Can anything shut down the Gold rally?

Introduction & Market Context

Civitas Resources Inc (NYSE:CIVI) presented its first quarter 2025 results on May 8, highlighting a strategic shift toward debt reduction and cost optimization while maintaining production growth. Following a disappointing fourth quarter 2024 that saw the company miss earnings expectations, Civitas is taking a more disciplined approach to capital allocation in the current volatile oil price environment.

The company’s stock has faced pressure in recent months, trading at $27.13 at market close on May 7, 2025, down significantly from its 52-week high of $78.63. After-hours trading showed a further decline of 1.27% to $26.69, reflecting ongoing investor concerns despite the company’s efforts to strengthen its financial position.

Quarterly Performance Highlights

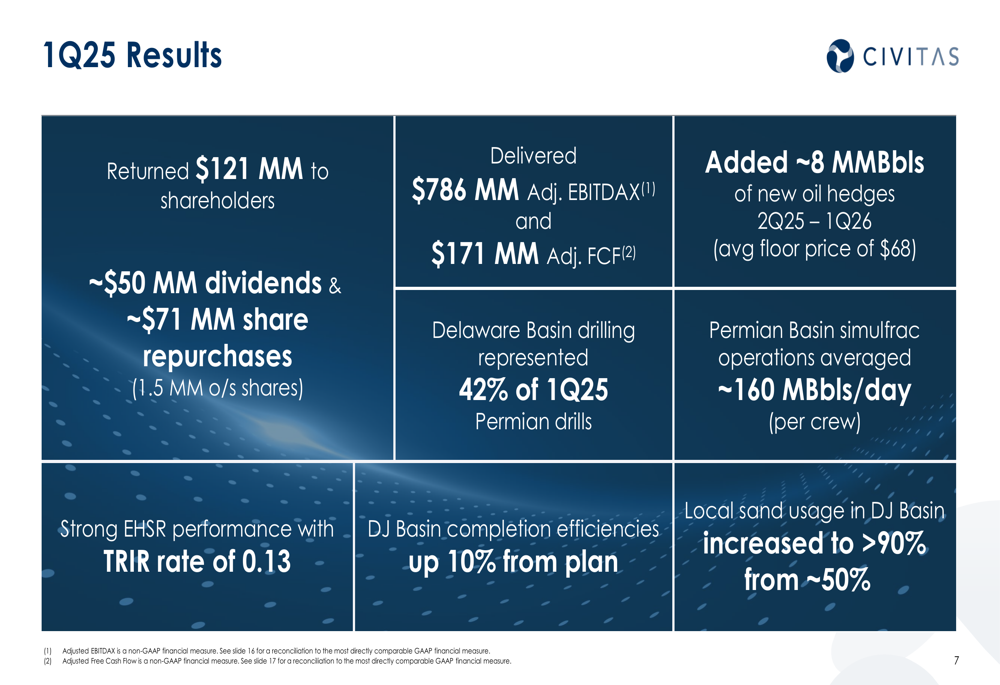

Civitas delivered $786 million in Adjusted EBITDAX and $171 million in Adjusted Free Cash Flow during the first quarter. The company returned $121 million to shareholders, split between approximately $50 million in dividends and $71 million in share repurchases, representing nearly 2% of outstanding shares.

As shown in the following quarterly results summary:

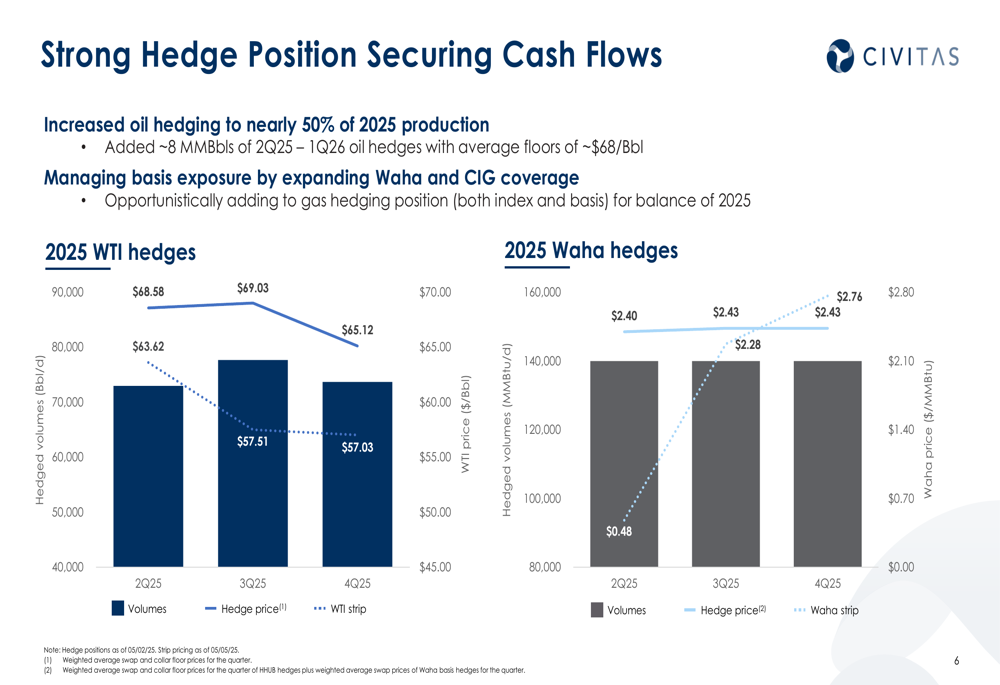

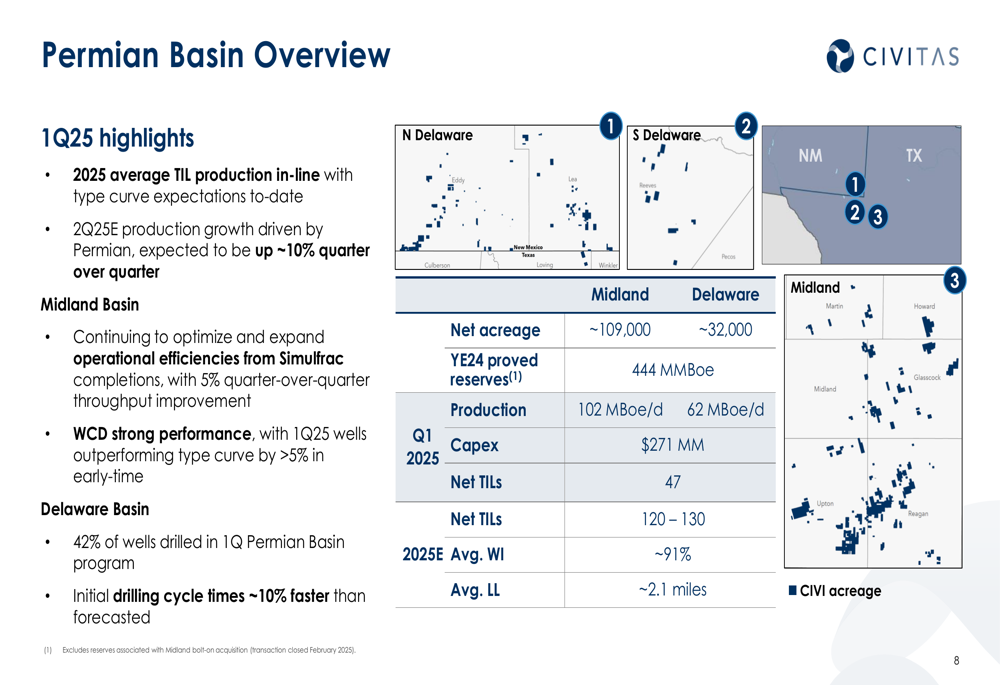

The company’s operational achievements included strong performance in its Delaware Basin drilling program, which represented 42% of first quarter Permian drills. Civitas also enhanced its hedge position by adding approximately 8 million barrels of new oil hedges for 2Q25-1Q26 with an average floor price of $68 per barrel.

