Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

ZipRecruiter Inc. (NYSE:ZIP) presented its corporate strategy on May 8, 2025, following the release of first-quarter results that showed the online recruitment platform facing significant headwinds. The company’s stock fell 3.33% in after-hours trading following a 7.24% gain during regular trading hours, reflecting mixed investor sentiment about its performance and outlook.

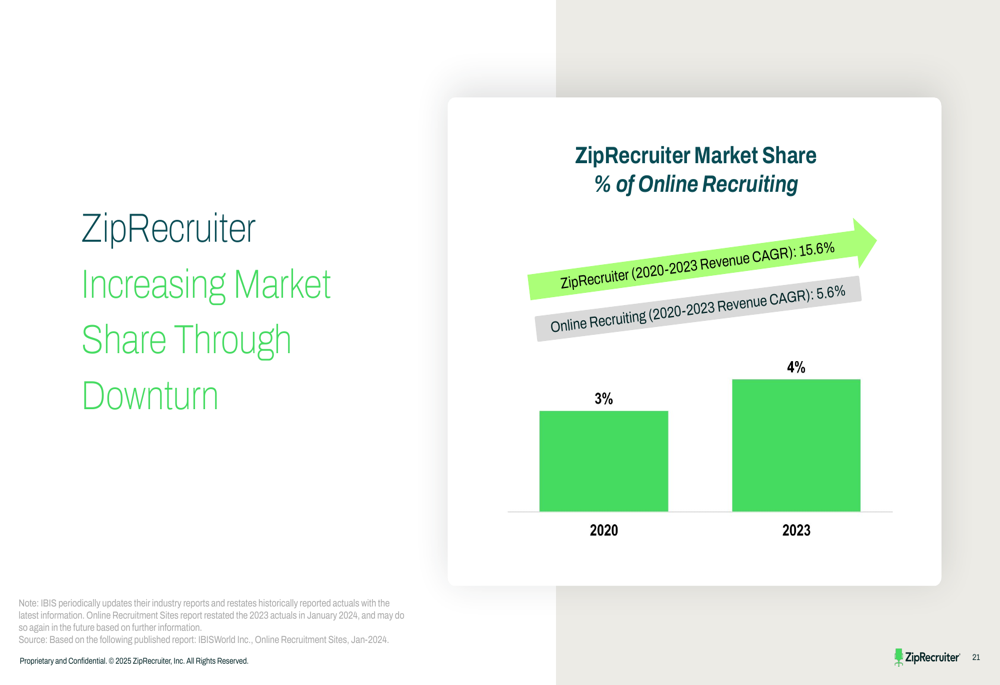

The presentation emphasized ZipRecruiter’s position in the $300+ billion recruiting industry, where online recruitment is growing at a faster rate (4.6% CAGR) than traditional recruiting methods (3.2% CAGR). Despite current challenges, the company highlighted its market share growth from 3% to 4% between 2020 and 2023, with a revenue CAGR of 15.6% during that period compared to the online recruiting industry’s 5.6%.

