Can anything shut down the Gold rally?

Introduction & Market Context

Ziff Davis, Inc. (NASDAQ:ZD) reported its first quarter 2025 financial results on May 8, 2025, showing overall revenue growth despite continued challenges with organic expansion. The digital media and internet company’s stock rose 3% in after-hours trading to $33.35, though it remains well below its 52-week high of $60.62.

The results come after a mixed fourth quarter 2024, when the company beat earnings expectations but missed revenue forecasts, leading to a significant stock decline. CEO Vivek Shah had previously highlighted a "meaningful disconnect" between the company’s market value and its fundamentals.

Quarterly Performance Highlights

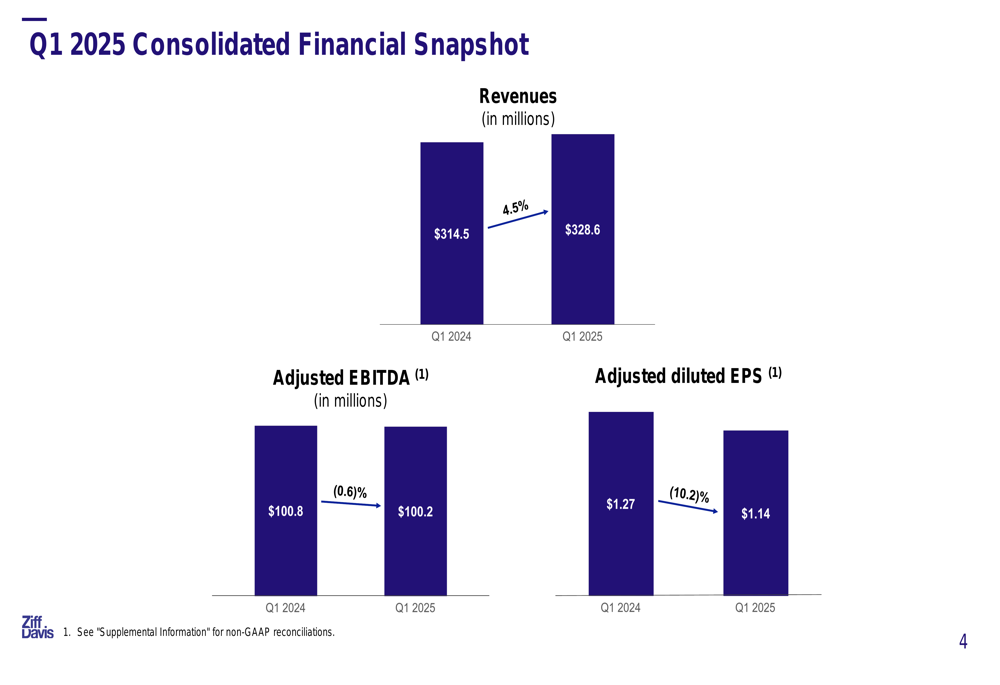

Ziff Davis reported Q1 2025 revenue of $328.6 million, a 4.5% increase from $314.5 million in the same period last year. However, profitability metrics showed some weakness, with adjusted EBITDA slightly decreasing by 0.6% to $100.2 million and adjusted diluted EPS falling 10.2% to $1.14.

As shown in the following consolidated financial snapshot:

