Trump announces trade deal with EU following months of negotiations

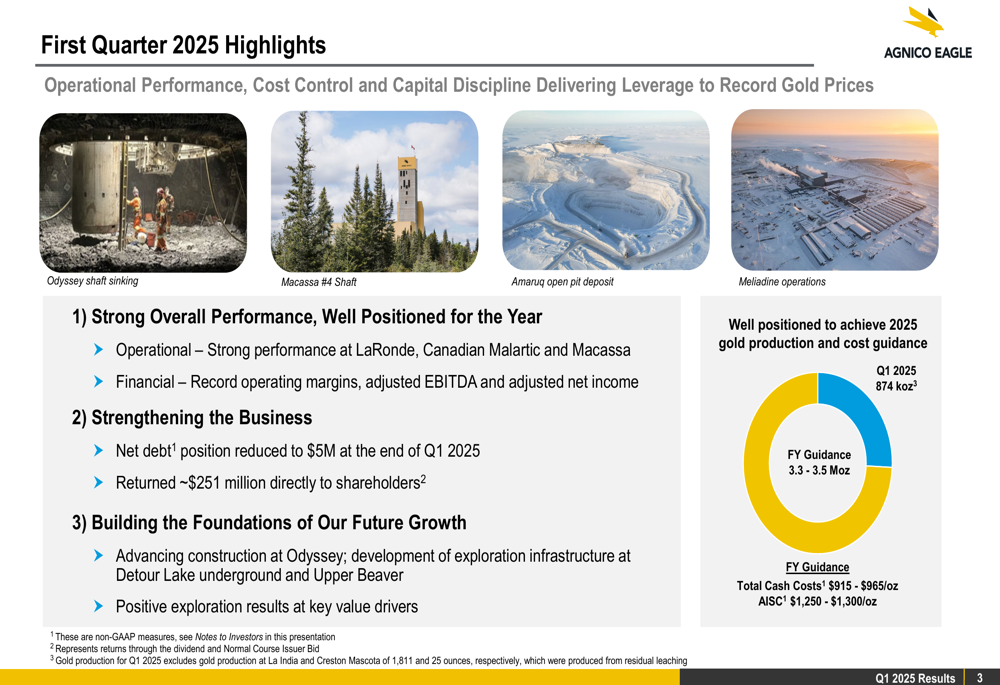

Agnico Eagle Mines Limited (NYSE:AEM) delivered exceptional first-quarter results for 2025, capitalizing on high gold prices while demonstrating strong operational performance and financial discipline. The company’s April 25 presentation highlighted record operating margins and the near elimination of net debt, positioning it well for future growth.