Quarterly Performance Highlights

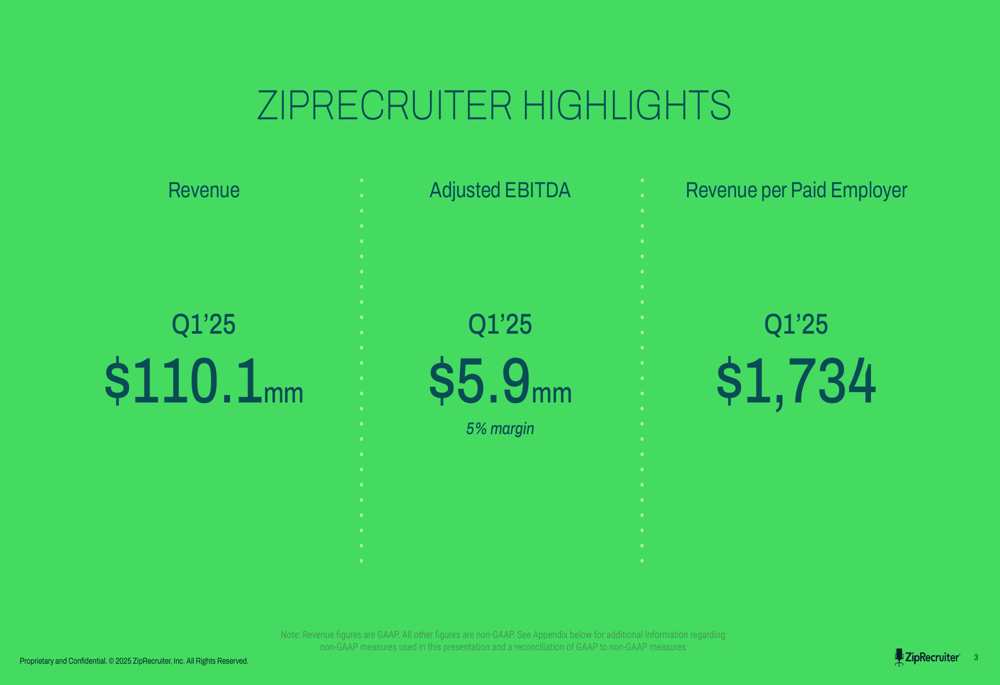

ZipRecruiter reported Q1 2025 revenue of $110.1 million, which exceeded analyst expectations but represented a 10% year-over-year decline. The company posted an Adjusted EBITDA of $5.9 million, reflecting a 5% margin – significantly lower than the 17% margin achieved in Q1 2024.

As shown in the following financial highlights slide from the presentation:

The decline in profitability comes despite the company’s efforts to maintain what it calls a "flexible financial model." The presentation noted that ZipRecruiter had achieved a 16% Adjusted EBITDA margin for FY 2024 "despite significant macroeconomic headwinds," but current results suggest increasing pressure on margins.

Quarterly paid employers increased 10% sequentially to 63,000, though this figure remains 11% lower year-over-year. Revenue per paid employer stood at $1,734 for the quarter, reflecting the company’s ability to monetize its customer base despite challenging conditions.

Strategic Initiatives

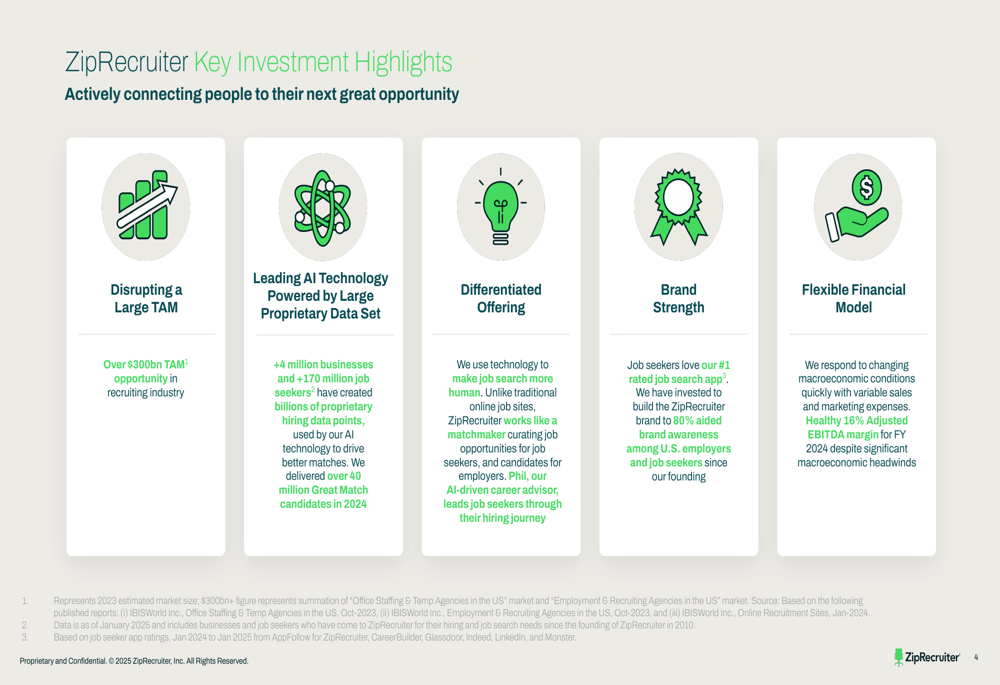

ZipRecruiter’s presentation heavily emphasized its AI-driven approach to connecting job seekers and employers. The company highlighted that its technology delivered over 40 million "Great Match" candidates in 2024, with 80% of employers receiving quality candidates within 24 hours of posting.

