Sun Valley Gold sells Vista Gold (VGZ) shares worth $2.16 million

Introduction & Market Context

First Internet Bancorp (NASDAQ:INBK) reported a significant net loss of $41.6 million for the third quarter of 2025, primarily driven by a strategic balance sheet restructuring that included the sale of $836.9 million in single tenant lease financing loans. The stock dropped 9.58% following the announcement, closing at $21.91, as investors reacted to the substantial loss and adjusted EPS of -$1.43, which fell well below analyst expectations of $0.63.

Despite the headline loss, the company highlighted several positive operational metrics in its presentation, including improved net interest margin and strong adjusted revenue growth, as it attempts to reposition its balance sheet for future profitability.

Strategic Balance Sheet Restructuring

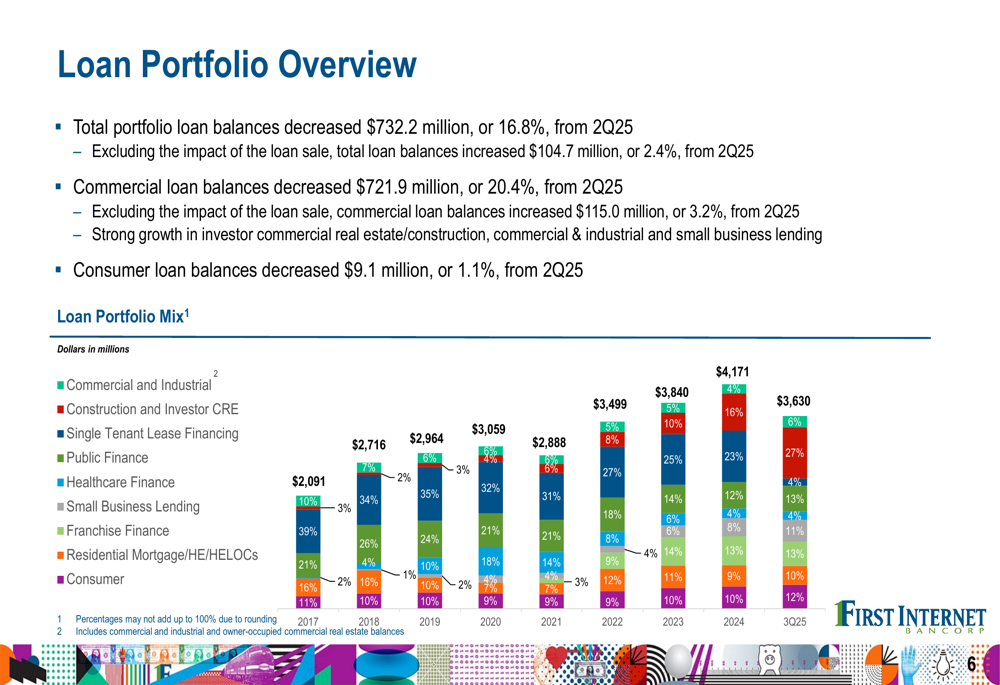

The centerpiece of First Internet’s third quarter was the completion of a major balance sheet optimization initiative through the sale of $836.9 million in single tenant lease financing loans. This transaction resulted in a $37.8 million loss but was presented as a strategic move to improve the company’s financial foundation and focus on higher-yielding lending segments.

As shown in the following loan portfolio overview, this sale dramatically transformed the company’s lending mix, reducing single tenant lease financing from a historically significant portion to just 5% of the total portfolio:

The company’s remaining loan portfolio now shows greater diversification across multiple segments, with construction and investor commercial real estate (16%), public finance (13%), and residential mortgage (13%) representing the largest components. This shift represents a significant strategic pivot for the bank, which had previously maintained a larger concentration in single tenant lease financing.

Quarterly Performance Highlights

Despite the substantial net loss, First Internet emphasized several positive operational metrics in its third quarter results. Adjusted revenue reached $43.5 million, representing a 30% increase over both the previous quarter and the same period last year. Adjusted pre-tax, pre-provision income grew to $18.1 million, up 54% from Q2 2025 and 64% from Q3 2024.