Executive Summary

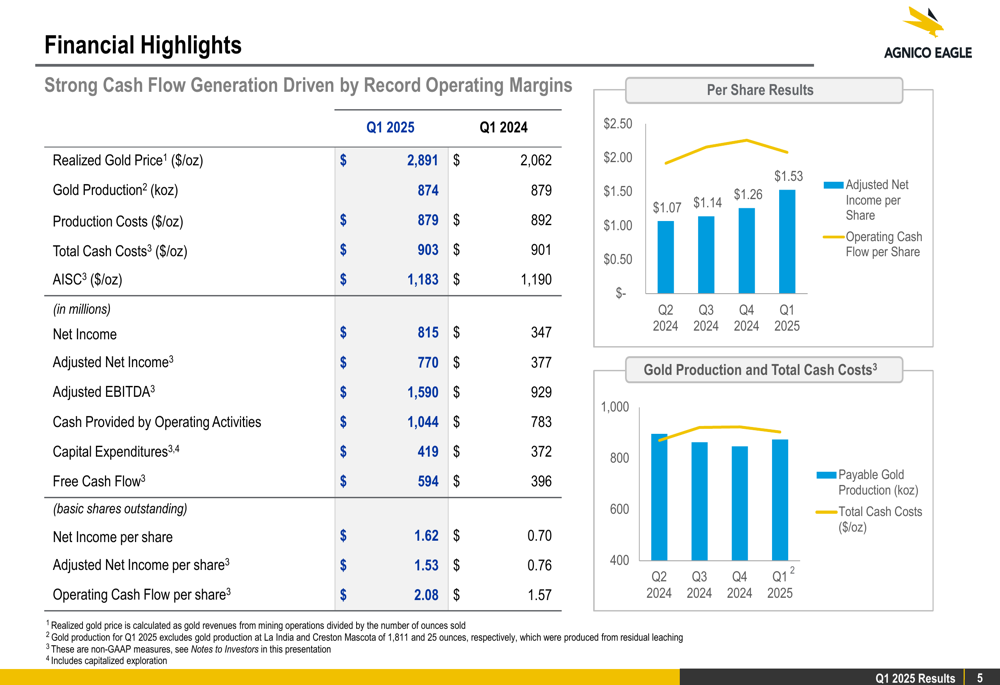

Agnico Eagle produced 874,000 ounces of gold in Q1 2025 at total cash costs of $903 per ounce, benefiting from a realized gold price of $2,891 per ounce. This combination drove record financial results, including adjusted EBITDA of $1.59 billion and free cash flow of $594 million.

"We’ve delivered strong overall performance across our operations, particularly at LaRonde, Canadian Malartic, and Macassa," the company noted in its presentation. "This has resulted in record operating margins, adjusted EBITDA, and adjusted net income."

The company remains on track to achieve its full-year 2025 guidance of 3.3-3.5 million ounces of gold production at total cash costs between $915-$965 per ounce and all-in sustaining costs (AISC) of $1,250-$1,300 per ounce.

As shown in the following chart of quarterly financial performance:

Financial Performance Highlights

Agnico Eagle’s Q1 2025 financial results demonstrated the company’s ability to convert high gold prices into shareholder value. Net income reached $815 million ($1.62 per share), while adjusted net income was $770 million ($1.53 per share). Operating cash flow totaled $1.04 billion ($2.08 per share), providing substantial financial flexibility.

The company’s production costs averaged $879 per ounce, while total cash costs were $903 per ounce and AISC was $1,183 per ounce. These metrics reflect Agnico Eagle’s continued focus on operational efficiency, building on the momentum seen in previous quarters. In Q3 2024, the company reported cash costs of $921 per ounce, indicating a slight improvement in cost control.

Capital expenditures for the quarter totaled $419 million, primarily directed toward growth projects at Odyssey, Detour Lake underground, and Upper Beaver, which are expected to drive future production increases.

The following slide highlights key operational achievements across the company’s portfolio:

Balance Sheet Strength

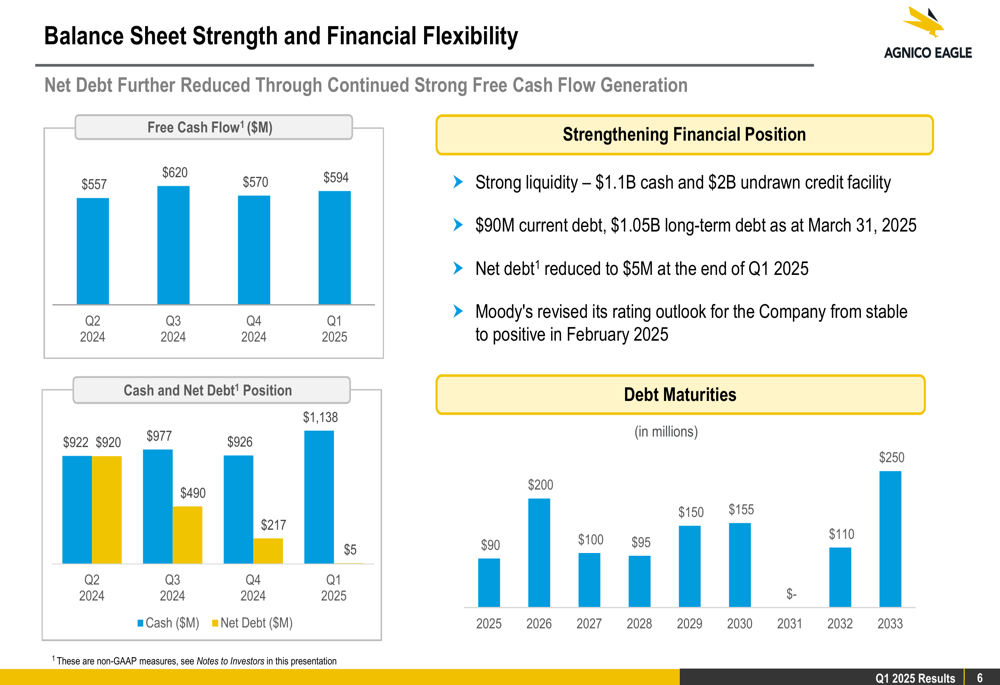

One of the most impressive aspects of Agnico Eagle’s Q1 2025 performance was the continued strengthening of its balance sheet. The company reduced its net debt position to just $5 million by the end of Q1 2025, down from $217 million at the end of Q4 2024 and $490 million in Q3 2024.

This dramatic debt reduction was achieved while maintaining strong shareholder returns, with approximately $251 million returned to shareholders during the quarter. The company maintains a quarterly dividend of $0.40 per share and intends to renew its share buyback program in May 2025.

Agnico Eagle’s liquidity position remains robust, with $1.1 billion in cash and a $2 billion undrawn credit facility. The company has minimal near-term debt maturities, with just $90 million due within the next six months.

The following chart illustrates the company’s impressive debt reduction trajectory:

Operational Performance

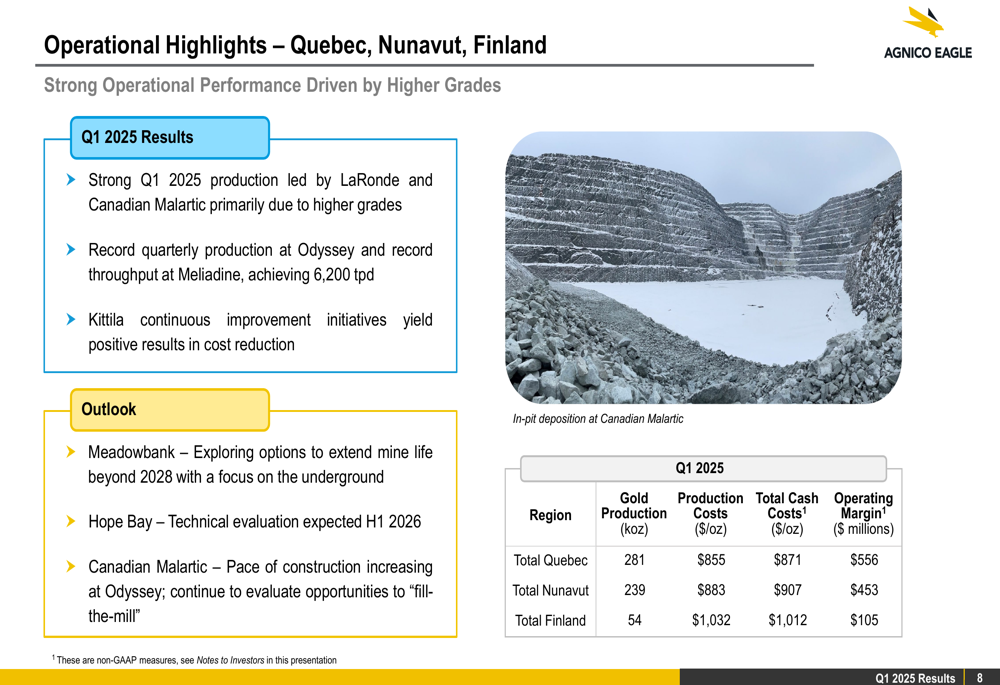

Agnico Eagle’s operations delivered strong results across most regions, with particularly notable performance in Quebec, Ontario, and Nunavut.