The company’s investment in AI technology is illustrated in this key highlights slide:

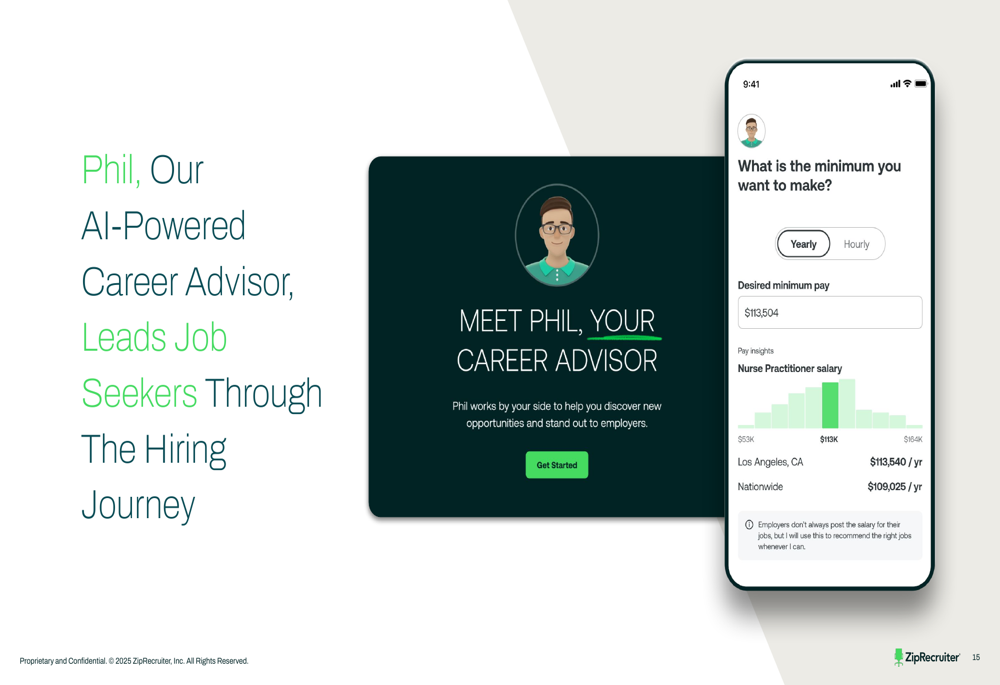

A central element of ZipRecruiter’s strategy is "Phil," an AI-powered career advisor that guides job seekers through their hiring journey. The company positions this technology as a key differentiator in making the job search process "more human" despite being technology-driven.

As shown in the following slide detailing Phil’s capabilities:

ZipRecruiter’s business model remains primarily subscription-based, with 78% of revenue coming from flat-rate pricing (daily, monthly, and annual subscription plans) and 22% from performance-based pricing (cost-per-click on job postings). This revenue mix provides some stability while allowing for performance-based growth opportunities.

Competitive Industry Position

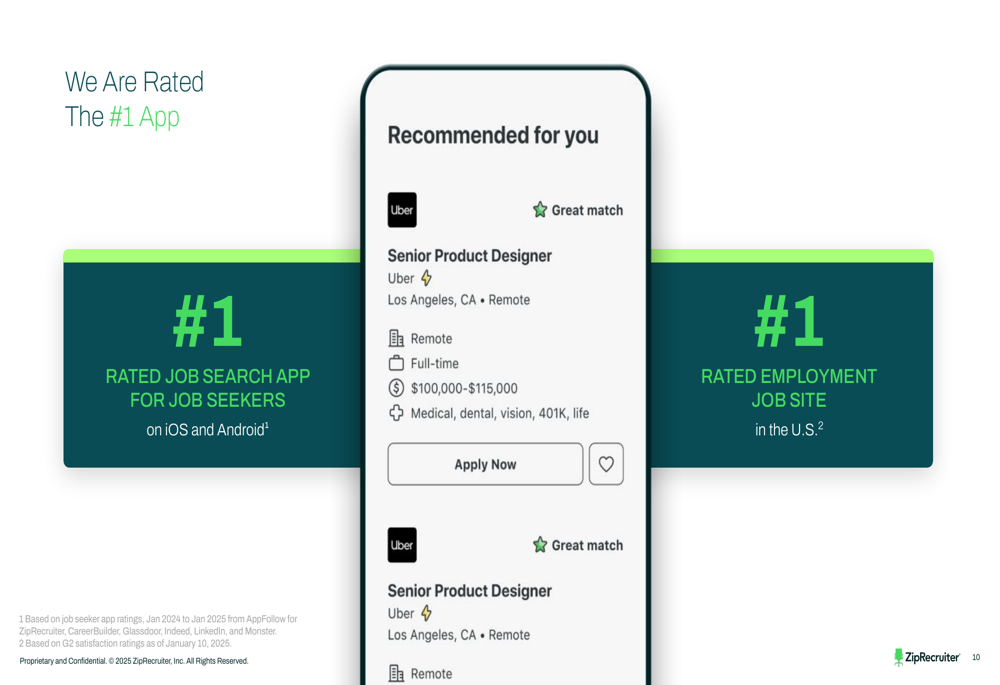

The presentation emphasized ZipRecruiter’s strong brand position, claiming the #1 rated job search app on both iOS and Android platforms. The company reported over 80% aided brand awareness, supported by extensive marketing relationships with major media platforms.