The following chart illustrates the key financial highlights for the quarter:

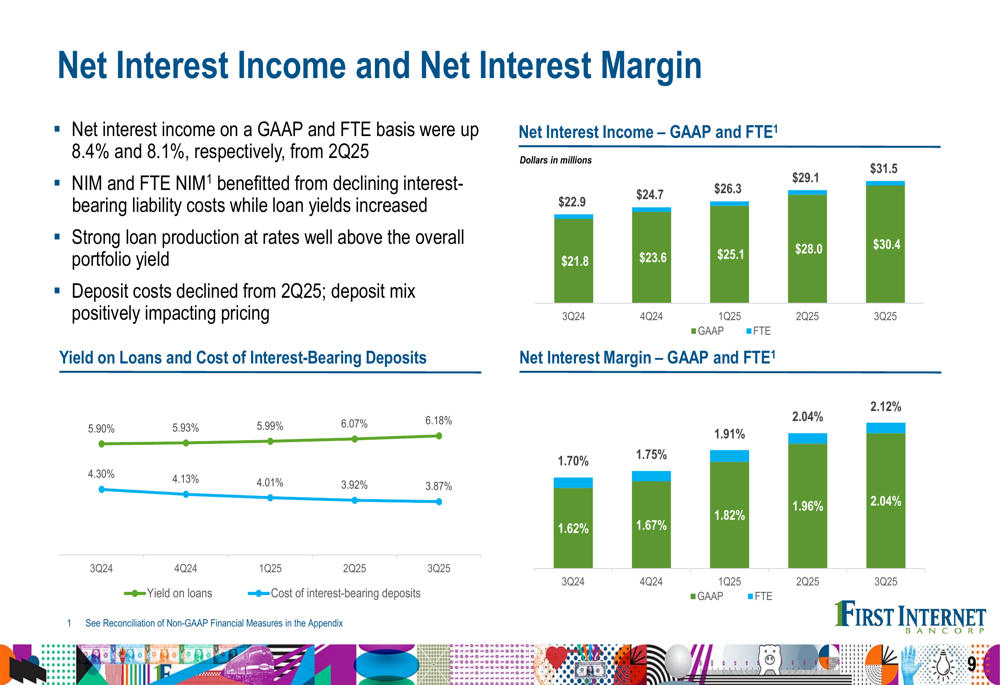

Net interest margin showed consistent improvement, reaching 2.04% on a GAAP basis and 2.12% on a fully taxable equivalent (FTE) basis, both increasing 8 basis points from the previous quarter. This positive trend in margin expansion has been consistent over the past five quarters, as shown in the following chart:

The margin improvement was driven primarily by lower interest-bearing liability costs, with deposit costs decreasing 5 basis points to 3.87% while the yield on interest-earning assets increased 3 basis points. New loan originations during the quarter carried a weighted average yield of 7.50%, well above the total portfolio yield.

