Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

Comstock Resources, Inc. (NYSE:CRK) presented its first quarter 2025 results on April 30, 2025, highlighting improved financial performance driven primarily by higher natural gas prices, despite a year-over-year decline in production volumes. The natural gas producer, which focuses on the Haynesville and Bossier shale plays in East Texas and North Louisiana, has continued its strategic shift toward Western Haynesville development while maintaining operational efficiency.

Following strong Q4 2024 results that exceeded analyst expectations, Comstock’s stock has shown significant momentum, with shares rising 148% over the past year according to recent market data. The company’s Q1 2025 results continue to demonstrate resilience in a natural gas market that has seen improved pricing compared to early 2024.

Quarterly Performance Highlights

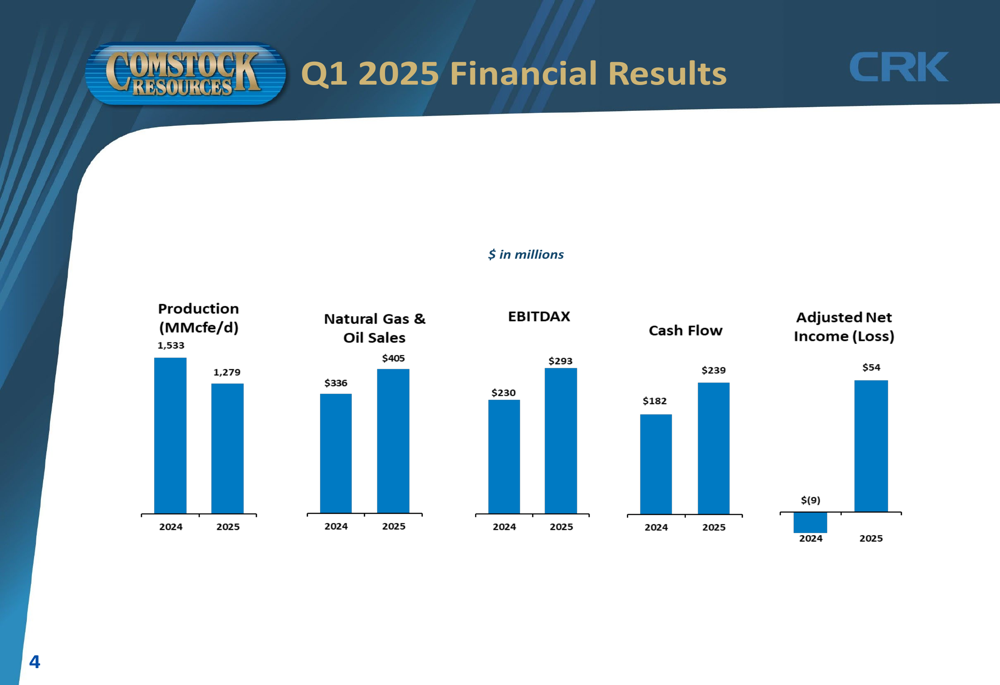

Comstock reported natural gas and oil sales of $405 million for Q1 2025, a 20.5% increase from $336 million in Q1 2024, despite production declining to 1,279 MMcfe/d from 1,533 MMcfe/d in the same period last year. The company generated operating cash flow of $239 million ($0.81 per diluted share), adjusted EBITDAX of $293 million, and adjusted net income of $53.8 million ($0.18 per diluted share).

As shown in the following chart comparing Q1 2025 financial results with Q1 2024:

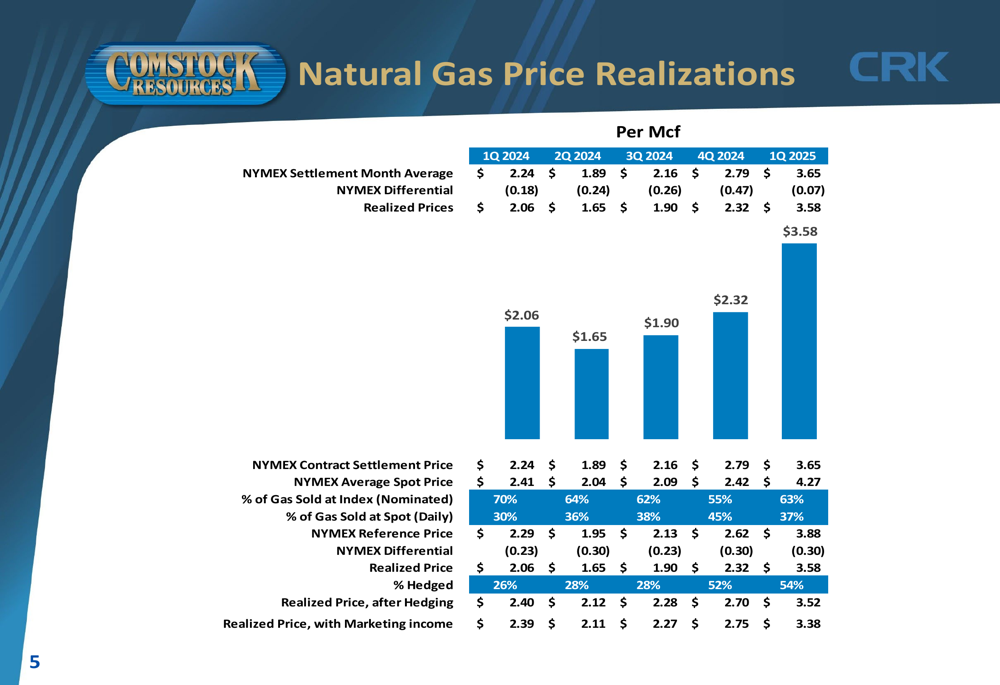

The improved financial performance was largely driven by higher natural gas price realizations, which reached $3.58 per Mcf in Q1 2025, compared to just $2.06 per Mcf in Q1 2024. This significant price improvement more than offset the production decline, allowing Comstock to swing from an adjusted net loss of $9 million in Q1 2024 to a profit of $54 million in Q1 2025.

The company’s natural gas price realizations over the past five quarters show a consistent upward trend:

Comstock has maintained its industry-leading cost structure, with Q1 2025 operating costs of $0.83 per Mcfe (including lifting costs of $0.30, gathering costs of $0.06, production and ad valorem taxes of $0.37, and G&A of $0.10). This efficient cost management has helped the company expand its EBITDAX margin from 61% in Q1 2023 to 76% in Q1 2025.

Operational Developments

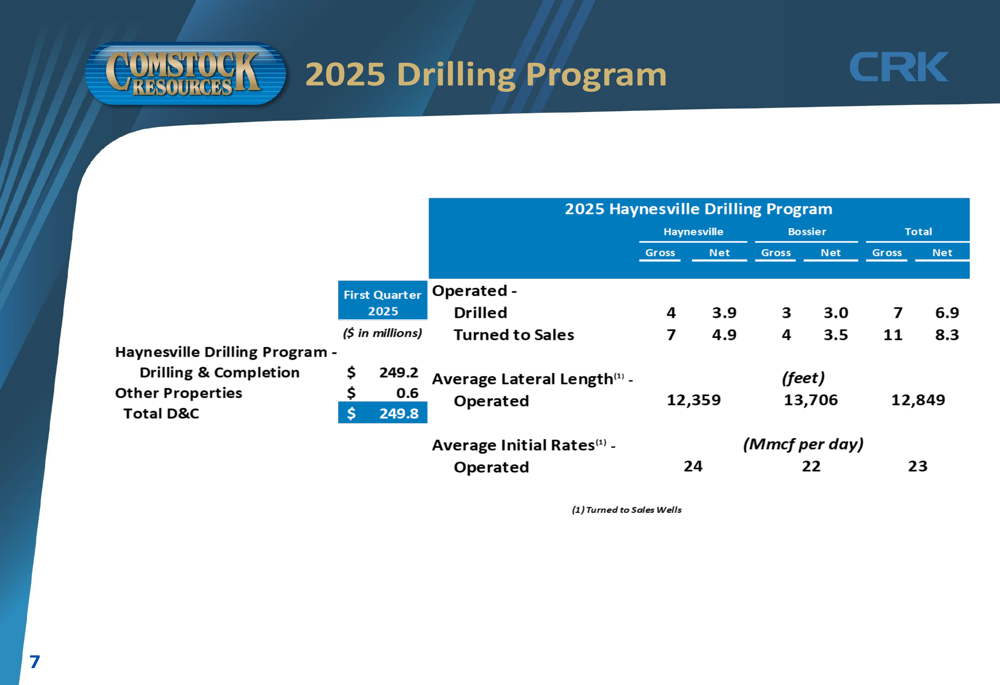

During Q1 2025, Comstock drilled 7 operated wells (4.9 net) in the Haynesville formation and 3 operated wells (3.0 net) in the Bossier formation. The company turned to sales 7 Haynesville wells (4.9 net) and 4 Bossier wells (3.5 net), with average initial production rates of 24 MMcf per day and 22 MMcf per day, respectively.