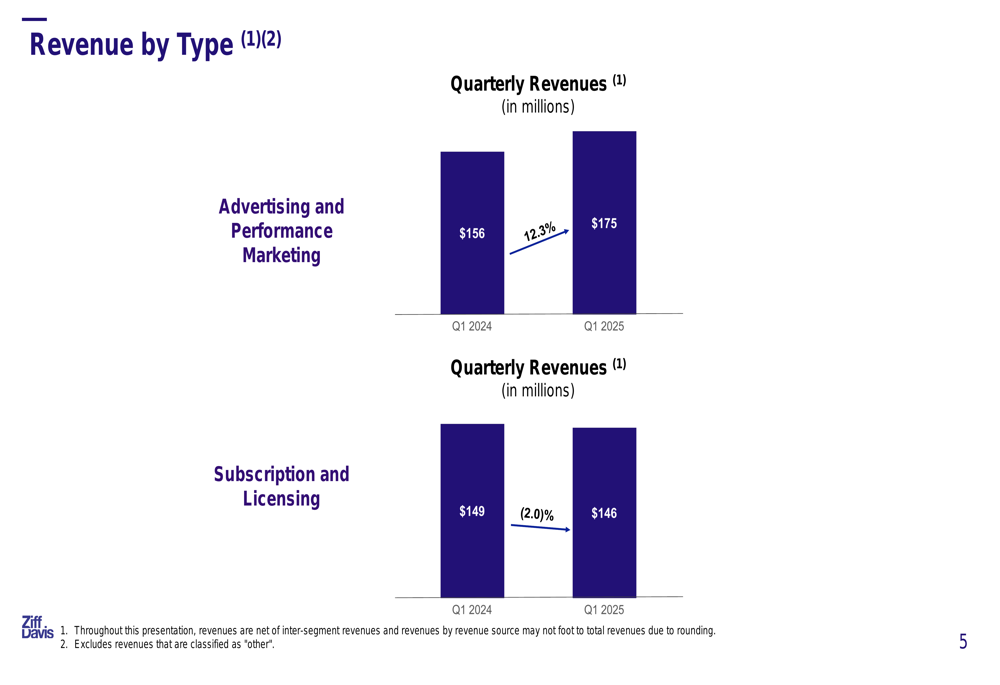

The company’s revenue growth was primarily driven by its advertising and performance marketing business, which increased 12.3% year-over-year to $175 million. Meanwhile, subscription and licensing revenue declined 2.0% to $146 million.

This revenue breakdown by type illustrates the divergence between these two business models:

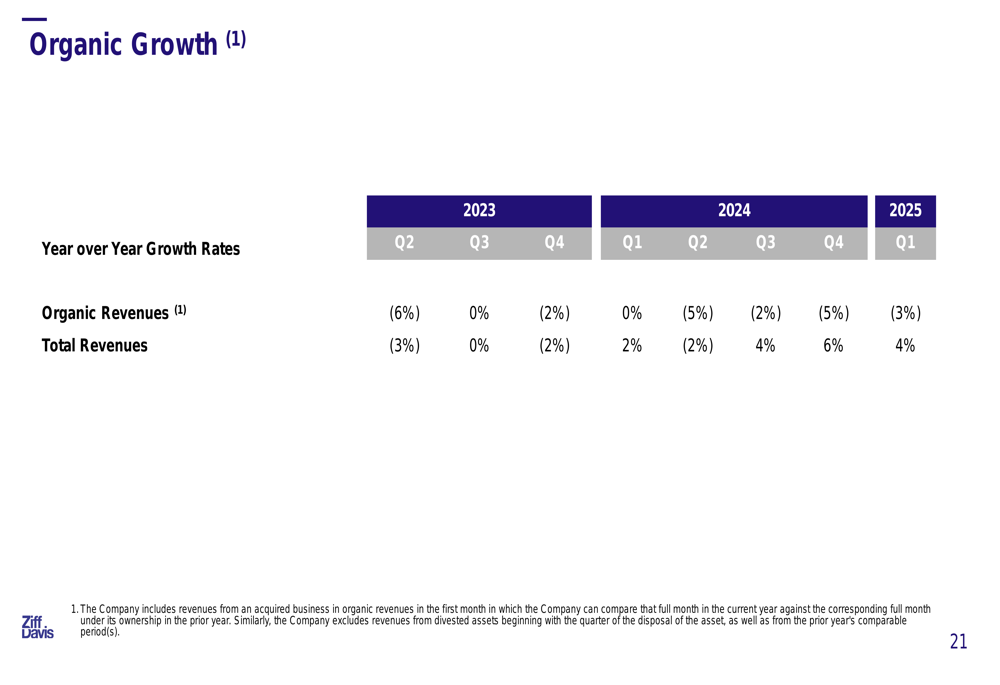

Despite the overall revenue growth, Ziff Davis continues to face challenges with organic growth, which remained negative at -3% for Q1 2025. This suggests that acquisitions, rather than internal expansion, are driving the company’s top-line growth.