Asset Quality and Credit Metrics

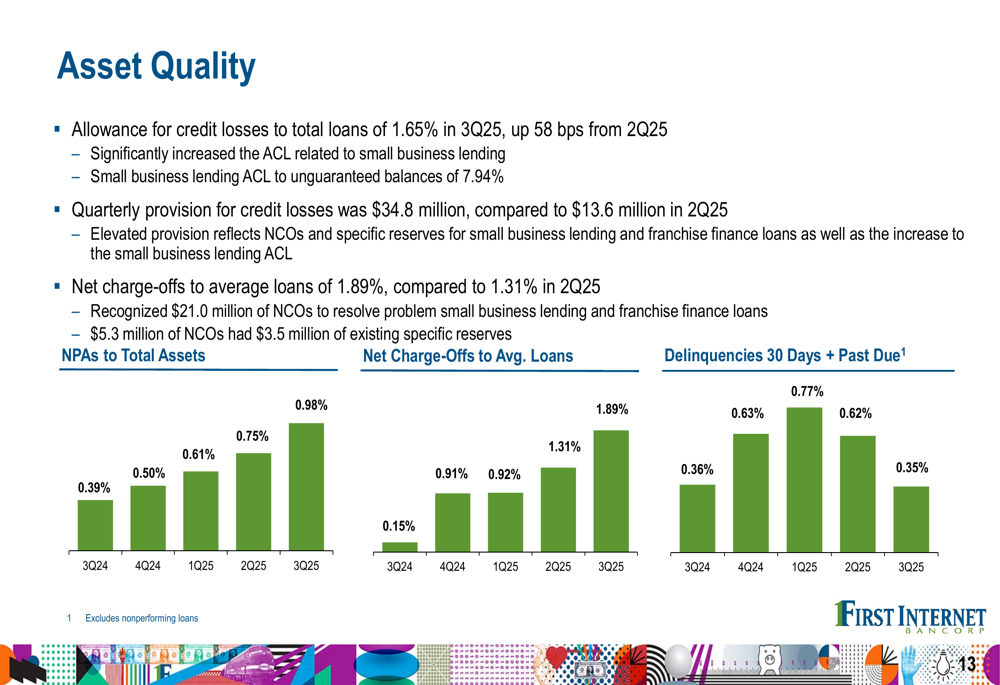

First Internet’s presentation highlighted "improving asset quality" as a key business achievement, particularly noting a 79% reduction in franchise finance delinquencies. However, broader asset quality metrics showed some deterioration, with non-performing assets to total assets increasing to 0.98% and net charge-offs to average loans rising to 1.89%.

The following chart illustrates these asset quality trends:

The allowance for credit losses to total loans increased 58 basis points to 1.65% in Q3 2025, and the quarterly provision for credit losses was $34.8 million, compared to $13.6 million in the previous quarter. These metrics suggest ongoing credit challenges despite the company’s efforts to improve its risk profile.

Deposit Strategy and Liquidity Position

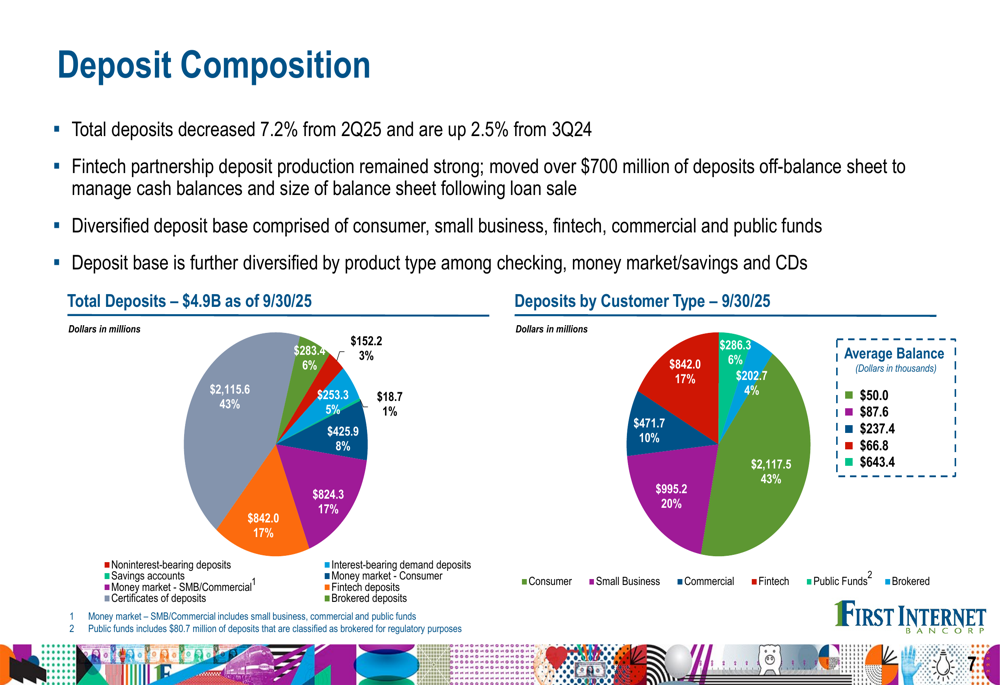

First Internet’s deposit strategy continues to leverage its Banking-as-a-Service (BaaS) model and fintech partnerships to drive liquidity. Total deposits decreased 7.2% from the previous quarter but remained 2.5% higher than the same period last year. The company noted that it moved over $700 million of deposits off-balance sheet to manage cash balances following the loan sale.

The following chart shows the company’s deposit composition:

Noninterest-bearing deposits represent 43% of total deposits, providing a stable and cost-effective funding base. The company’s deposit mix by customer type shows diversification across consumer (20%), small business (10%), commercial (43%), fintech (17%), public funds (6%), and brokered deposits (4%).