In Quebec, gold production reached 281,000 ounces at total cash costs of $871 per ounce, generating an operating margin of $556 million. Strong performance at LaRonde and Canadian Malartic was primarily attributed to higher grades, while Odyssey achieved record quarterly production.

The Nunavut platform produced 239,000 ounces at total cash costs of $907 per ounce, resulting in an operating margin of $453 million. Ontario operations contributed 239,000 ounces at total cash costs of $838 per ounce, with an operating margin of $495 million. Macassa achieved multiple production records, though Detour Lake production was affected by adverse weather conditions.

The following slide provides a detailed breakdown of regional operational performance:

Growth Projects and Exploration

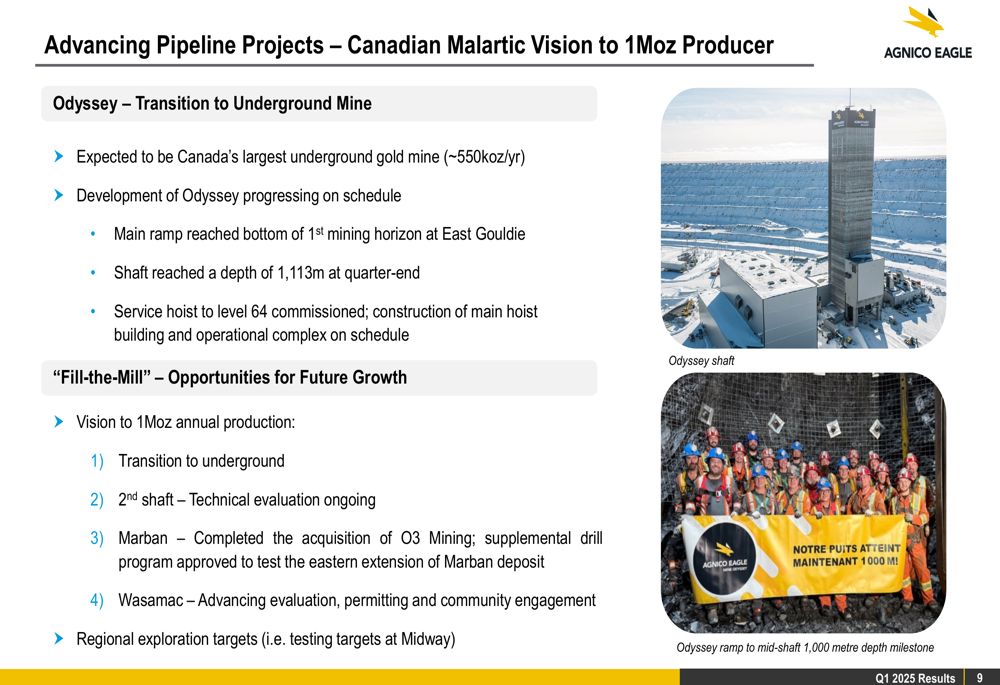

Agnico Eagle continues to advance several key growth projects that will shape its future production profile. At Canadian Malartic, the Odyssey underground project is progressing on schedule, with the main ramp reaching the bottom of the first mining horizon at East Gouldie and the shaft reaching a depth of 1,113 meters by quarter-end.

The company envisions Odyssey becoming Canada’s largest underground gold mine, with expected production of approximately 550,000 ounces per year. The broader vision for Canadian Malartic is to achieve annual production of 1 million ounces through various "fill-the-mill" opportunities.

As illustrated in the following slide on the Odyssey project:

In Ontario, Agnico Eagle is advancing two significant projects. At Detour Lake, currently Canada’s largest producing mine with a mine life extending to the 2050s, the company is developing a 2-kilometer exploration ramp to support its pathway to 1 million ounces of annual production beginning in 2030.

The Upper Beaver project is also progressing, with potential average annual production of approximately 210,000 ounces beginning in 2031. The company is advancing work on an exploration ramp and shaft.

