Gold prices hovers near all-time high amid global political uncertainty

Introduction & Market Context

Faes Farma SA (BME:FAE) presented its first-half 2025 results on April 22, showing strong revenue growth across all business segments while experiencing a temporary decline in profitability due to strategic investments and one-off costs. The Spanish pharmaceutical company's stock is currently trading at €4.60, up 0.43% on July 24, and has shown resilience, trading near its 52-week high of €4.73.

Executive Summary

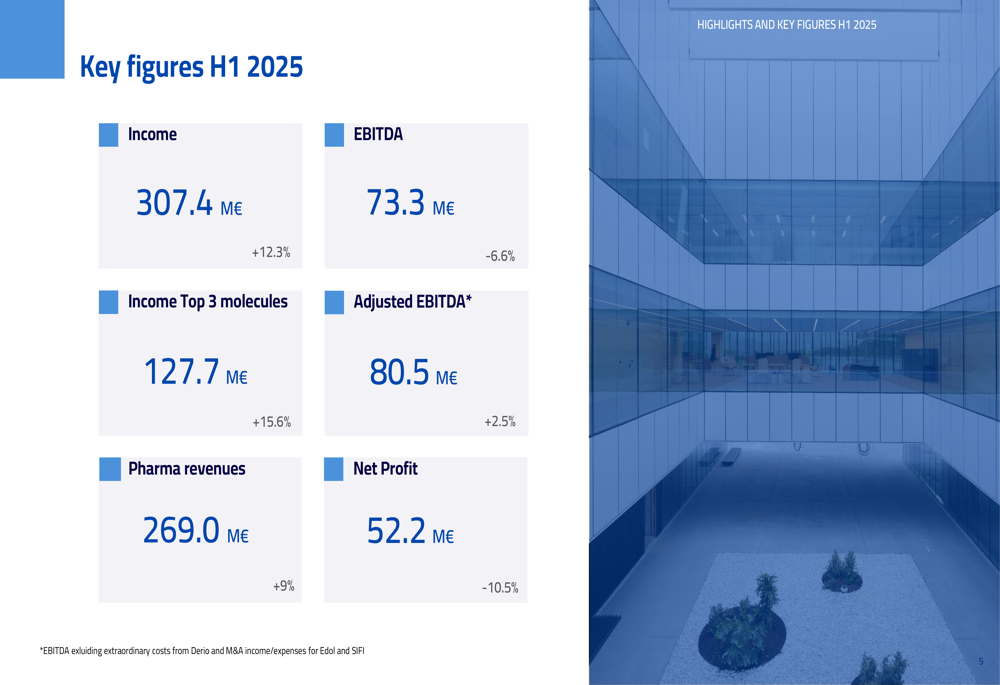

Faes Farma reported total revenues of €307.4 million for H1 2025, representing a 12.3% increase compared to the same period last year. This growth was driven by strong performance across all business areas, with particularly impressive results from its international operations and animal nutrition segment. However, the company's EBITDA declined 6.6% to €73.3 million, while net profit fell 10.5% to €52.2 million, primarily due to one-off costs related to the new Derio plant and M&A expenses.

When excluding these extraordinary costs, adjusted EBITDA showed a healthier 2.5% growth to €80.5 million, aligning with the company's full-year guidance.

As shown in the following key financial figures chart:

Detailed Financial Analysis

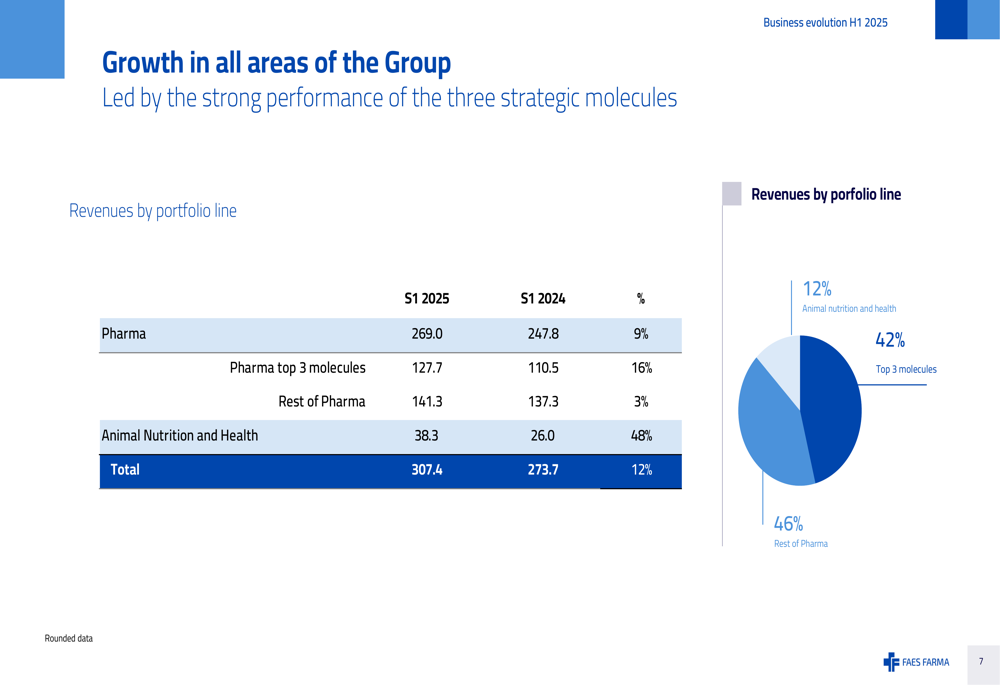

Faes Farma's revenue growth was broad-based across its business segments. Pharmaceutical (TADAWUL:2070) revenues increased 9% to €269.0 million, while the company's top three molecules generated €127.7 million, up 15.6% year-over-year. The animal nutrition and health division was particularly strong, with revenues surging 48% to €38.3 million.

The revenue breakdown by business area reveals the diversified nature of the company's growth:

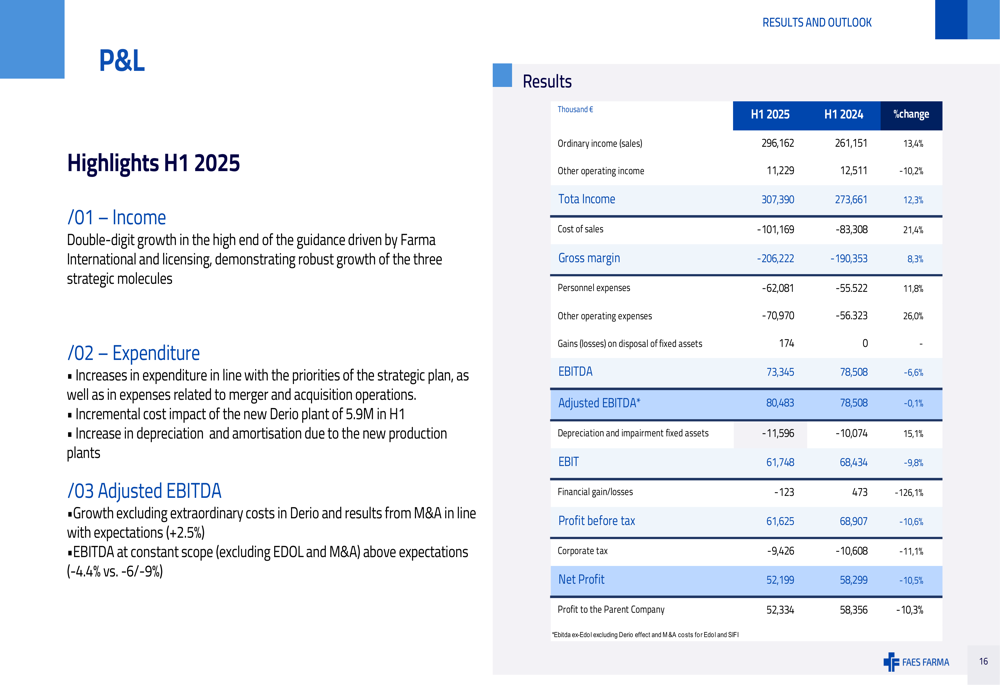

Despite the strong top-line performance, profitability metrics showed a decline. The company's P&L statement highlights that while ordinary income from sales increased 13.4% to €296.2 million, EBITDA fell 6.6% to €73.3 million and net profit decreased 10.5% to €52.2 million. This decline was primarily attributed to increased expenses in line with the strategic plan and the incremental cost impact of €5.9 million from the new Derio plant in the first half.

