German construction sector still in recession, civil engineering only bright spot

Booking Holdings Inc (NASDAQ:BKNG) reported strong first-quarter 2025 results on April 29, with revenue growing 8% year-over-year to $4.76 billion, driven by robust performance in alternative accommodations and continued strength in mobile bookings. Despite the positive results, the stock declined 3.57% in premarket trading.

Quarterly Performance Highlights

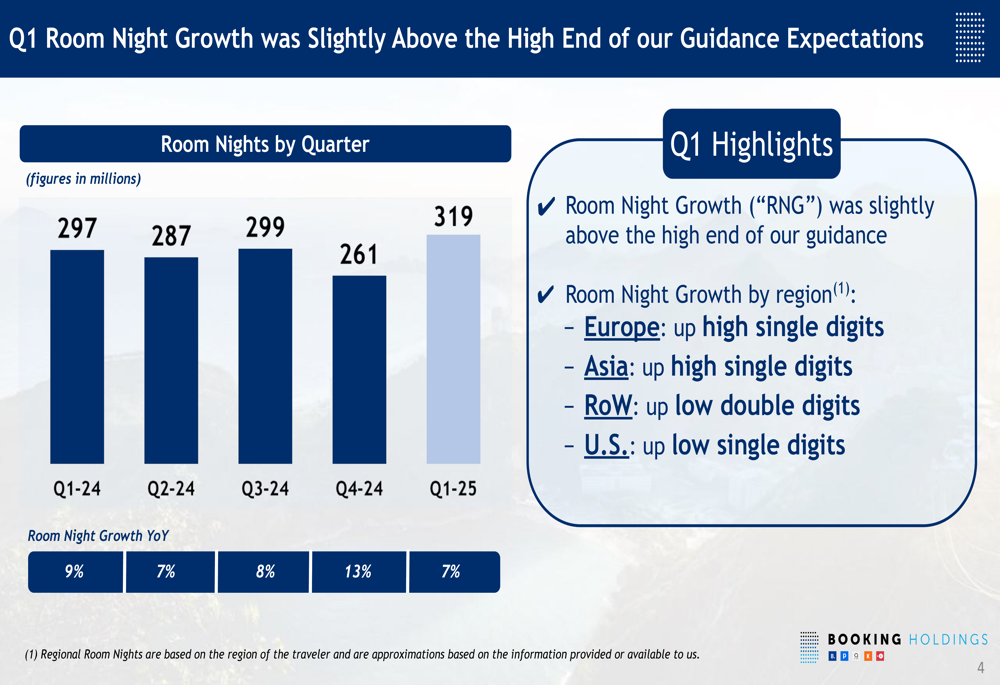

The travel giant achieved 319 million room nights in Q1 2025, representing a 7% year-over-year increase and exceeding the company’s guidance. This growth was geographically diverse, with Europe and Asia both up high single digits, Rest of World increasing low double digits, and the U.S. showing low single-digit growth.

As shown in the following chart of quarterly room night growth:

Alternative accommodations continued to outperform the broader business, with room nights in this segment growing 12% year-over-year, compared to 7% for total room nights. The company’s alternative accommodations listings increased 9% year-over-year to 8.1 million, demonstrating Booking’s commitment to this fast-growing segment.

The following chart illustrates how alternative accommodations growth consistently outpaces total room night growth:

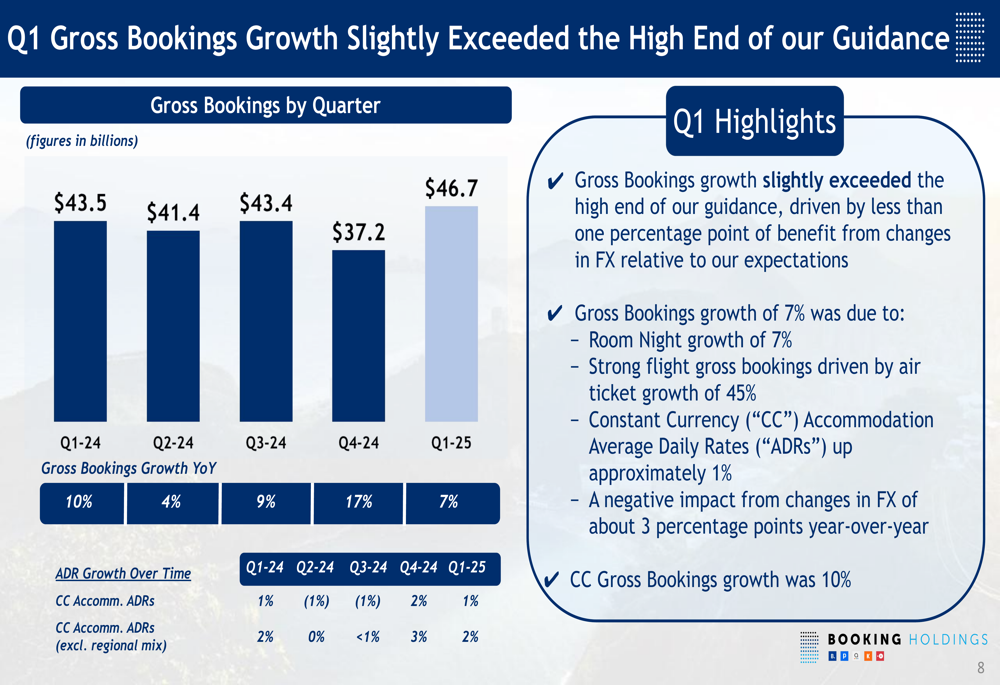

Gross bookings reached $46.7 billion in Q1, up 7% year-over-year, slightly exceeding the company’s guidance. This growth was driven by increased room nights, strong flight bookings, and a modest 1% increase in constant currency accommodation average daily rates.

The quarterly progression of gross bookings is shown here:

Detailed Financial Analysis

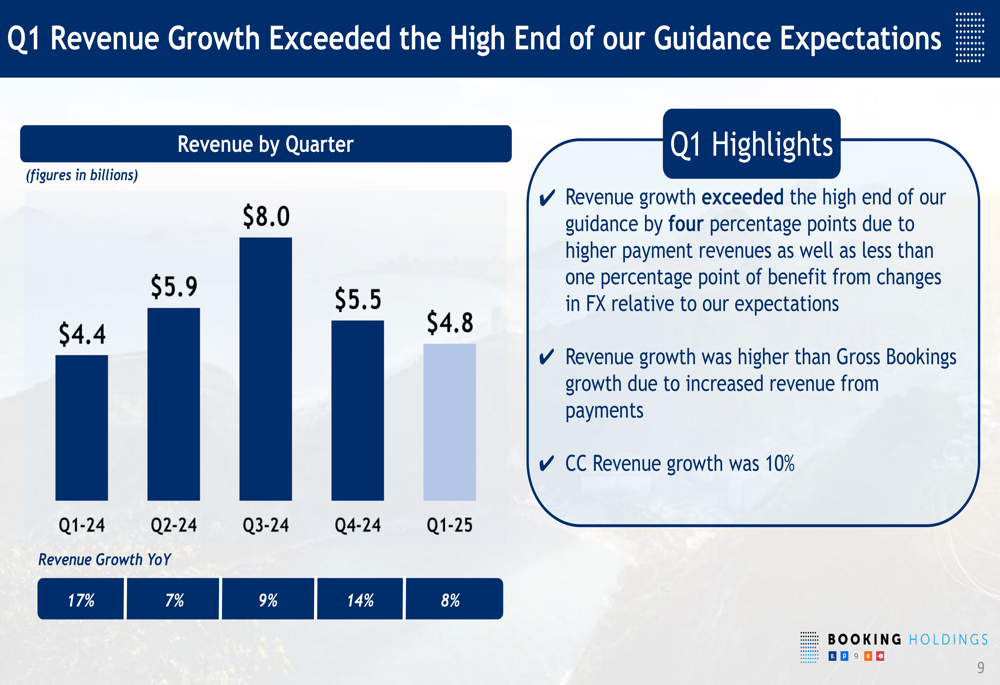

Revenue for Q1 2025 reached $4.76 billion, an 8% increase year-over-year, exceeding the high end of guidance. When adjusted for currency effects, revenue growth was even stronger at 10%. The company attributed this performance to higher payment revenues.

