Bitcoin price today: steady near $92k after sharp losses; Fed caution weighs

Bread Financial Holdings Inc (NYSE:BFH) shares rose 4.43% following the release of its second quarter 2025 results on July 24, closing at $56.42. The financial services company demonstrated resilience amid economic uncertainty, reporting solid earnings and improved credit metrics while advancing key strategic initiatives.

Executive Summary

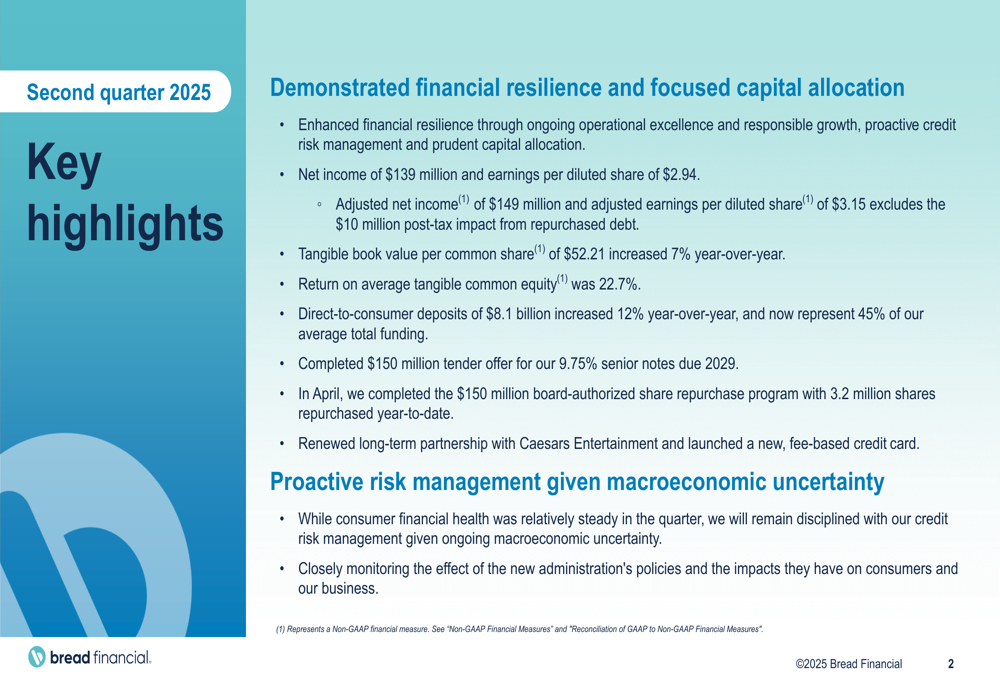

Bread Financial reported net income of $139 million or $2.94 per diluted share for the second quarter. Excluding the $10 million post-tax impact from repurchased debt, adjusted net income reached $149 million or $3.15 per diluted share. The company achieved a strong return on average tangible common equity of 22.7%, while tangible book value per share increased 7% year-over-year to $52.21.

"We enhanced our financial resilience through ongoing operational excellence and responsible growth, proactive credit risk management and prudent capital allocation," the company stated in its presentation, highlighting its focus on navigating macroeconomic uncertainty.

As shown in the following key highlights slide, Bread Financial completed several strategic initiatives during the quarter, including a $150 million tender offer for senior notes and the completion of a $150 million share repurchase program:

Quarterly Performance Highlights

Credit sales increased 4% year-over-year to $6.8 billion, while average loans decreased slightly by 1% to $17.7 billion. Revenue declined marginally by 1% to $929 million compared to the same period last year. Total non-interest expenses increased by 3% to $481 million, primarily due to debt extinguishment costs.