The following chart illustrates the company’s organic growth trend over the past eight quarters:

Segment Performance Analysis

Ziff Davis’s performance varied significantly across its five business segments:

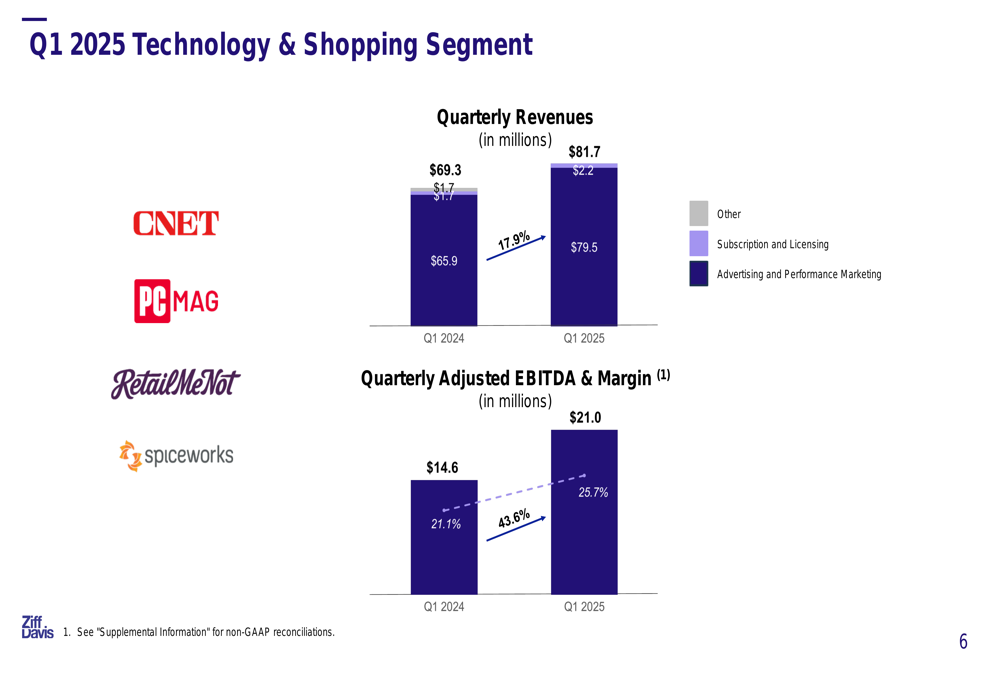

The Technology & Shopping segment was the standout performer, with revenue increasing 17.9% to $81.7 million and adjusted EBITDA margin expanding to 25.7%. This segment, which includes brands like CNET and RetailMeNot, showed strong growth in both customer metrics and revenue per customer.

