AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

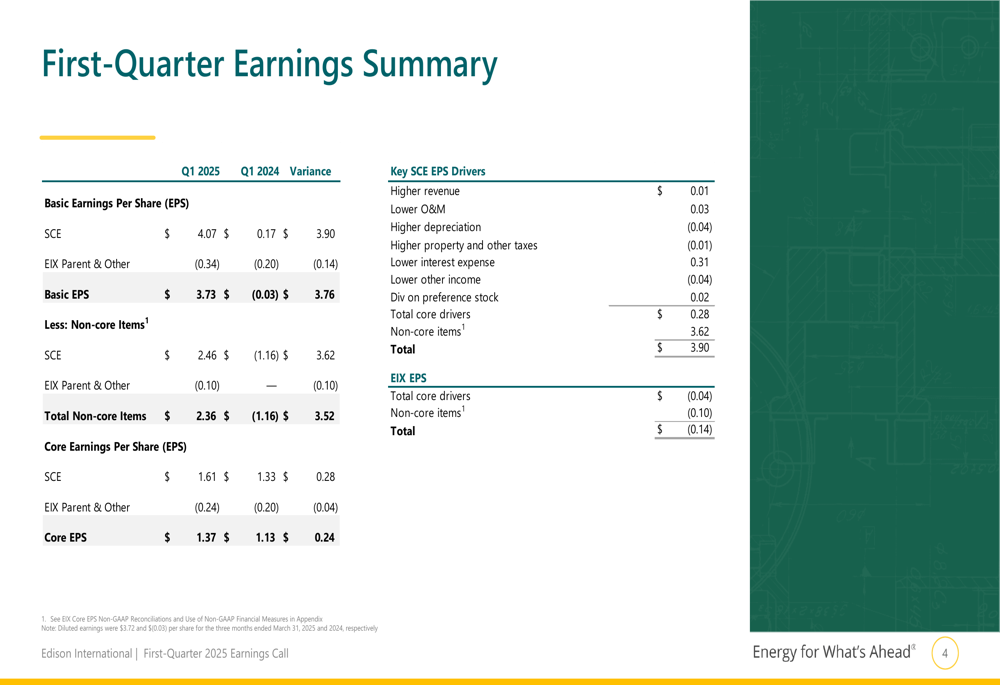

Edison International (NYSE:EIX) presented its first-quarter 2025 financial results on April 29, showing significant year-over-year earnings growth despite falling short of analyst expectations. The utility company reported core earnings per share of $1.37, representing a 21% increase from $1.13 in Q1 2024, but slightly below the forecast of $1.41.

Following the earnings announcement, Edison’s stock declined 1.24% in after-hours trading to $57.72, reflecting investor disappointment over the earnings miss. The company’s revenue of $3.81 billion also fell short of the expected $4.4 billion, creating additional pressure on the stock, which has already experienced a 28% decline over the past six months.

Quarterly Performance Highlights

Edison’s first-quarter results showed a dramatic improvement in basic EPS, which reached $3.73 compared to a loss of $(0.03) in the same period last year. This substantial increase was largely driven by non-core items, particularly related to the settlement of legacy wildfire issues.

As shown in the following quarterly earnings summary:

The core EPS of $1.37 was primarily driven by Southern California Edison’s (SCE) performance, which contributed $1.61 per share, partially offset by Edison International parent and other costs of $(0.24) per share. Key drivers for SCE’s improved performance included lower interest expense (+$0.31) and lower operations and maintenance costs (+$0.03), partially offset by higher depreciation (-$0.04) and lower other income (-$0.04).

