German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

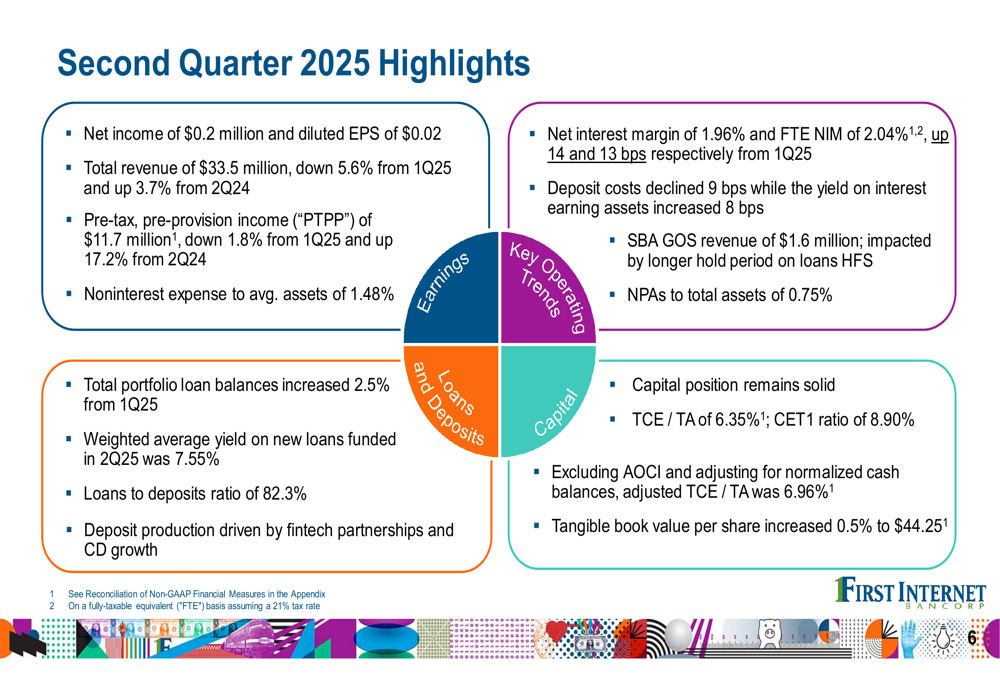

First Internet Bancorp (NASDAQ:INBK) reported minimal profitability for the second quarter of 2025, with net income of just $0.2 million and diluted earnings per share of $0.02, according to the company’s Q2 2025 presentation released on July 24. This represents a significant decline from the already disappointing Q1 2025 results, when the company reported EPS of $0.11 against analyst expectations of $0.76.

The digital banking pioneer continues to face headwinds from credit quality issues, particularly in its small business lending and franchise finance portfolios. Despite these challenges, the company showed improvement in net interest margin and provided guidance suggesting a stronger second half of the year.

INBK shares have struggled in 2025, currently trading at $27.38, down 1.01% in the most recent session and well below the 52-week high of $43.26, though above the 52-week low of $19.54.

Quarterly Performance Highlights

First Internet Bancorp’s second quarter results revealed mixed performance across key metrics. Total (EPA:TTEF) revenue was $33.5 million, down 5.6% from Q1 2025 but up 3.7% compared to Q2 2024. Pre-tax, pre-provision income (PTPP) was $11.7 million, representing a slight decrease of 1.8% from the previous quarter but a 17.2% increase year-over-year.

As shown in the following quarterly highlights chart, the company maintained a solid capital position with tangible common equity to tangible assets of 6.35% and saw tangible book value per share increase 0.5% to $44.25:

Net interest margin showed improvement, with GAAP NIM at 1.96% and FTE NIM at 2.04%, up 14 and 13 basis points respectively from Q1 2025. This positive trend in margin expansion was a bright spot in an otherwise challenging quarter.