Strategic Initiatives

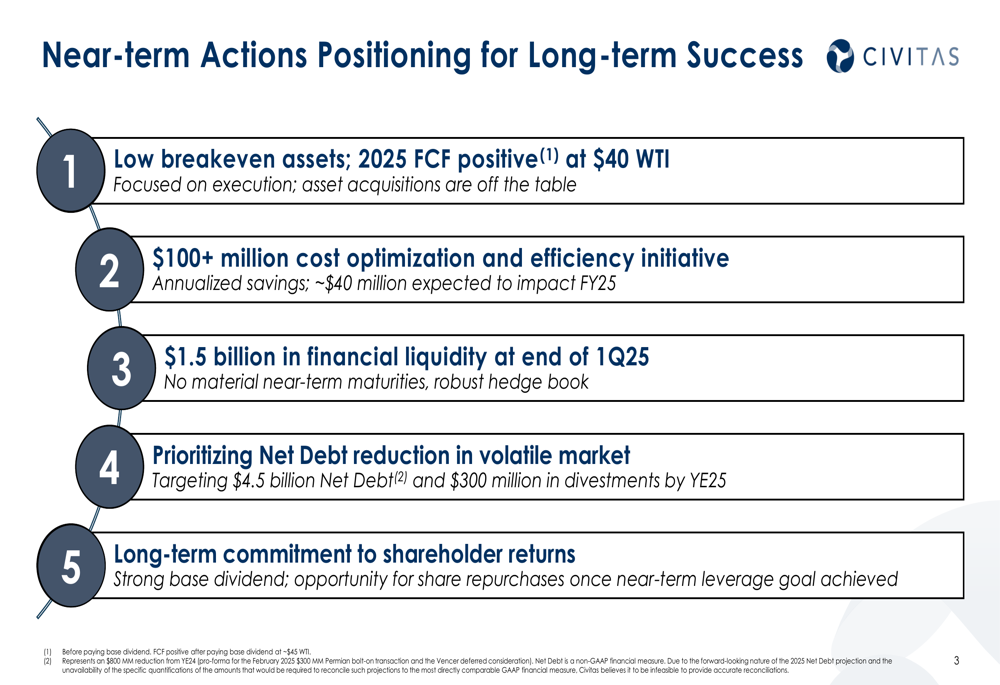

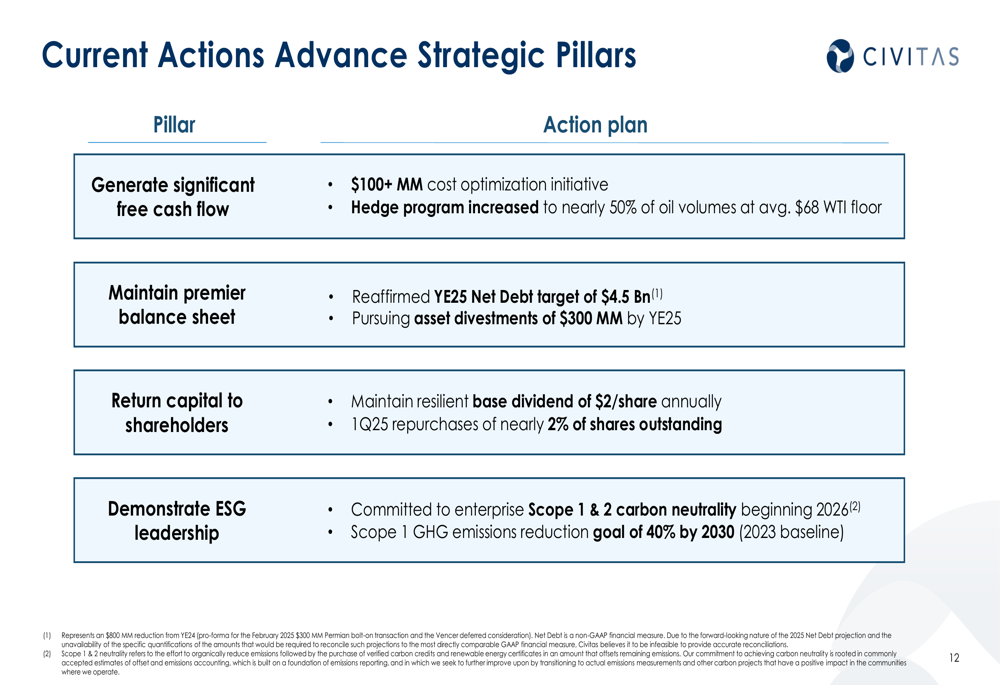

Civitas outlined five key near-term actions aimed at positioning the company for long-term success, with debt reduction taking center stage. The company is targeting a year-end 2025 Net Debt of $4.5 billion, representing an $800 million reduction from year-end 2024 levels (pro-forma for recent transactions).