Capital Investment & Growth Strategy

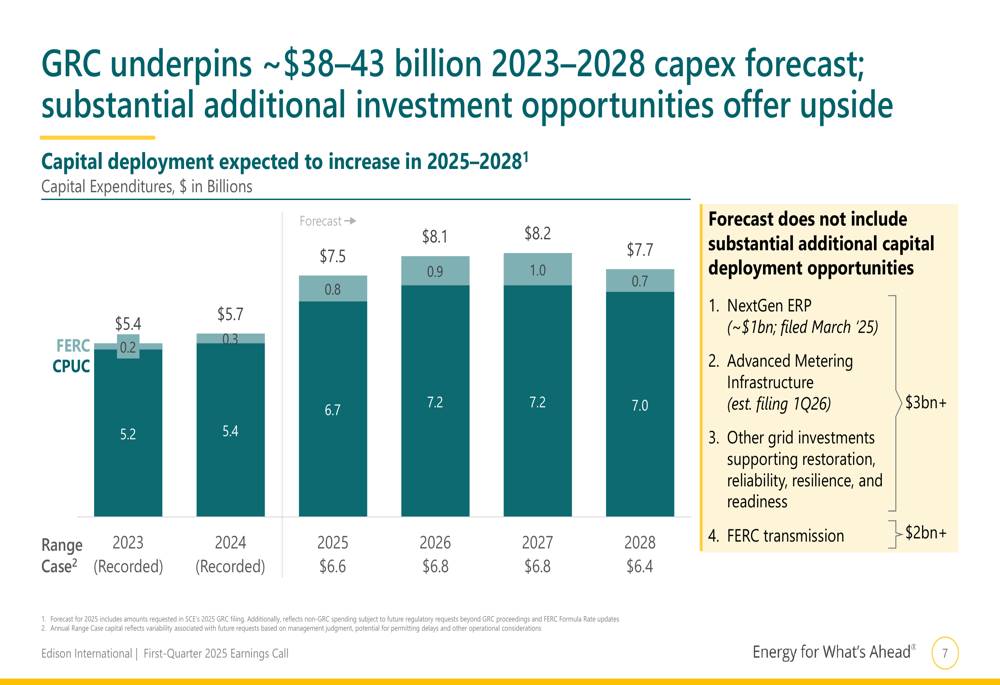

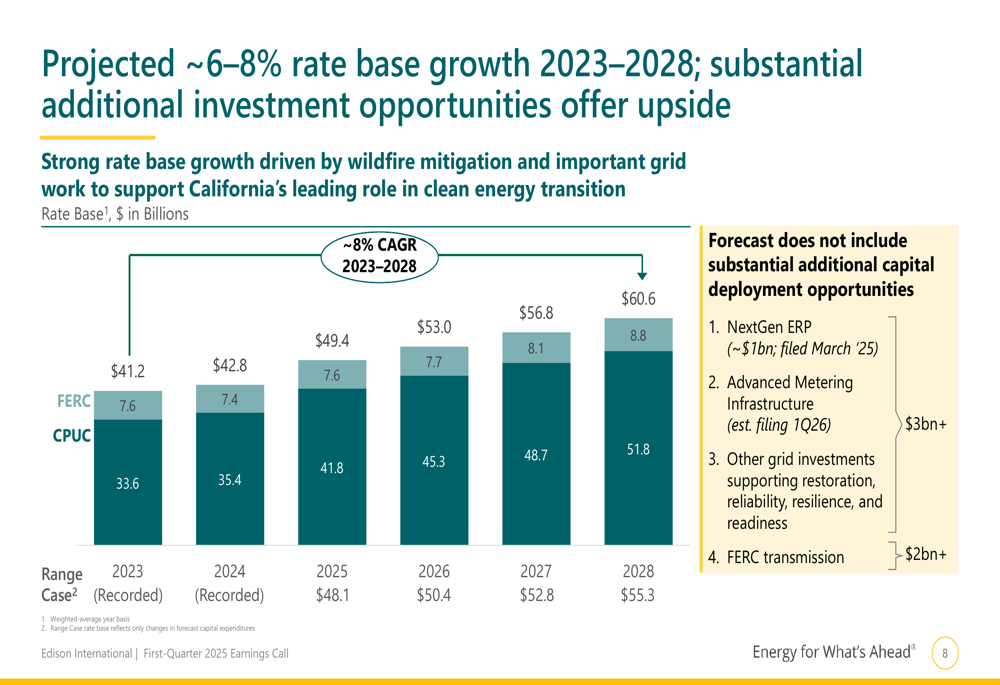

Edison reaffirmed its ambitious capital expenditure plan of approximately $38-43 billion for 2023-2028, with spending expected to increase significantly in the coming years. This investment strategy is primarily focused on wildfire mitigation and grid infrastructure to support California’s clean energy transition.

The company’s capital deployment is projected to grow substantially from 2025 through 2028, as illustrated in this capital expenditure forecast:

This investment is expected to drive rate base growth of approximately 6-8% annually from 2023 to 2028, with the rate base projected to increase from $42.8 billion in 2024 to $60.6 billion by 2028:

Edison’s management emphasized that these forecasts do not include substantial additional capital deployment opportunities, such as the NextGen Enterprise Resource Planning program (~$1 billion, filed March 2025) and Advanced Metering Infrastructure (>$3 billion, expected filing in Q1 2026).