The following table details the company’s Q1 2025 drilling program:

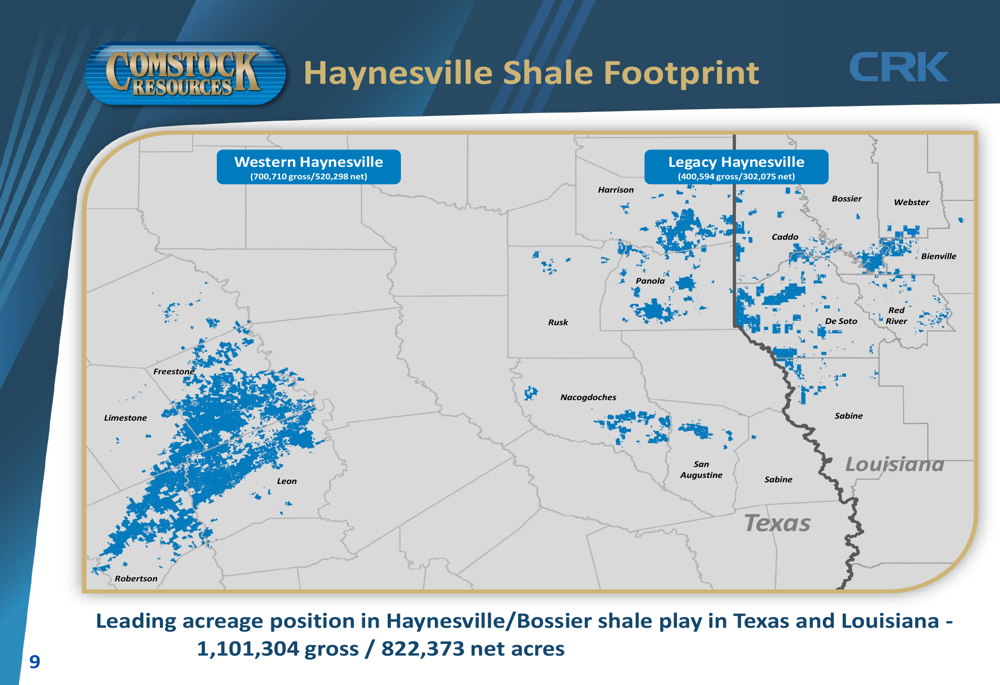

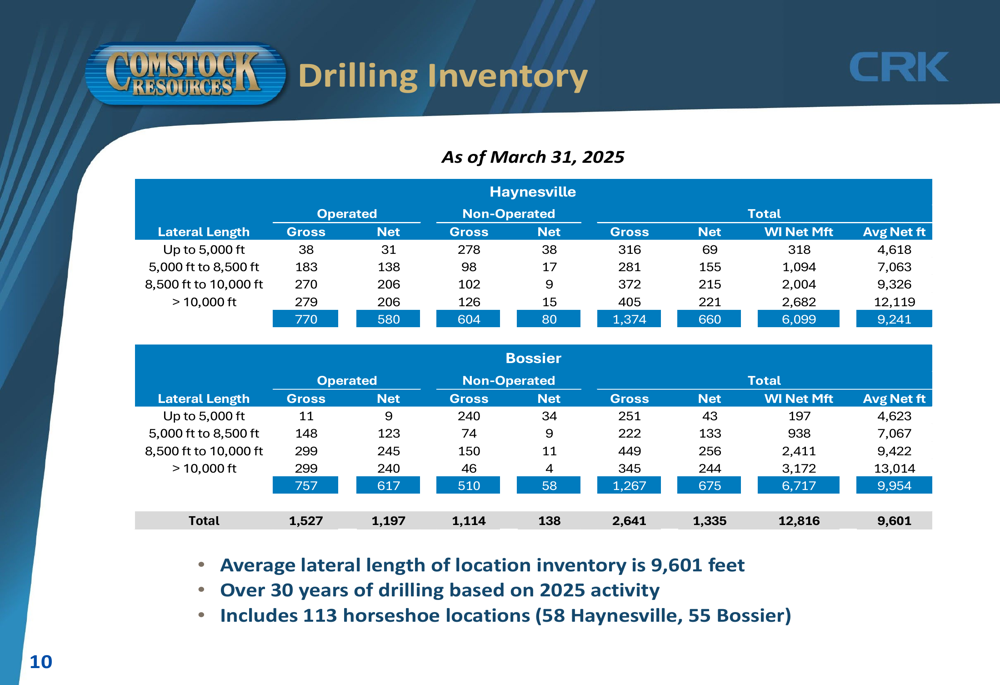

Comstock continues to expand its footprint in the Haynesville shale play, where it holds a leading acreage position of 1,101,304 gross acres (822,373 net acres) across Western Haynesville and Legacy Haynesville regions:

The company’s drilling inventory remains robust, with over 30 years of drilling locations based on 2025 activity levels. This includes 113 horseshoe locations (58 in Haynesville and 55 in Bossier), providing significant long-term growth potential.

