U.S. stock futures slip lower; Cook’s firing increases Fed independence worries

Introduction & Market Context

Essential Properties Realty Trust (NYSE:EPRT) released its Q2 2025 investor presentation on July 24, highlighting strong portfolio performance and continued investment activity. The net lease REIT maintained near-full occupancy while deploying significant capital into new properties, despite having reported a slight earnings miss in Q1 2025.

The company’s stock closed at $30.87 on July 23, down 0.94% for the day and trading below its 52-week high of $34.88. According to recent earnings data, EPRT missed Q1 2025 EPS forecasts by $0.01 but exceeded revenue expectations, suggesting mixed but generally positive operational performance.

Quarterly Performance Highlights

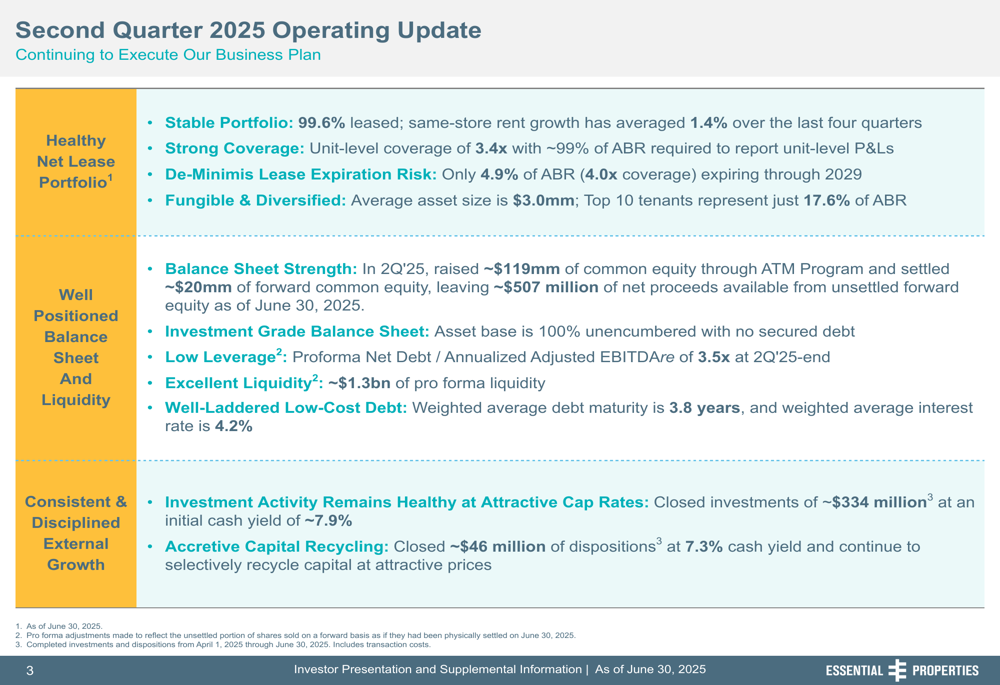

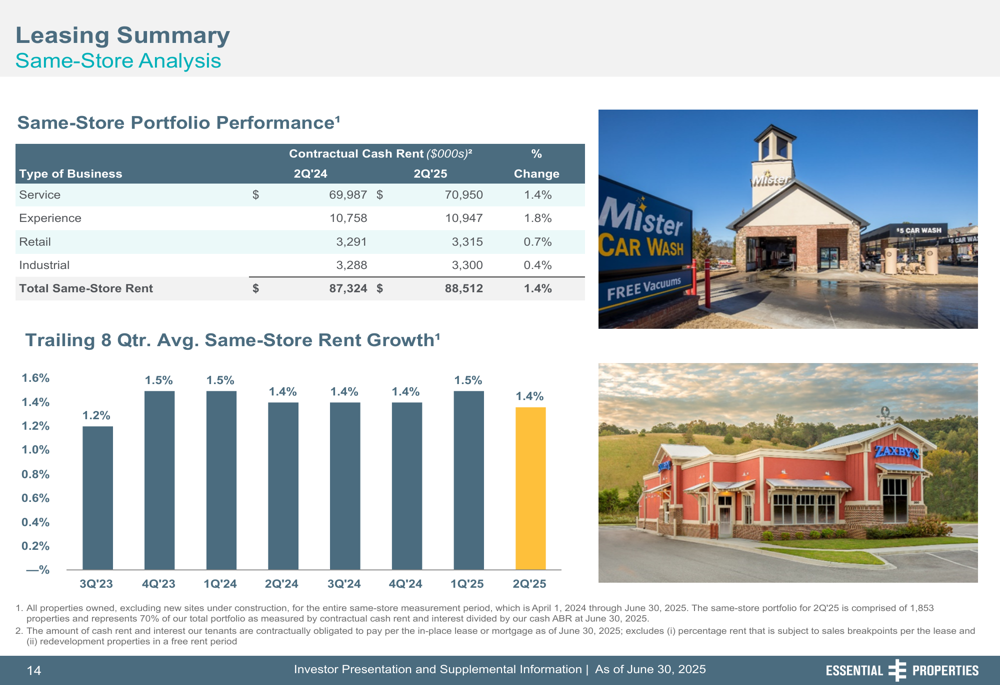

Essential Properties reported a remarkably healthy portfolio for Q2 2025, achieving 99.6% occupancy with 1.4% same-store rent growth. The company highlighted its low lease expiration risk, with only 4.9% of leases expiring through 2029, providing significant revenue visibility.

As shown in the following quarterly operating update, the company completed approximately $334 million of new investments at an attractive 7.9% initial cash yield, while disposing of approximately $46 million in properties at a 7.3% cash yield:

The company’s portfolio demonstrated consistent performance across property types, with service-oriented properties showing 1.4% same-store rent growth and experiential properties growing at 1.8% when comparing Q2 2024 to Q2 2025. This steady growth pattern has been maintained over recent quarters, with trailing eight-quarter average same-store rent growth between 1.2% and 1.5%.