Cash and unused borrowing capacity totaled $2.9 billion as of September 30, 2025, representing 180% of total uninsured deposits and 216% of adjusted uninsured deposits, highlighting the company’s strong liquidity position. The loans-to-deposits ratio remained favorable at 73.9%.

Capital Position and Book Value Impact

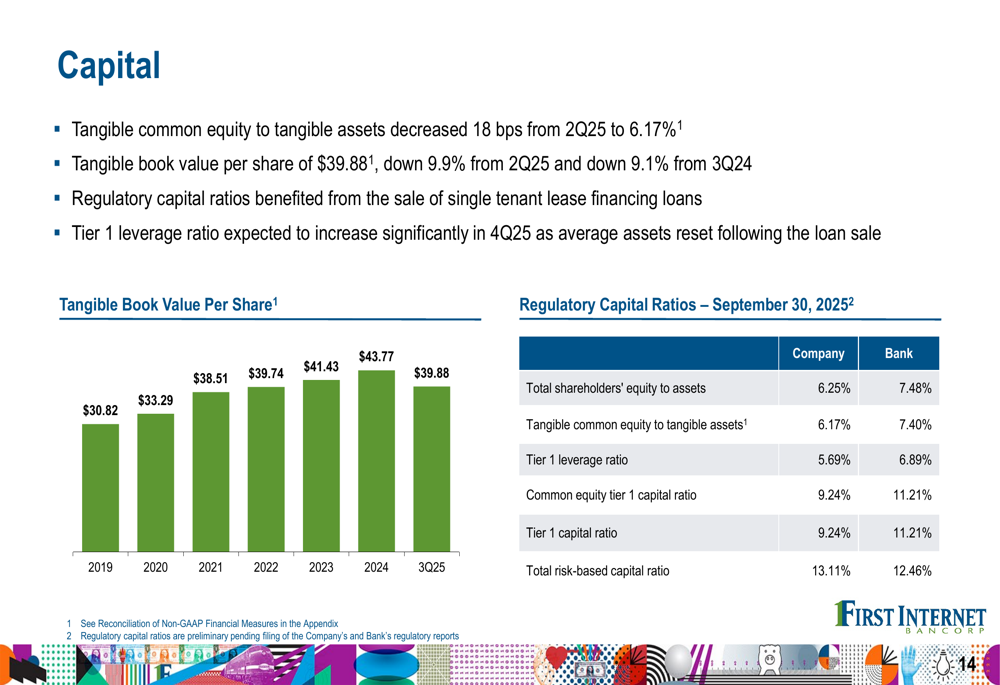

The strategic loan sale had a significant impact on First Internet’s capital position and book value. Tangible book value per share decreased 9.9% to $39.88 from the previous quarter and was down 9.1% from the same period last year, as shown in the following chart:

Despite this decline, the company maintained solid regulatory capital ratios, with a common equity tier 1 capital ratio of 9.24% and a total risk-based capital ratio of 13.11%. Tangible common equity to tangible assets decreased slightly to 6.17%, down 18 basis points from the previous quarter.

Forward-Looking Statements

Looking ahead, First Internet projects loan balance growth of 4-6% for Q4 2025 and expects net interest margin to improve to between 2.4% and 2.5%. The company anticipates net interest income of $32.75-$33.5 million and continued yield enhancement in its loan portfolio.

Management expressed increased conviction in the company’s long-term outlook, citing its strong liquidity position as a foundation for profitable growth. The company’s focus areas include construction and investor commercial real estate, where it sees strong loan pipelines, and continued expansion of its Banking-as-a-Service model through fintech partnerships.

During the earnings call, CEO David Becker emphasized the company’s consistent delivery of "strong net interest income improvements over the last 12 to 18 months" and highlighted the impact of AI-driven analytics on the company’s loan portfolios. President and COO Nicole Lorch noted the impact of inflation on the company’s business, particularly on small businesses, which could present challenges in the coming quarters.

While the strategic balance sheet restructuring resulted in a significant short-term loss, First Internet Bancorp’s presentation emphasized its efforts to build a stronger foundation for sustainable profitability through improved net interest margin, diversified lending focus, and strategic fintech partnerships.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.