The following P&L highlights provide a comprehensive view of the company's financial performance:

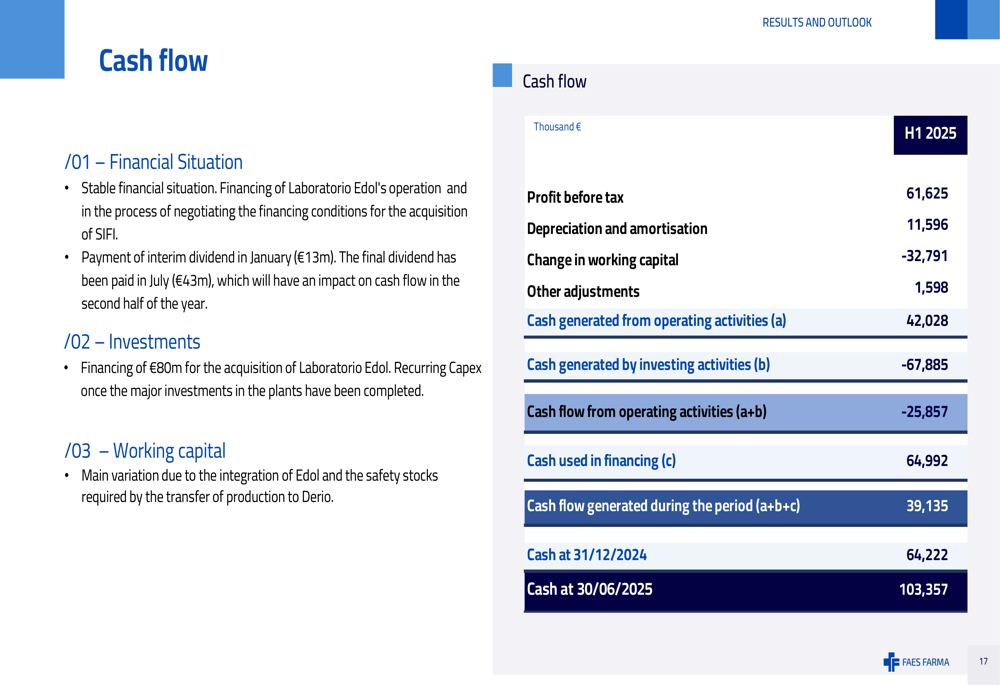

From a cash flow perspective, Faes Farma maintained a stable financial position despite significant investment activity. The company generated €42 million from operating activities but used €67.9 million in investing activities, largely related to the acquisition of Laboratorio Edol. Financing activities contributed €65 million, resulting in a net increase in cash of €39.1 million for the period. As of June 30, 2025, the company had €103.4 million in cash.

The cash flow analysis provides further details on the company's financial movements:

Business Segment Performance

Faes Farma's pharmaceutical business showed solid growth across different geographical regions. The Iberian market (Spain and Portugal) grew 5% to €115.8 million, with prescription sales in Spain increasing 8% while healthcare and consumer products declined 3%. Portugal showed stronger growth at 14%, primarily driven by prescription products.

International pharmaceutical operations were a significant growth driver, increasing 14% to €81.7 million. Latin America was particularly strong with 17% growth, led by Colombia (+32%), Ecuador (+33%), and Peru (+24%). The rest of the world markets grew 9%, with steady growth across all areas, particularly in Asia and MENA regions.