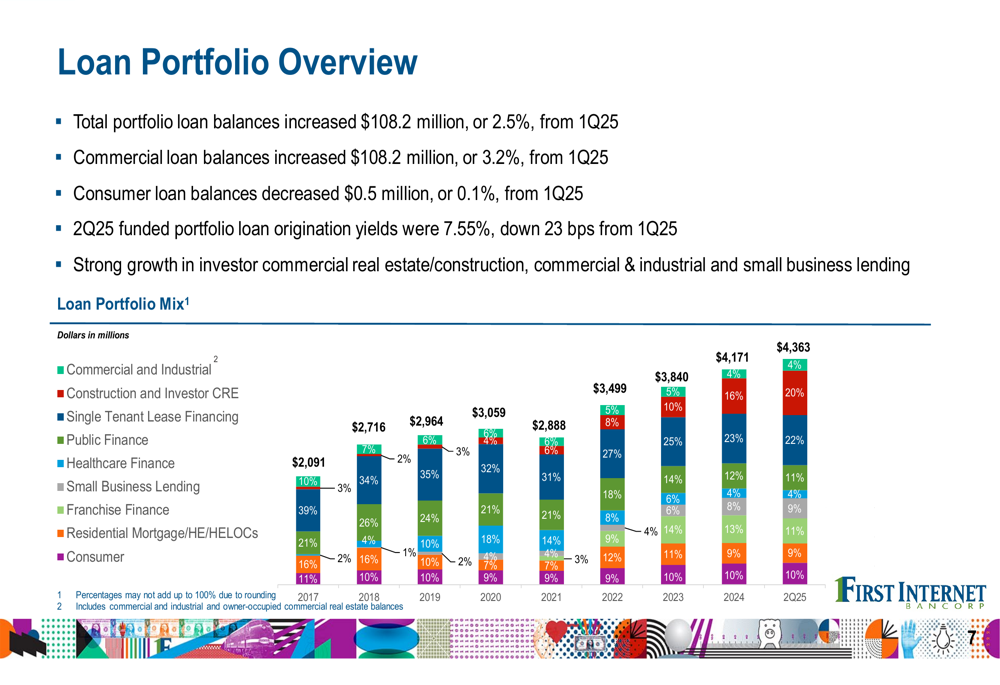

The loan portfolio grew by $108.2 million or 2.5% from Q1 2025, with commercial loans increasing by 3.2%. The company’s funded portfolio loan origination yields were 7.55% in Q2, down 23 basis points from the previous quarter.

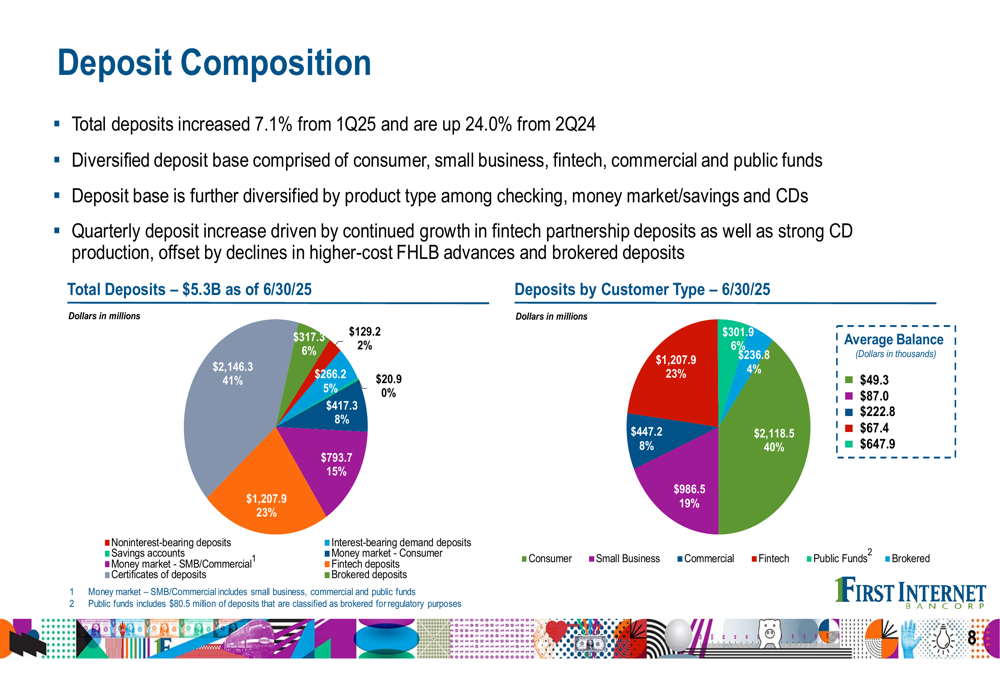

Deposit growth remained strong, with total deposits increasing 7.1% from Q1 2025 and 24.0% from Q2 2024. The company maintained a diversified deposit base across consumer, small business, fintech, commercial, and public funds segments.

