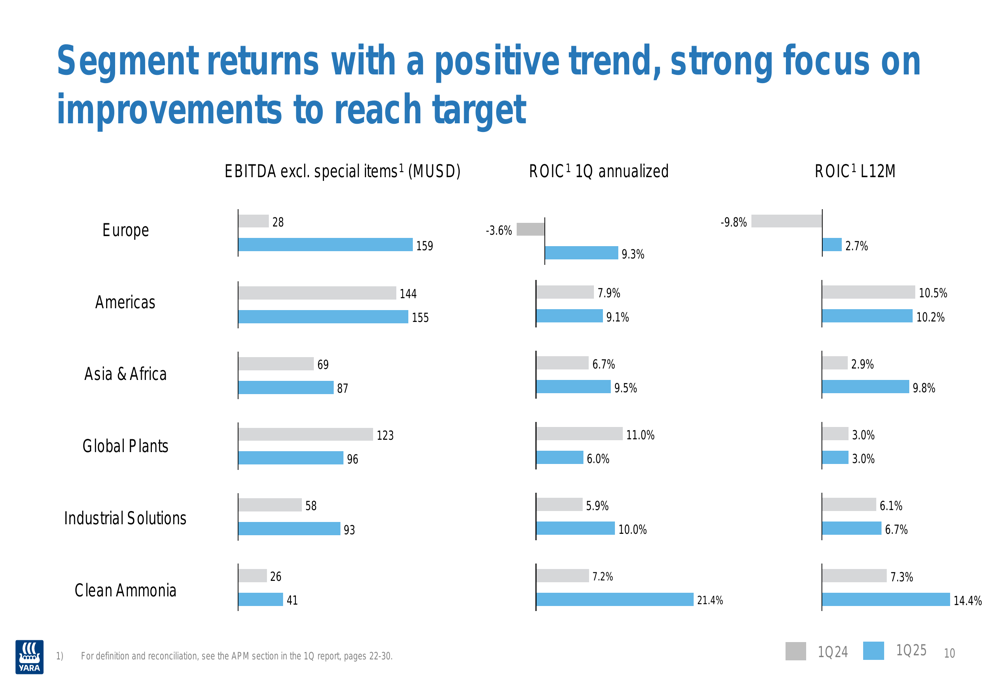

The European market showed a remarkable recovery, with nitrate and NPK deliveries returning to pre-war (2021) levels. This recovery was a significant driver of Yara’s improved financial performance, with the Europe segment’s EBITDA increasing from $28 million to $159 million and its ROIC improving from -3.6% to 9.3%.

Segment performance across the company showed a generally positive trend. The Clean Ammonia segment demonstrated the highest ROIC at 21.4%, up from 7.2% in Q1 2024. Industrial Solutions also performed well, with EBITDA increasing from $58 million to $93 million and ROIC improving from 5.9% to 10.0%.