The following chart shows the quarterly revenue progression:

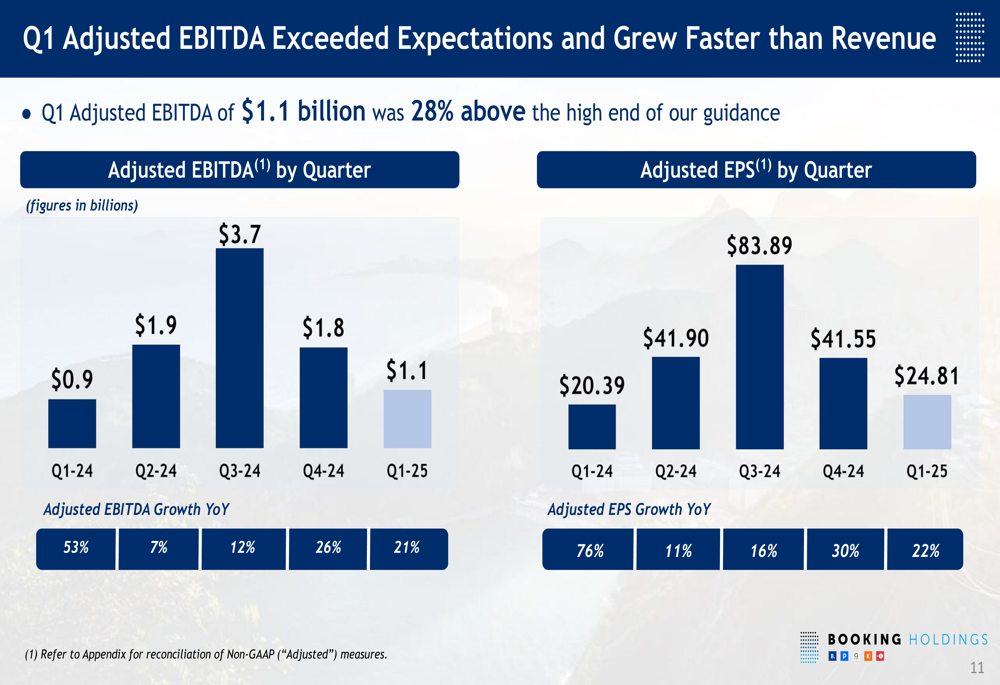

Booking Holdings demonstrated impressive profitability improvements, with Q1 Adjusted EBITDA reaching $1.09 billion, up 21% year-over-year and 28% above the high end of guidance. Adjusted EBITDA margin improved to 35.3% of revenue in Q1 2025, compared to 33.7% in Q1 2024.

The company’s adjusted earnings per share reached $24.81 in Q1, representing a 22% increase from the prior year’s $20.39. This significantly outperformed analyst expectations of $17.45, according to the earnings report.

As illustrated in the following chart of Adjusted EBITDA and EPS growth:

Free cash flow generation remained strong at $3.2 billion for Q1, up 23% year-over-year. The company continued its capital return program, returning $2.1 billion to shareholders through share repurchases and dividends during the quarter.

Notably, Booking Holdings has maintained disciplined expense management, with adjusted fixed operating expenses declining 3% year-over-year to $1.16 billion in Q1 2025, while headcount growth slowed to just 2% year-over-year.

Strategic Initiatives

The company’s strategic focus on alternative accommodations continues to yield results, with this segment now representing 37% of total room nights, an increase from the prior year. The 12% growth in alternative accommodation room nights outpaced the overall 7% room night growth, highlighting the importance of this segment to Booking’s future.