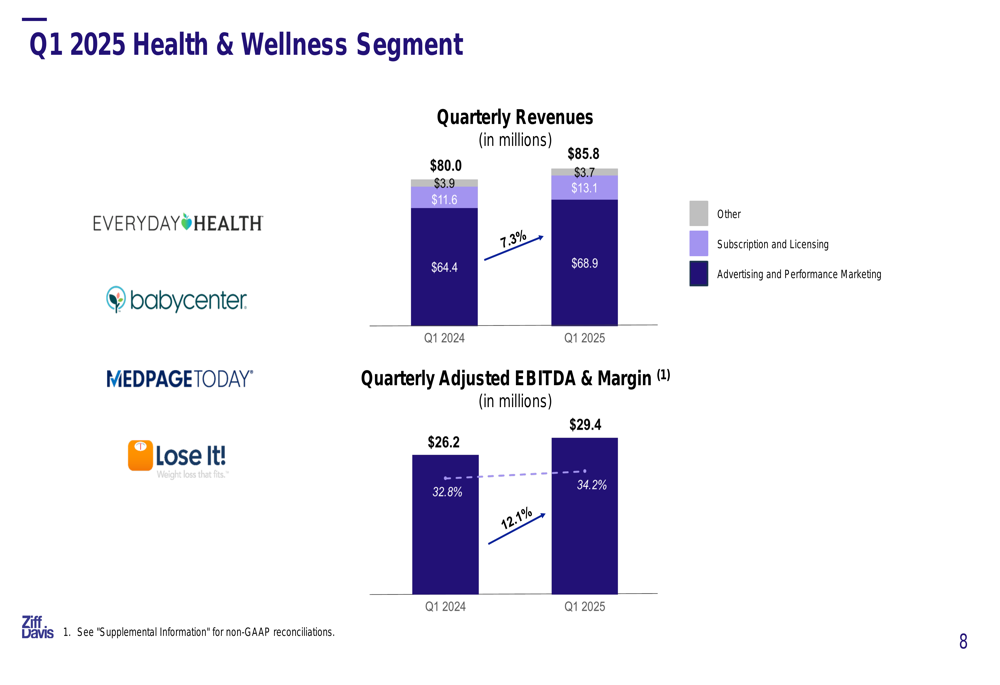

The Health & Wellness segment also performed well, with revenue growing 7.3% to $85.8 million and adjusted EBITDA increasing 12.1% to $29.4 million. This segment includes properties like Everyday Health and BabyCenter.

In contrast, the Cybersecurity & Martech segment showed significant weakness, with revenue declining 10.8% to $67.3 million and adjusted EBITDA falling 25.2% to $22.2 million. This underperformance represents a concerning trend for what has historically been a high-margin business for the company.

The Gaming & Entertainment segment (including IGN and Humble Bundle) saw modest revenue growth of 3.8% to $38.0 million, though adjusted EBITDA margin declined to 31.9%. The Connectivity segment (Ookla and Downdetector) grew revenue by 5.0% to $55.8 million while maintaining strong EBITDA margins above 50%.

Financial Position and Capital Structure

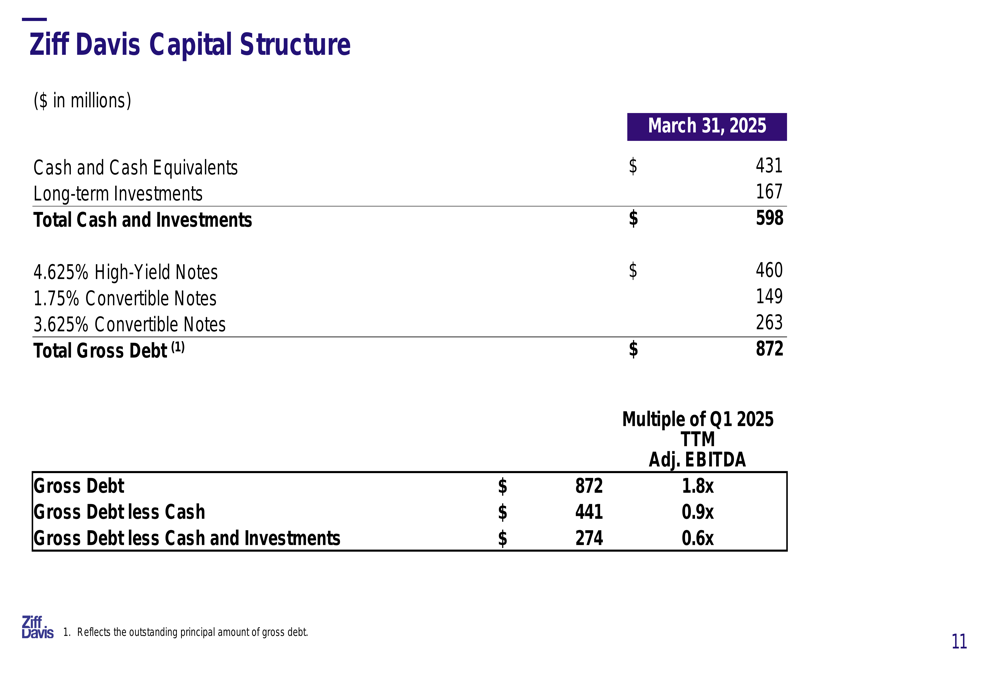

Ziff Davis maintained a strong balance sheet as of March 31, 2025, with $431 million in cash and cash equivalents and $167 million in long-term investments. The company’s total gross debt stood at $872 million, resulting in a net debt position of $274 million when excluding cash and investments.

The capital structure details are illustrated below:

Despite the strong balance sheet, free cash flow turned negative in Q1 2025 at -$5.0 million, compared to $47.4 million in Q1 2024. This significant decline in cash generation could potentially impact the company’s ability to pursue acquisitions or return capital to shareholders if the trend continues.