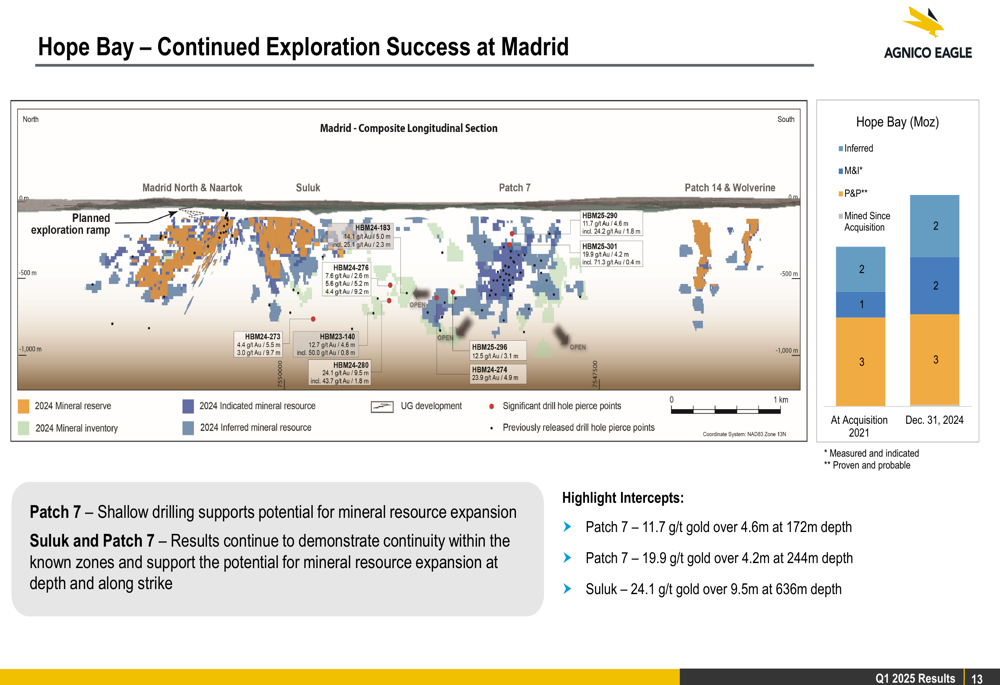

Exploration success continues at Hope Bay, where drilling at the Patch 7 and Suluk zones has returned impressive intercepts, including 24.1 g/t gold over 9.5 meters at 636 meters depth at Suluk. These results support potential mineral resource expansion at the project.

The following slide highlights exploration success at Hope Bay:

Sustainability Focus

Agnico Eagle emphasized its commitment to sustainable mining practices in its Q1 2025 presentation. The company’s approach includes a focus on safety through risk management, decarbonization efforts, and positive relationships with Indigenous communities.

The company reported a global greenhouse gas intensity of 0.38t CO2e per ounce and zero significant environmental incidents during the period. Social highlights included 646 Indigenous employees and a board composition that is 36% women.

Agnico Eagle invested approximately $11 million in community donations, spent about $1.9 billion on local goods and services, and directed approximately $1 billion to Indigenous businesses, underscoring its commitment to creating shared value in the regions where it operates.

Outlook and Guidance

Agnico Eagle remains well-positioned to achieve its 2025 gold production guidance of 3.3-3.5 million ounces at total cash costs of $915-$965 per ounce and AISC of $1,250-$1,300 per ounce.

The company’s capital allocation strategy balances reinvestment in growth projects, debt reduction, and shareholder returns. With its net debt position now at minimal levels, Agnico Eagle has enhanced financial flexibility to pursue its growth initiatives while maintaining its commitment to shareholder returns.

As gold prices remain elevated, with the company’s shares trading near $119.63 as of April 24, 2025, Agnico Eagle appears well-positioned to continue generating strong cash flows and creating shareholder value through its disciplined approach to mining in low-risk jurisdictions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.