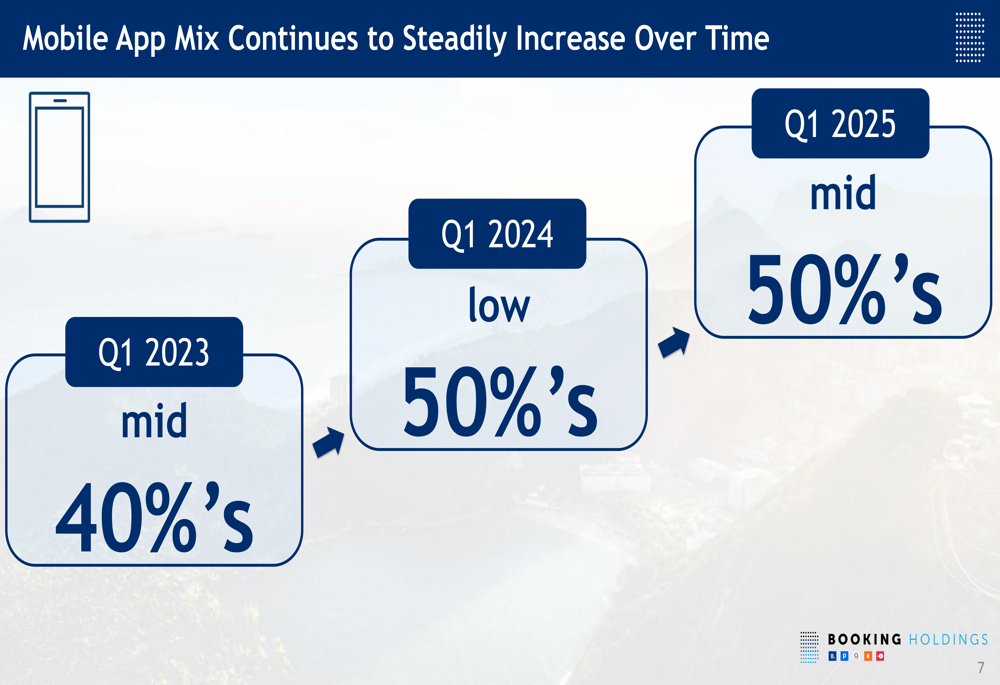

Mobile app usage also showed strong momentum, with the mobile app mix reaching the mid-50% range in Q1 2025, up from the low-50% range in Q1 2024. This progression demonstrates increasing customer loyalty and engagement with Booking’s platforms.

The mobile app mix progression is shown in the following visualization:

Connected Transactions, which integrate multiple travel services into a single booking experience, grew more than 35% year-over-year and now represent a high single-digit percentage of Booking.com’s total transactions. This growth reflects the company’s success in creating a more seamless travel booking experience.

The company also noted that its business-to-consumer direct mix was in the mid-60% range on a trailing twelve-month basis, indicating strong direct customer relationships rather than reliance on third-party channels.