2025 Outlook and Guidance

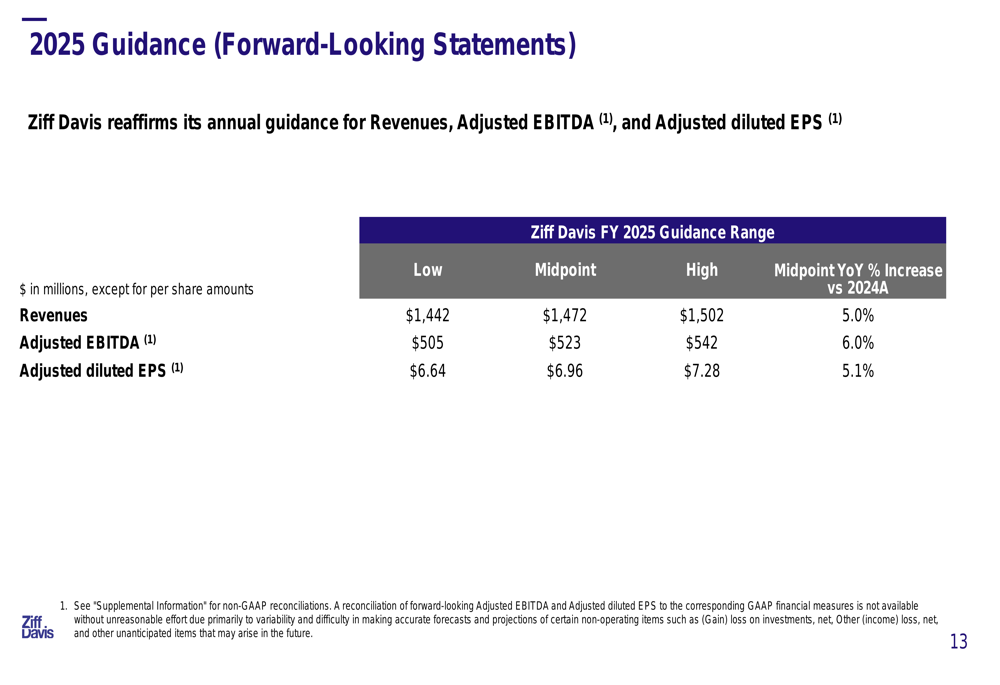

Ziff Davis reaffirmed its full-year 2025 guidance, projecting revenue of $1,472 million (5.0% year-over-year increase), adjusted EBITDA of $523 million (6.0% increase), and adjusted diluted EPS of $6.96 (5.1% increase).

The detailed guidance ranges are presented in the following table:

This guidance suggests management expects improved performance in the remaining quarters of 2025, particularly given the negative organic growth in Q1. During the previous quarter’s earnings call, executives had indicated that Q1 2025 would be relatively muted, with stronger growth projected for the latter half of the year.

