U.S. stock futures slip lower; Cook’s firing increases Fed independence worries

Introduction & Market Context

Everus Construction Group Inc. (NYSE:ECG) presented its first quarter 2025 financial results on May 14, 2025, revealing substantial growth driven primarily by data center construction and other high-tech infrastructure projects. The market has responded enthusiastically to the results, with ECG shares jumping 15.69% in premarket trading to $59.49, significantly outpacing the company’s 52-week range of $31.38 to $77.93.

The construction services provider demonstrated strong momentum across most key financial metrics, continuing a multi-year growth trajectory while maintaining consistent margins despite rapid expansion.

Quarterly Performance Highlights

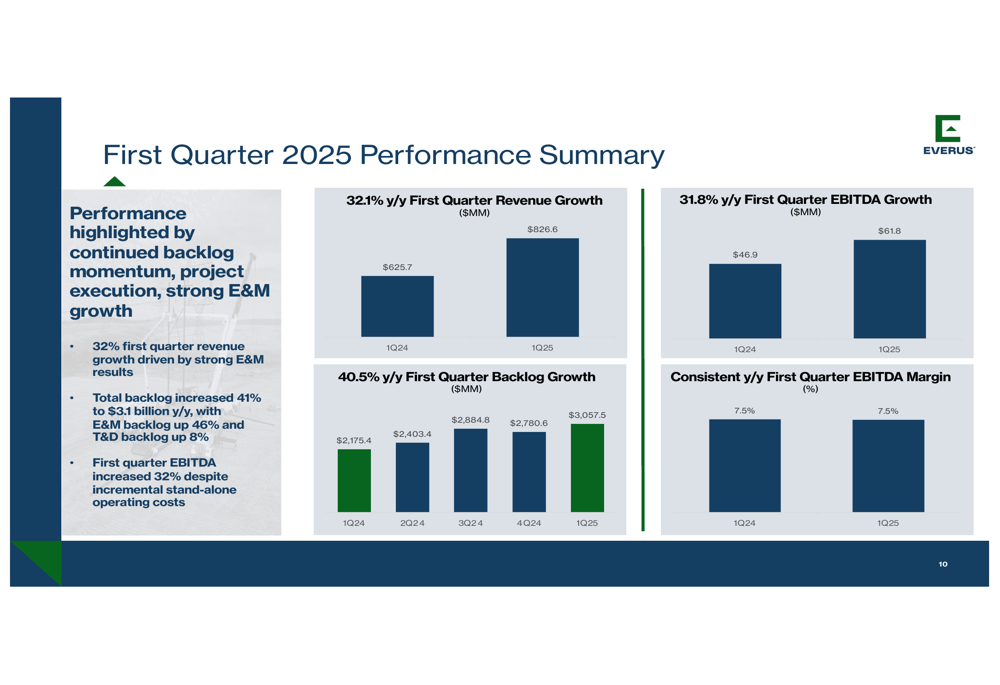

Everus reported impressive financial results for Q1 2025, with revenue reaching $826.6 million, a 32.1% increase compared to $625.7 million in Q1 2024. EBITDA grew at a similar pace, rising 31.8% year-over-year to $61.8 million, while maintaining a steady EBITDA margin of 7.5%.

The company’s backlog, a critical indicator of future revenue potential, showed even stronger growth, expanding 40.5% year-over-year to reach $3.1 billion. This substantial backlog provides Everus with enhanced visibility into future quarters and supports the company’s full-year guidance.

As shown in the following performance summary chart, Everus has demonstrated consistent growth across its key financial metrics:

Net income for the quarter reached $36.7 million, up from $28.2 million in the same period last year, representing a 30.1% increase. This strong bottom-line performance reflects the company’s ability to efficiently convert its growing revenue into profits despite the challenges of rapid expansion.