Credit Quality Challenges

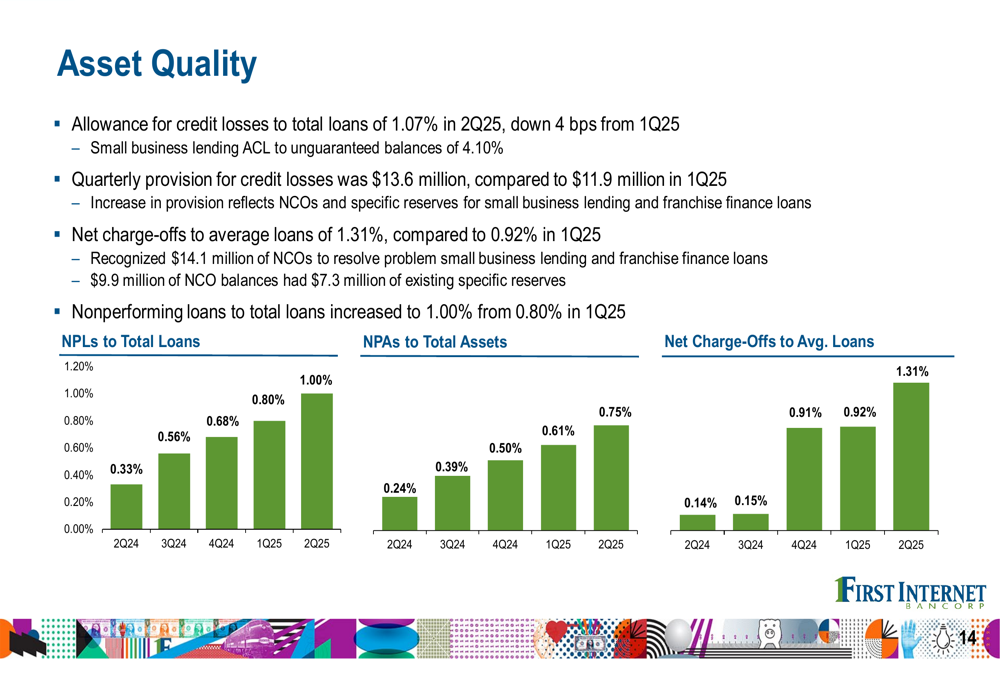

Credit quality issues continued to weigh heavily on First Internet Bancorp’s performance in Q2 2025. Net charge-offs reached $14.3 million, primarily from small business lending and franchise finance portfolios, despite having $7.3 million of specific reserves in place.

Nonperforming loans increased by $9.3 million from Q1 2025 to $43.5 million as of June 30, 2025, representing 1.00% of total loans, up from 0.80% in the previous quarter. On a more positive note, total delinquencies (excluding nonperforming loans) declined to 0.62% of total performing loans.

The following chart illustrates the deterioration in asset quality metrics:

In the franchise finance segment, the company moved $12.6 million to nonaccrual status in Q2 2025, with specific reserves of $4.5 million. However, management noted that no loans were on deferral as of June 30, 2025, down from 22 at the end of 2024, suggesting some stabilization in this portfolio.

Small business lending, which represents 11% of the total loan portfolio, continued to experience elevated nonaccrual loans and net charge-offs, particularly in the 2022-2023 vintages. Management indicated that refinements to approval criteria beginning in 2023 have led to improved performance, and nonaccrual loans appear to have plateaued. Delinquencies in this segment as of June 30, 2025, were down $2.4 million, or 23%, from December 31, 2024.