The strategic roadmap emphasizes financial discipline and operational efficiency:

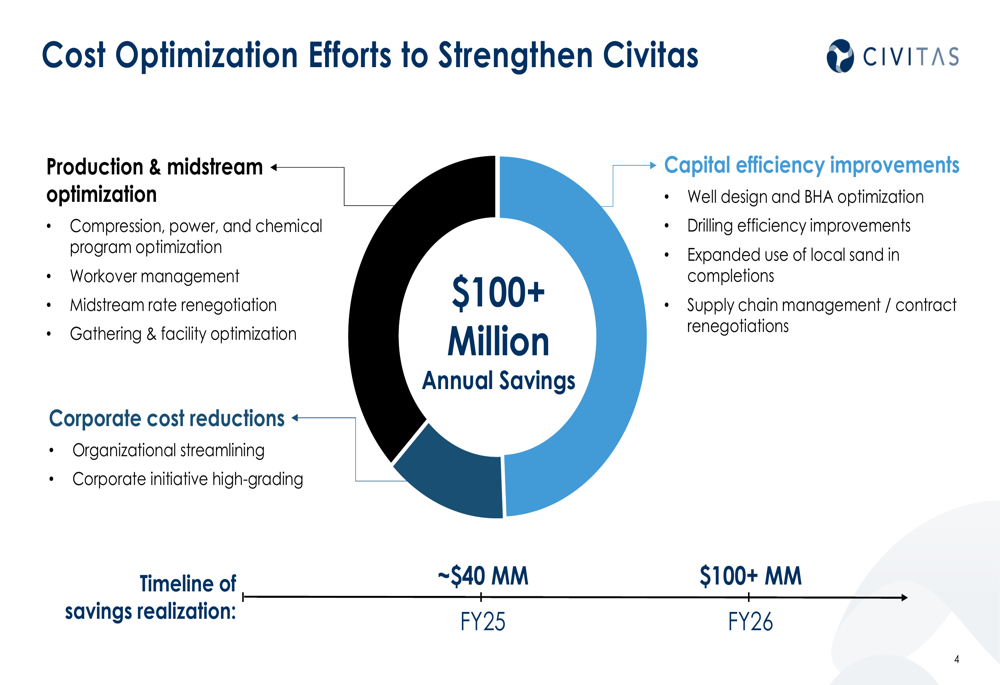

A cornerstone of Civitas’ strategy is its comprehensive cost optimization initiative, which targets over $100 million in annual savings. The program spans production and midstream optimization, corporate cost reductions, and capital efficiency improvements, with approximately $40 million in savings expected to impact fiscal year 2025 results.