The company's financial performance remained solid across key metrics, as illustrated in the financial highlights slide:

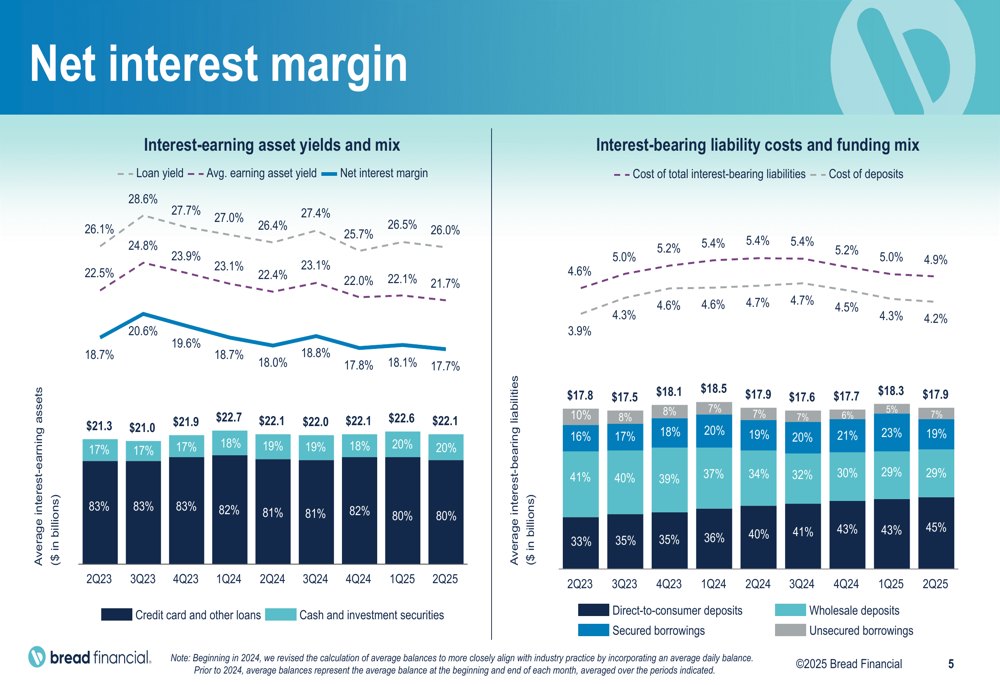

Bread Financial's funding strategy continued to shift toward direct-to-consumer deposits, which increased 12% year-over-year to $8.1 billion, now representing 45% of average total funding. This strategic shift helps the company maintain stable and cost-effective funding sources.

The following chart illustrates the company's net interest margin trends, showing a slight compression from 18.7% in Q2 2023 to 17.7% in Q2 2025:

Credit Quality & Risk Management

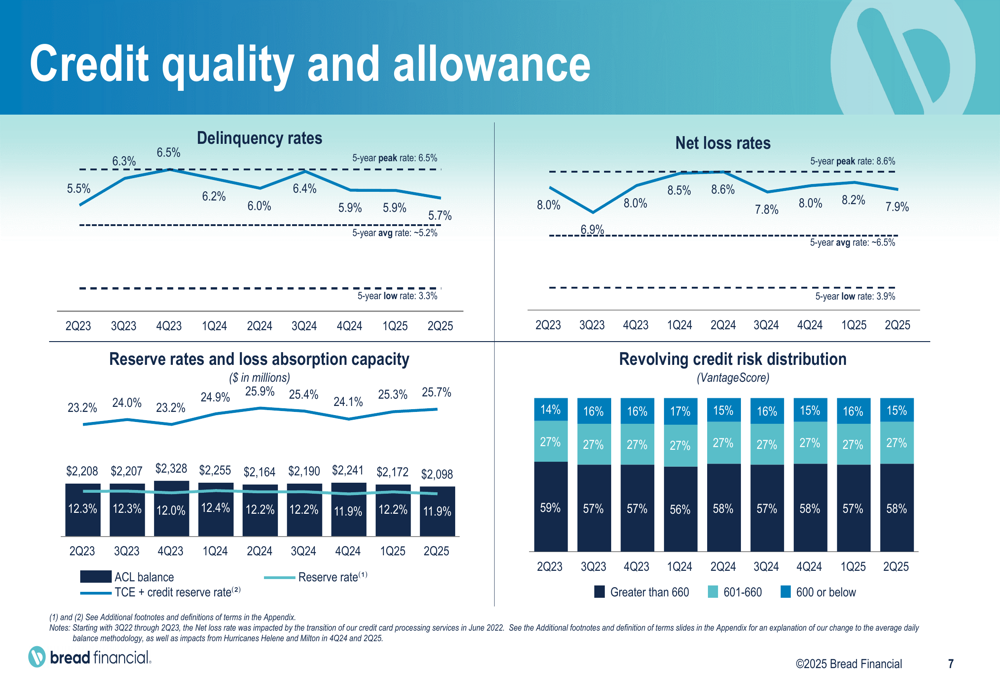

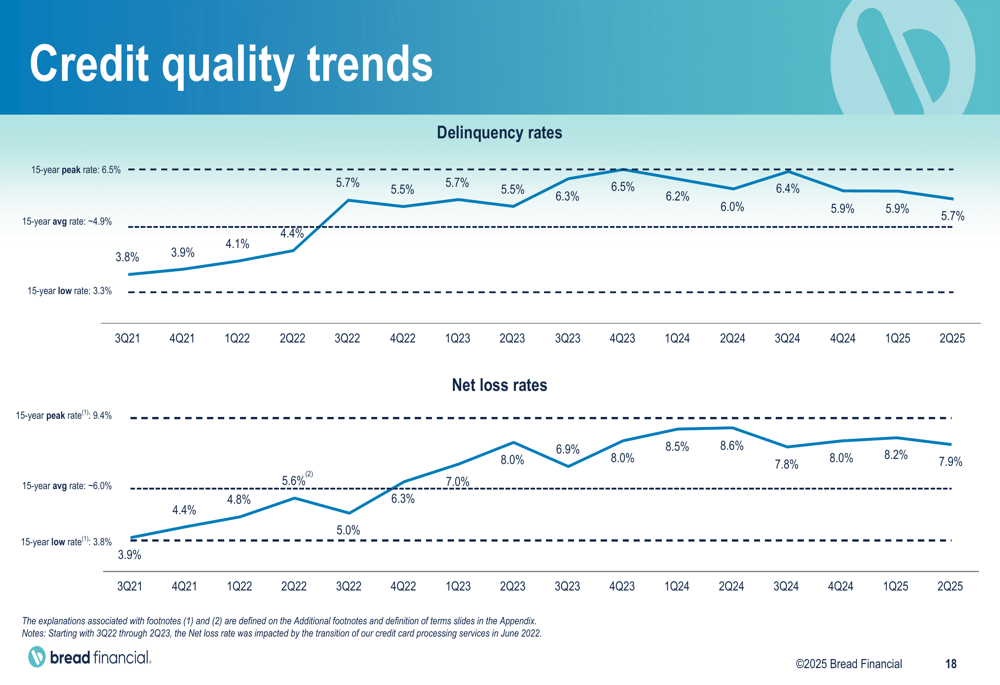

One of the most notable improvements in Bread Financial's Q2 results was in credit quality metrics. The net loss rate decreased to 7.9% from 8.6% in the same quarter last year, while the delinquency rate remained stable at 5.7%.

"While consumer financial health was relatively steady in the quarter, we will remain disciplined with our credit risk management given ongoing macroeconomic uncertainty," the company noted in its presentation, adding that it is "closely monitoring the effect of the new administration's policies and the impacts they have on consumers and our business."

The following slide details the company's credit quality metrics and allowance for credit losses, which stood at $2.098 billion or 11.9% of loans, slightly down from 12.2% a year ago:

The improvement in credit metrics is further illustrated in this trend chart showing delinquency and net loss rates over time:

Strategic Initiatives

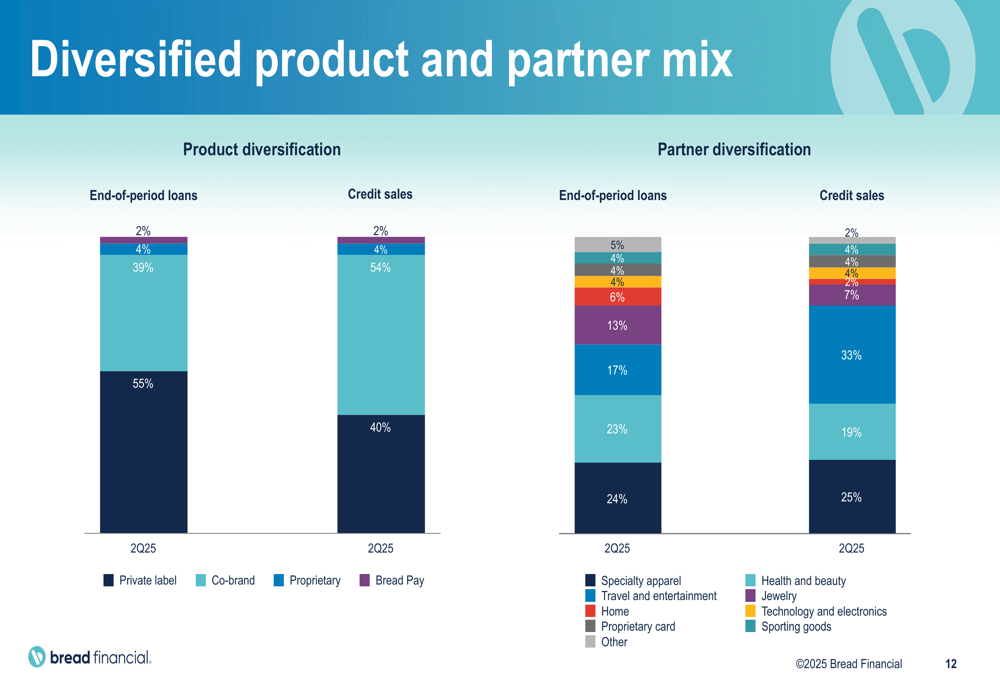

Bread Financial continued to advance its strategic initiatives during the quarter, including renewing its long-term partnership with Caesars Entertainment and launching a new, fee-based credit card. The company maintains a diversified product and partner mix, as shown in the following chart:

The company's product portfolio includes private label credit cards (55% of end-of-period loans), proprietary cards (39%), co-brand cards (4%), and Bread Pay buy-now-pay-later offerings (2%). This diversification helps mitigate risks associated with any single product category or retail partner.

