Can anything shut down the Gold rally?

JP Morgan has upgraded Apollo Types (APTY) to Overweight from Neutral, highlighting the company's dedication to reducing debt and pursuing disciplined growth. Despite a modest margin miss in the 4QFY24 results, APTY has already announced price increases to counteract the impact of environmental protection requirements (EPR) and commodity inflation. Additionally, strong free cash flow (FCF) conversion, exceeding 100%, underscores the company's financial resilience.

The recent decline in APTY's stock price, down 12% since the 3Q results compared to Nifty Auto's 16% increase, reflects concerns over commodity inflation and higher environmental costs. While 1HFY25 margins may face some pressure, JP Morgan anticipates price hikes and lower interest expenses to bolster full-year earnings, projecting a 13% year-on-year increase.

Offer: Unlock the power of informed investing with InvestingPro! Access comprehensive stock analysis, actionable insights, and accurate fair value calculations, all in one platform. Click here and start your investment journey with a massive 69% discount!

Despite maintaining FY25/26E EPS estimates, JP Morgan has raised the price target to INR 555, rolled forward to Jun-25. APTY's current valuation stands at 13x FY26E P/E with a 7% FCF yield.

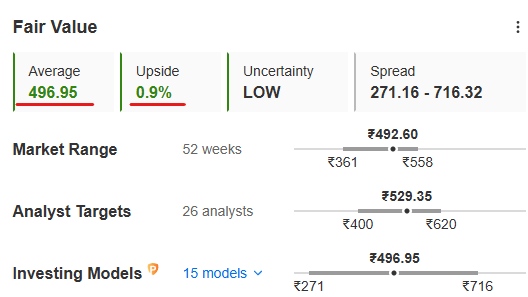

Image Source: InvestingPro+

But if we look at the fair value of Apollo Tyres (NS:APLO), investors might not get a big smile on their faces. After going through 15 complex financial models, the fair value comes at INR 469.95, leaving a minor 0.9% upside from the CMP of INR 492.6. The stock can be considered almost fairly valued.

A total of 26 analysts that are covering this counter have given an average upside target of INR 529.35. While JP Morgan is also looking for INR 555, investors can think of holding their positions for a little longer but at the same time they can also look to tighten their stop losses to protect their profits in case the stock takes a U-turn.

Key Highlights from the 4QFY24 Scorecard:

- Consolidated adjusted EBITDA of INR 11bn, up 10% year-on-year, slightly below JP Morgan estimates.

- India EBITDA, adjusted for EPR, missed by 2%, with flat year-on-year revenue offset by better-than-expected margins.

- Reported PAT at INR 3.5bn was 30% below JP Morgan estimates, primarily due to operating miss and EPR provisions.

- Net debt declined to INR 25bn as of Mar-24, with a notable improvement in ROCE to 16% in FY24.

APTY management emphasizes pricing adjustments to mitigate EPR and commodity inflation impacts, with a 3% price hike already implemented. Capex for FY24 was lower than guidance at INR 7bn, with FY25 guidance at INR 10bn, aiming for near-debt-free status by FY26.

India replacement growth has seen double-digit growth in April, indicating a strong start to FY25. EU growth is also robust, with a focus on improving the product mix, particularly in ultra-high performance (UHP) tyres.

Valued at Jun-26E P/B of 2x, reflecting improving return ratios. The price target implies a P/E of 15x and EV/EBITDA of 7.5x. Risks include potential price competition in India, weakness in EU replacement tyre demand, and resumption of a large capex cycle.

What are you waiting for? Click here to grab your limited-time offer of 69% discount on a revolutionary investment analysis tool - InvestingPro!

Also Read: Breakout: Stock Breaks Trendline with a 5% Circuit

X (formerly, Twitter) - Aayush Khanna