Strategic Initiatives

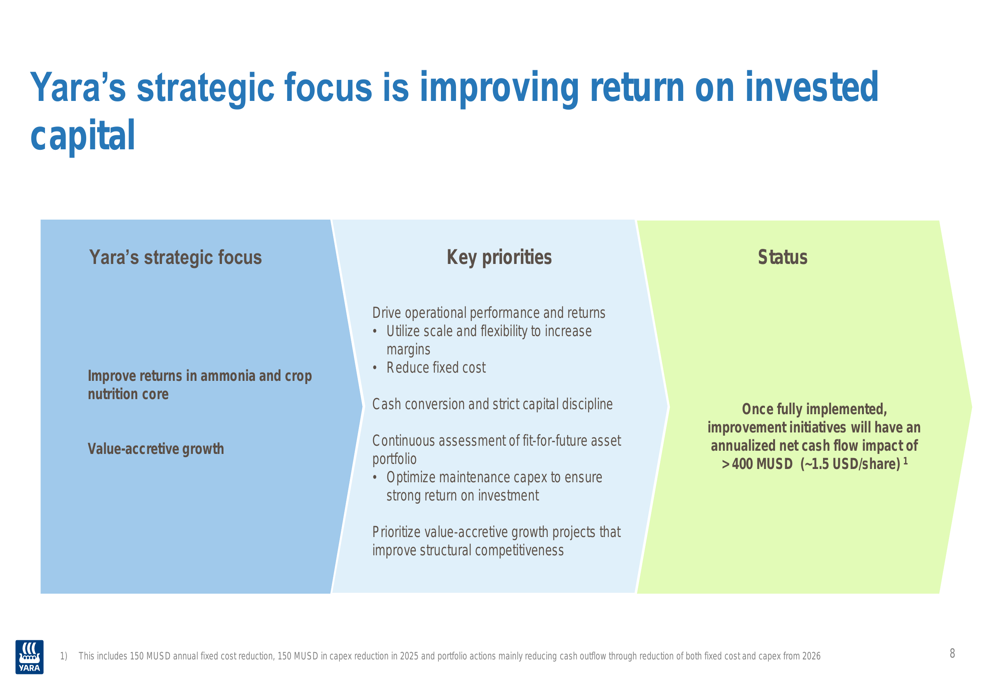

Yara’s strategic focus centers on improving return on invested capital through three key priorities: improving returns in ammonia and crop nutrition core business, pursuing value-accretive growth, and optimizing the company’s portfolio. The company expects these improvement initiatives, once fully implemented, to deliver an annualized net cash flow impact exceeding $400 million.

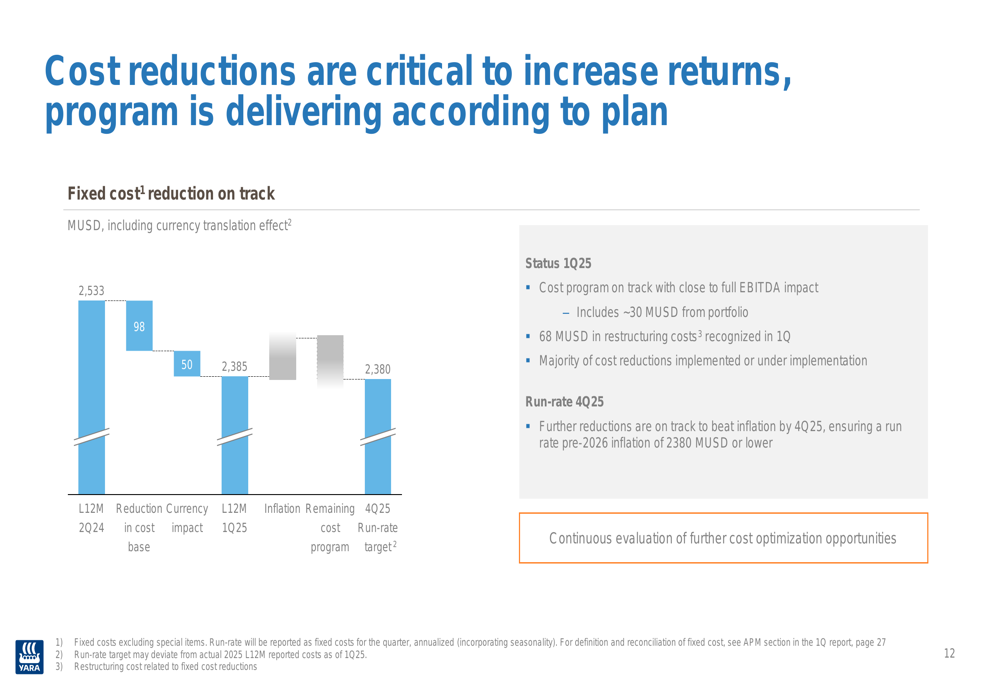

Cost reduction efforts are progressing according to plan, with fixed costs excluding special items reduced to $2,385 million (last 12 months) from $2,533 million, including currency translation effects. The company recognized $68 million in restructuring costs in Q1 2025 as part of this program. Management indicated that the majority of cost reductions have been implemented or are under implementation, with further reductions on track to beat inflation by Q4 2025.