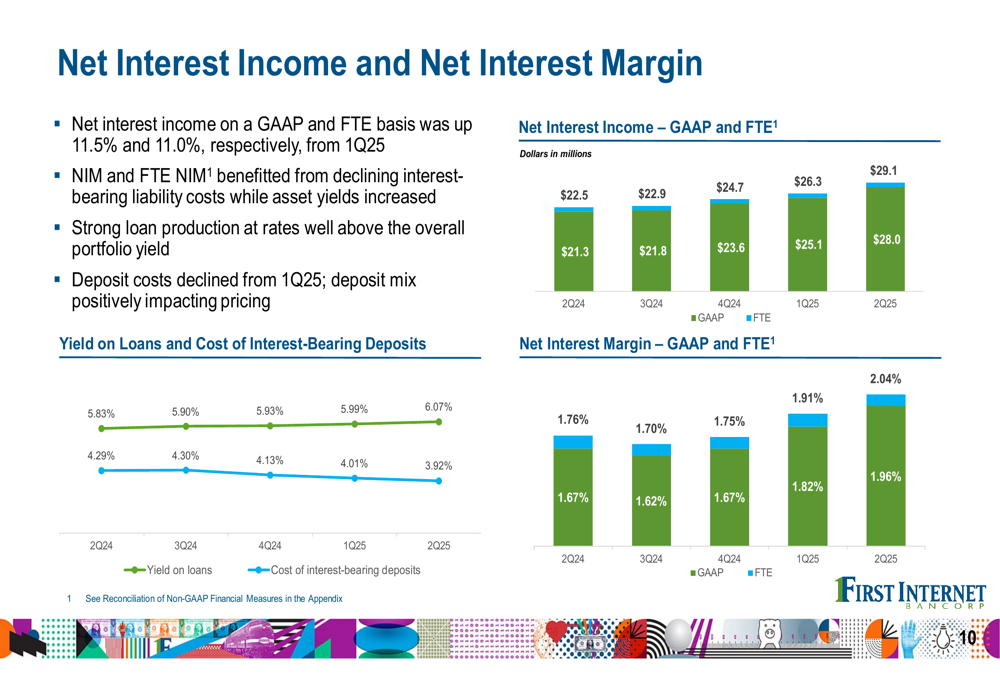

Net Interest Income Improvement

Despite the earnings challenges, First Internet Bancorp showed notable improvement in net interest income and margin. Net interest income on both GAAP and FTE bases increased by 11.5% and 11.0%, respectively, from Q1 2025.

The following chart shows the positive trend in net interest income and margin over the past five quarters:

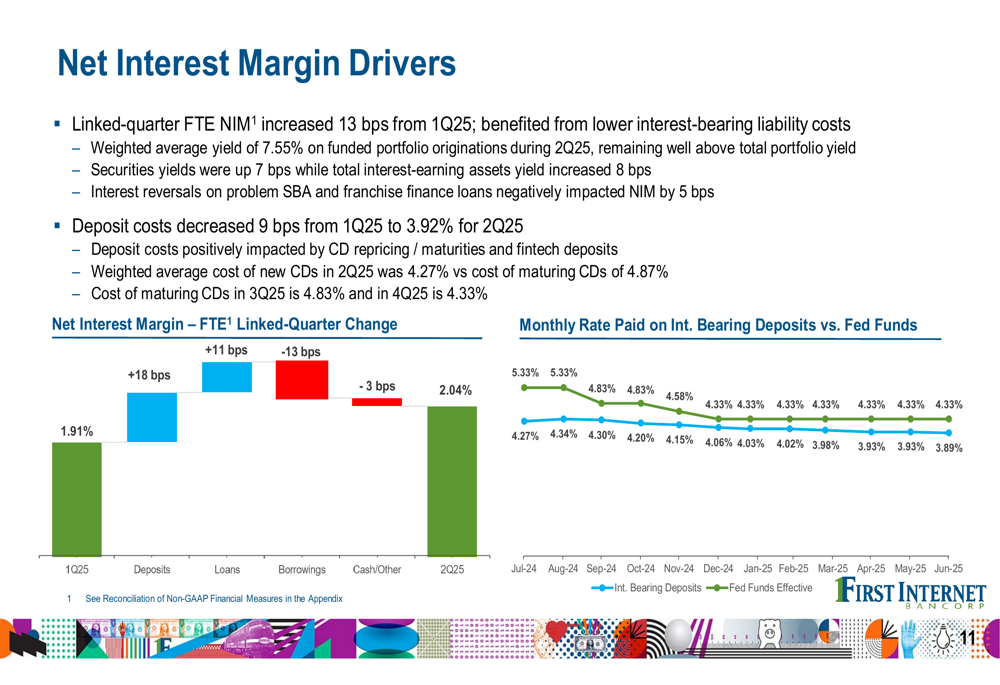

The linked-quarter FTE NIM increase of 13 basis points was primarily driven by declining interest-bearing liability costs. Deposit costs decreased 9 basis points from Q1 2025 to 3.92% for Q2 2025, contributing significantly to the margin improvement.