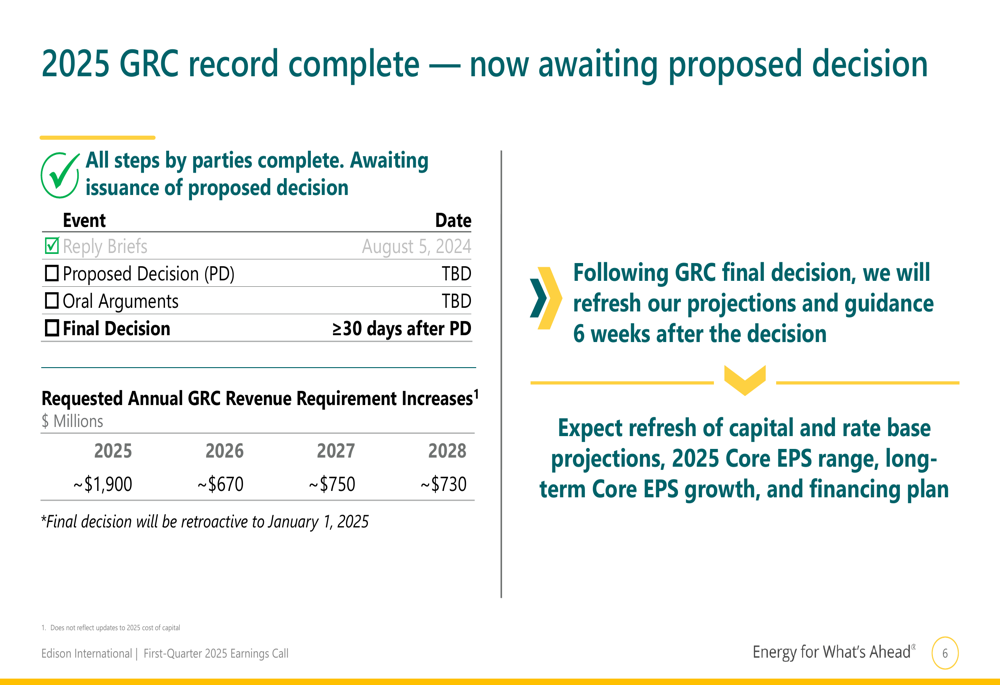

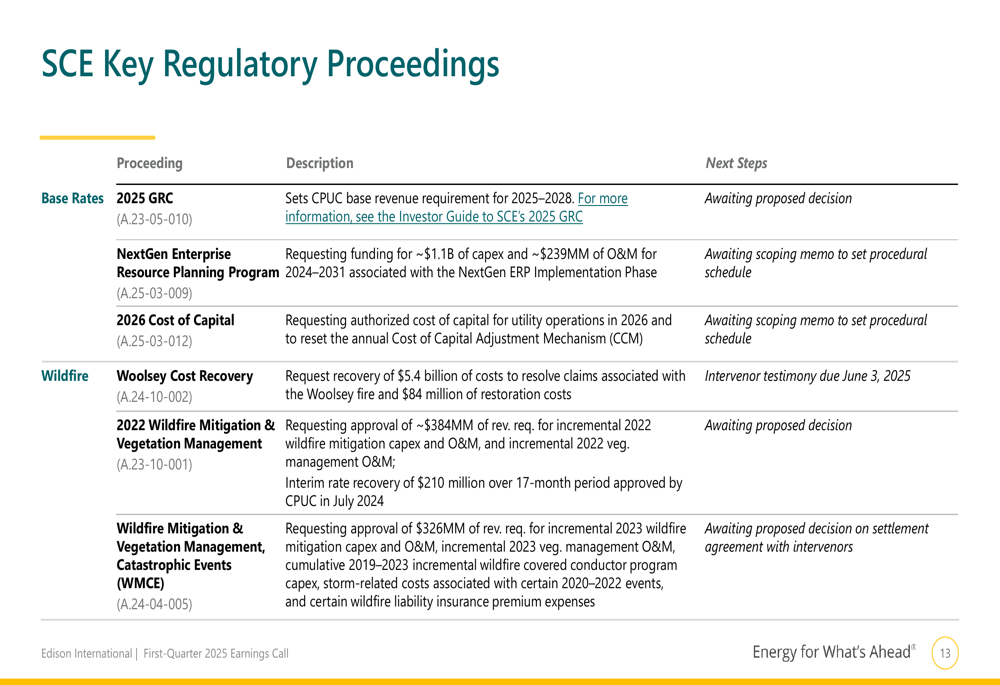

Regulatory Proceedings & Risk Management

The company highlighted significant progress in resolving legacy wildfire issues, with the Thomas, Koenigstein, and Montecito (TKM) settlement approved and accounted for in first-quarter results. The settlement, valued at approximately $1.6 billion, has strengthened Edison’s balance sheet by offsetting normal-course debt issuances.