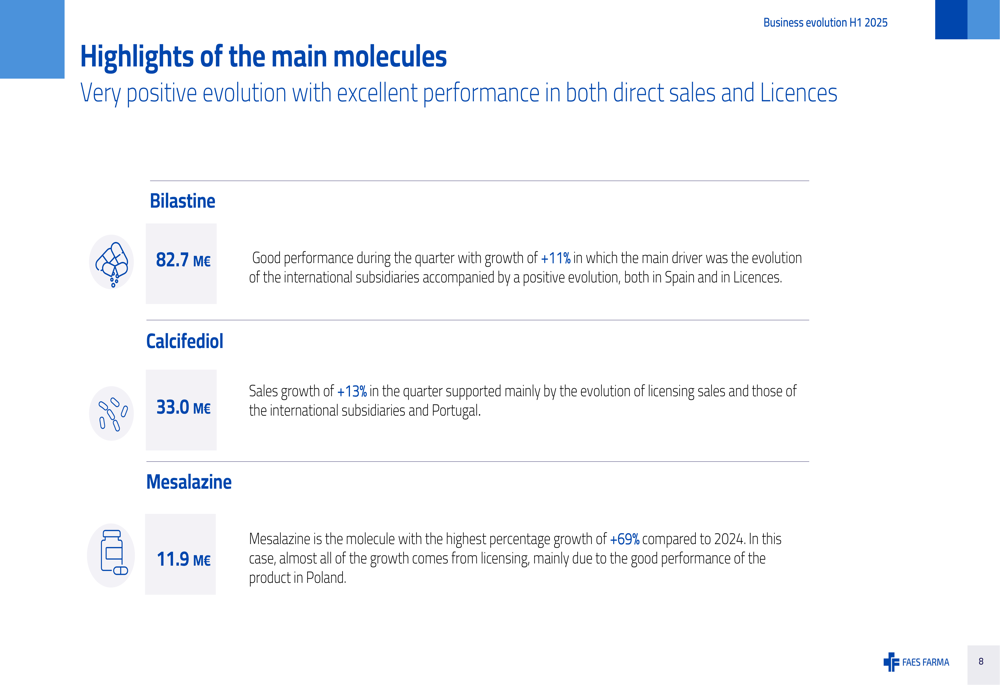

The company's licensing business also performed well, growing 13% to €72.8 million. Bilastine licenses increased 8%, while other licenses surged 37%, driven by strong sales growth in Poland and Nordic countries, as well as new Calcifediol launches.

The performance of Faes Farma's three main molecules was particularly noteworthy:

The animal nutrition and health division (FARM Faes) showed exceptional growth, with revenues increasing 48% to €38.3 million, primarily driven by the ISF business.

Strategic Initiatives & Outlook

Faes Farma highlighted several strategic developments during the first half of 2025. On the R&D front, the company secured approval for pediatric bilastine in Europe for children under 6 years old and completed the clinical phase of three studies in April. The evaluation of Mesalazine 1.5g gastroresistant tablets is expected to begin on August 4.

The company has been actively pursuing its expansion strategy through acquisitions. It secured €80 million in debt for the purchase of Laboratorios Edol and made progress in financing agreements for the SIFI acquisition. The contract for the SIFI acquisition has been signed and approved by shareholders.

Looking ahead, Faes Farma has introduced a new Strategic Plan for 2025-2030, although specific details were not provided in the presentation.

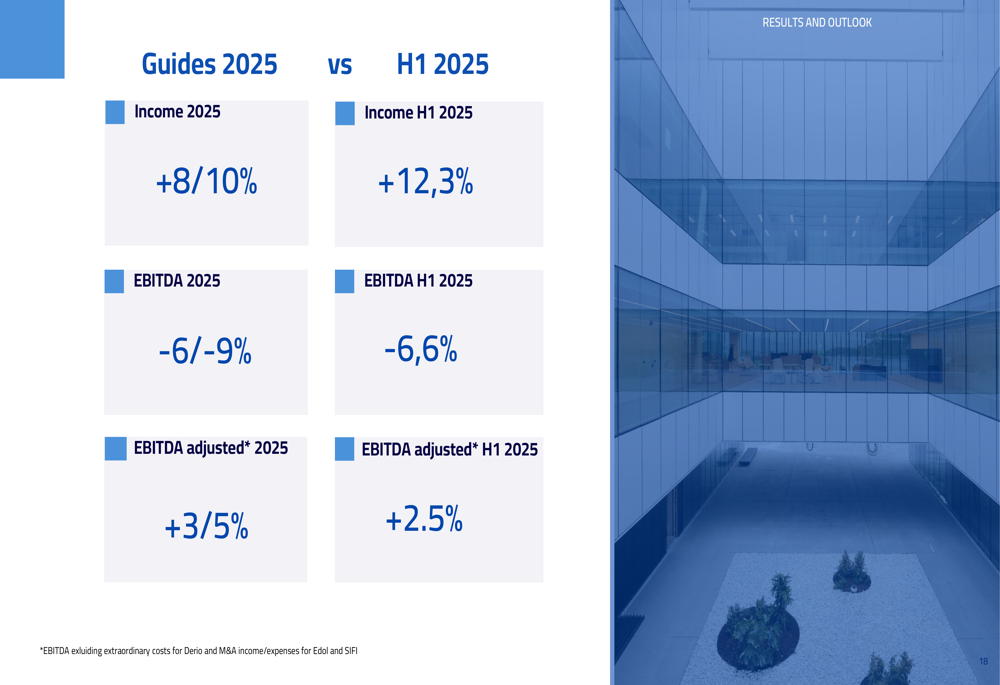

The company's H1 2025 performance is tracking well against its full-year guidance, as shown in the following comparison:

For the full year 2025, Faes Farma expects revenue growth of 8-10% (compared to 12.3% achieved in H1), EBITDA decline of 6-9% (6.6% decline in H1), and adjusted EBITDA growth of 3-5% (2.5% growth in H1). This suggests that the company anticipates its second-half performance to be broadly in line with the first half, with some potential moderation in revenue growth.

While the temporary impact on profitability from strategic investments and one-off costs is evident, Faes Farma's strong revenue growth across all business segments and geographies, coupled with its expansion initiatives, positions the company for sustainable long-term growth as these investments begin to yield returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.