The net interest margin drivers chart below illustrates the factors affecting the quarterly NIM change:

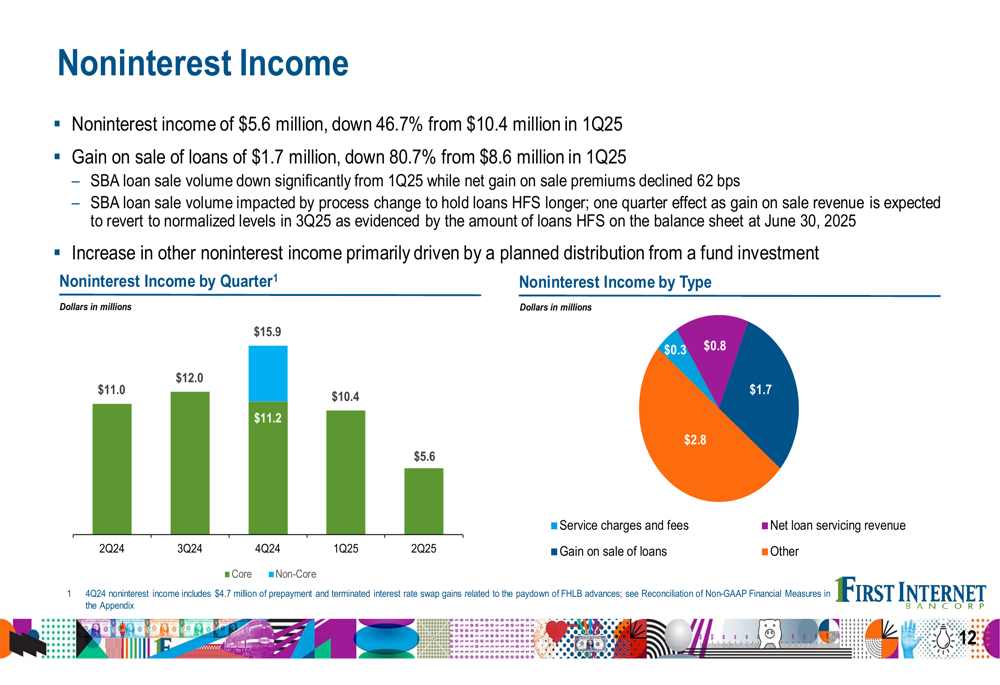

Strategic Initiatives

A key strategic decision that impacted Q2 2025 results was the deferral of secondary market sales of SBA (LON:SBA) loans. This significantly reduced noninterest income, which fell to $5.6 million, down 46.7% from $10.4 million in Q1 2025. Gain on sale of loans was just $1.7 million, down 80.7% from $8.6 million in the previous quarter.

The following chart shows the dramatic decline in noninterest income:

Management indicated that the company has begun to resume loan sales and expects SBA 7(a) loan sale activity to normalize in Q3 2025, which should boost noninterest income in future quarters.