The company’s competitive positioning is illustrated in this brand strength slide:

ZipRecruiter’s two-sided marketplace connects over 4 million employers with more than 170 million job seekers, creating what the company describes as billions of proprietary hiring data points that power its AI matching algorithms.

The company’s market share growth relative to the broader online recruiting industry is highlighted in the following slide:

This data suggests that despite current revenue challenges, ZipRecruiter has been gaining share in its target market through the recent economic cycle, potentially positioning it for stronger performance when labor market conditions improve.

Forward-Looking Statements

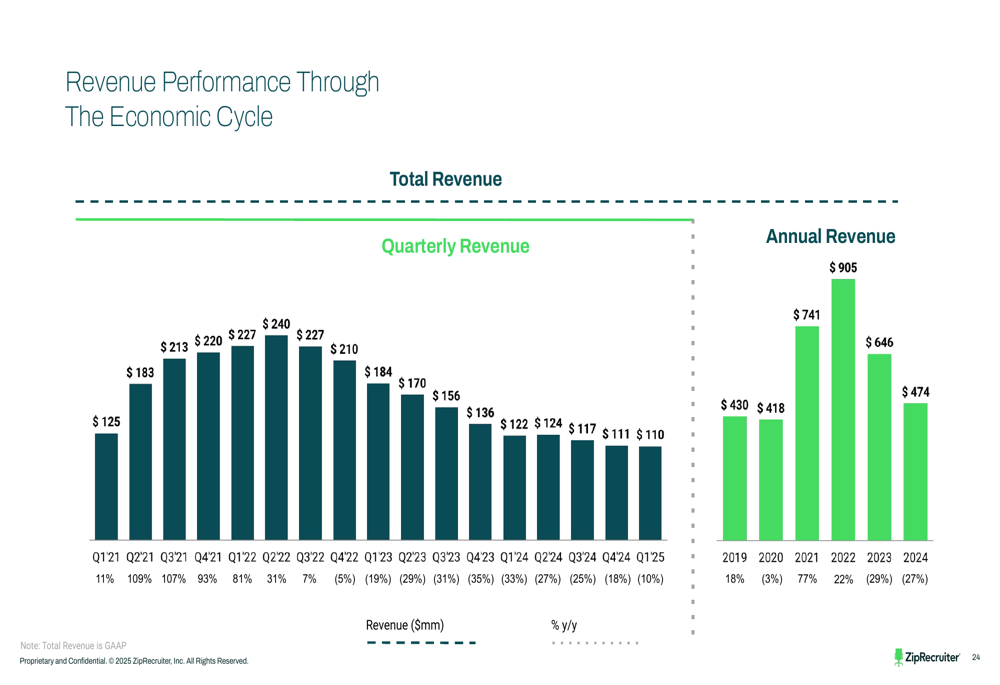

Looking ahead, ZipRecruiter projects Q2 2025 revenue of $111 million, representing a modest 1% quarter-over-quarter increase. Management expressed cautious optimism about achieving year-over-year revenue growth by Q4 2025, with full-year adjusted EBITDA margins expected to remain in the mid-single digits.

The company’s revenue performance through economic cycles is illustrated in this comprehensive chart:

CEO Ian Siegel expressed confidence in the company’s positioning for an eventual labor market recovery, stating, "We believe we are poised for outsized growth when the inevitable recovery in the labor market returns." This sentiment suggests management views current challenges as cyclical rather than structural.

The company maintains a strong balance sheet with $468 million in cash, providing financial flexibility as it navigates the current environment. During Q1, ZipRecruiter repurchased 4.6 million shares for $27.4 million, demonstrating confidence in its long-term prospects despite near-term headwinds.

ZipRecruiter’s growth strategy focuses on increasing both sides of its marketplace – attracting more job seekers and employers – while continuing to strengthen its AI technology platform and optimize its performance-based pricing model. The company also indicated plans to expand its global footprint, though specific international growth targets were not detailed in the presentation.

As the online recruitment market continues to evolve, ZipRecruiter’s emphasis on AI-driven matching and marketplace optimization represents a strategic bet that technology can deliver superior outcomes for both employers and job seekers, potentially driving improved financial performance when labor market conditions normalize.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.