Detailed Financial Analysis

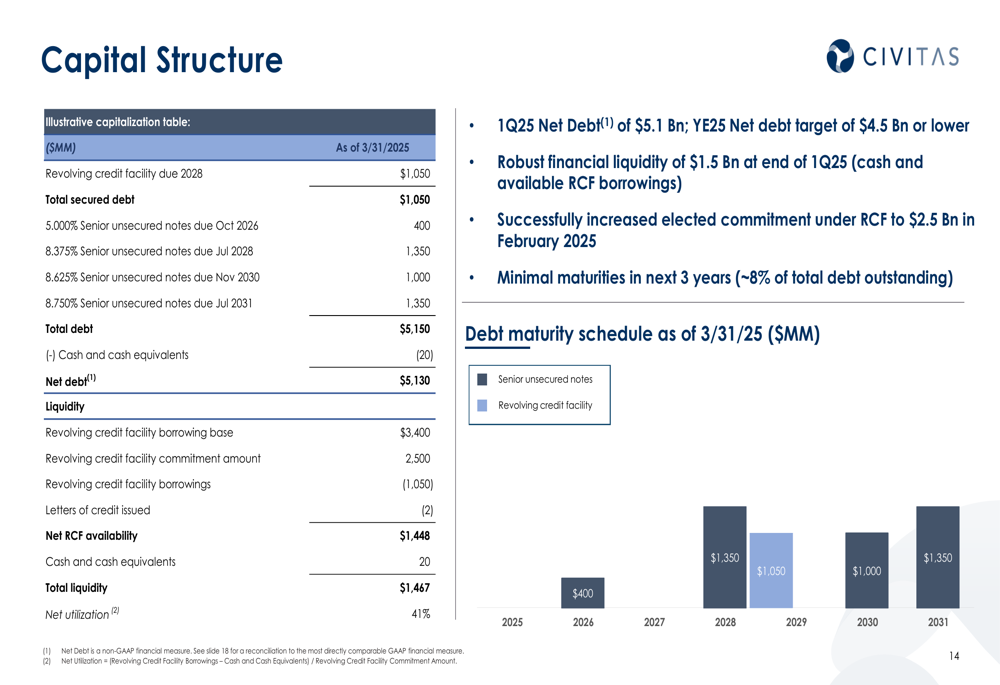

Civitas ended the first quarter with Net Debt of $5.1 billion and financial liquidity of $1.5 billion. The company successfully increased its elected commitment under its revolving credit facility to $2.5 billion in February 2025, providing additional financial flexibility.