Comstock has made notable progress in improving drilling efficiency, particularly in the Legacy Haynesville region, where footage drilled per day increased from 679 feet in 2017 to 1,027 feet in Q1 2025. Similarly, drilling costs per lateral foot in Legacy Haynesville decreased to $523 in Q1 2025 from higher levels in previous years.

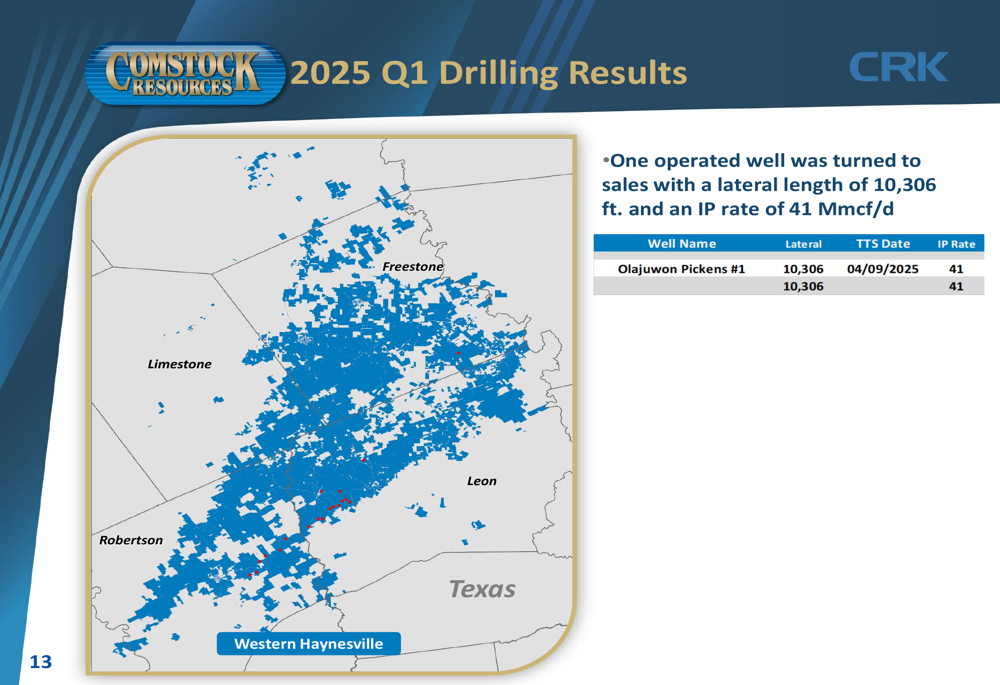

In the Western Haynesville area, the company highlighted a particularly successful well in Texas. As shown in the following drilling results:

Strategic Initiatives & Outlook

Looking ahead, Comstock’s 2025 strategy continues to focus on developing its Western Haynesville assets while maintaining operations in Legacy Haynesville. The company plans to operate four rigs in Western Haynesville to delineate the new play, expecting to drill 20 wells and turn 16 wells to sales in 2025. Additionally, three operated rigs will continue drilling in Legacy Haynesville, with plans to drill 25 wells and turn 31 wells to sales this year.