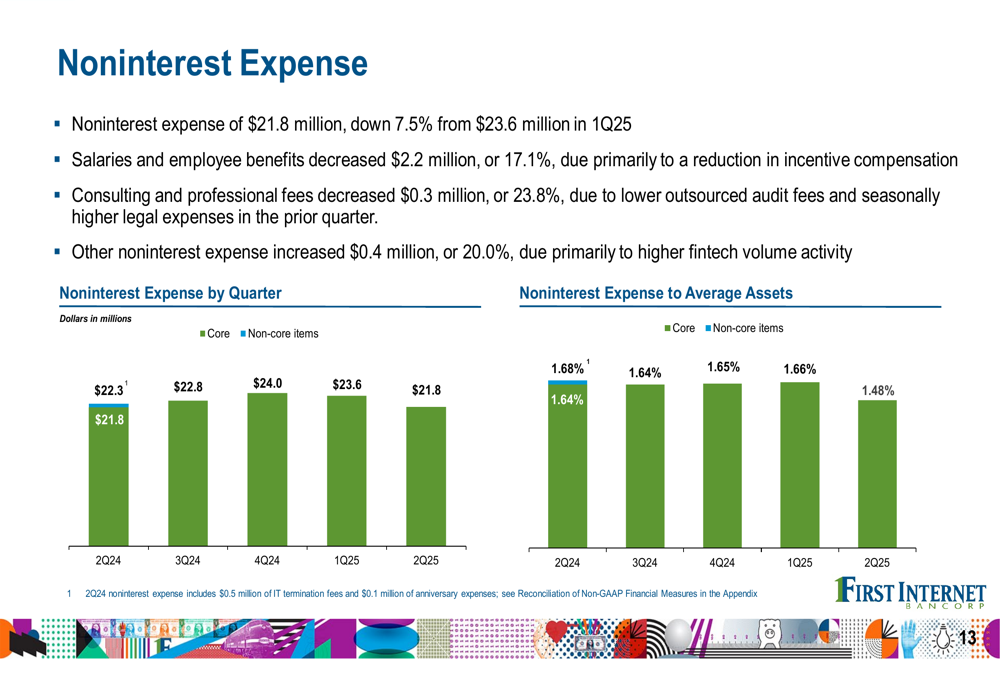

On the expense side, the company showed improvement with noninterest expense of $21.8 million, down 7.5% from $23.6 million in Q1 2025. Salaries and employee benefits decreased by $2.2 million, or 17.1%, reflecting cost control measures.

Forward-Looking Statements

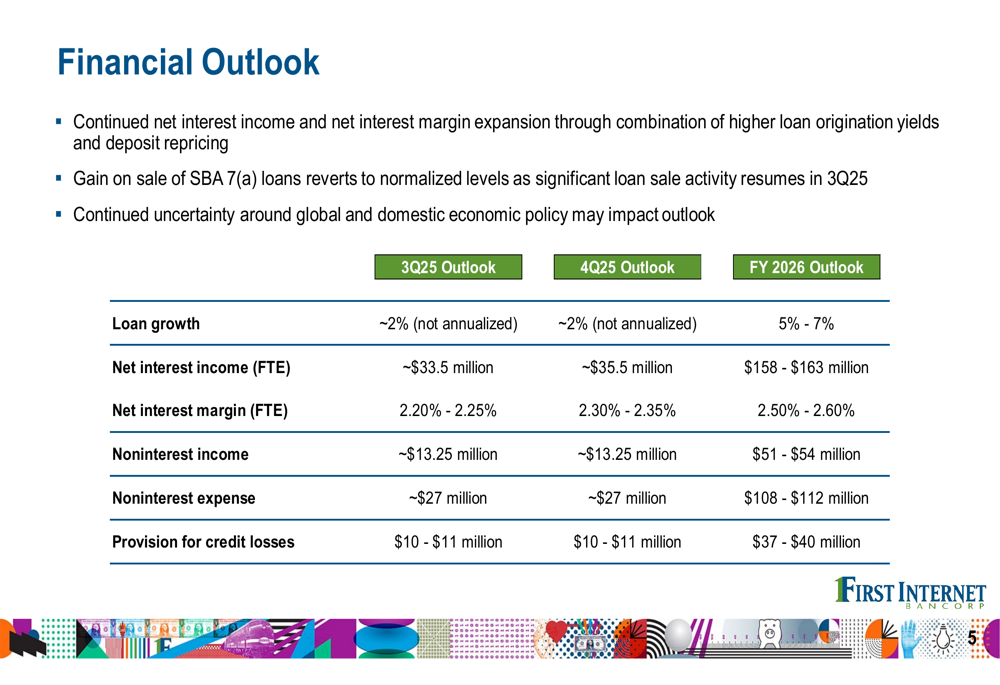

First Internet Bancorp provided a detailed financial outlook that suggests improving performance in the second half of 2025 and into 2026. The company projects continued net interest income and net interest margin expansion, with SBA 7(a) loan sale activity resuming in Q3 2025.

The financial outlook table below provides specific forecasts for key metrics:

Loan growth is projected at approximately 2% (not annualized) for both Q3 and Q4 2025, with 5%-7% growth expected for fiscal year 2026. Net interest income (FTE) is forecast to reach approximately $33.5 million in Q3 2025 and $35.5 million in Q4 2025, with full-year 2026 projections of $158-$163 million.

Net interest margin (FTE) is expected to continue its upward trajectory, reaching 2.20%-2.25% in Q3 2025 and 2.30%-2.35% in Q4 2025, with further expansion to 2.50%-2.60% projected for fiscal year 2026.

Noninterest income is forecast at approximately $13.25 million for both Q3 and Q4 2025, reflecting the expected resumption of SBA loan sales. However, provision for credit losses is projected to remain elevated at $10-$11 million for each of the next two quarters, indicating that credit quality challenges are expected to persist in the near term.

While management’s outlook suggests a path to recovery, the company acknowledges uncertainty around global economic policy that could affect these projections. Investors will likely be watching closely to see if First Internet Bancorp can execute on this guidance after two consecutive quarters of disappointing earnings results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.