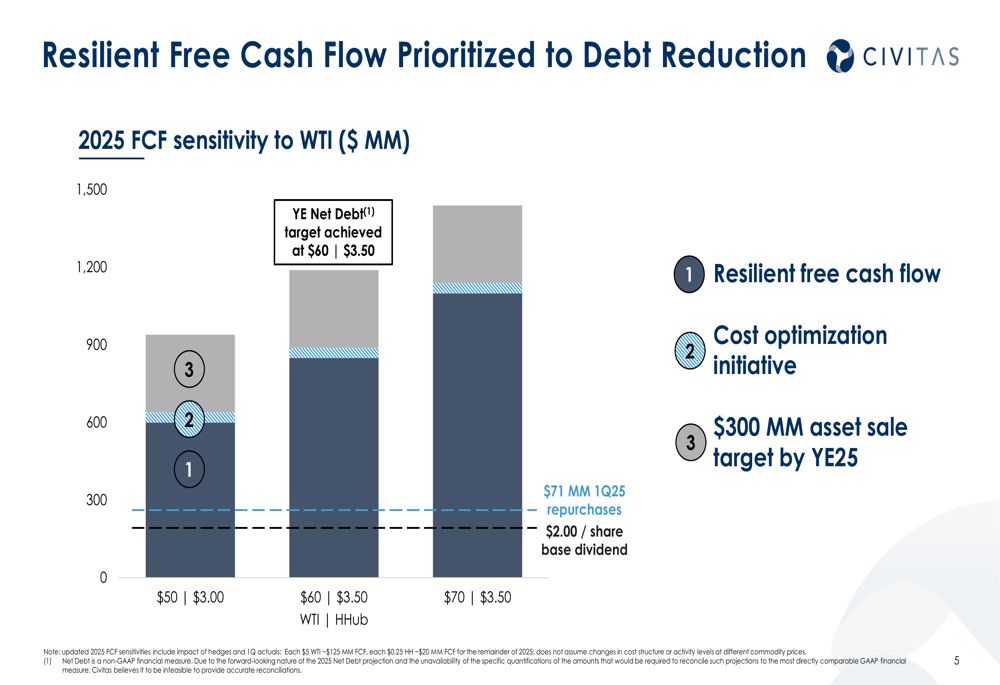

The company’s free cash flow sensitivity to oil prices demonstrates its path to achieving debt reduction targets:

At $60 WTI and $3.50 Henry Hub natural gas prices, Civitas expects to achieve its year-end Net Debt target. Should oil prices reach $70 WTI, the company could potentially repurchase additional shares or consider dividend increases. Management has also set a target of $300 million in asset sales by year-end 2025 to further support debt reduction efforts.

Civitas has strengthened its hedge position to secure cash flows in the volatile commodity price environment:

The company has increased oil hedging to nearly 50% of 2025 production, adding approximately 8 million barrels of hedges for 2Q25-1Q26 with average floor prices of around $68 per barrel. This provides significant downside protection while allowing for participation in potential price upside.

Competitive Industry Position

Civitas continues to advance its operations across both the Permian and DJ Basins. In the Permian, the company holds approximately 141,000 net acres across the Midland and Delaware Basins, with first quarter production of 164 MBoe/d. The Delaware Basin is emerging as a growth driver, with drilling cycle times approximately 10% faster than forecasted.

The following overview highlights Civitas’ Permian Basin operations:

In the DJ Basin, where Civitas holds approximately 357,000 net acres, the company achieved completions cycle times approximately 10% faster than planned and executed its first pad with 100% local sand utilization, driving savings of approximately $80,000 per well.

Forward-Looking Statements

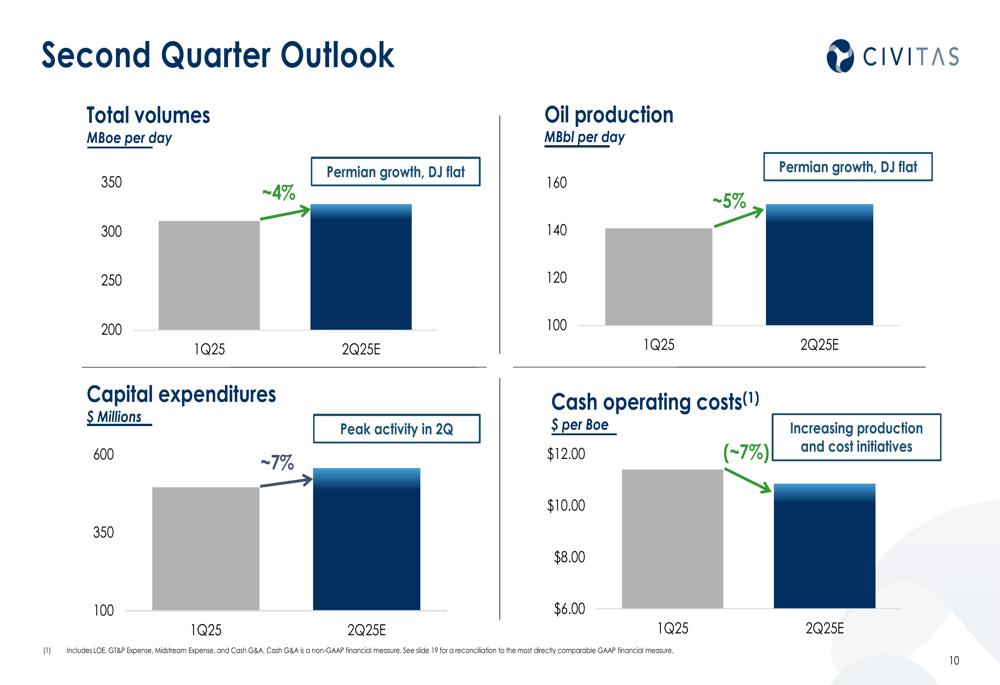

Civitas provided a positive outlook for the second quarter, projecting approximately 4% growth in total production volumes and 5% growth in oil production compared to the first quarter. This growth is expected to be driven primarily by Permian Basin operations, while DJ Basin production is forecast to remain flat.