Portfolio Composition and Strategy

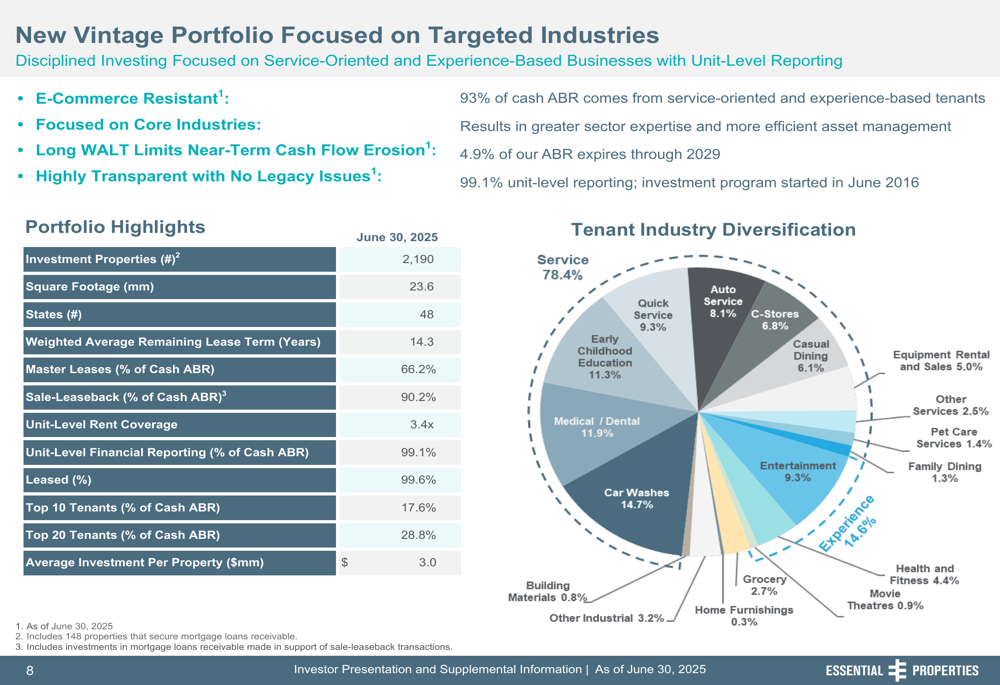

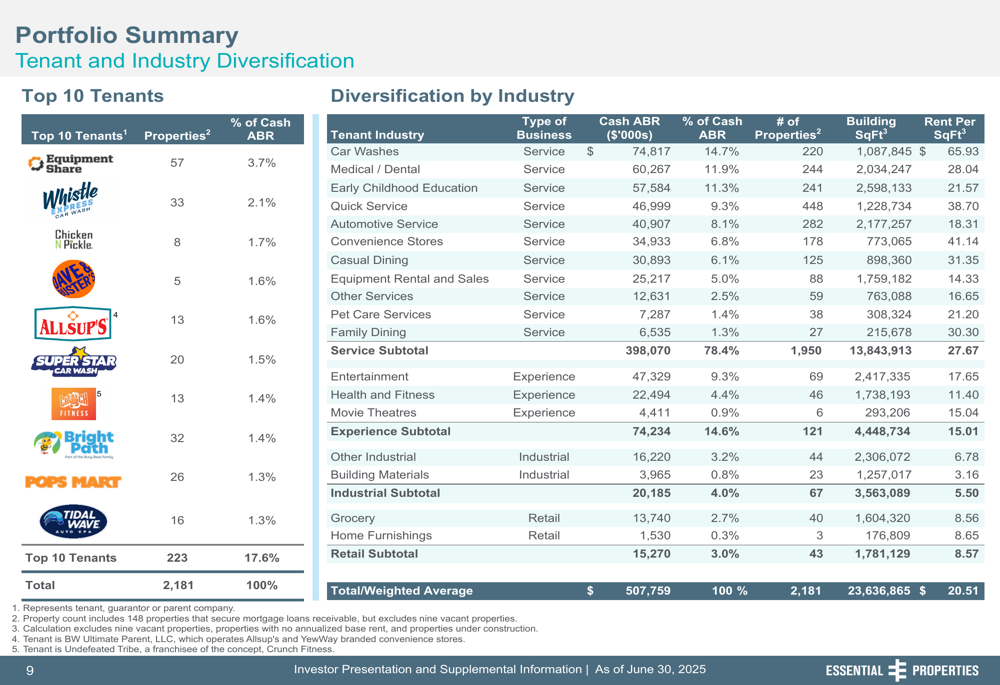

Essential Properties continues to differentiate itself through its focus on service-oriented and experiential properties, which together comprise 93% of its portfolio. The company maintains a highly diversified tenant base, with its top 10 tenants representing just 17.6% of annualized base rent (ABR), significantly lower than industry peers.

The following chart illustrates the company’s tenant and industry diversification:

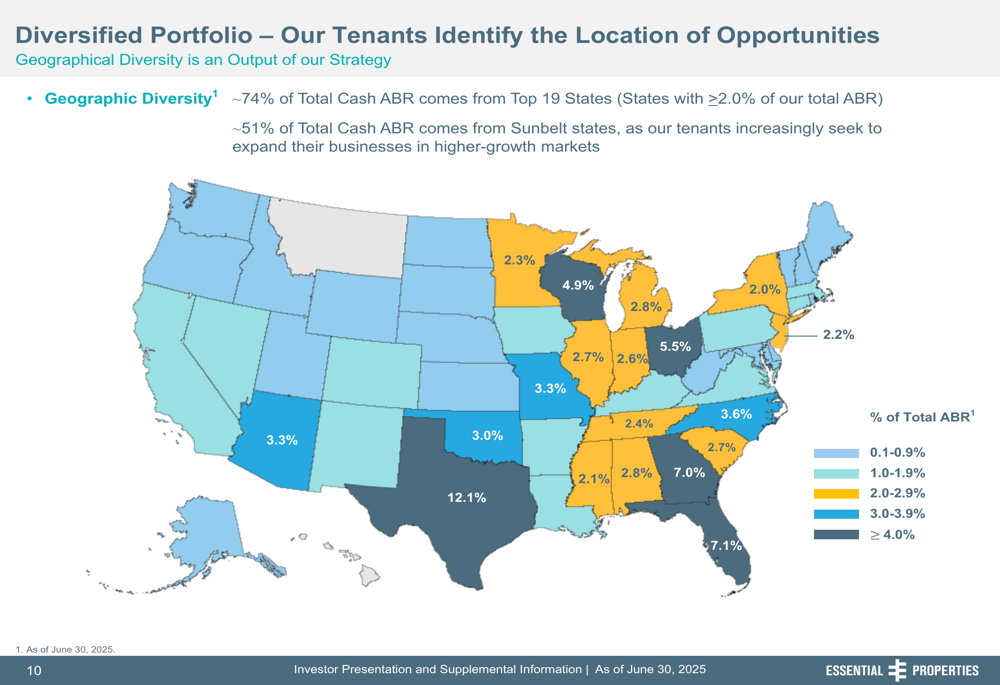

Geographically, the portfolio shows strategic concentration in high-growth markets, with approximately 51% of total cash ABR coming from Sunbelt states. Texas represents the largest state exposure at 12.1% of ABR, reflecting the company’s focus on expanding in regions with favorable demographic trends.

A key strength of Essential Properties’ portfolio is its tenant financial transparency and strong unit-level performance. The presentation highlighted that 99.1% of tenants provide unit-level financial reporting, and 70% of cash ABR comes from properties with rent coverage ratios of 2.0x or higher, indicating strong tenant financial health.

Investment Activity and Growth

The company’s external growth strategy showed consistent momentum throughout recent quarters. Investment volume increased from $213 million in Q3 2023 to $334 million in Q2 2025, with cash cap rates remaining attractive in the 7.6%-8.1% range.

The following chart details the company’s investment activity over the past several quarters:

Notably, 93% of Q2 2025 investments were sale-leaseback transactions, and 88% involved existing tenant relationships. This high percentage of repeat business demonstrates the company’s ability to leverage established relationships for growth while maintaining disciplined underwriting standards.

Financial Position and Liquidity

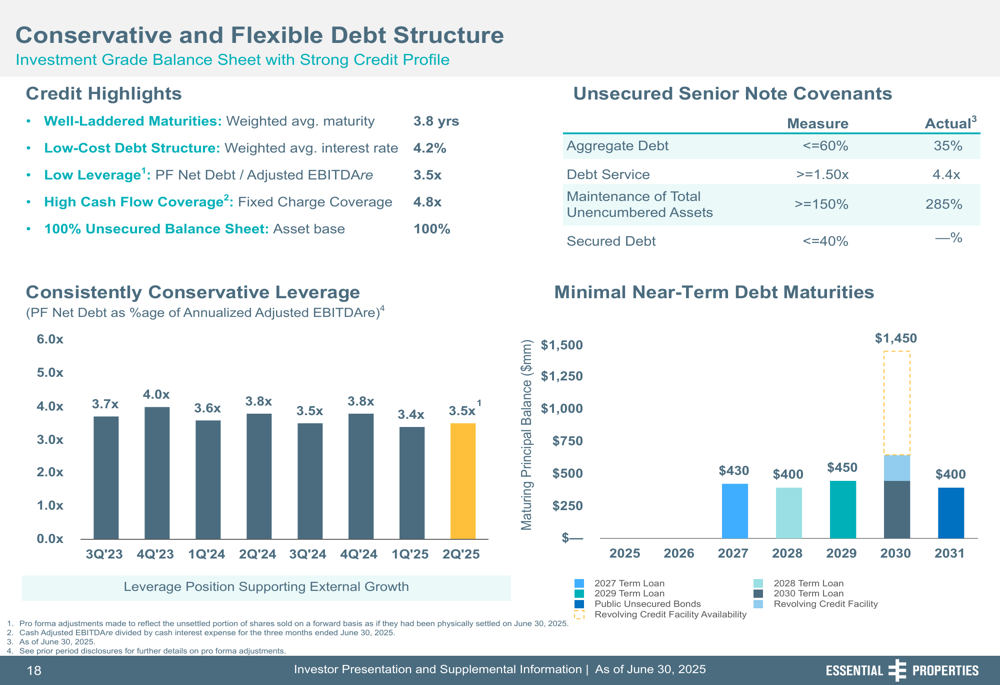

Essential Properties emphasized its conservative financial profile, featuring an investment-grade balance sheet with a low leverage ratio of 3.5x proforma net debt to annualized adjusted EBITDAre. The company’s debt structure is well-laddered with a weighted average maturity of 3.8 years and an average interest rate of 4.2%.