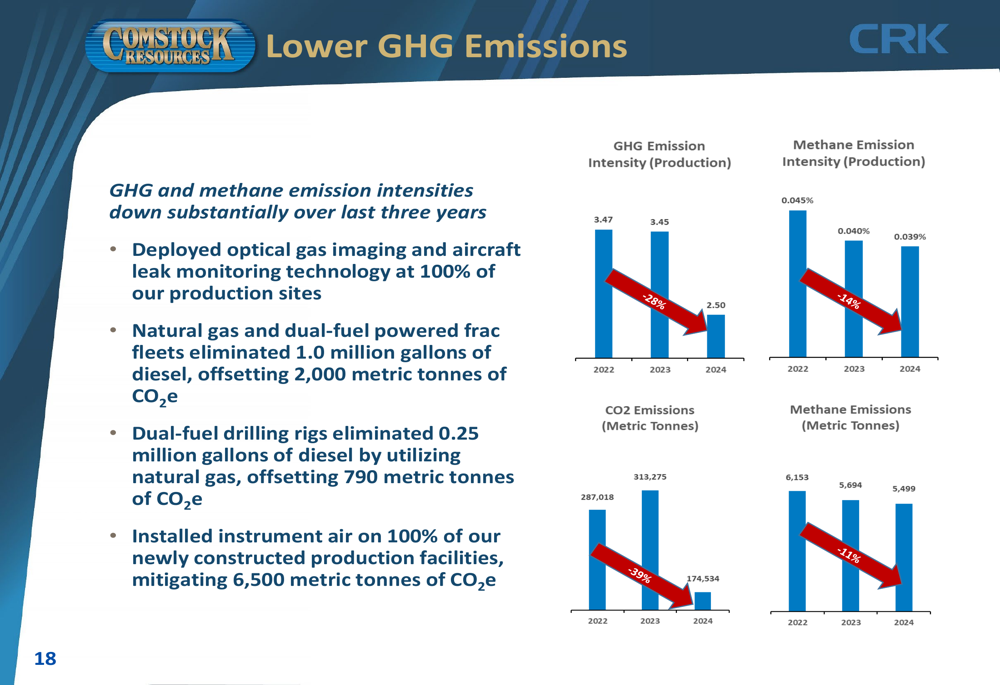

The company has made significant progress in reducing its environmental footprint, with substantial decreases in GHG and methane emission intensities over the past three years:

For 2025, Comstock provided guidance for production between 1,300 and 1,400 MMcfe/d, with drilling and completion costs projected at $1,000-$1,100 million. The company expects to fund its drilling program entirely from operating cash flow, highlighting its improved financial position.

Financial Position

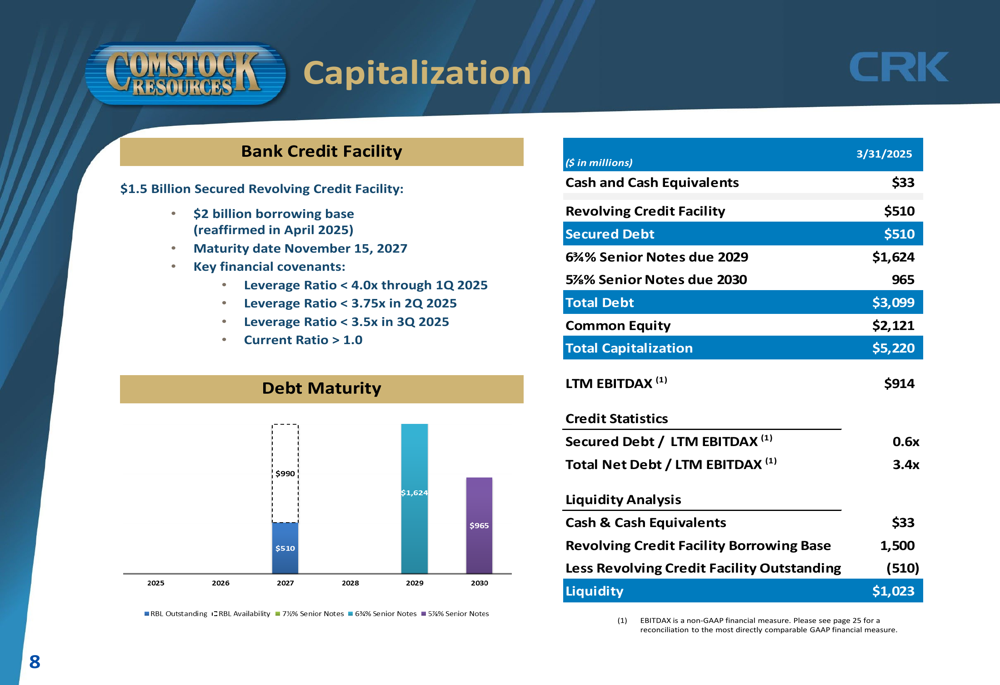

As of March 31, 2025, Comstock reported total debt of $3,099 million, with a net debt to LTM EBITDAX ratio of 3.4x. The company maintained strong liquidity of $1,023 million, including $33 million in cash and cash equivalents and availability under its revolving credit facility.

The company’s debt maturity schedule is well-structured, with no significant maturities until 2029, when $1,624 million in 6.75% Senior Notes come due, followed by $965 million in 5.875% Senior Notes due in 2030.

Despite the free cash deficit of $9.7 million in Q1 2025 (after capital expenditures of $249.8 million), this represents a significant improvement from the $143 million deficit in Q1 2024. The company expects its Western Haynesville midstream development to require $130-$150 million in 2025, which will be funded entirely by its midstream partner.

With natural gas prices showing improvement and operational efficiencies continuing to advance, Comstock appears well-positioned to capitalize on its extensive Haynesville/Bossier acreage while maintaining financial discipline and advancing its environmental initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.