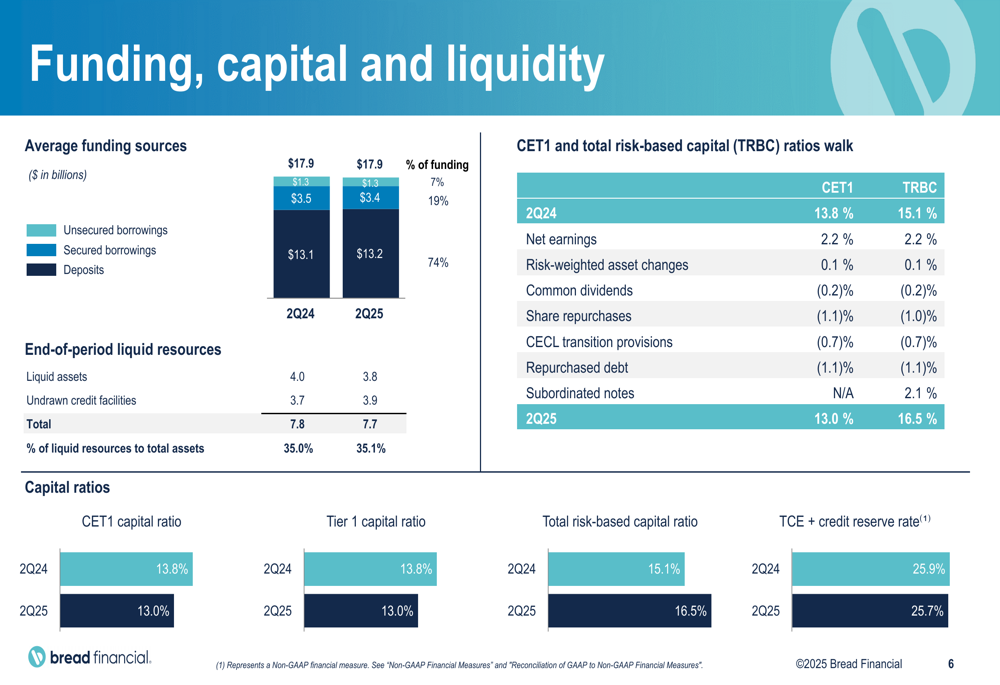

Bread Financial's capital position remained strong, with liquid resources of $7.7 billion representing 35.1% of assets. The company's funding, capital, and liquidity metrics are detailed in the following slide:

Forward-Looking Statements

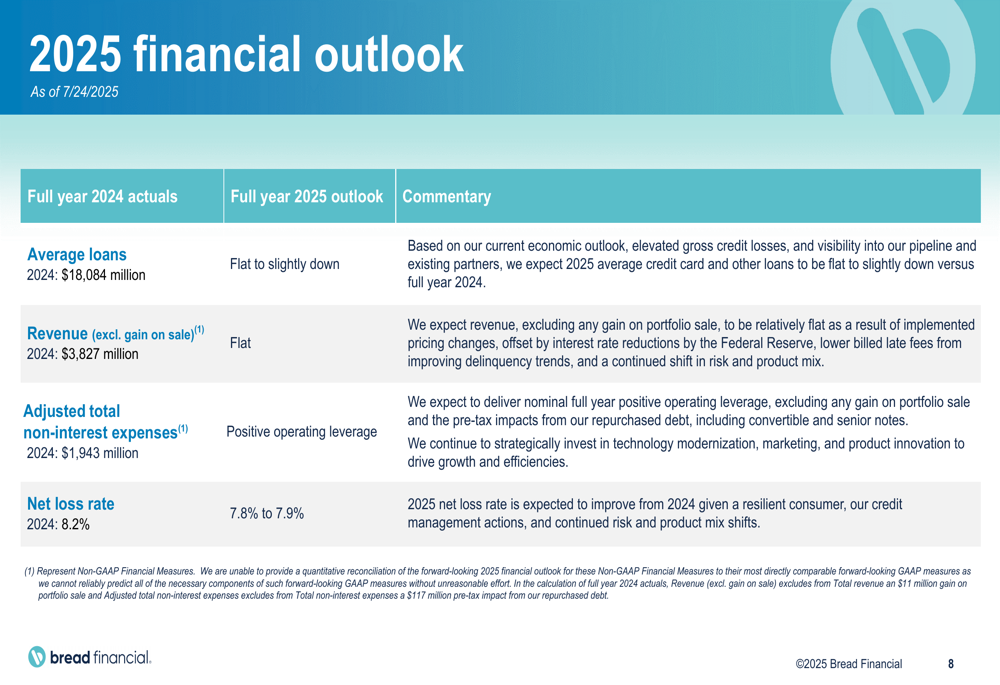

Looking ahead, Bread Financial provided a cautious but stable outlook for the remainder of 2025. The company expects average loans to be flat to slightly down, with revenue (excluding gain on sale) projected to be flat compared to 2024.

The company anticipates positive operating leverage through adjusted non-interest expense management and expects the net loss rate to improve from 2024, targeting 7.8% to 7.9% for the full year.

The following slide outlines the company's financial outlook for 2025:

Bread Financial's strategic focus for 2025 centers on four key areas: responsible growth, managing to the macroeconomic and regulatory environment, disciplined capital allocation and risk management, and operational excellence. These priorities aim to position the company for sustainable growth while navigating economic uncertainties.

"We are well positioned to deliver strong returns which we expect to translate into sustainable long-term value for our shareholders," CEO Ralph Andretta stated in the earnings call, emphasizing the flexibility of Bread Financial's product offerings.

With its improved credit metrics, strategic partnerships, and disciplined approach to capital management, Bread Financial appears well-positioned to navigate the current economic environment while continuing to deliver value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.