The following slide details the status of legacy wildfire resolutions:

Meanwhile, the Woolsey fire cost recovery proceeding continues, with Edison requesting approximately $5.4 billion. The regulatory timeline extends into the first quarter of 2026, with various milestones throughout 2025.

In March 2025, Edison filed its 2026 cost of capital application, requesting an ROE of 11.75% compared to the 2025 authorized level of 10.33%. The company cited ongoing wildfire risk and its role in advancing California’s clean energy goals as key drivers for the increase:

Forward-Looking Statements

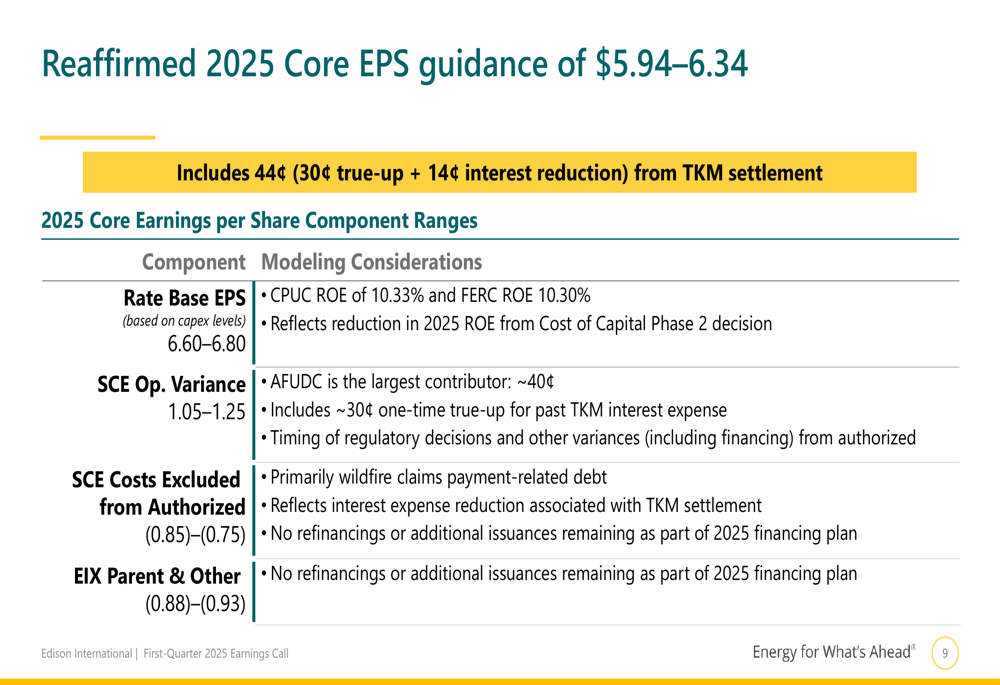

Edison reaffirmed its 2025 core EPS guidance range of $5.94 to $6.34, which includes a 44¢ contribution from the TKM settlement (30¢ true-up plus 14¢ interest reduction):

Looking beyond 2025, the company expects 5-7% core EPS growth for 2025-2028, underpinned by the strong rate base growth of approximately 6-8%. This growth projection is supported by Edison’s 2025-2028 consolidated financing plan, which shows minimal equity needs:

CEO Pedro Pizarro expressed confidence in meeting the 2025 EPS guidance and delivering the projected 5-7% core EPS compound annual growth rate through 2028. CFO Maria Rigatti added that the company is well-positioned for growth due to a strong regulatory backdrop and robust rate base growth, coupled with significant needs for incremental grid investment.

Edison continues to maintain a strong dividend profile with a current yield of approximately 6% and 21 consecutive years of dividend growth. The company expects substantial load growth in the coming decades, projecting 35% growth by 2035 and 80% by 2045, driven by California’s electrification initiatives.

Despite these positive projections, investors should note that Edison faces ongoing regulatory challenges, wildfire-related liabilities, and potential fluctuations in capital expenditure needs that could impact financial stability. The company’s ability to secure favorable regulatory outcomes, particularly regarding the 2026 cost of capital application and Woolsey fire cost recovery, will be critical factors in achieving its long-term growth objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.