Segment Analysis

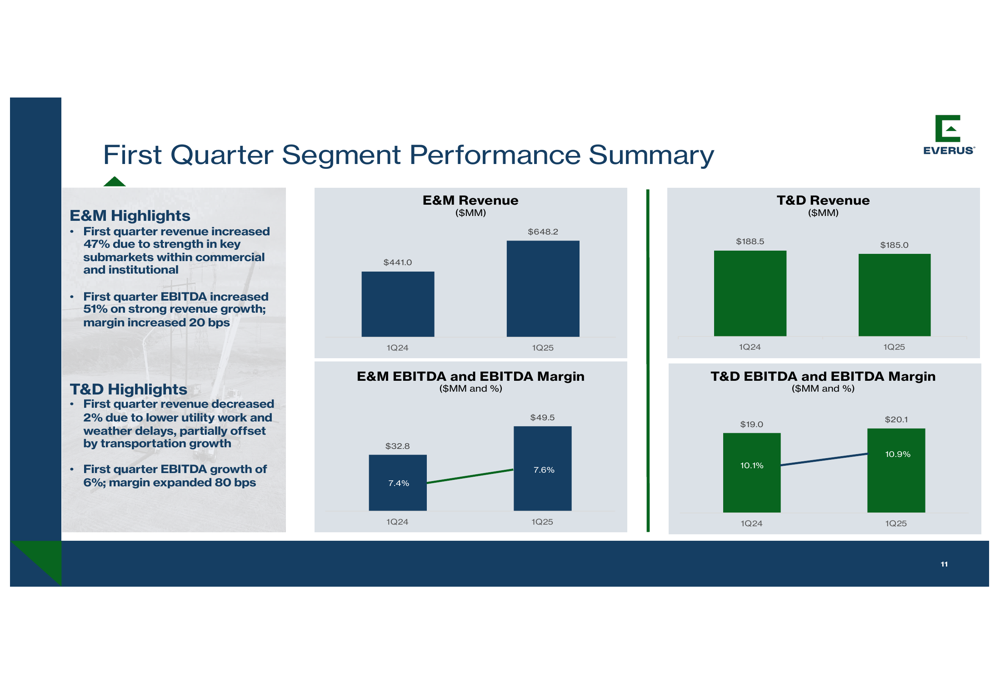

Everus’s performance was driven by particularly strong results in its Electrical & Mechanical (E&M) segment, which saw revenue surge 47% to $648.2 million. The E&M segment’s EBITDA grew even faster, increasing 51% year-over-year, demonstrating the company’s ability to improve profitability while scaling operations. This growth was primarily attributed to increased data center construction activity, a sector experiencing robust demand due to AI infrastructure expansion.

The Transmission & Distribution (T&D) segment presented a different picture, with revenue declining slightly by 2% to $185.0 million. However, despite the revenue dip, the segment’s EBITDA increased by 6%, indicating improved operational efficiency and margin expansion.

The following chart illustrates the contrasting performance between the two segments:

Balance Sheet & Financial Position

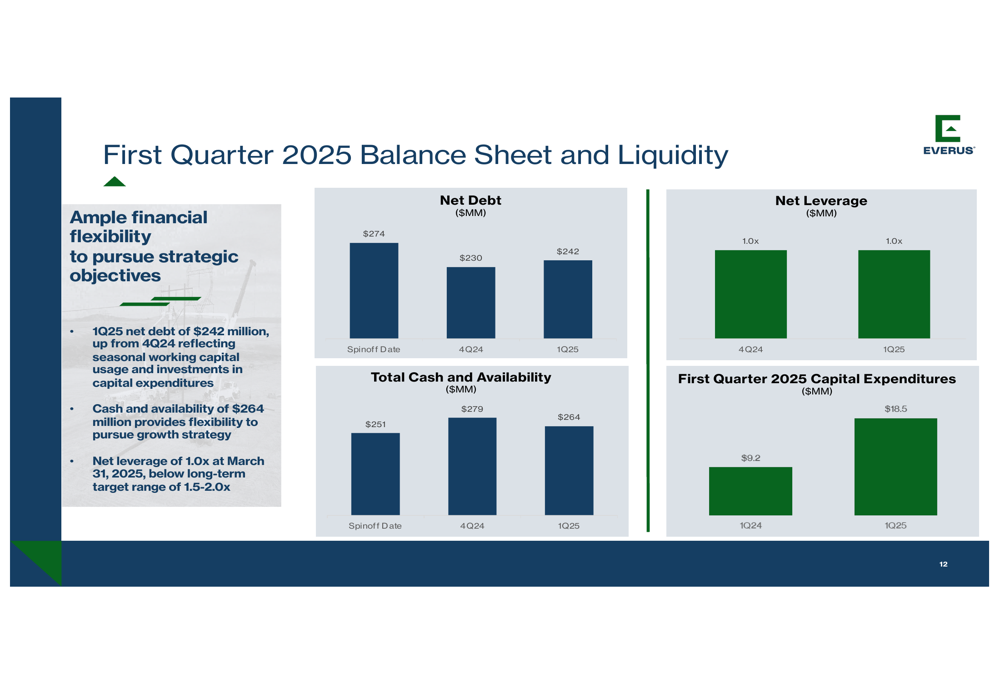

Everus maintained a strong financial position in Q1 2025, with net debt of $242 million and total cash and availability of $264 million. The company’s net leverage ratio stood at a conservative 1.0x, well below its long-term target range of 1.5x-2.0x, providing significant financial flexibility for future investments and potential acquisitions.