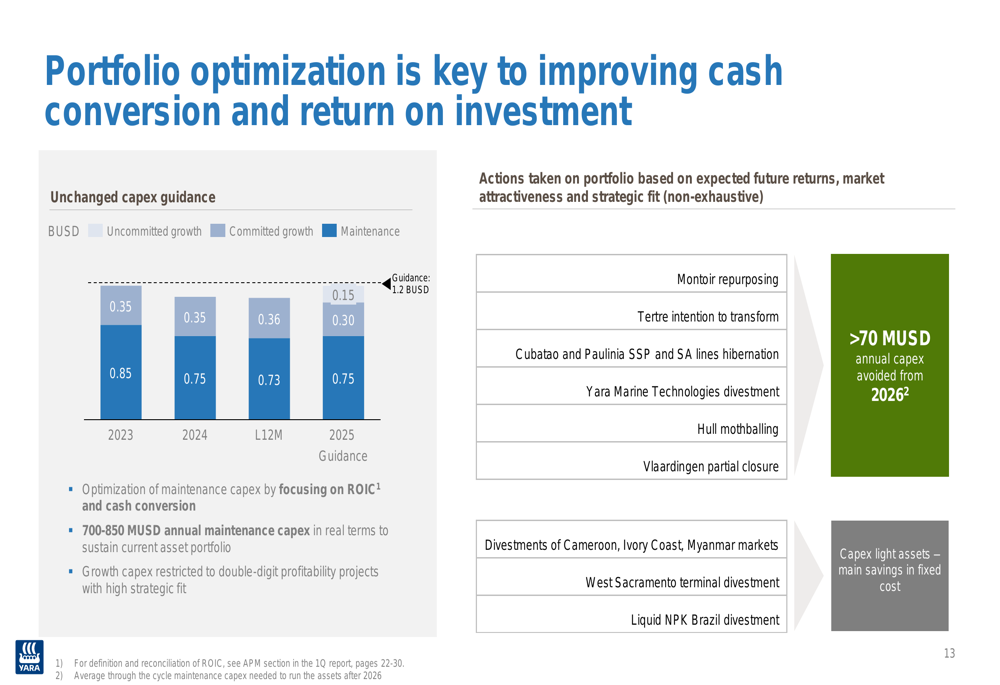

Portfolio optimization remains a key strategic focus for improving cash conversion and return on investment. Yara has maintained its capital expenditure guidance at $1.2 billion for 2025, while implementing various portfolio actions based on expected future returns, market attractiveness, and strategic fit. These actions include repurposing the Montoir facility, transforming Tertre, hibernating certain production lines, and divesting non-core assets.

Forward-Looking Statements

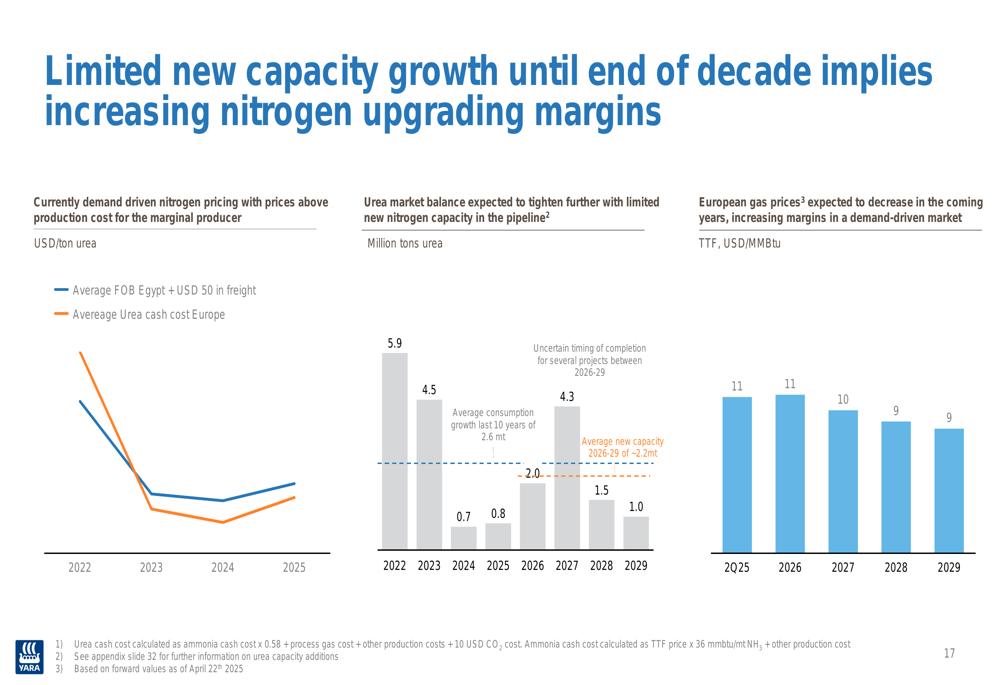

Yara’s outlook remains positive, with management highlighting stronger nitrogen fundamentals and limited new capacity growth until the end of the decade. This supply-demand dynamic is expected to support nitrogen upgrading margins in the medium term.

The company’s European nitrate plants are well-positioned to manage energy volatility, with high flexibility in ammonia imports. Additionally, Yara expects European gas prices to decrease in coming years, which could further enhance margins in a demand-driven market.

Regulatory developments, including the Carbon Border Adjustment Mechanism (CBAM) and Emissions Trading System (ETS), are likely to lift urea prices in Europe, potentially triggering increased nitrate and NPK margins, particularly when upgraded from low-carbon ammonia.

Yara’s global scale in ammonia production underpins its flexibility and value creation potential, particularly in upstream US projects. The company positions itself as the only player able to offtake a new ammonia project at sufficient scale, creating potential for significant shareholder value through equity investments in US ammonia production.

With its strategic initiatives progressing as planned and favorable market fundamentals, Yara appears well-positioned to continue its positive performance trajectory through 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.