The second quarter outlook shows improving operational metrics:

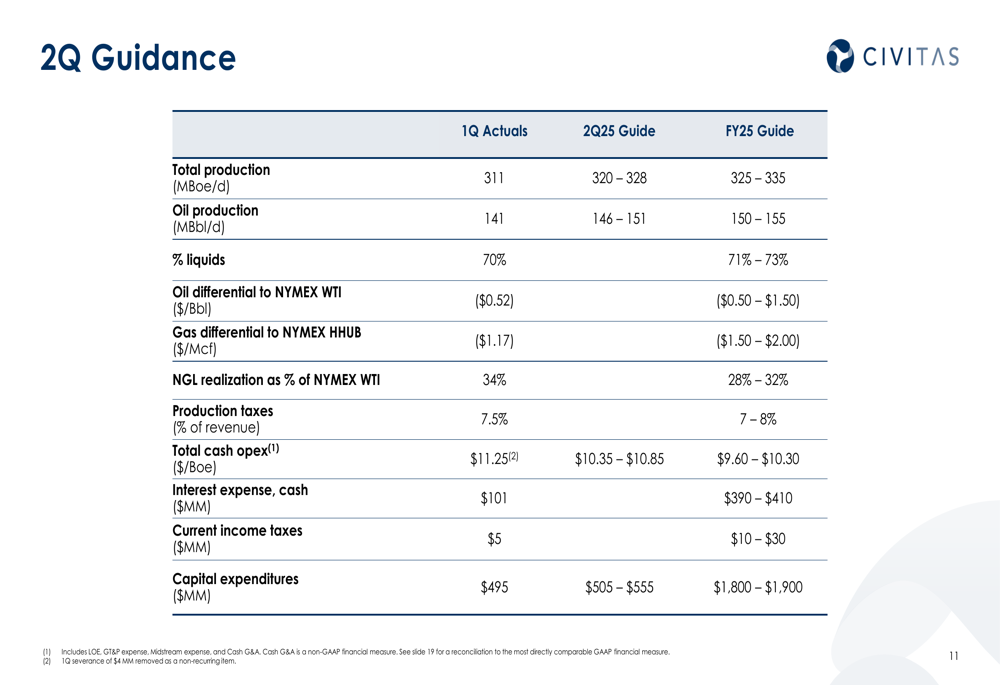

For the full year 2025, Civitas is guiding to:

- Total (EPA:TTEF) production of 325-335 MBoe/d

- Oil production of 150-155 MBbl/d

- Capital expenditures of $1.8-1.9 billion

- Cash operating costs of $9.60-10.30 per Boe

The company remains committed to its strategic pillars of generating significant free cash flow, maintaining a premier balance sheet, returning capital to shareholders, and demonstrating ESG leadership:

Executive Summary

Civitas Resources’ first quarter 2025 presentation reflects a company focused on financial discipline and operational efficiency in a challenging market environment. Following its fourth quarter 2024 earnings miss, management has prioritized debt reduction and cost optimization while maintaining its commitment to shareholder returns through a $2 per share annual base dividend.

The company’s capital structure shows minimal near-term debt maturities, providing runway to execute its strategic initiatives:

With production growth expected in the second quarter, particularly in the Permian Basin, and a comprehensive cost optimization program targeting over $100 million in annual savings, Civitas is positioning itself to strengthen its balance sheet while delivering value to shareholders. The company’s enhanced hedge position provides downside protection in a volatile commodity price environment, supporting its ability to generate free cash flow across various price scenarios.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.