The company’s balance sheet strength is illustrated in the following chart:

Capital expenditures for the quarter totaled $18.5 million, representing approximately 2.2% of revenue, which aligns with the company’s long-term expectation of maintaining CapEx between 2.0% and 2.5% of revenue.

Free cash flow for the quarter was negative at ($8.1) million, compared to positive $15.4 million in Q1 2024. Management attributed this temporary cash flow reduction to project timing rather than any fundamental operational issues, emphasizing that the company expects cash flow to normalize throughout the remainder of the year.

Forward Guidance & Strategy

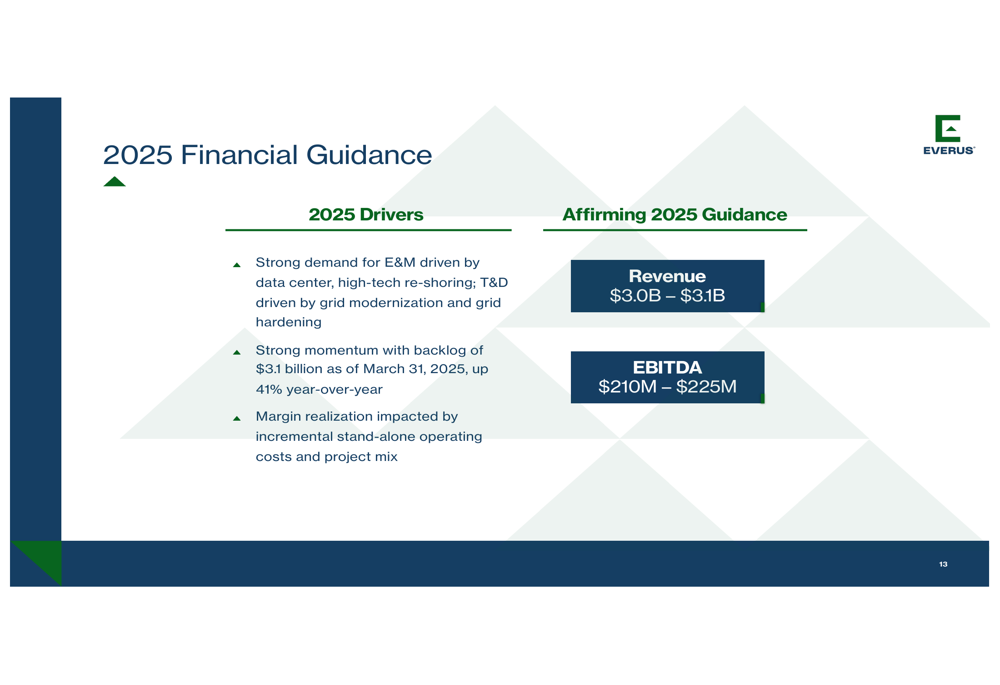

Everus affirmed its full-year 2025 guidance, projecting revenue between $3.0 billion and $3.1 billion and EBITDA between $210 million and $225 million. This guidance is supported by the company’s strong backlog and continued favorable end-market trends, particularly in data centers, high-tech manufacturing (driven by the CHIPS Act), and hospitality projects in Las Vegas.

The company’s financial guidance is summarized in the following slide:

Everus continues to execute its "4EVER" strategy, which focuses on four key pillars: Employees (attracting and retaining talent), Value (creating long-term shareholder value), Execution (safety and quality), and Relationships (customer focus). This framework underpins the company’s long-term financial expectations, which include 5-7% organic revenue CAGR and 7-9% EBITDA CAGR.

The company’s investment thesis highlights its multiple growth drivers, scaled national platform with market-leading local brands, and disciplined capital allocation approach, as illustrated below:

Conclusion

Everus Construction Group’s Q1 2025 results demonstrate robust growth across most key metrics, particularly in the E&M segment driven by data center construction. The company’s ability to maintain consistent margins while rapidly scaling operations speaks to its operational discipline and effective execution of its strategic framework.

With a strong backlog, healthy balance sheet, and favorable end-market trends, Everus appears well-positioned to meet its 2025 guidance and continue its growth trajectory. The market’s strongly positive reaction to these results suggests investors are confident in the company’s ability to capitalize on the ongoing infrastructure and technology construction boom.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.