The presentation highlighted the company’s strong liquidity position of approximately $1.3 billion, consisting of cash, unused revolver capacity, and unsettled forward equity:

This substantial liquidity provides significant capacity for continued investment activity without immediate need for additional capital raising. The company also noted its conservative 65% payout ratio, which generates approximately $130 million in retained free cash flow annually for reinvestment.

Competitive Positioning

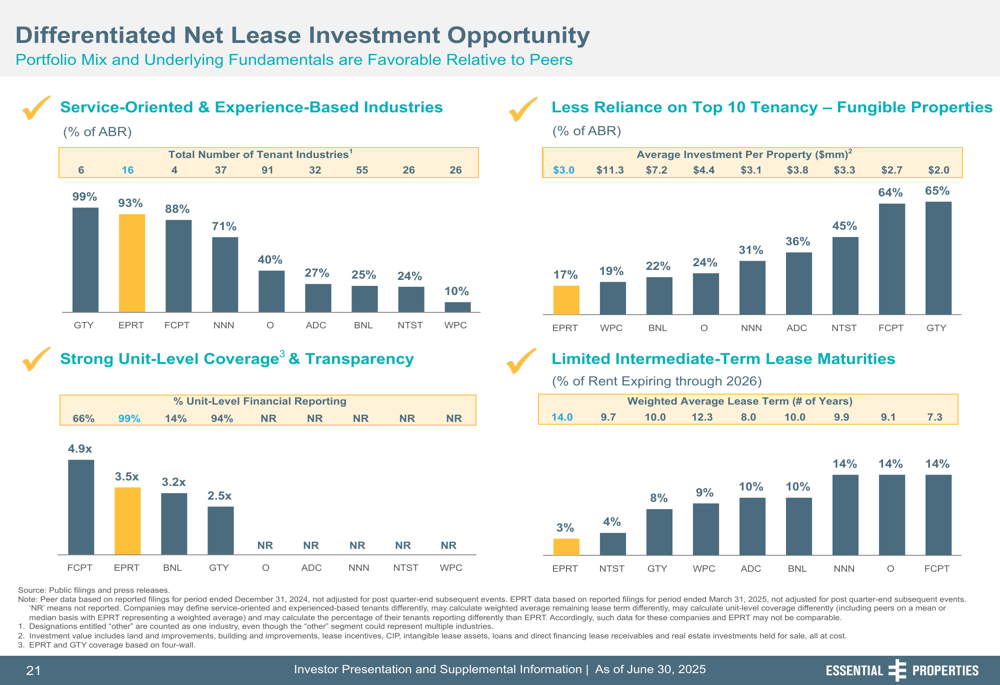

Essential Properties positioned itself as a differentiated investment opportunity within the net lease REIT sector. The presentation compared EPRT to peers across several key metrics, highlighting its higher concentration in service-oriented and experiential industries, lower tenant concentration risk, stronger unit-level coverage, and lower leverage.

The following chart illustrates these competitive advantages:

The company also highlighted its relative valuation metrics, showing that despite projecting higher 2025E AFFO per share growth of approximately 8% compared to most peers, EPRT trades at a discount to its net asset value (NAV).

Forward Outlook

While the Q2 presentation did not provide explicit forward guidance, the company’s strong liquidity position and consistent investment activity suggest continued growth potential. In its Q1 2025 earnings call, management reaffirmed AFFO per share guidance of $1.85-$1.89 for full-year 2025 and expressed confidence in achieving the upper half of its $900 million to $1.1 billion investment target for the year.

The presentation’s emphasis on the company’s differentiated business model, strong tenant relationships, and conservative financial position indicates management’s confidence in sustaining its growth trajectory despite potential economic uncertainties. With 88% of Q2 investments coming from repeat business and a healthy investment pipeline, Essential Properties appears well-positioned to continue its disciplined growth strategy through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.