Forward-Looking Statements

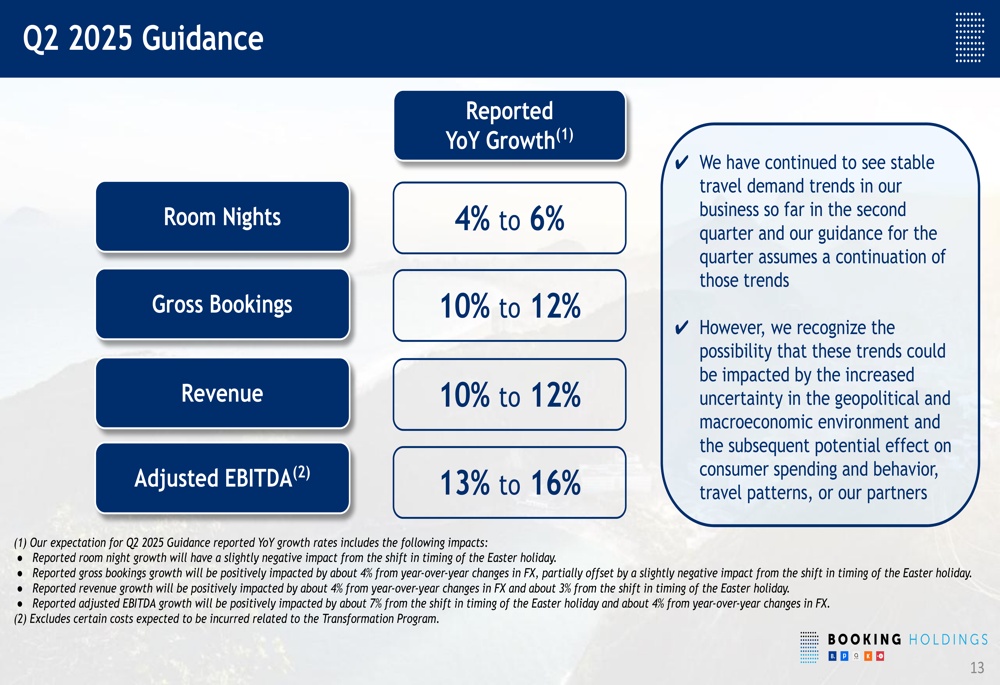

For Q2 2025, Booking Holdings provided the following guidance:

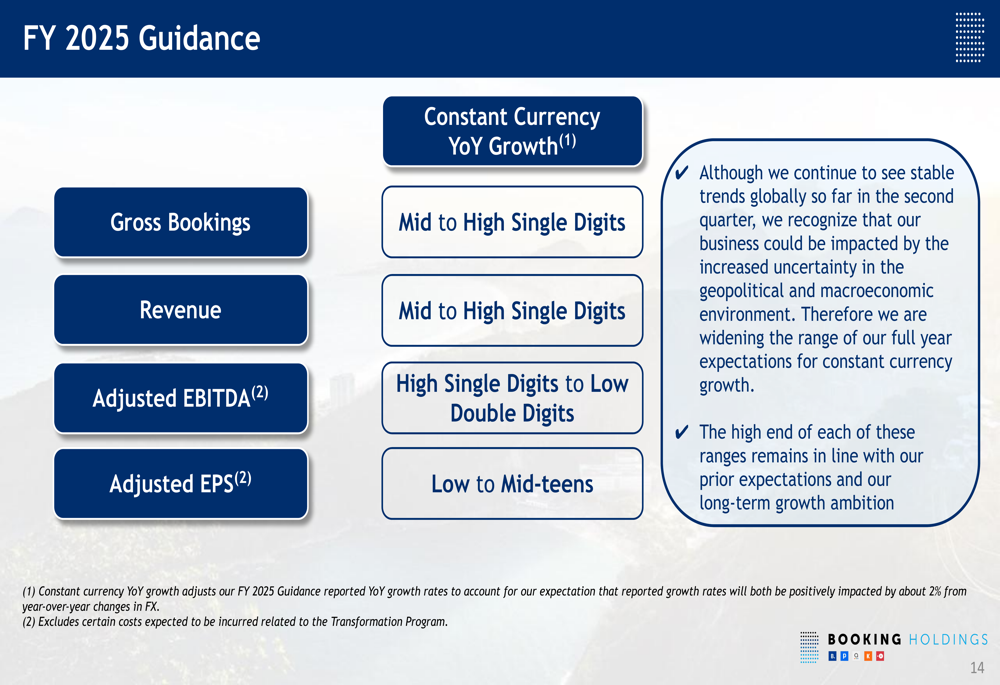

Looking further ahead, the company maintained its full-year 2025 guidance, projecting mid to high single-digit growth in gross bookings and revenue, with adjusted EBITDA expected to grow in the high single digits to low double digits. Adjusted EPS is forecast to grow in the low to mid-teens.

The company noted that while it continues to see stable travel demand, it has widened its guidance range to account for uncertainty in the geopolitical and macroeconomic environment.

Despite the strong financial results, Booking Holdings’ stock was down 3.57% in premarket trading to $4,733.98, suggesting that investors may have been expecting even stronger results or guidance. The stock remains below its 52-week high of $5,337.24 but well above its 52-week low of $3,180.

According to the earnings call transcript, CEO Glenn Vogel highlighted the impact of AI on improving customer experience, while CFO Ewout Steenbergen emphasized the company’s global diversification as a strength in mitigating country-specific challenges. The company continues to face risks from geopolitical uncertainty, potential weakness in the US market, and intense competition in the travel sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.