Operational Metrics and Challenges

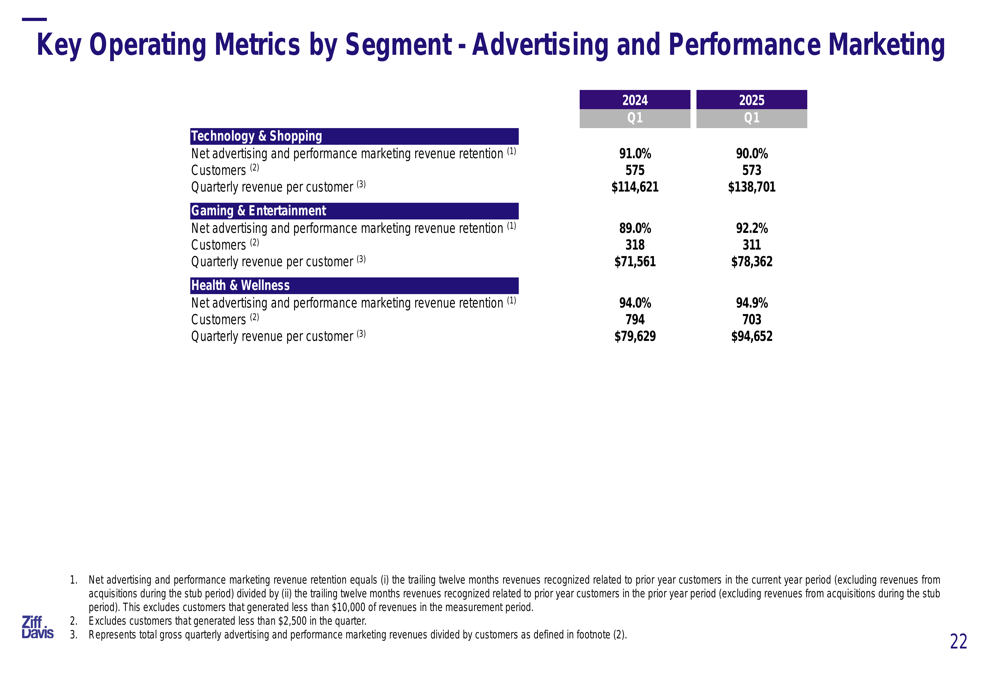

The presentation revealed important operational metrics across segments. In the advertising and performance marketing business, customer retention rates remained generally strong, though the number of customers varied by segment. The Technology & Shopping segment saw stable customer counts but significant increases in revenue per customer, rising from $114,621 to $138,701 quarterly.

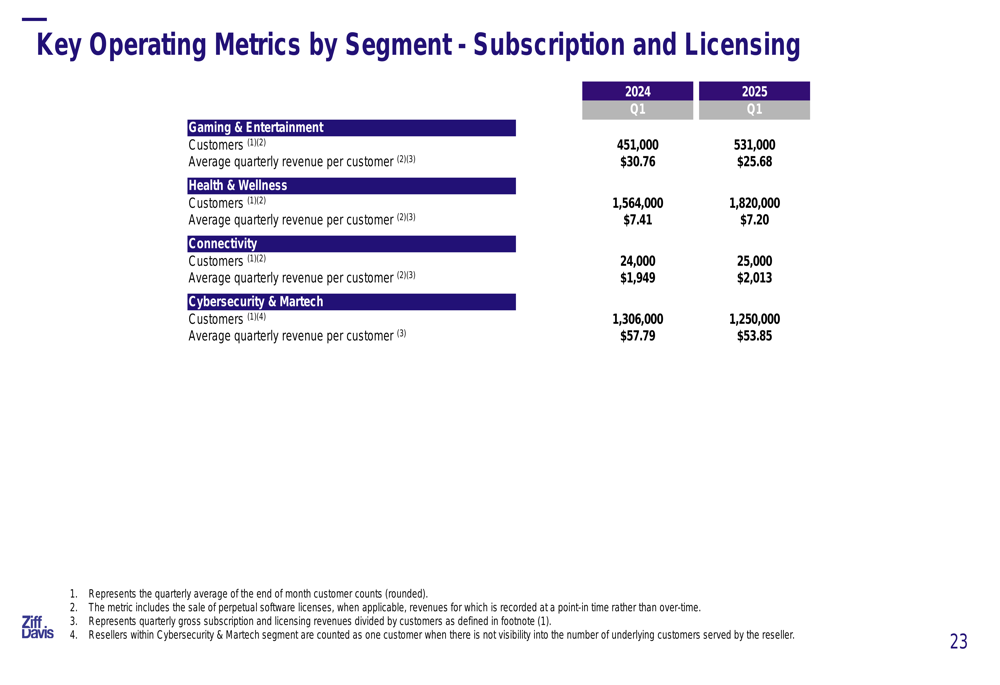

As shown in the following operational metrics:

For subscription businesses, customer trends were mixed. Gaming & Entertainment and Health & Wellness saw customer growth but declining average revenue per customer, while Cybersecurity & Martech experienced both customer loss and revenue per customer decline.

These metrics highlight the company’s ongoing challenge of balancing customer acquisition with monetization across its diverse portfolio of digital properties.

While Ziff Davis continues to execute its acquisition-driven growth strategy, the persistent negative organic growth and declining free cash flow raise questions about the sustainability of its current approach. The significant divergence in segment performance also suggests potential strategic reviews may be needed for underperforming units, particularly in the Cybersecurity & Martech segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.